Talk like a Federal Reserve Governor!

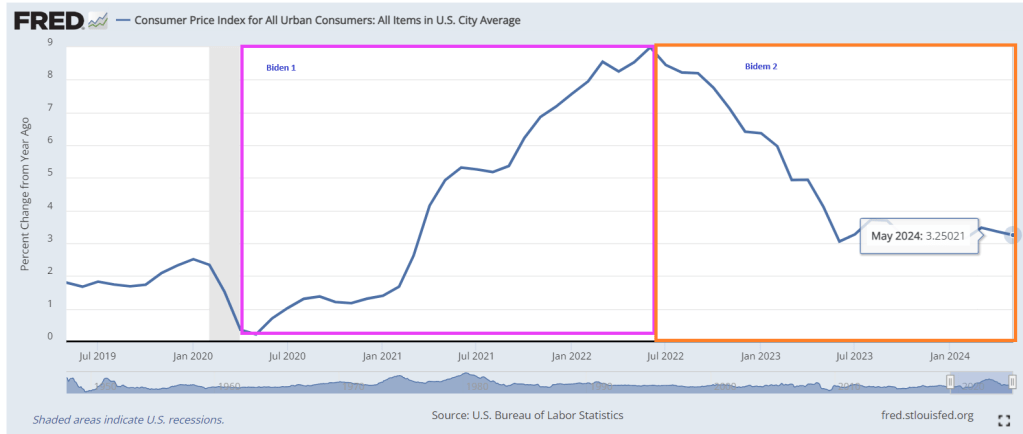

A number of pominent cheerleaders (economists) have come out before CNN debate to claim that another Trump Presidency will generate even worse inflation than it has under Biden. Really? Before Covid struck in 2020, the last CPI YoY reading for Trump was only 2.34%. It rose to 9% YoY under Biden in June 2022. How did this happen? Federal binge spending and reckless Federal Reserve monetary policy.

The Nobel Prize -winning “economists” seem to have forgotten the unprecented money printing and interest rate suppression when Covid srtuck in 2020.

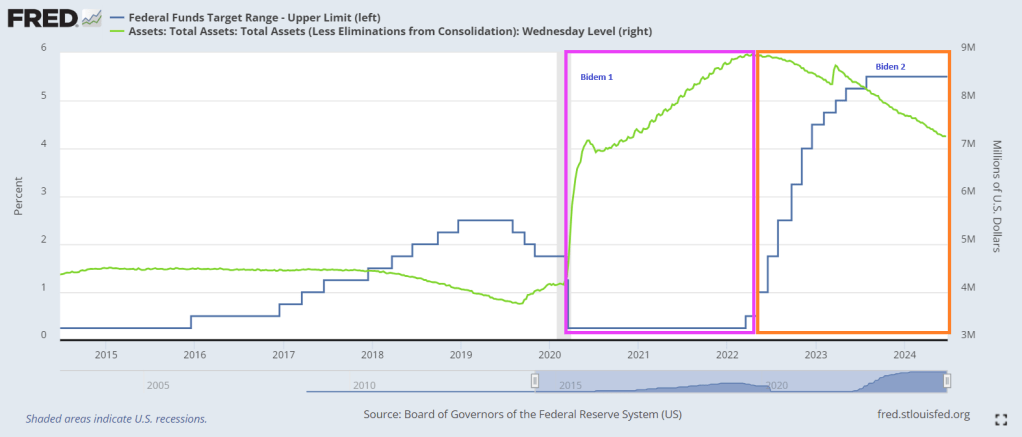

Of course, inflation soared after the massive Covid stimulus in 2020. It kept rising until The Fed started raising their target rate in 2022. But The Fed’s balance sheet remains elevated (green line).

In terms of M2 Money printing of Federal Reserve currency, M2 Money expanded greatly with Covid and continued to grow until 2022. Then M2 Money growth slowed as The Fed raised rates in 2022. Inflation started to decline (but price levels remained high) after The Fed raised rates and M2 Money growth stalled.

From Zero Hedge: With a Trump presidency looking virtually assured after Biden’s cataclysmic debate fiasco, the “expert” fear-brigade that defined Trump’s first term in office is out in full force, and last week 16 Nobel Prize-winning economists (not to be confused with 51 former spies) – who have previously been silent as a group over the brazen bull of inflation cooking Americans alive under President Biden, have teamed up for a pre-election collab to let us know that former President Trump ‘could stoke inflation if he wins.’

And while it is obvious that this latest attempt by the “expert class” to influence voters is nothing but more pro-Biden propaganda, the question of inflation’s fate under a Trump administration is certainly pertinent, especially now that the Fed’s new inflation target is effectively 3%. We ourselves took a look at this last week in “What Will Happen To Inflation Under A Trump Presidency“, and observed that it does make intuitive sense that if tariffs ramp up – as Trump has promised they will in bilateral China trade – then some inflationary impulse is almost certain to follow. This is how Rabobank’s strategist Philip Marey put it:

Biden’s recent decision to keep the Trump tariffs on China and add “strategic” tariffs are clearly part of the election campaign where Biden and Trump are outbidding each other to show that they want to bring jobs back to America. Although a Biden baseline would show lower inflation than a Trump baseline, and more Fed rate cuts, it is important to stress that both presidents will continue to follow a protectionist course, which means that inflation in both scenarios is higher than under a hypothetical free trade president. The same is true for Fed policy rates. When it comes to trade policy, both Republicans and Democrats have become protectionist, especially regarding China. This will lead to higher inflation and could slow down economic growth, especially if other countries retaliate against the US.

Again, there is nothing controversial about this view: it is the definition of conventional wisdom. But what is conventional wisdom is once again dead wrong as it has been for much of the past 15 years?

That is the hypothesis of none other than one of the most outspoken and contrarian Wall Street strategists, BofA’s Michael Hartnett, who in his latest Flow Show writes that far from inflationary, any new trade war launched by Trump will be a substantially deflationary event.

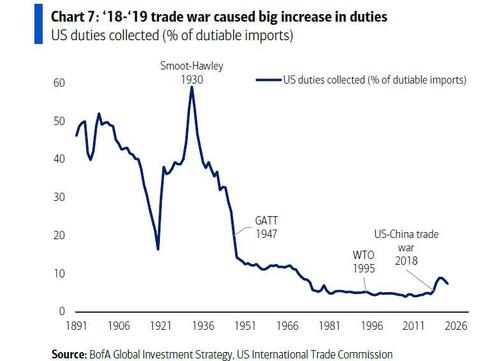

As Hartnett reminds us, the US-China trade war in 2018-2019 saw the largest rise in % of US duties collected since 1930 Smoot-Hawley.

And while Trump tariffs were maintained and even extended by Biden – something the 16 Nobel prize winners failed to mention – Hartnett warns that new tariffs in the next 12 months would be deflationary not inflationary, and here’s why: the Q1 2018 trade war backdrop was strong macro (ISM @ 60) and low rates (Fed funds @ 1.25%)… but the backdrop now for the next big rise in tariffs under Trump in the first half of 2025 is ISM <50 and Fed funds @ 5.5%, and most importantly, the global economy now is much weaker than in 2018.

As a result, unlike 7 years ago, it will take far less to push the world into a deflationary recession, one where China will not be able to push the global economy higher, and Trump’s new tariffs will be just the straw that breaks inflation’s back. Of course, it will also trigger a brutal global recession but at this point an economic slowdown may be welcome by an American population that is sick of seeing grocery prices rose by double digits every few months.

Incidentally, not much else will change, because the reality is that for much of the past decade the uniparty has been in control, and no matter how you slice it, both Biden and Trump (even before covid) are responsible for the 2 largest deficits of the past 80 years…

… yet inflation is now the #1 issue for electorate – which means “drunken sailor” spending by the government will mostly be frowned upon – and indeed US government spending is finally starting to ease off, down 2% on a rolling 12-month basis, with Hartnett showing in the next chart that fiscal excess wanes “bigly” in Year 1 of a new Presidential cycle:

Furthermore, while an election “sweep” scenario is bond negative, a presidential “split” with Congress is positive, and the latest probablities cited by Hartnett are: Trump/split Congress 40%, Biden/split Congress 25%, Trump sweep 25%, Biden sweep 10%.

Some more details from the Hartnett note:

- US government is a $6-7tn beast, 3rd largest GDP in world and been growing >8% p.a. past few years;

- While most expect US fiscal to remain stimulative post-election (e.g. CBO sees US deficit >5.5% GDP next 10 years), US government spending -2% on 12-month rolling basis;

- 1st year of new Presidential cycle typically sees big slowdown, and most important electoral bloc in 2024 (65mn Gen Z & Millennial votes set to outnumber 50mn Baby Boomers) says most important issue is inflation, followed by healthcare and housing

Hartnett’s Bottom line: inflation not a vote-winner in ’24…

…and so absent sweeps and big tax cuts, the BofA CIO cautions that “fiscal no longer cyclical negative for bonds.”

To summarize: if Hartnett is right on his two assumptions, namely i) the next trade war with China will be deflationary and ii) the result of the election will see a big drop in government spending and thus, inflation, the obvious trade would be to buy deeply discounted bonds, something which Hartnett has been pitching for the past few months.

But wait there’s more…. in fact, three reasons more why Hartnett is extremely bullish on bonds in his near and medium-term outlook.

- The first has to do with his current view of the investing landscape and that investors are “long the rich sectors” (Magnificent 7) and “short the poor sectors (e.g. REITs/small cap/ARKK); and with cyclical “middle class sectors” (industrials, homebuilders, resources, Nikkei, DAX) rolling over, the MSCI ACWI equal-weighted index is now down 0.6% YTD…” that to Hartnett is all positive for bonds.

- The second is that Asian currencies (Japan yen, China renminbi) are close to multi-decade lows; And in a world where a strong US dollar dominates (and makes Asian exports super-competitive), coupled with far less fiscal stimulus (after the election) and no rate cuts by the Fed, US manufacturing will suffer (note manufacturing states of PA, WI, MI will decide election). That to Hartnett is also positive for bonds, and negative the US dollar in H2.

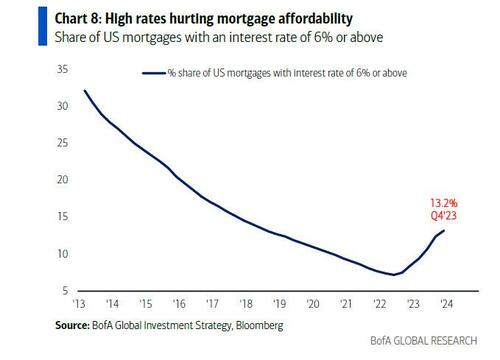

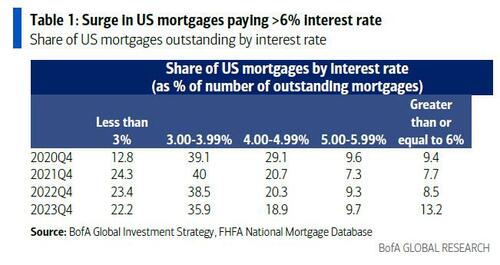

- The third and final reason has to do with housing, to wit: “long homebuilders” has been the “anti” hard-landing/recession trade past 9 months; well the XHB is down 10% from Mar’24 peak with housing starts at 4-year low + rising impact of rates on mortgage affordability (estimated that ~15% of the more than 50mn US mortgages have a rate at or above 6%…up from 13% in Q4’23)

Now for the beleagured residential mortgage market.

And since lower homebuilders when rates are dropping (or about to drop) signals labor market weakening, any payroll confirmation of a weak US labor market (i.e. payrolls below 125-150k) would send 30Y TSY yields tumbling below 4%. Investors’ reaction would be a weak US dollar, maintenance “long Nasdaq, short Russell” trade, as well as further downward pressure in coming weeks on “middle class” cyclicals. As to what could burst the current tech/AI/semi bubble, Hartnett writes that a “major rotation from mega-cap tech “rich sectors” to small-cap “poor sectors” awaits unambiguous “hard landing” evidence, and “fast & furious” Fed cuts, is what is needed for asset allocators to cut stocks to go long bonds.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.