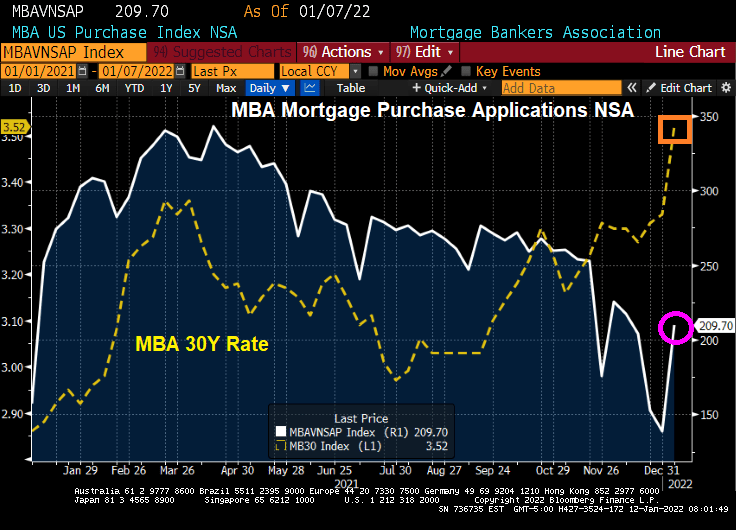

US mortgage purchase applications rose 51.2% from previous week, despite mortgage rates rising.

Of course, the first weeks of most years see large increases in mortgage purchase applications.

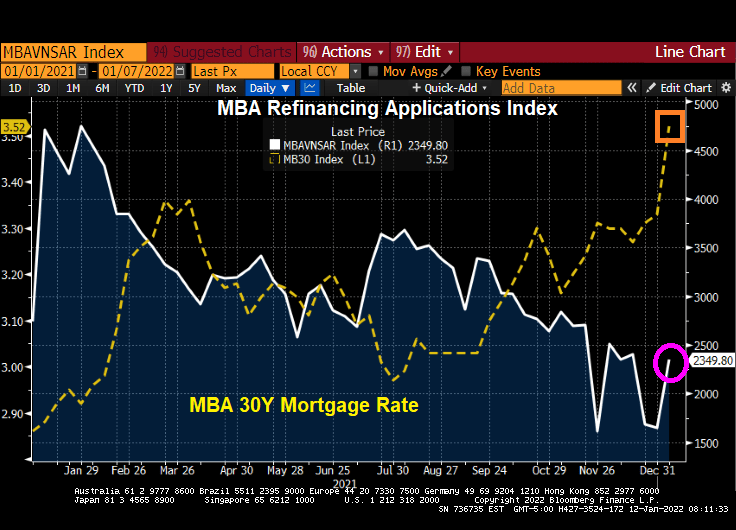

Mortgage refinancing applications were up 42.77% from the previous week.

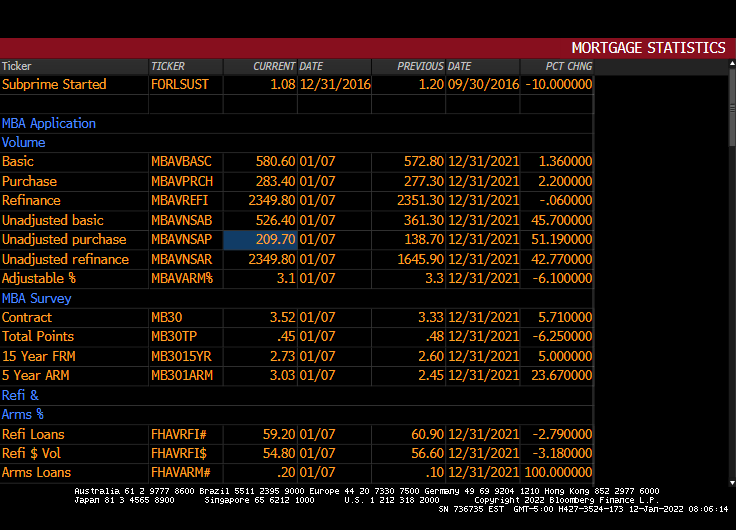

Here is the MBA data.

So, the US housing market is off to a fast (and hot) start to 2022.

You must be logged in to post a comment.