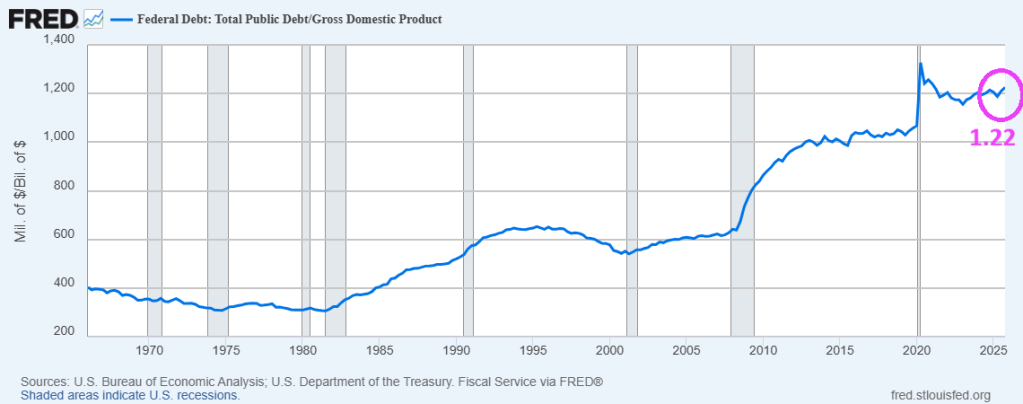

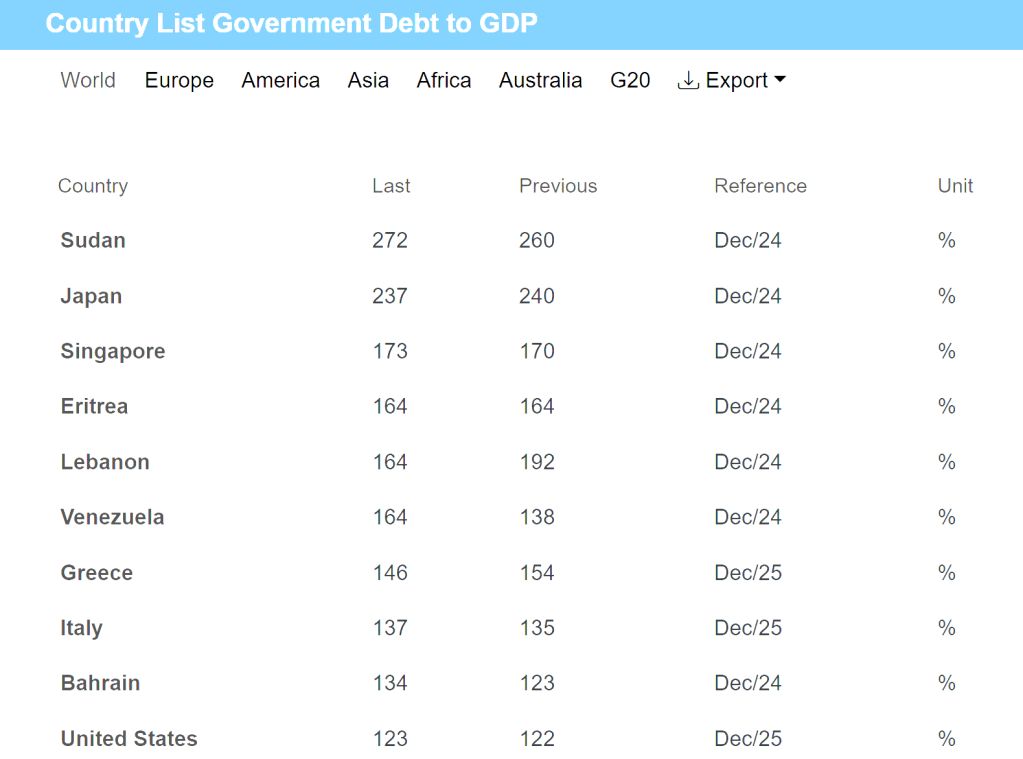

It used to be that a debt-to-GDP (Gross Domestic Product) ratio above 1.0 would be disastrous. Yet, the US Debt-to-GDP ratio rises during and after most recessions. Why? The old Keynesian model called for increased government spending and debt to pull the country out of a recession. But the Keynesian model called for debt to be repaind after the recession ended. But after most recessions, the Federal government keeps spending and borrowing. Following the Covid outbreak of 2020, the US debt-to-GDP ratio exceeded 1.0 and has remained fairly constant since.

As of today, the US Federal debt load is $39.204 trillion while GDP is $32.090 trillion resulting in a debt-to-GDP ratio of 1.22.

The leader in the debt-to-GDP race is … Sudan! Followed by Japan and Singapore.

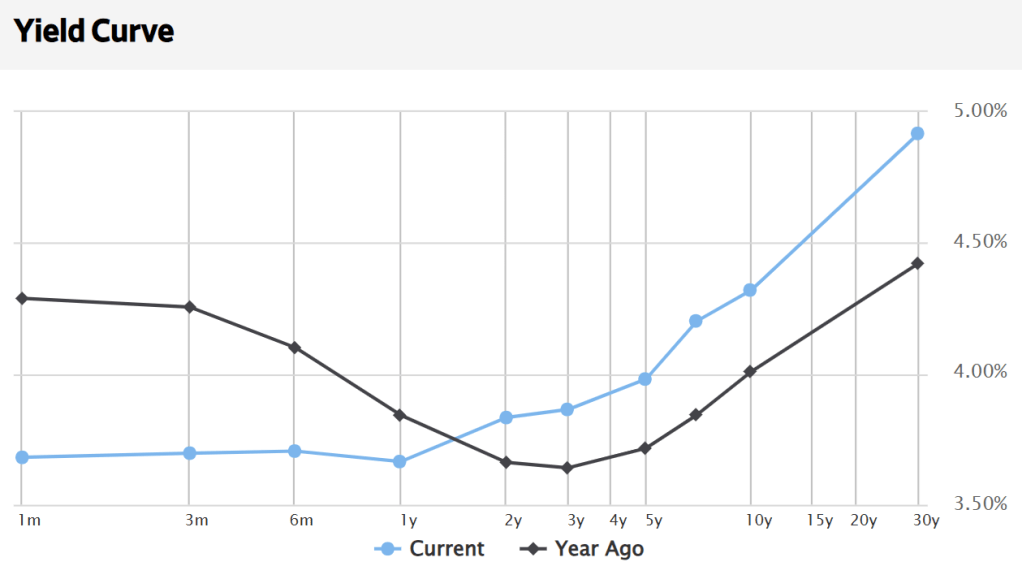

Trump’s threats of bombing Iran back to the stone age continues. But the impact on Treasury yields is interesting. As the US economy continues to grow, the US Treasury curve takes on the familiar upward slope. With rising long rates. Particularly when compared to the negative humped yield curve of a year ago.

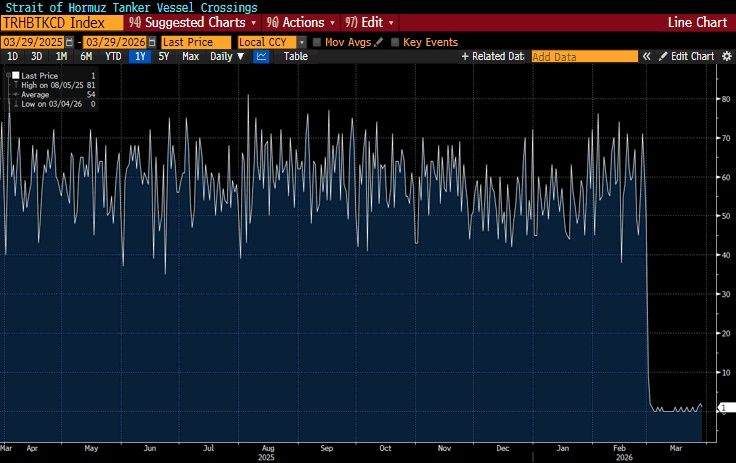

The Strait of Hormuz, a choke point for Middle East crude oil delivery to the rest of the world, has witnessed vessel crossings grinding to a near halt.

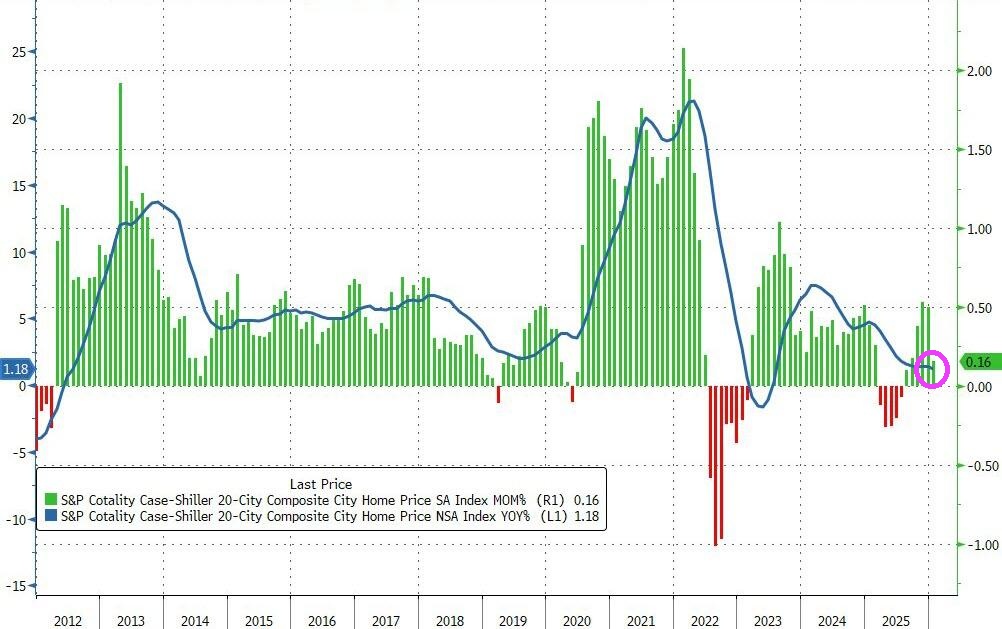

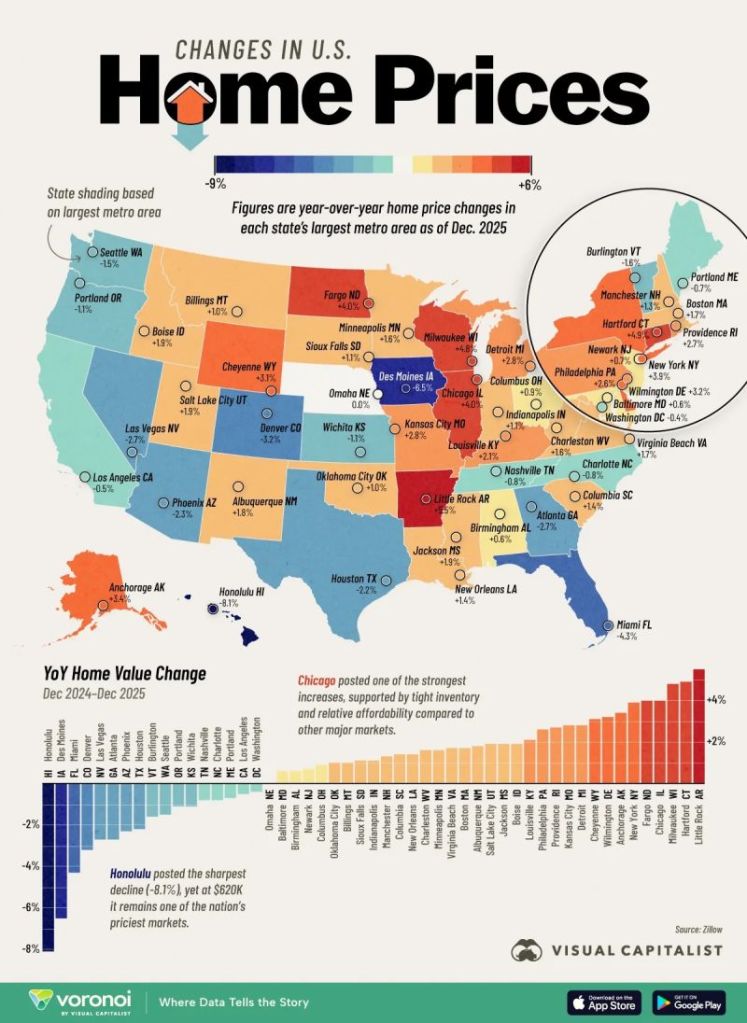

We are seeing mean reversion in home prices in red cities and blue cities.

The price of homes in America’s to 20 cities rose just 0.16% MoM in January (the lowest MoM rise since August and well below the 0.35% MoM expected.

Source: Bloomberg

Home prices rose 0.9% YoY as mortgage rates have fallen. Home prices are still too high.

New York leads with a 4.9% annual gain, followed by Chicago at 4.6% and Cleveland at 3.6%, while Tampa fell 2.5%…

Don’t be confused. This isn’t leftists running to blue cities. It is mean reversion. The prior fleeing blue cities to red cities created a mean reversion effect where red cities home prices rose too fast and blue cities fell too fast.

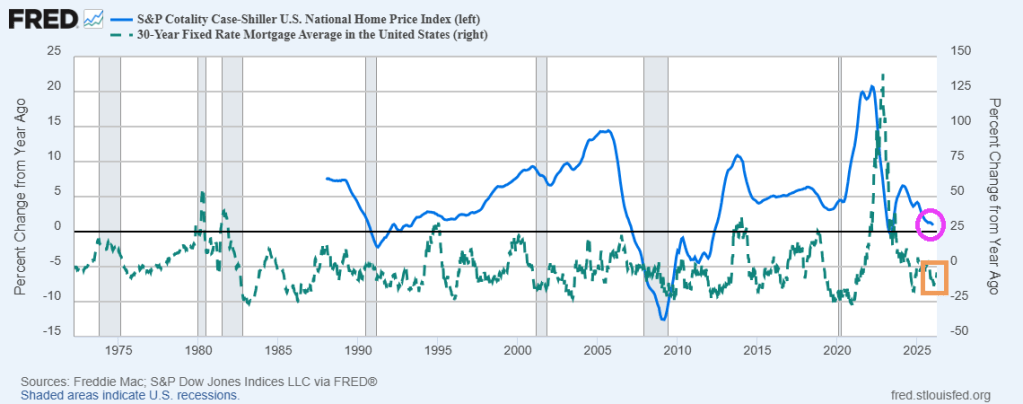

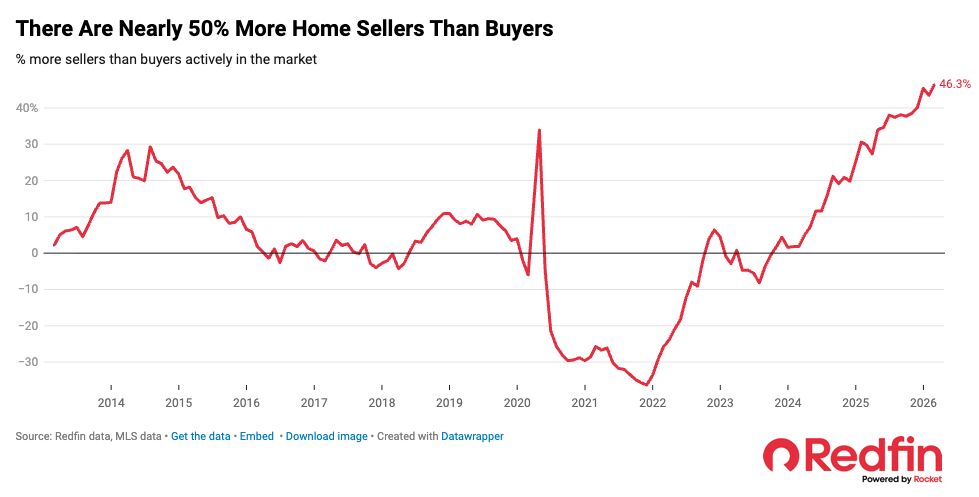

Nothing has been the same in the US housing market since the Covid outbreak of 2020. According to Redfin, there are nearly 50% more home sellers than buyers.

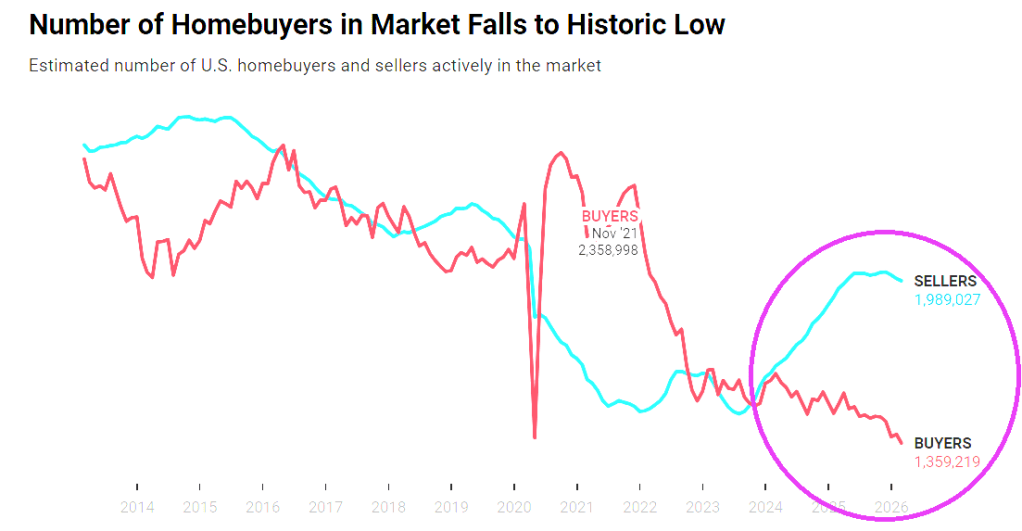

And the number of homebuyers has fallen to historic lows.

A good reason there are so few buyers is that home prices has soared after the Federal government’s spending spree after Covid.

Prayers for the soul of Noelia Castillo Ramos, murdered by the Spanish government. For being gangrape TWICE by immigrants then attempted suicide.

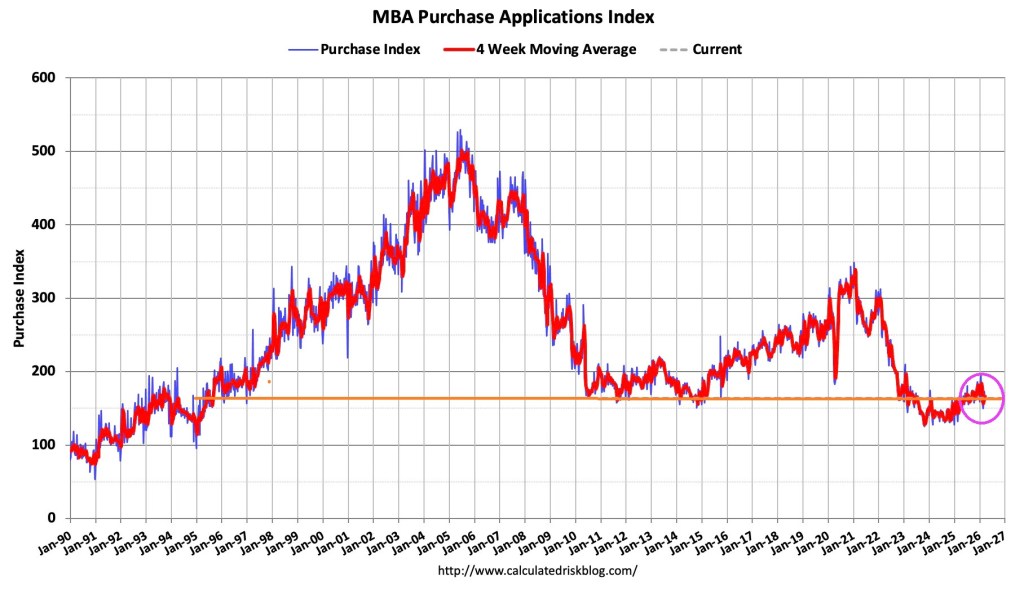

Mortgage applications decreased 10.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 20, 2026.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 10 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 5 percent higher than the same week one year ago.

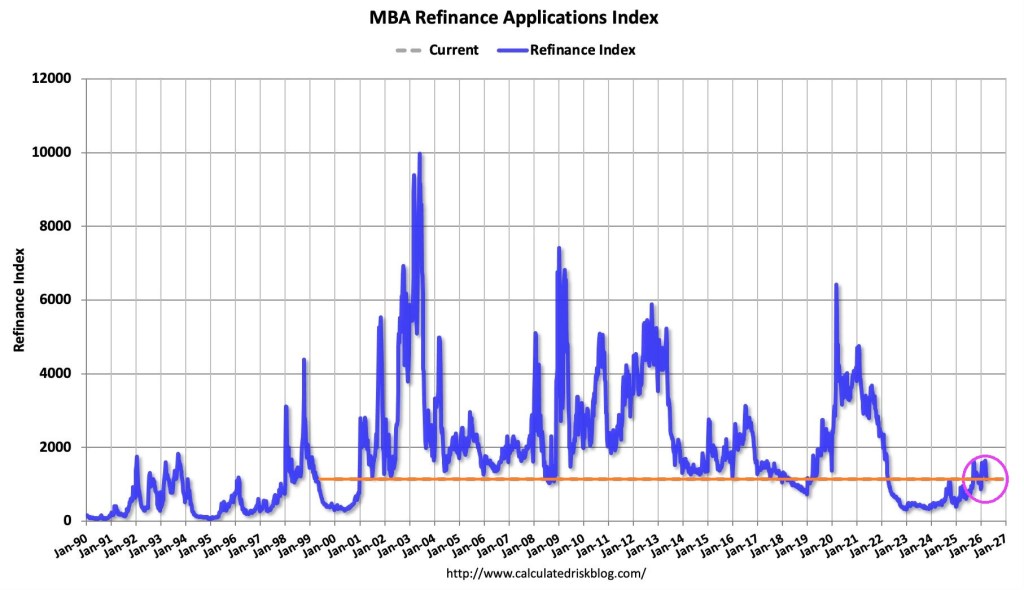

The Refinance Index decreased 15 percent from the previous week and was 52 percent higher than the same week one year ago.

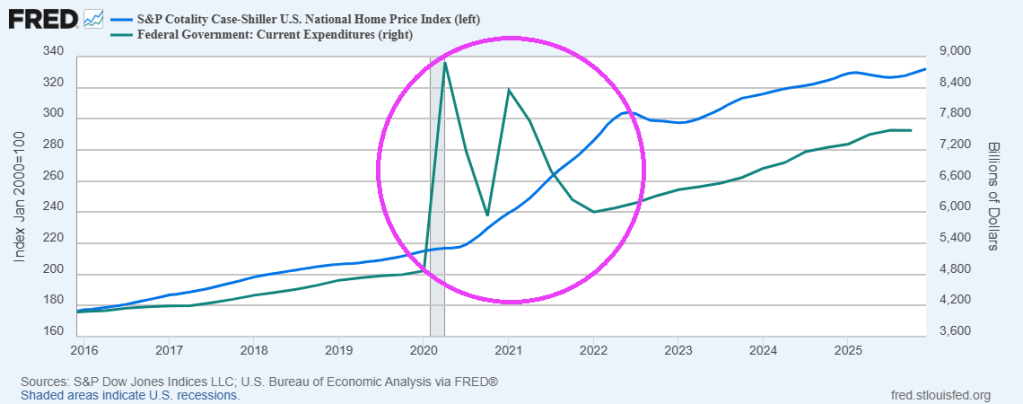

Nothing has been the same since Covid outbreak in 2020 and the resulting Federal government spemding spree.

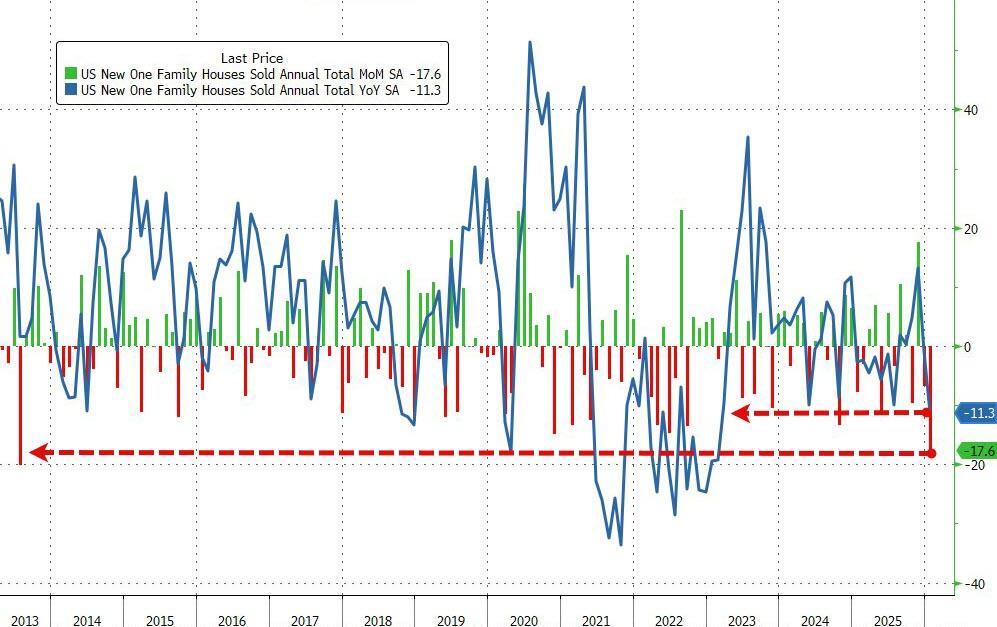

Despite falling mortgage rates, analysts expected December’s drop in new home sales to accelerate in January… and accelerate they did… crashing a stunning 17.6% MoM (-2.7% MoM exp) – the biggest MoM drop since July 2013.

This huge MoM drop dragged sales down 11.3% YoY – the worst slide in three years.

Source: Bloomberg

This huge drop dragged the new home sales SAAR down to its lowest since 2022, catching down to existing and pending sales…

Inventories are up (Houses for sale in Jan. rose 0.4% m/m to 476,000), prices are down (Median down 6.8% YoY at $400k – lowest since 2024)…

…and remember these deals were signed in January – meaning this is not mortgage related (some suggesting weather impact – Northeast sales down 44.7% MoM, MidWest -33.9% MoM, but the scale is immense).

Moral of the story: US home prices are too high for millions of households to afford.

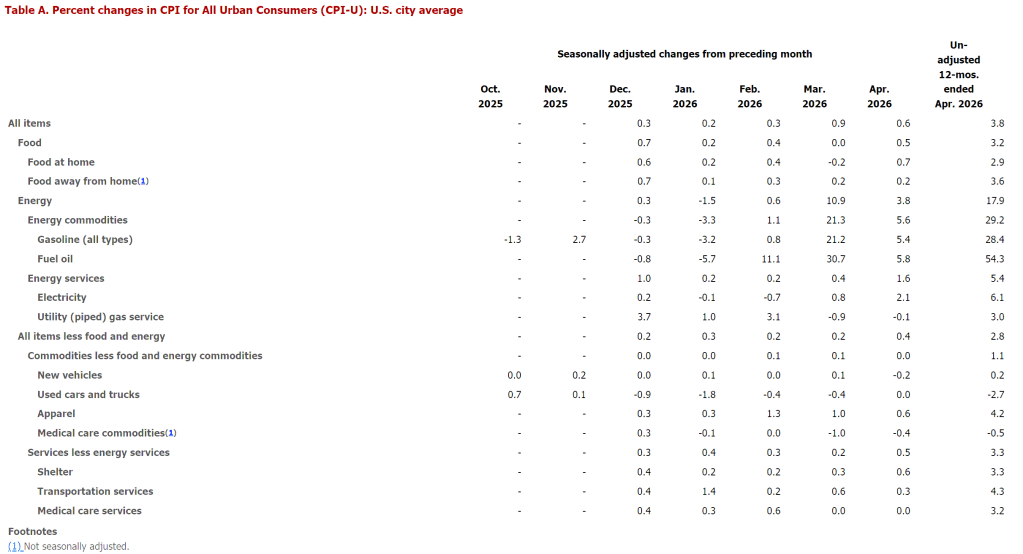

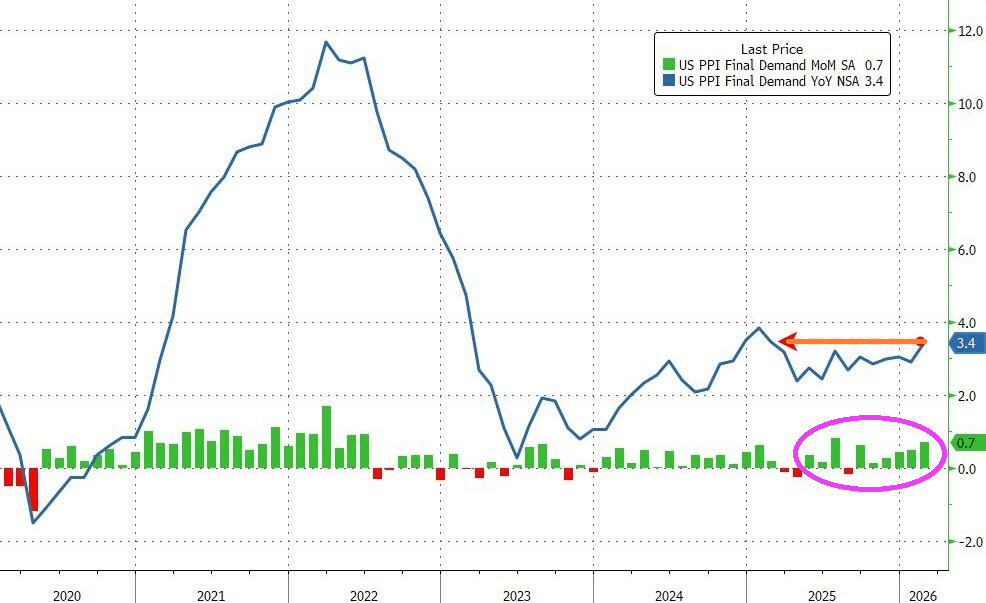

Producer prices were higher by 3.4% YoY (notably hitter than the 3.0% expected and up from the 2.9% prior). That is the hottest PPI since January 2025

Source: Bloomberg

More than half of the February rise in prices for final demand can be attributed to a 0.5-percent advance in the index for final demand services. Prices for final demand goods increased 1.1 percent.

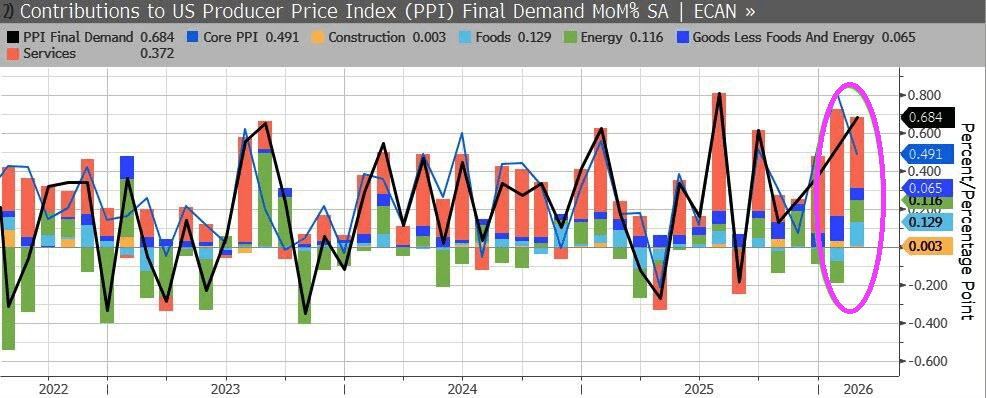

Core PPI (ex Food and Energy) also soared (+0.5% MoM) pushing core prices up by 3.9% YoY – the highest since Jan 2025.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.