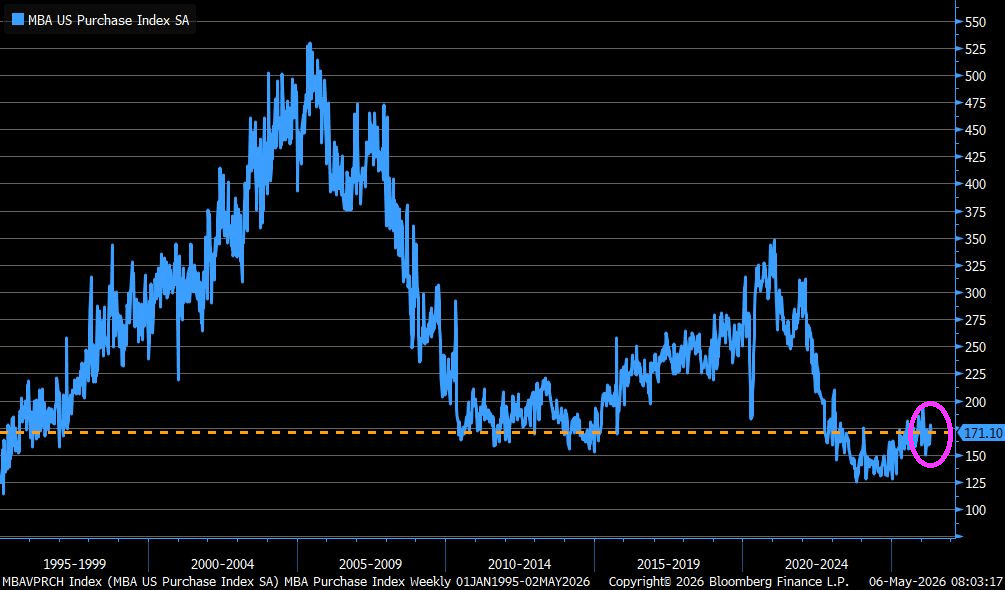

MBA Mortgage Purchase Index down -3.7% over the past week after climbing +1.2% in prior week…30y mortgage rate rose to +6.45% up from +6.37% and highest in a month.

With the Federal government playing an outsized role in the housing and mortgage markets, the Federal goverment is like an enormous Mantis Shrimp.

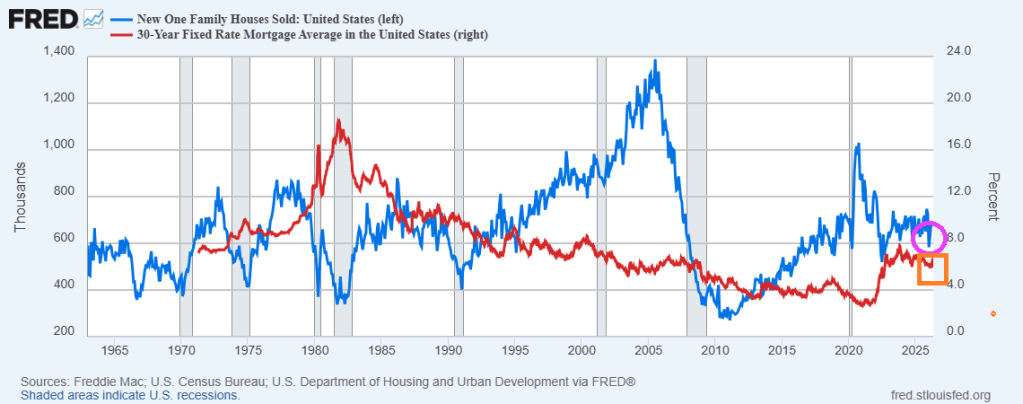

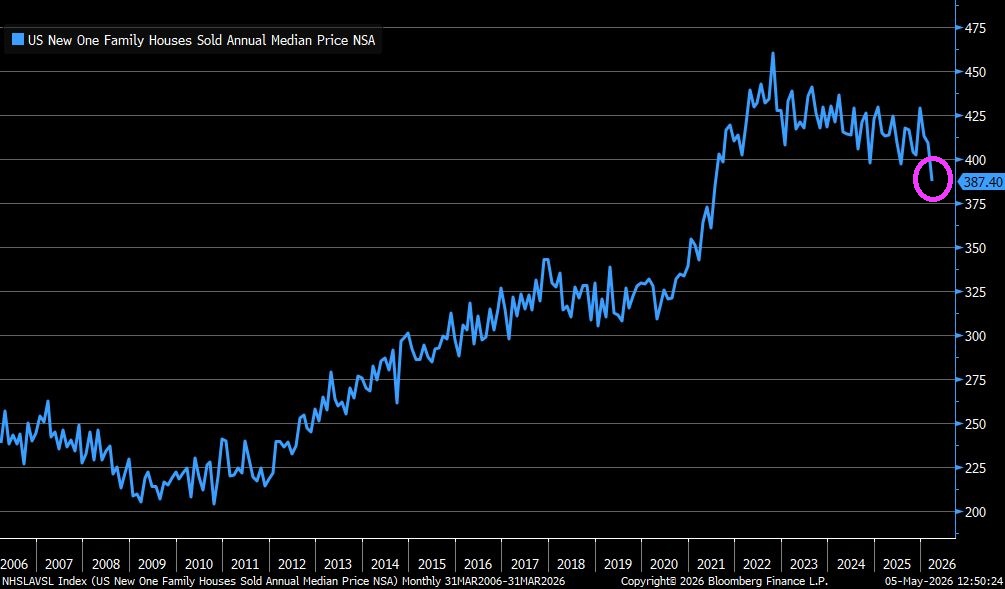

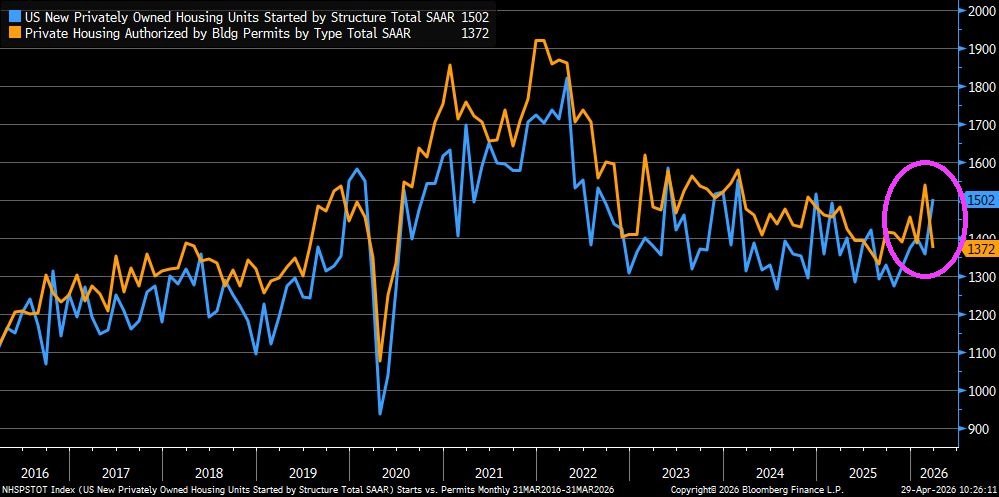

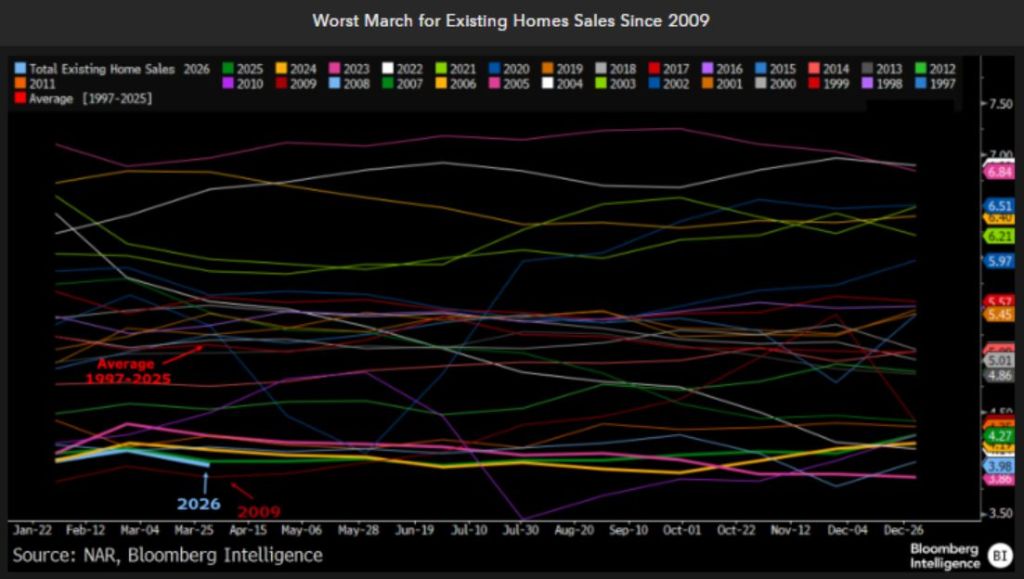

High home prices show signs of cooling, mortgage rates remain fairly constant, while new home sales increase by 47k in March. Despite rising mortgage rates.

The bigger picture? New home sales remain relatively depressed after the Covid outbreak in 2020.

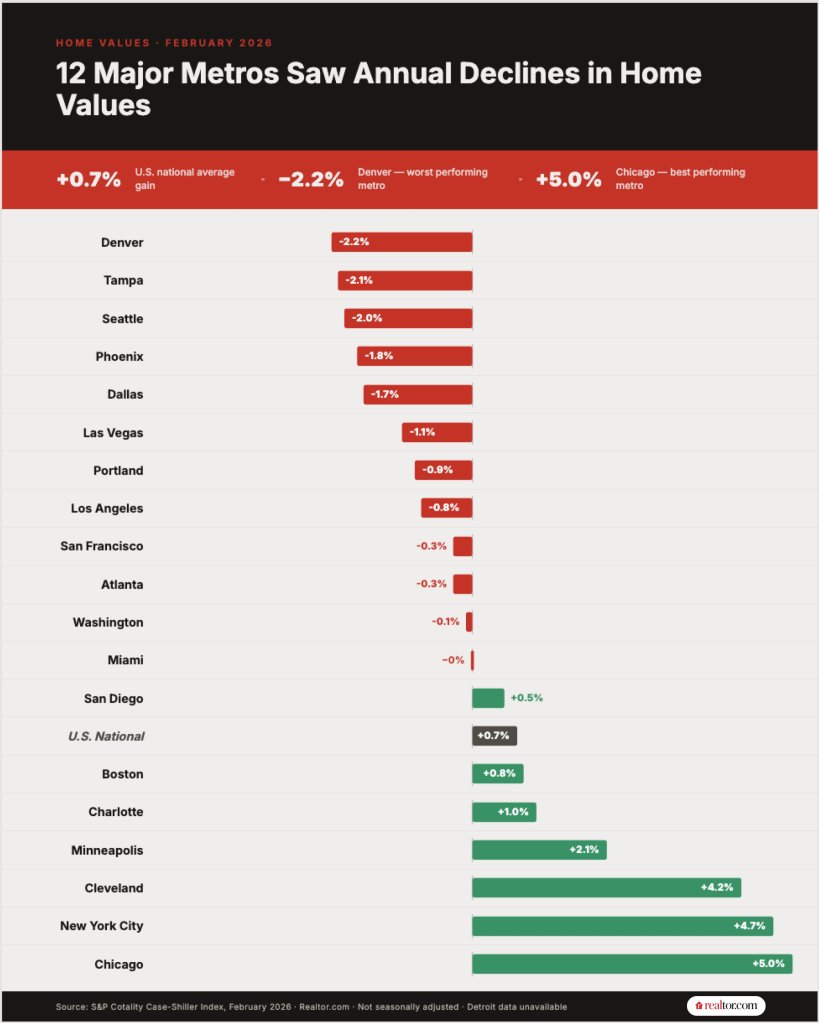

More than half of major U.S. metropolitan areas posted year-over-year home price declines in February, with Denver (-2.2%) displacing Tampa (-2.1%) as the weakest market, according to data from the S&P Cotality Case-Shiller Index released Tuesday.

Los Angeles (-0.8%) and Washington, DC (-0.1%) also joined the list of markets with falling home values, signaling weakness that expanding out of the long-suffering Sunbelt region.

kkk

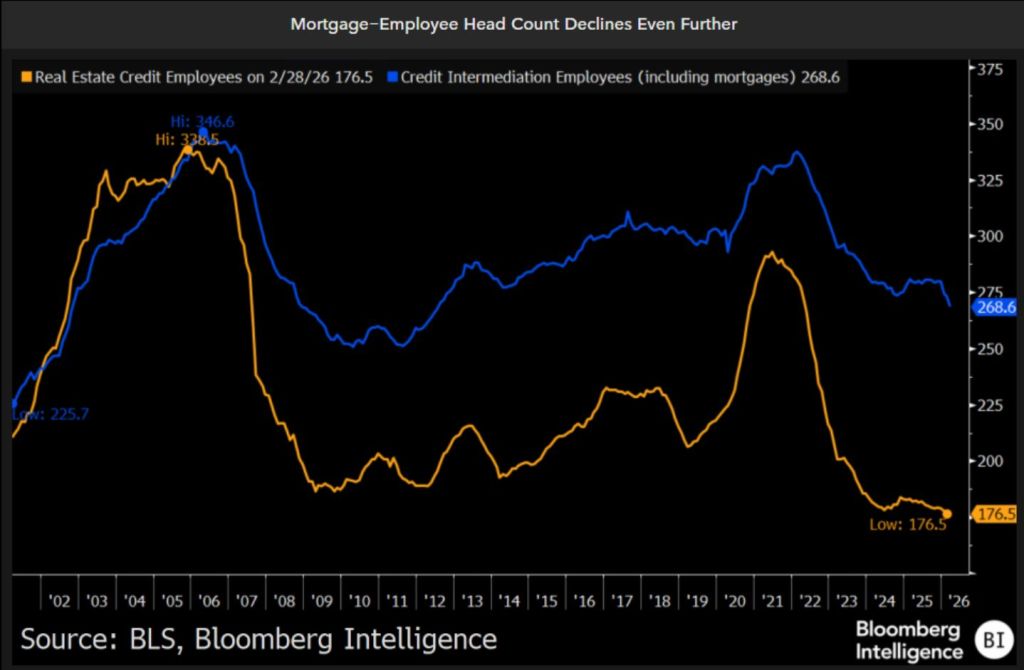

Mortgage employee headcount has fallen to lowest level since the housing bubble and mortgage crisis of 2005-2008.

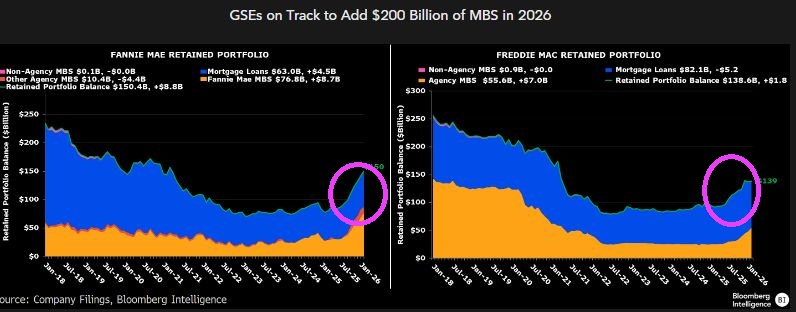

I spoke at the American Action Forum in Washington DC on the future of government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. Speaking with me was Laurie Goodman from The Urban Institute. Laurie loves Fannie Mae and Freddie Mac and argued passionately against shutting them down. I argued to shrink their retained portfolios to zero and privatize them.

When Trump was elected President for the second time and the House of Representatives was controlled by Republicans, there was hope that Fannie Mae and Freddie Mac would be privatized. But alas, it was not to be.

In fact, the retained portfolios for Fannie Mae (left) and Freddie Mae (right) are increasing, not decreasing.

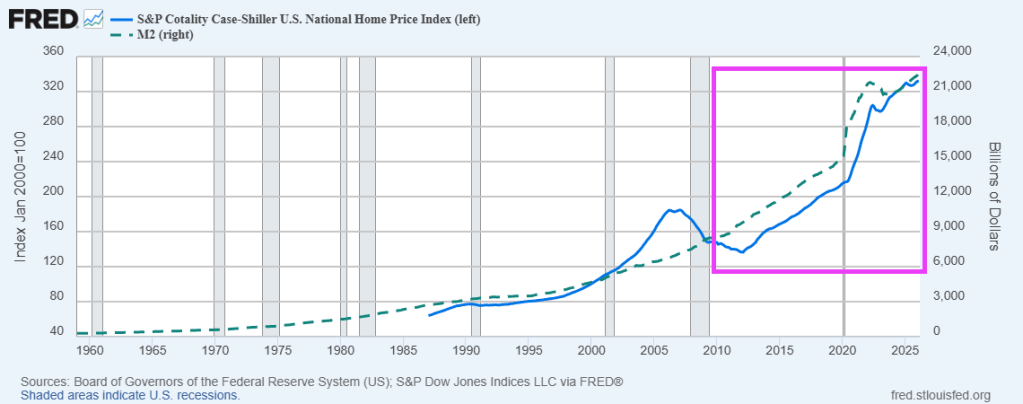

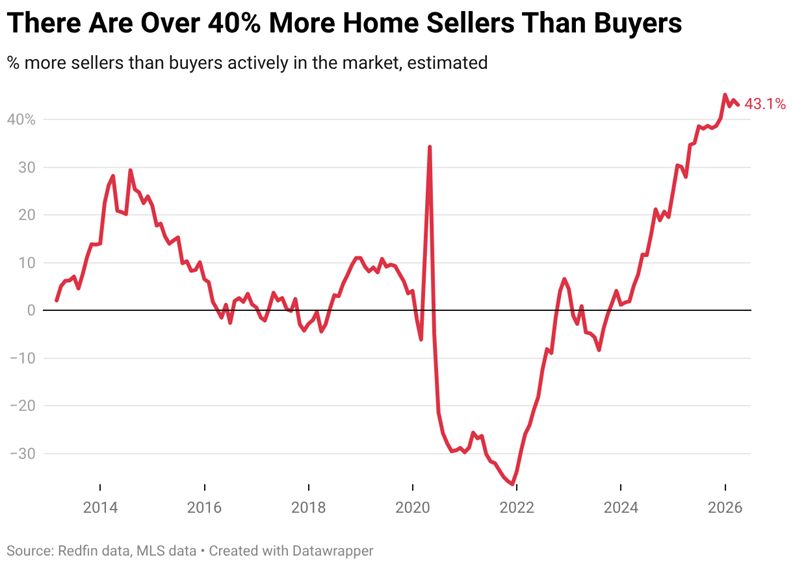

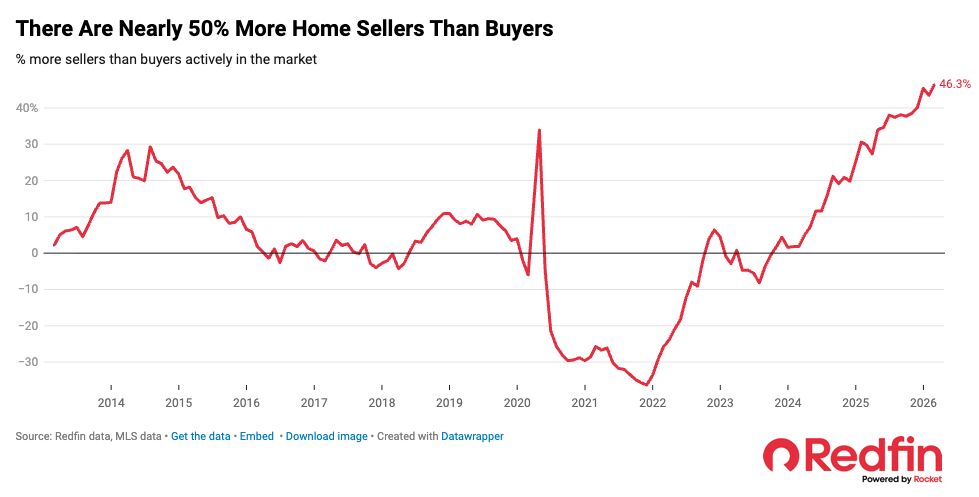

Nothing has been the same in the US housing market since the Covid outbreak of 2020. According to Redfin, there are nearly 50% more home sellers than buyers.

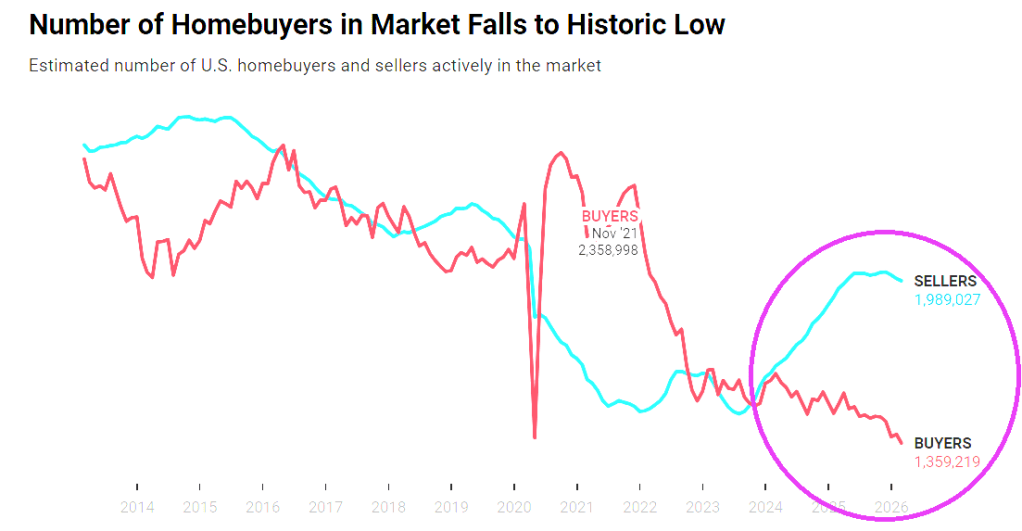

And the number of homebuyers has fallen to historic lows.

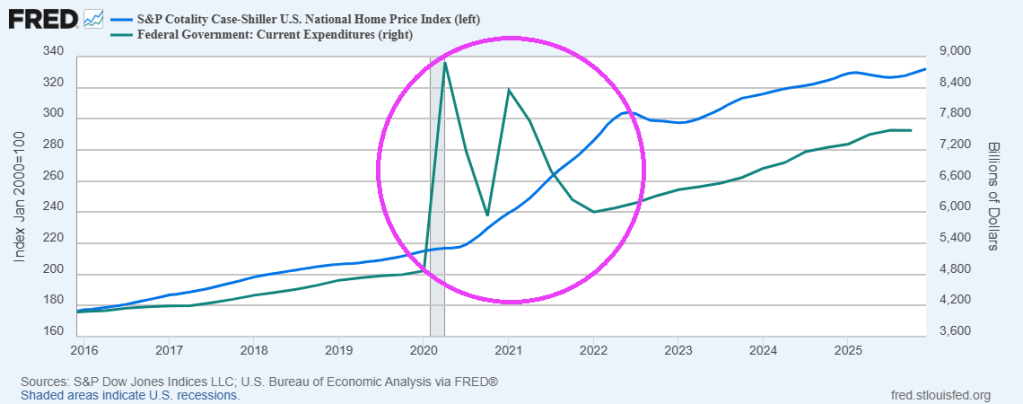

A good reason there are so few buyers is that home prices has soared after the Federal government’s spending spree after Covid.

Prayers for the soul of Noelia Castillo Ramos, murdered by the Spanish government. For being gangrape TWICE by immigrants then attempted suicide.

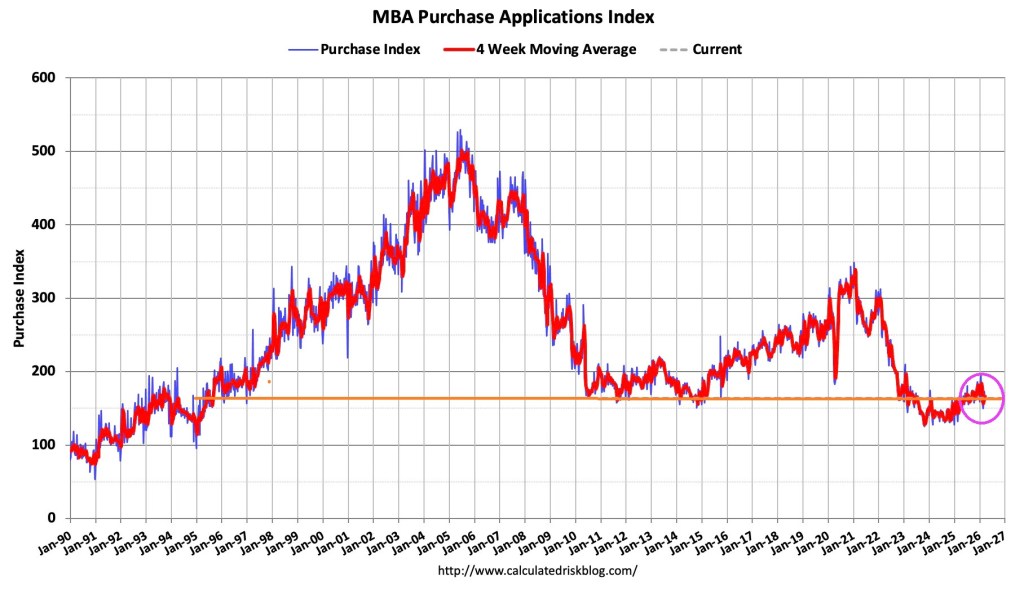

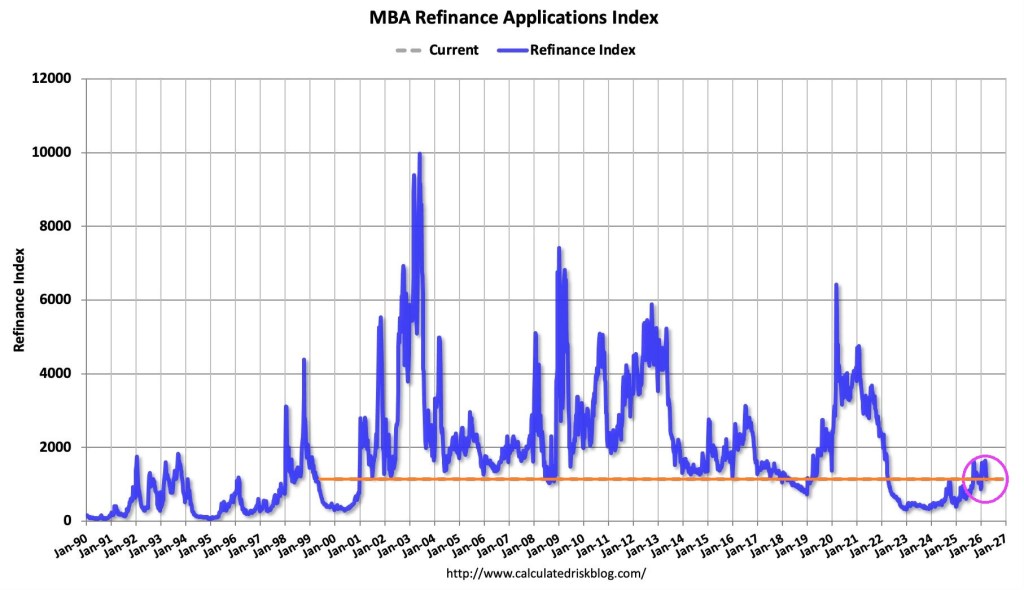

Mortgage applications decreased 10.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 20, 2026.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 10 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 5 percent higher than the same week one year ago.

The Refinance Index decreased 15 percent from the previous week and was 52 percent higher than the same week one year ago.

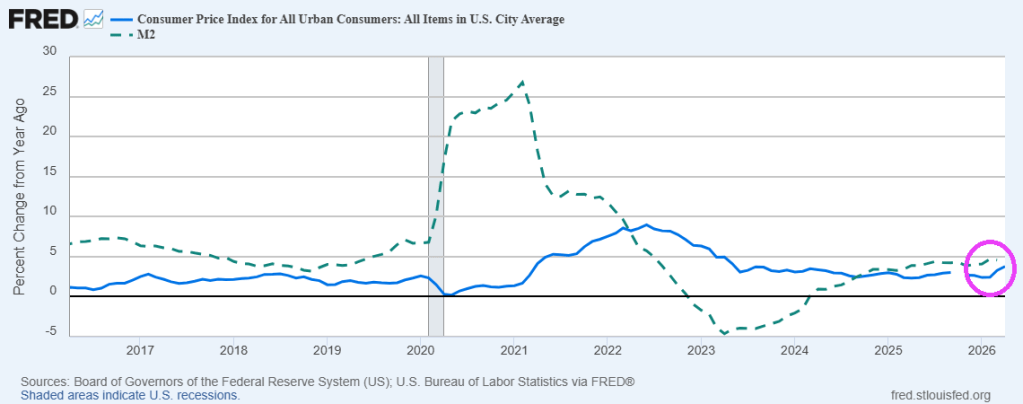

Nothing has been the same since Covid outbreak in 2020 and the resulting Federal government spemding spree.

You must be logged in to post a comment.