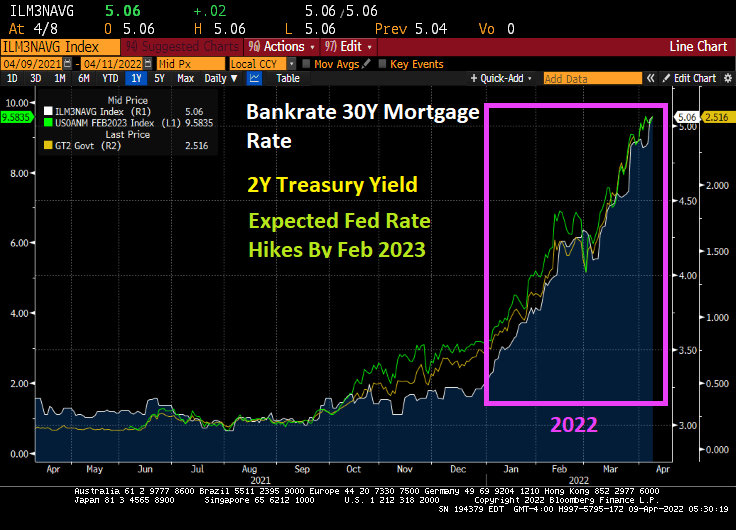

2022 has been a tough year for bond investors and the mortgage industry.

Doubleline’s Jeff Gundlach observed that the 2 Year Treasury yield is up 125 bp over the past month or so. I commented that the 2 Year Treasury Yield is up 179 bp since December 31, 2021 and the 30-year mortgage rate is also up 179 bp since the end of 2021. Yes, 2022 has been a dismal year for bonds and the mortgage market.

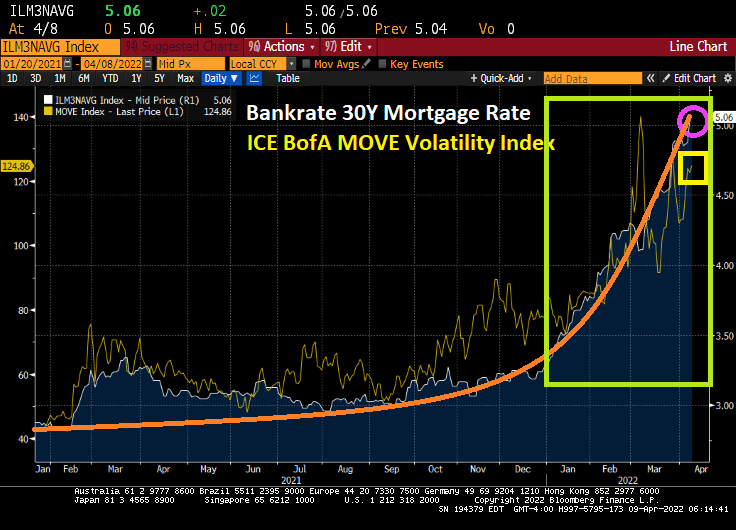

The ICE BofA MOVE index, a yield curve weighted index of the normalized implied volatility on 1-month Treasury options, has risen in 2022 along with the 30-year mortgage rate as the normally dormant Federal Reserve finally waking-up and trying to fight inflation.

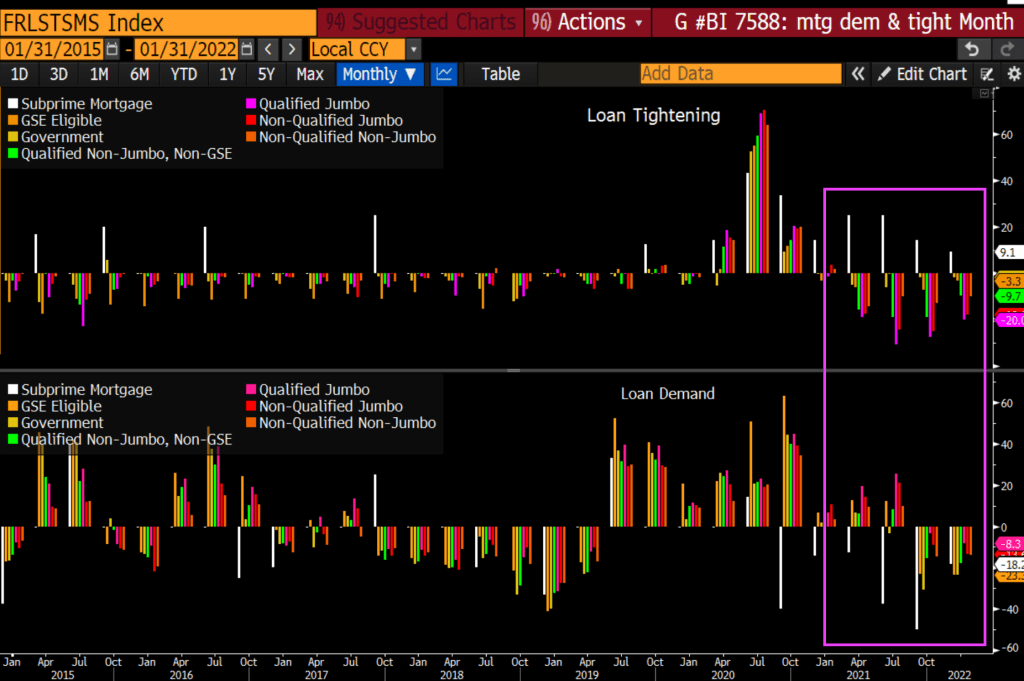

Mortgage demand backs off due to anticipated Fed rate hikes.

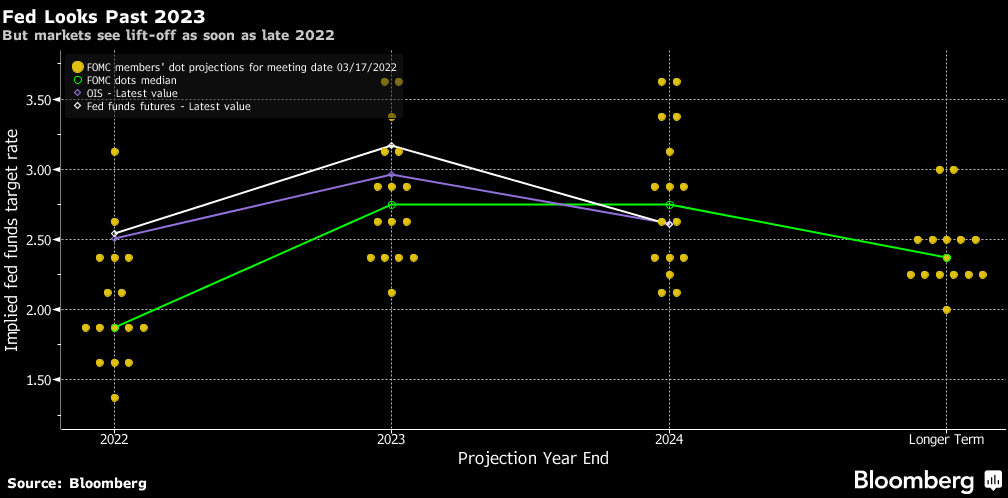

The latest Fed Dots Plot reveals that Fed Open Market Committee members are expecting Fed Funds rate increases in 2023, but remaining the same in 2024 (FOMC median projection). Then falling in the longer term.

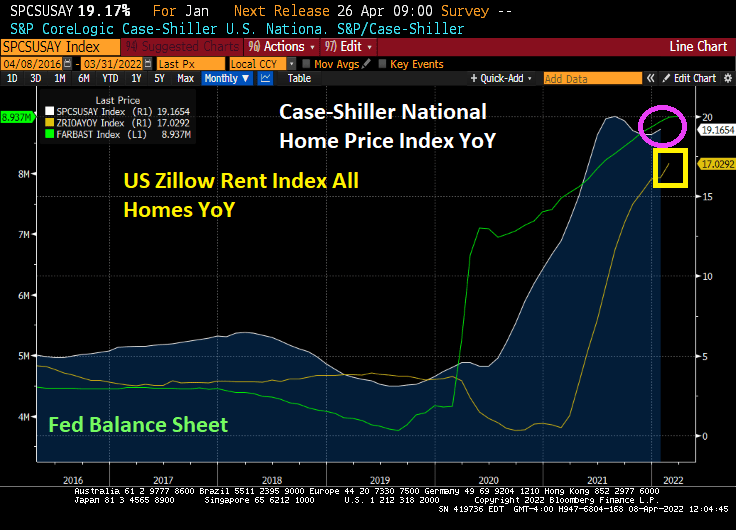

With home prices and rents soaring with Federal Reserve stimulus, let’s see how home prices and rents react to The Fed raising rates. My models forecast a slowdown in late summer 2022 to 6% home price growth YoY as The Fed actually implements their quantitative tightening.

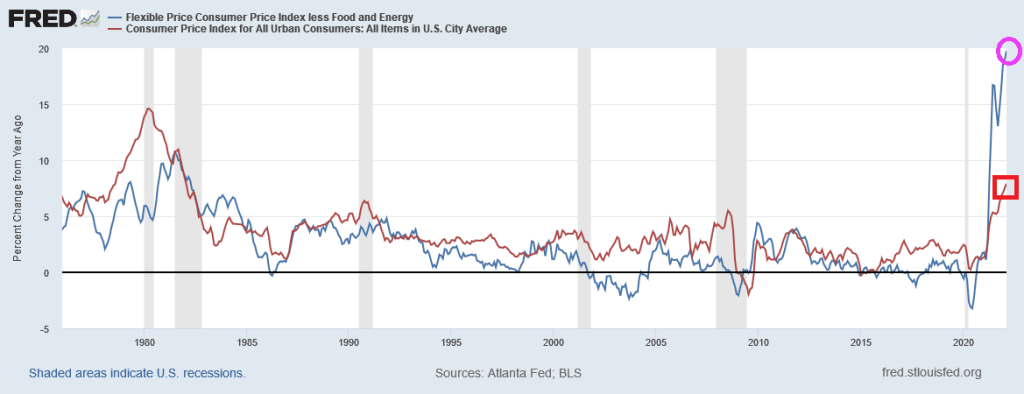

Inflation? CPI YoY is the highest in 40 years and FLEXIBLE Core CPI is 20% and the highest since … Lyndon B. Johnson was President (the flexible price index only goes back to 1968). Actually, Flexible Price inflation is even higher than it was under LBJ. Perhaps this is one of those accomplishments that Biden staffer are complaining never gets discussed.

On a side note, Sheila Bair has stepped down as CEO of government mortgage giant Fannie Mae.

The Financial House is a Rockin’ … but not in a good way.

You must be logged in to post a comment.