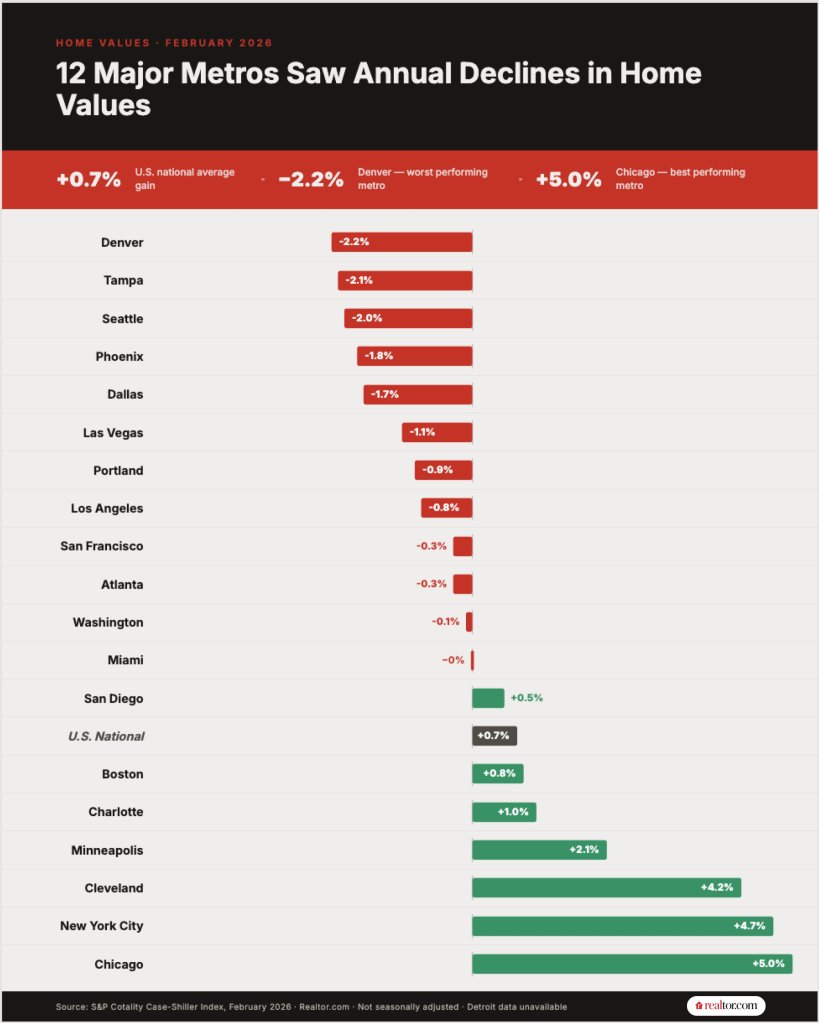

More than half of major U.S. metropolitan areas posted year-over-year home price declines in February, with Denver (-2.2%) displacing Tampa (-2.1%) as the weakest market, according to data from the S&P Cotality Case-Shiller Index released Tuesday.

Los Angeles (-0.8%) and Washington, DC (-0.1%) also joined the list of markets with falling home values, signaling weakness that expanding out of the long-suffering Sunbelt region.

kkk

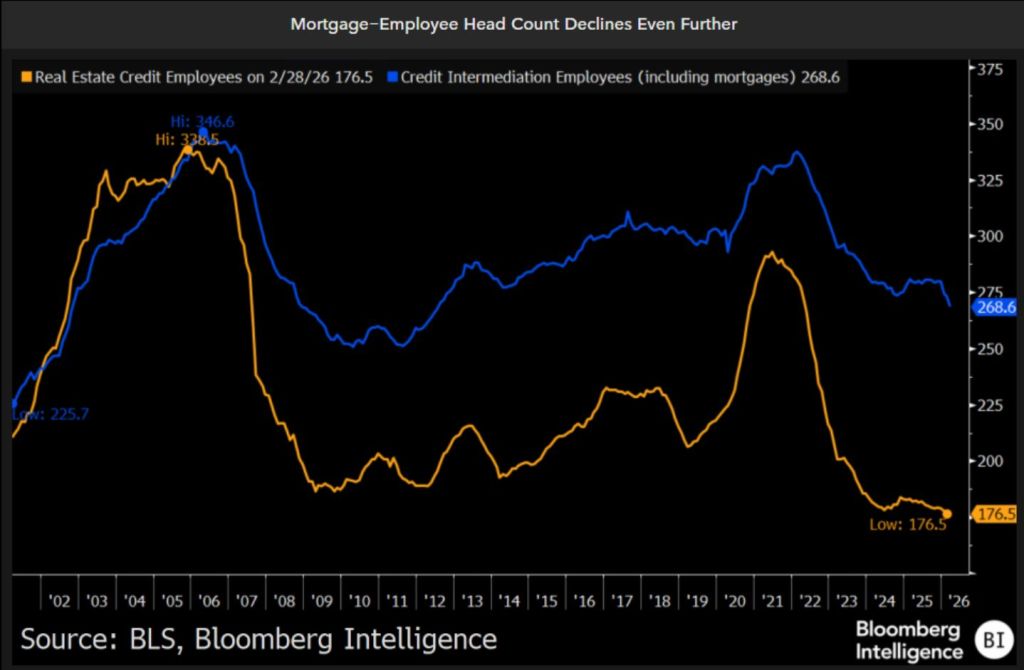

Mortgage employee headcount has fallen to lowest level since the housing bubble and mortgage crisis of 2005-2008.

So much for the “Trump has ruined the economy” mantra of politicians and celebrities.

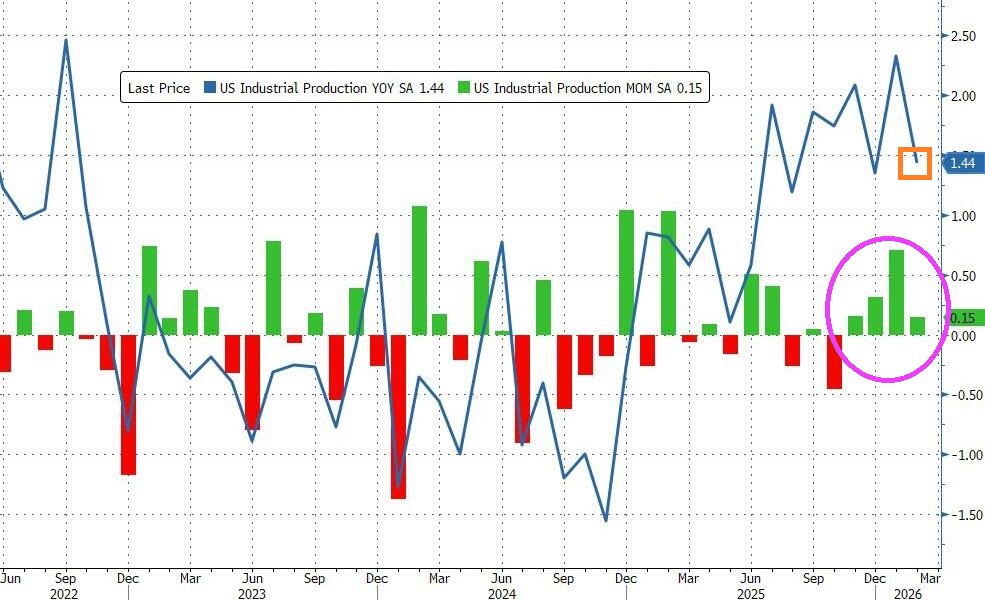

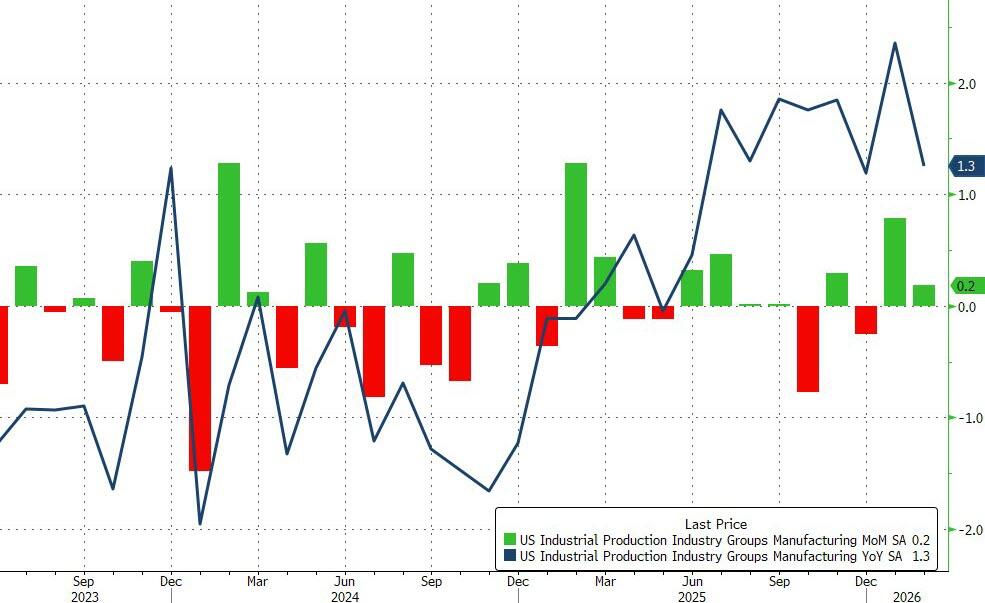

After a strong gain in January, US Industrial Production continued to expand in February, rising 0.2% MoM (better than expected +0.1%) – the fourth straight month of gains with Production up 1.44% YoY.

Source: Bloomberg

Manufacturing output also beat expectations, rising 0.2% MoM in February.

Durable manufacturing output edged up 0.1 percent, with mixed results across categories; the index for motor vehicles and parts posted the largest gain, and the index for machinery posted the largest loss.

Nondurable manufacturing output rose 0.2 percent, with gains in the production of chemicals, of plastic and rubber products, and of paper products outweighing declines in the output of petroleum and coal products and of food, beverage, and tobacco products. The output of other manufacturing (publishing and logging) rose 1.3 percent.

Mining output increased 0.8 percent in February, following a 0.9 percent increase in January. The output of utilities fell 0.6 percent in February, reflecting no change in the index for electric utilities and a 4.7 percent drop in the index for natural gas utilities.

Source: Bloomberg

Capacity Utilization printed 76.3 (better than expected)…

…maintaining the positive trend since Trump’s second term began.

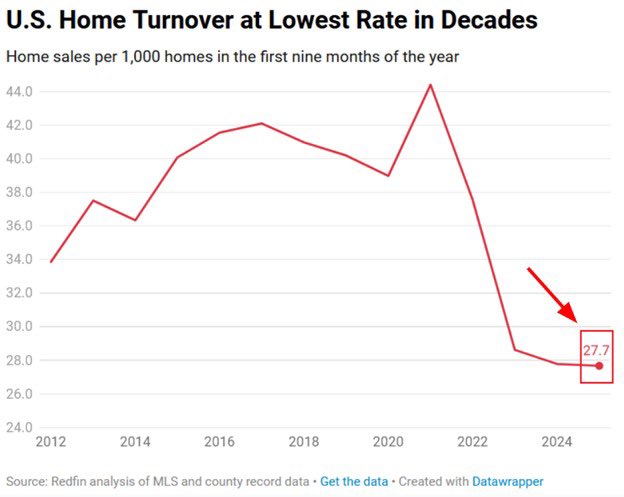

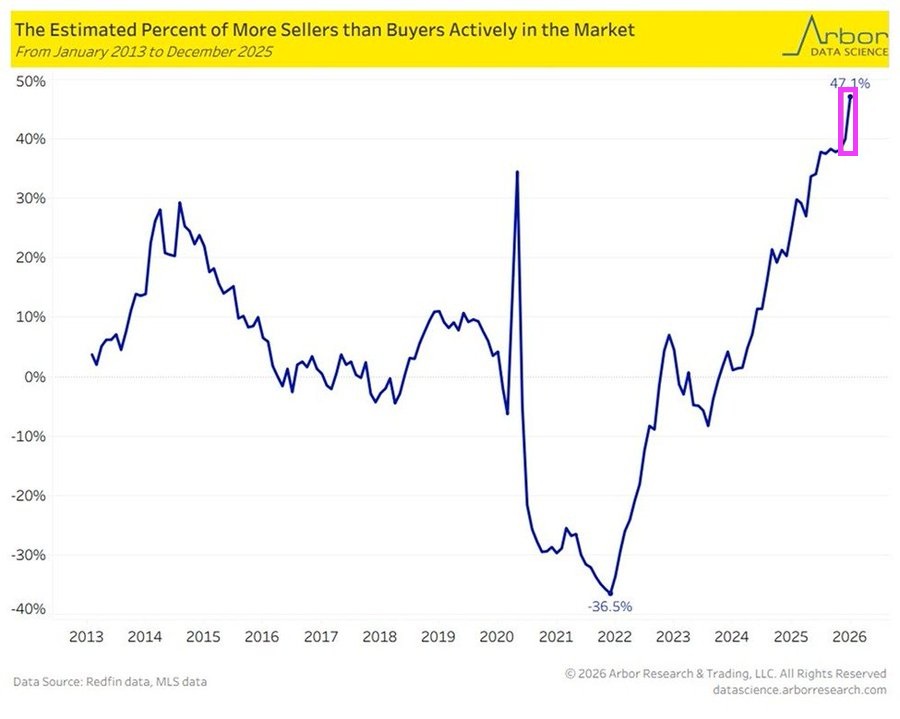

Home prices exploded under Biden and Covid Federal spending. Making housing unaffordable for millions. Now the turnover rates for homes is at its lowesst rate in decades.

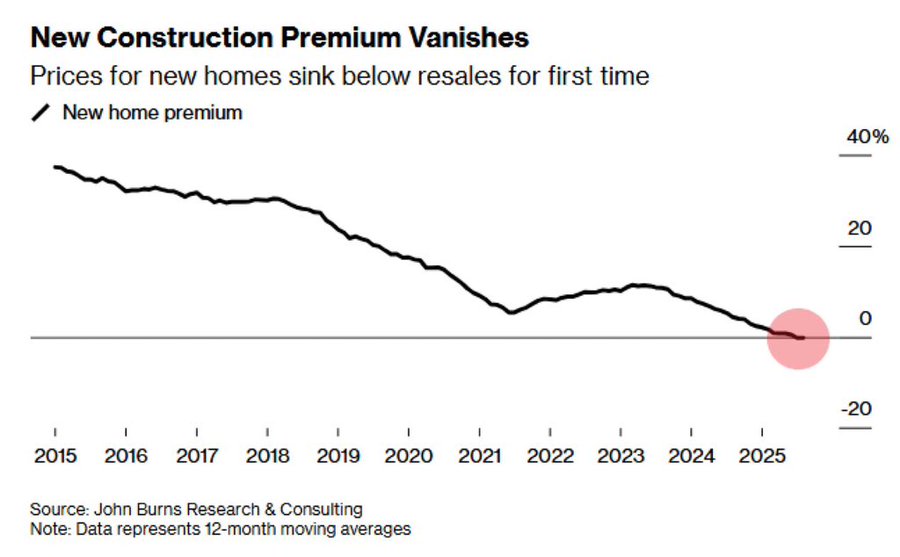

Existing homes are now more expensive than new homes.

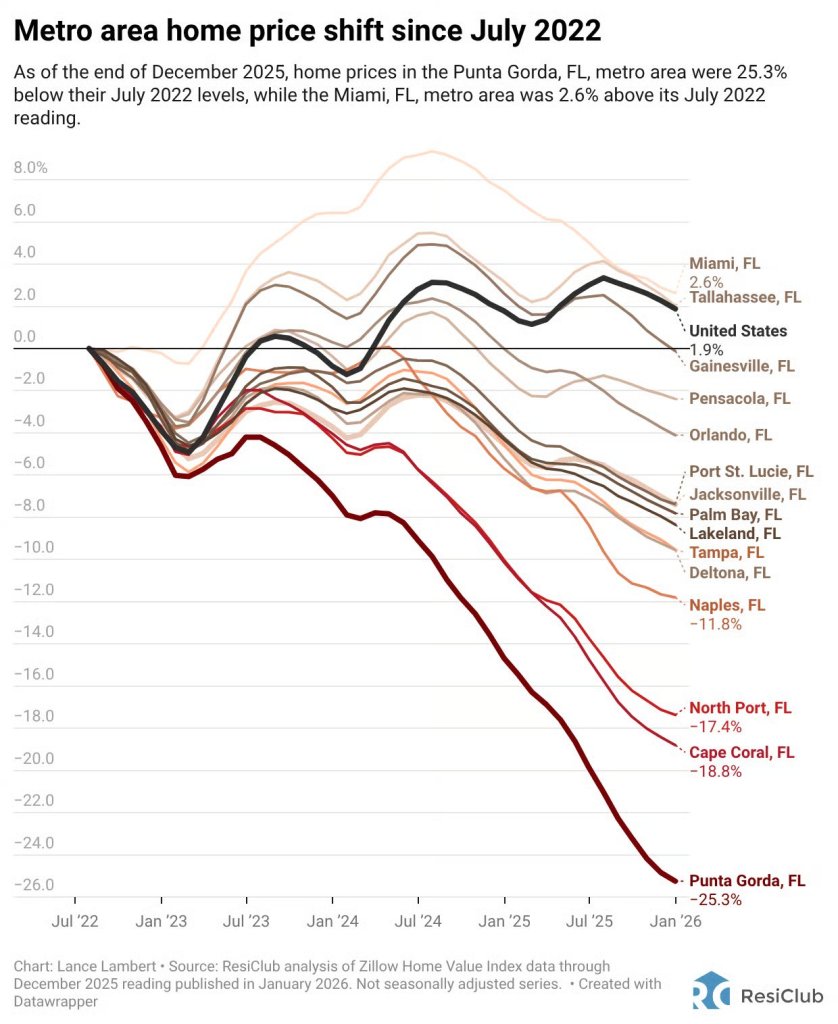

Florida housing is getting gut-punched from Naples to Punta Gorda.

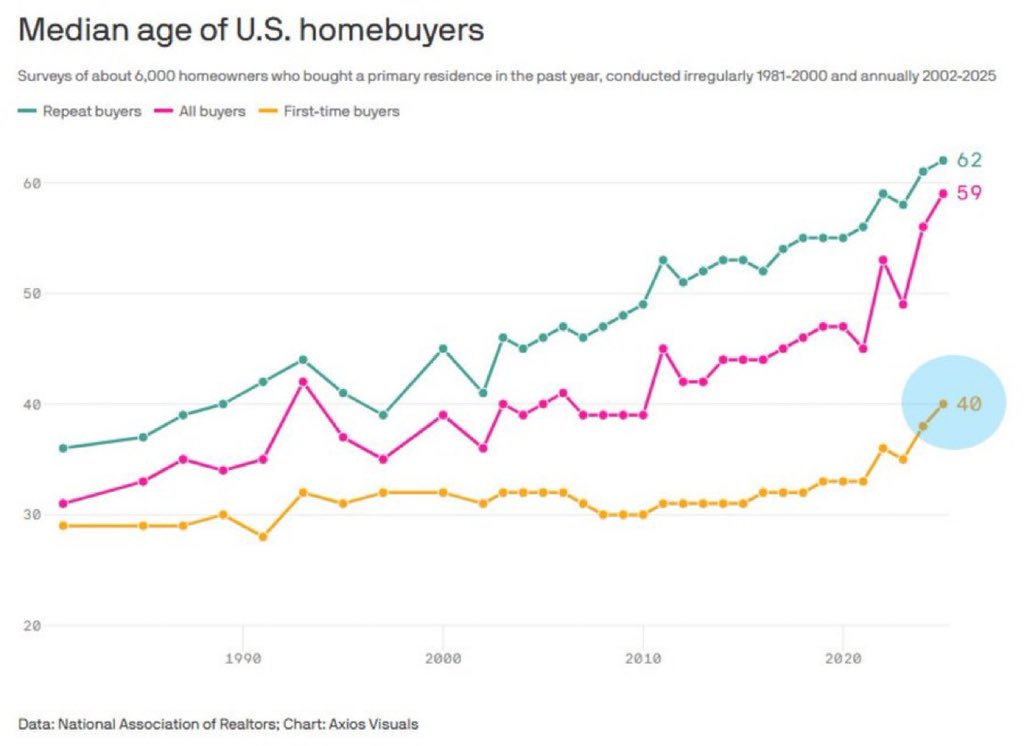

Yikes! Median age of first time homebuyers is 40.

Fortunately, Joe Biden is out of office. But Chuck Schumer may make a comeback and restart the insane Covid-era spending. Schumer, the penultimate knucklehead in Congress, approved Ketanji Brown Jackson to sit on the Supreme Court of the USA.

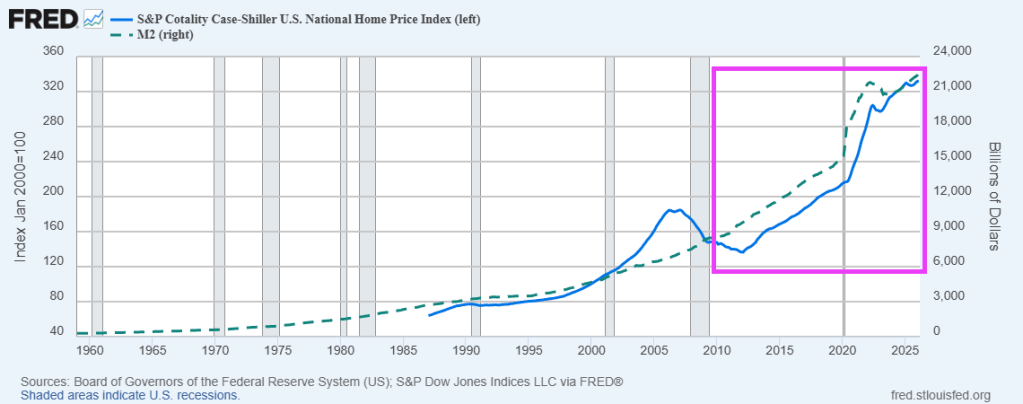

Keep on printing money. It seems that home price growth requires The Fed to keep printing money.

S&P/Case-Shiller released the monthly Home Price Indices for November (“November” is a 3-month average of September, October and November closing prices). September closing prices include some contracts signed in July, so there is a significant lag to this data. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The S&P Cotality Case-Shiller U.S. National Home Price NSA Index posted a 1.4% annual gain for November, in line with the previous month.

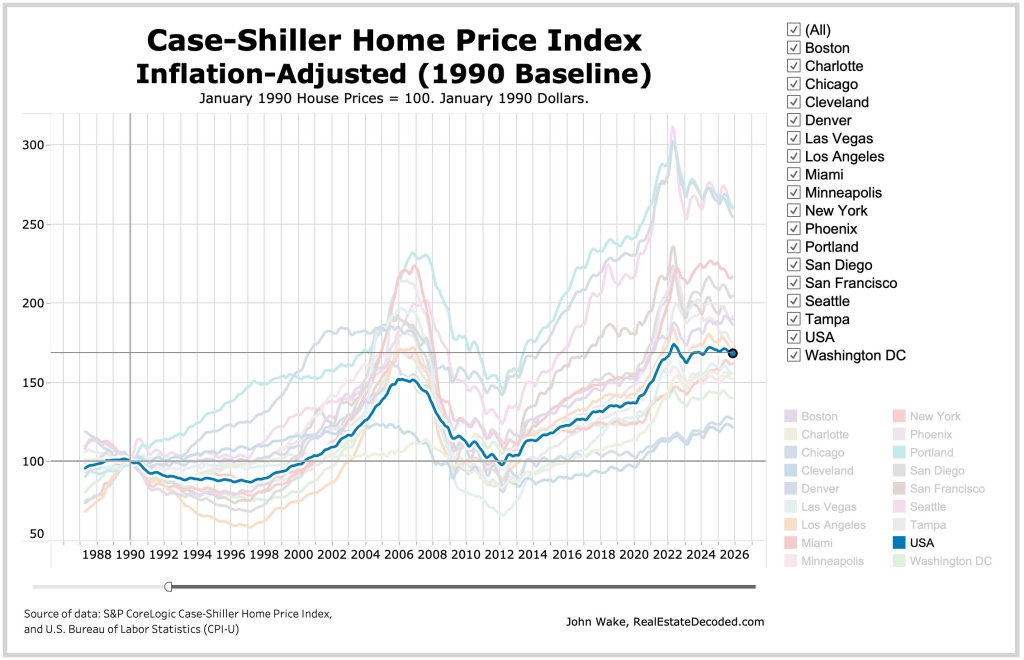

Real home values declined as consumer inflation (2.7%) outpaced the National Index gain (1.4%) by 1.3 percentage points.

Regional divergence persisted: Midwestern and Northeastern markets led by Chicago (+5.7%) and New York (+5.0%) posted gains, while Sun Belt cities including Tampa (–3.9%), Phoenix (–1.4%), Dallas (–1.4%), and Miami (–1.0%) saw declines. … “Regional patterns continue to illustrate a stark divergence. Chicago leads all cities for a second consecutive month with a 5.7% year-over-year price increase, followed by New York at 5.0% and Cleveland at 3.4%. These historically steady Midwestern and Northeastern markets have maintained respectable gains even as overall conditions cool. By contrast, Tampa home prices are 3.9% lower than a year ago – the steepest decline among the 20 cities, extending that market’s 13-month streak of annual drops. Other Sun Belt boomtowns remain under pressure as well: Phoenix (-1.4%), Dallas (-1.4%), and Miami (-1.0%) each continue to see year-over-year declines, a dramatic turnaround from their pandemic-era strength.

“Monthly price changes were mixed but leaned negative in November, underscoring persistent softness. On a non-seasonally adjusted basis, 15 of the 20 major metro areas saw prices decline from October (versus 16 declines in the previous month). Only a handful of markets – including Los Angeles, San Diego, Miami, New York, and Phoenix – eked out slight gains before seasonal adjustment. After accounting for typical seasonal slowing, the National Index inched up just 0.4% for the month, indicating that price momentum remains muted. … The S&P Cotality Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 1.4% annual gain for November. The 10-City Composite showed an annual increase of 2.0%, up from a 1.9% increase in the previous month. The 20-City Composite posted a year-over-year increase of 1.4%, up from a 1.3% increase in the previous month. … The pre-seasonally adjusted U.S. National Index saw a drop of 0.1% and the 20-City Composite Index fell 0.03%, while the 10-City Composite Index increased 0.1%.

After seasonal adjustment, the U.S. National Index reported a monthly increase of 0.4%, and both the 10-City Composite and 20-City Composite Indices posted month-over-month gains of 0.5%.

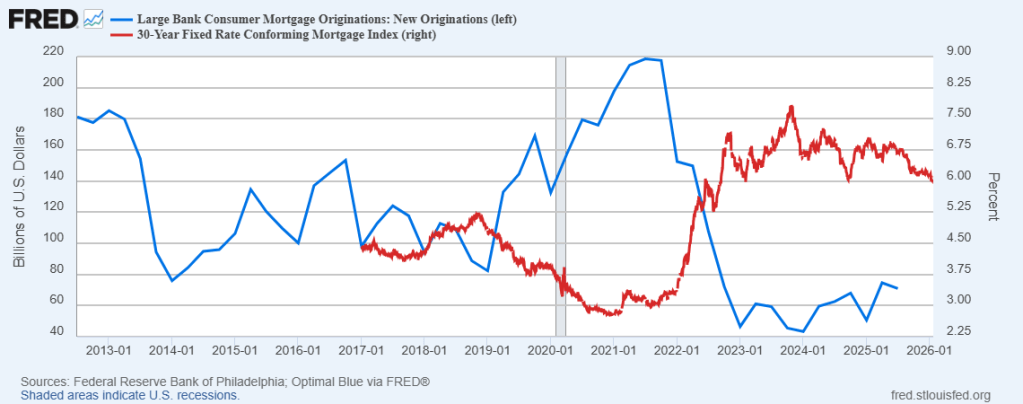

Mortgage demand is recovering slowly from Biden-era mismanagement. Rising mortgage rates coupled with rising home prices made housing affordability get flushed down the toilet.

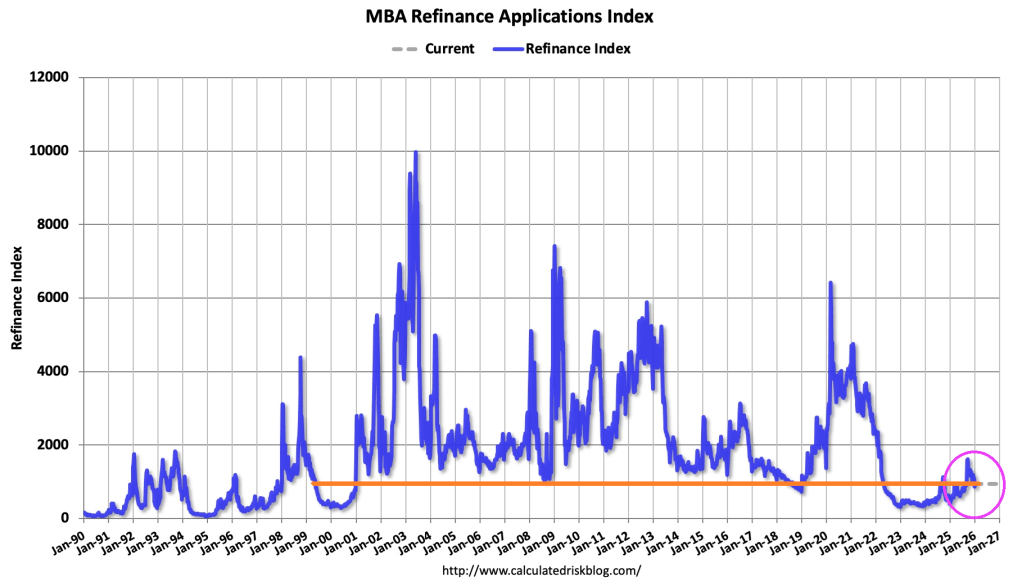

Mortgage applications decreased 9.7 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 2, 2026. The results include an adjustment for the holidays.

The Market Composite Index, a measure of mortgage loan application volume, decreased 9.7 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 28 percent compared with two weeks ago. The unadjusted Refinance Index decreased 31 percent from two weeks ago and was 108 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from two weeks earlier. The unadjusted Purchase Index decreased 23 percent compared with two weeks ago and was 10 percent higher than the same week one year ago.

The holiday adjusted Refinance Index decreased 14 percent from two weeks ago and was 133 percent higher than the same week one year ago.

This is the opposite of the housing bubble from The Big Short where home prices in Phoenix, Las Vegas, Los Angeles and Florida rose then crashed. Instead, the fastest growing cities are in the northeast and midwest.

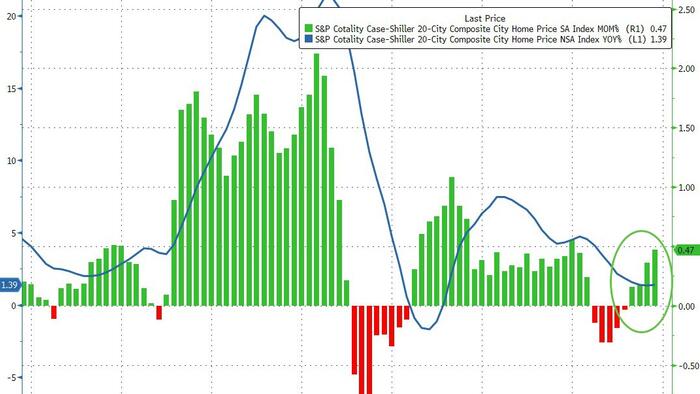

The Case-Shiller 20-City Home Price Index rose 1.3% year over year in October 2025, easing from a 1.4% increase in September and coming in slightly above market expectations of a 1.1% gain. This represents the smallest annual increase since July 2023, reinforcing signs that the US housing market is settling into a much slower growth phase. Home price appreciation continues to trail consumer inflation. With October CPI estimated at around 3.1%, inflation-adjusted home values appear to have edged modestly lower over the past year.

Regional data point to a pronounced geographic rotation. Chicago now leads all major markets with a 5.8% annual gain, followed by New York at 5.0% and Cleveland at 4.1%. In contrast, Tampa recorded a 4.2% decline, the steepest among the 20 cities, and its 12th consecutive month of falling annual prices. Other former pandemic boom markets, especially in the Sun Belt, are seeing the sharpest declines, led by Phoenix (-1.5%), Dallas (-1.5%), and Miami (-1.1%).

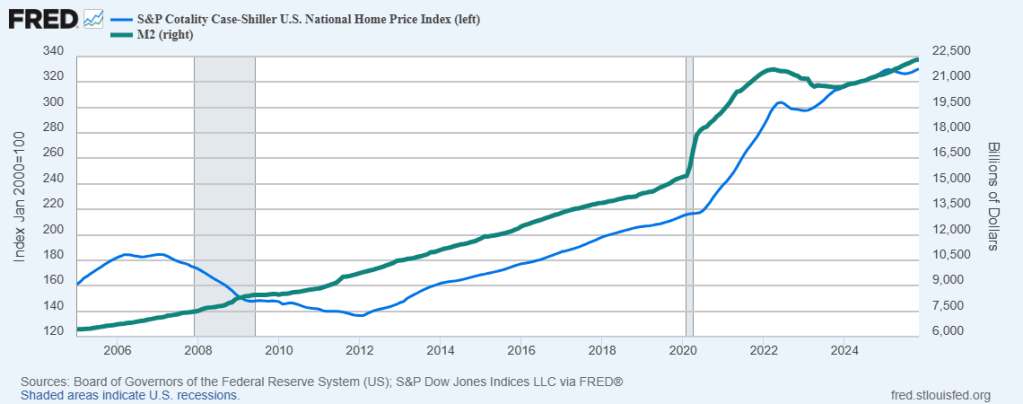

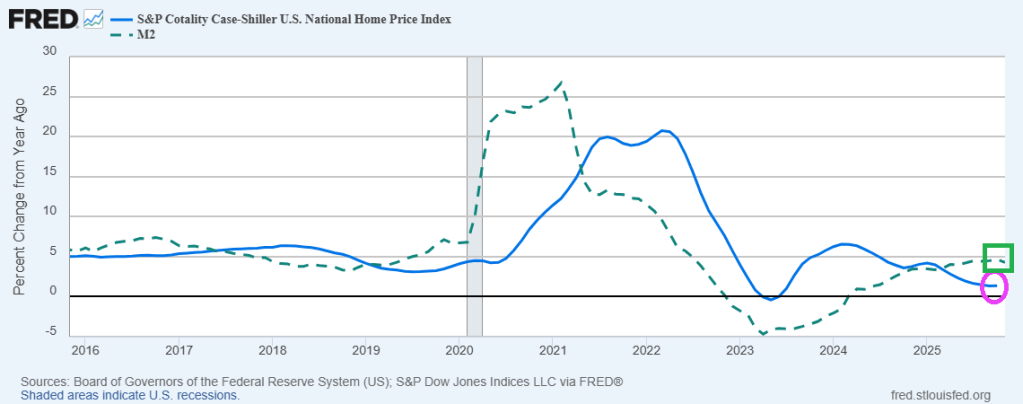

Housing price growth has stalled even though M2 money growth is higher YoY.

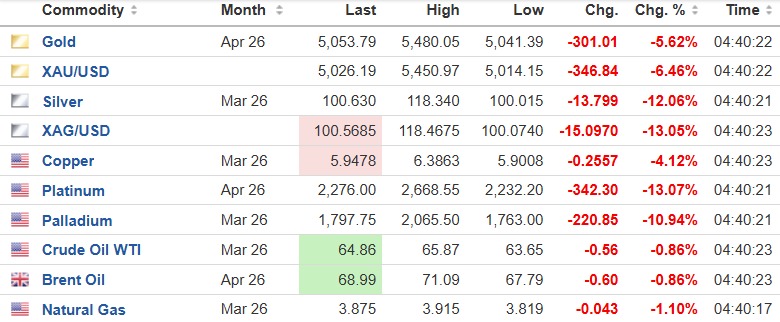

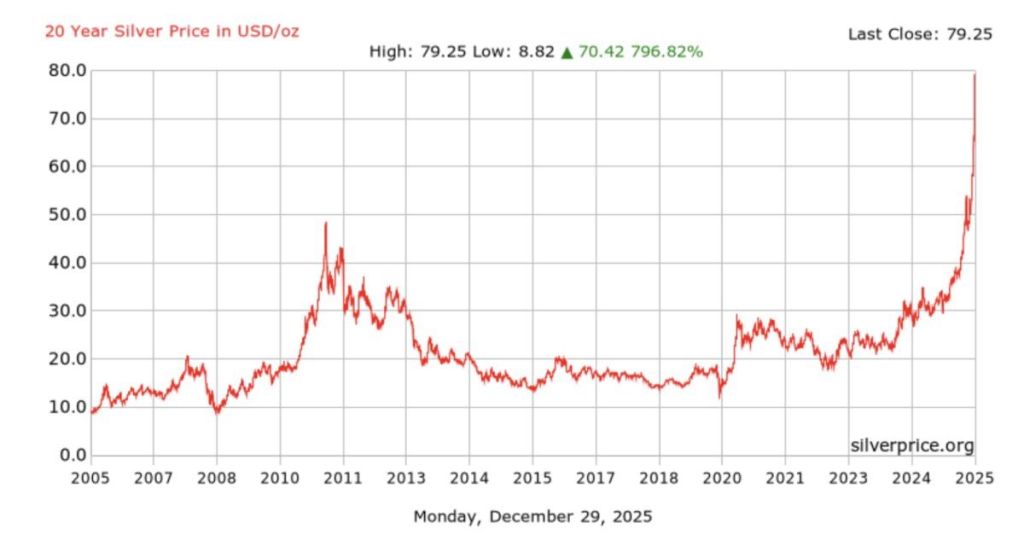

On the silver front, silver regained losses yesterday, but increased margin requirements are causing losses again.

{kind=link}

You must be logged in to post a comment.