They can’t accuse Fed Chair Jerome Powell of trying too hard to help Donald Trump. Mortgage rates moved lower last week, following declining Treasury yields as economic data releases signaled a weakening U.S. economy. As a result, the 30-year fixed rate decreased for the third straight week to 6.77 percent. As a result …

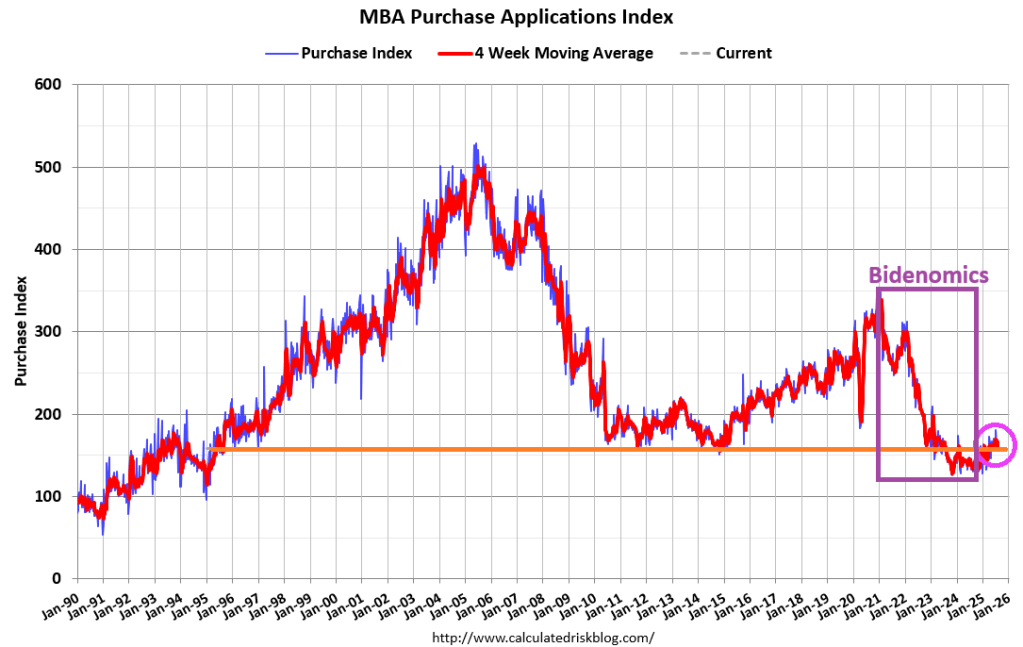

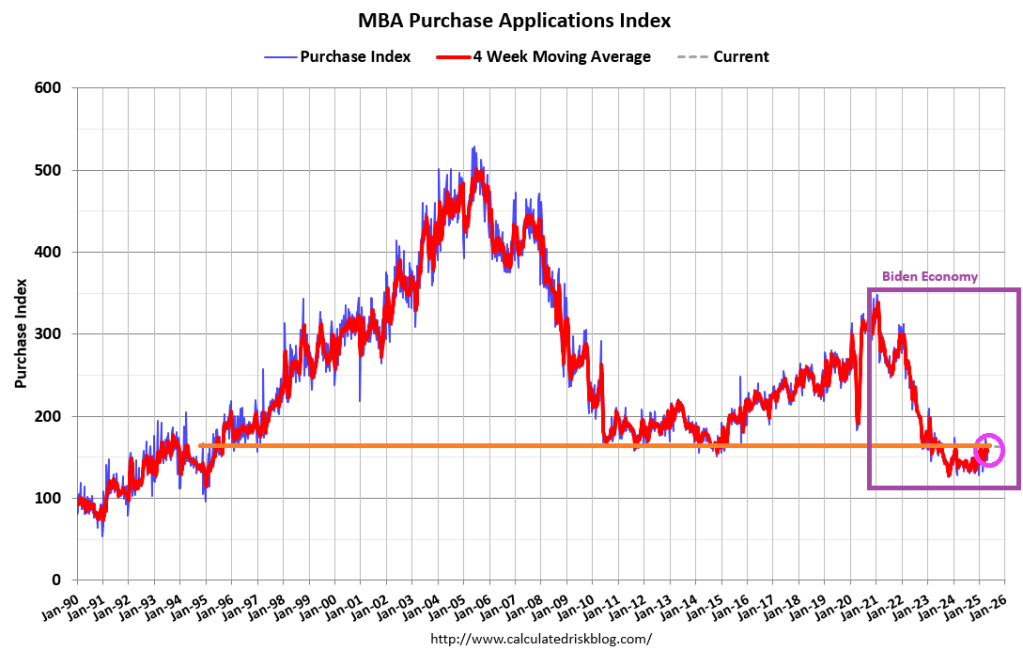

The Market Composite Index, a measure of mortgage loan application volume, increased 3.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 18 percent higher than the same week one year ago.

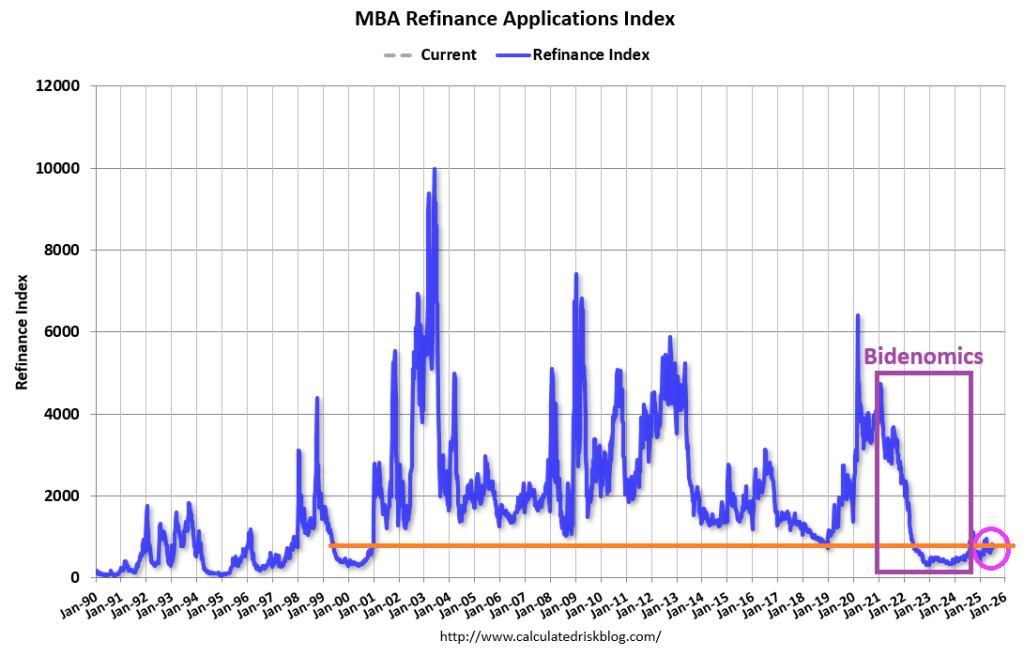

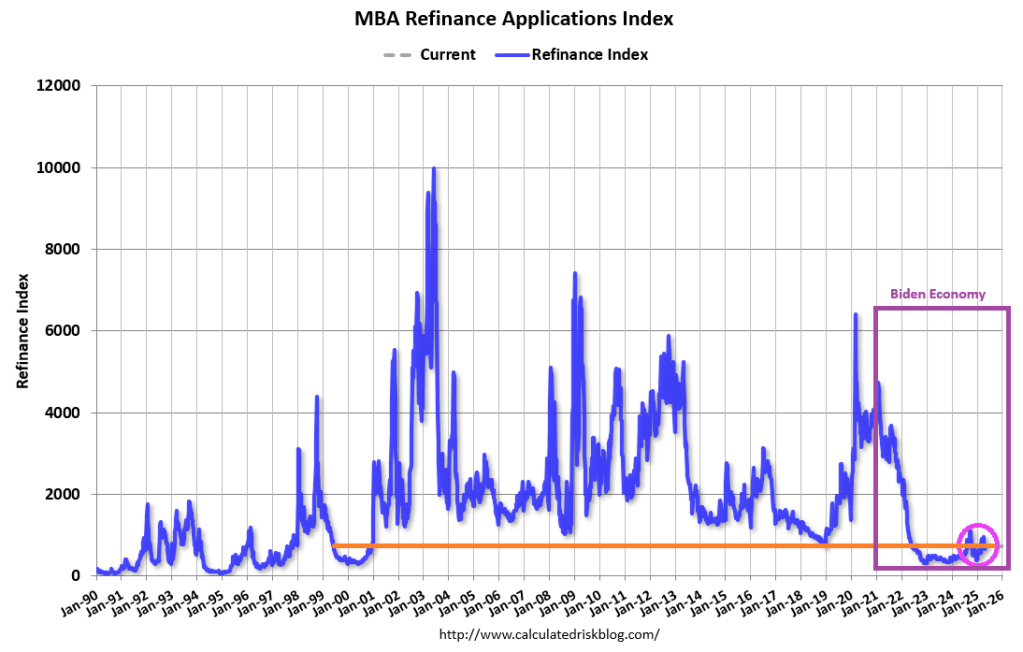

The Refinance Index increased 5 percent from the previous week and was 18 percent higher than the same week one year ago.

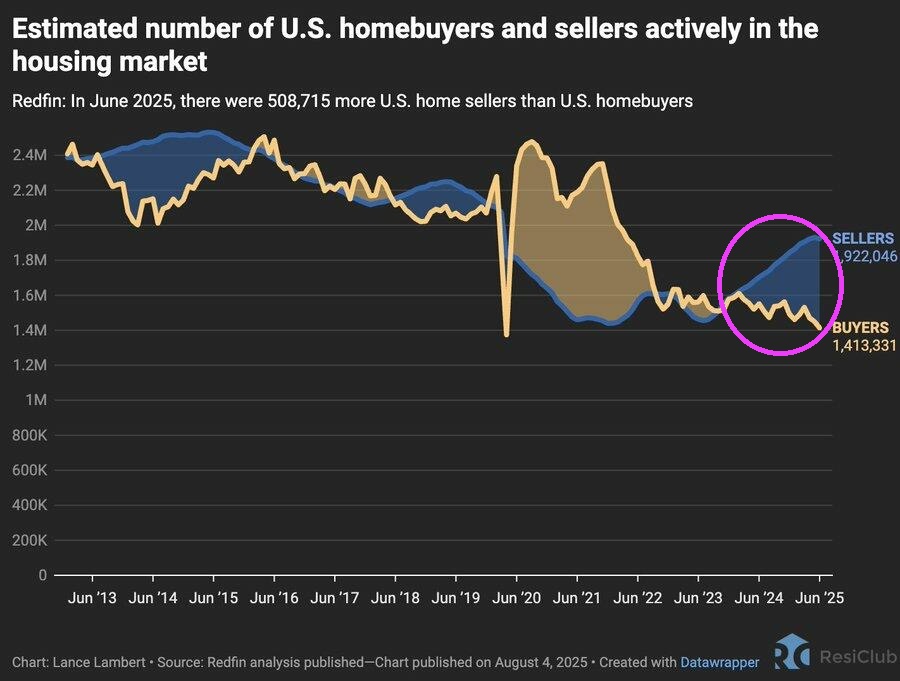

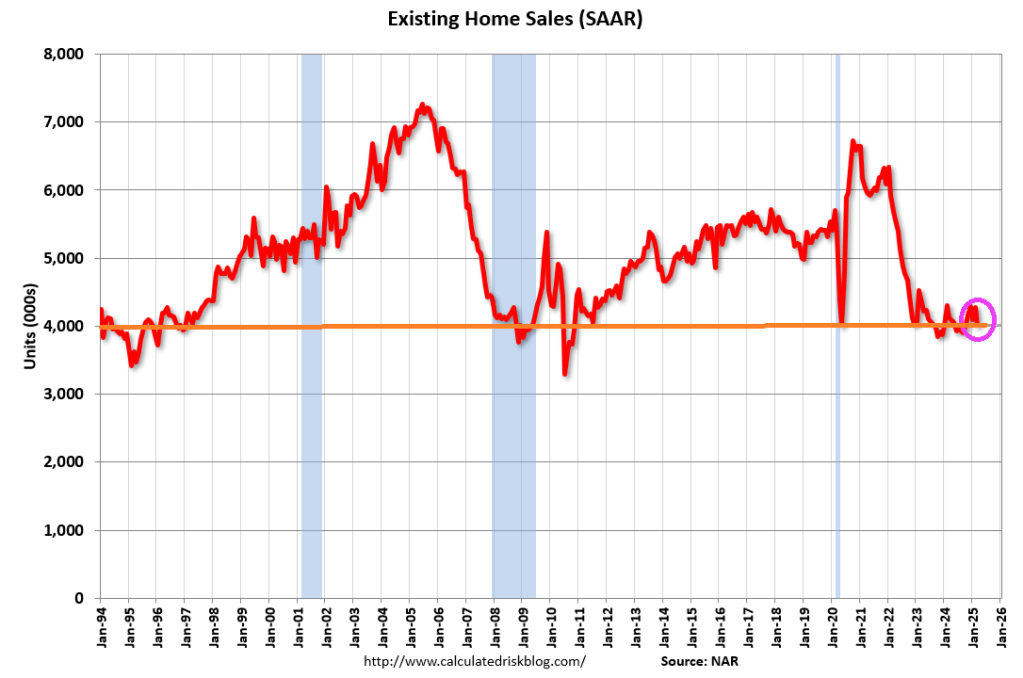

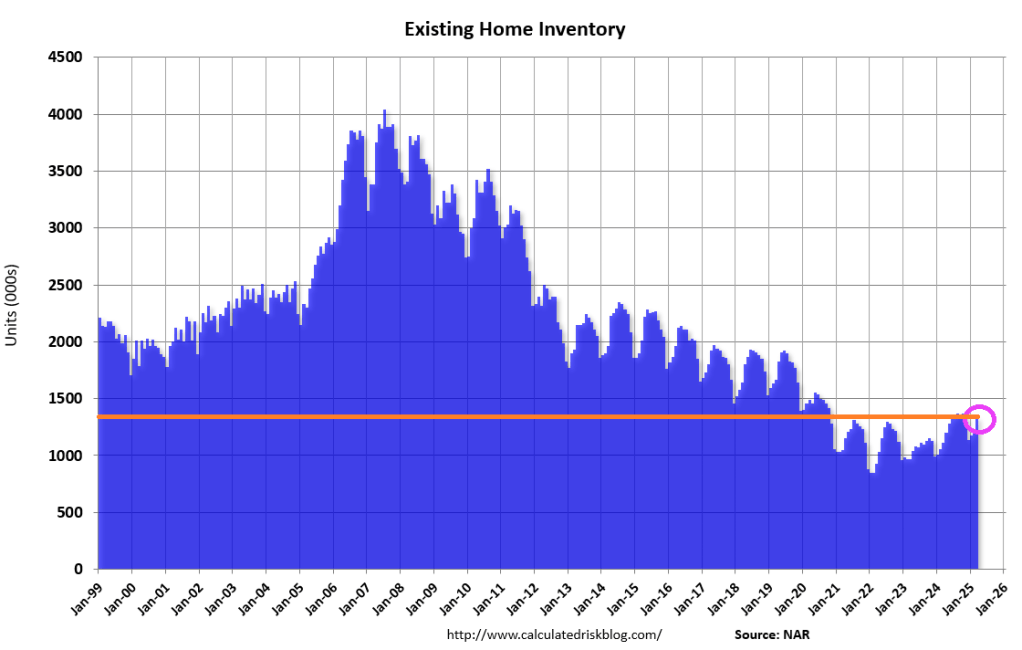

And the number of sellers in the housing market is greatly outweighing the number of buyers.

Mortgage and housing economists should breathe a sigh of relief that Bidenomics is over, but I doubt it they will.

You must be logged in to post a comment.