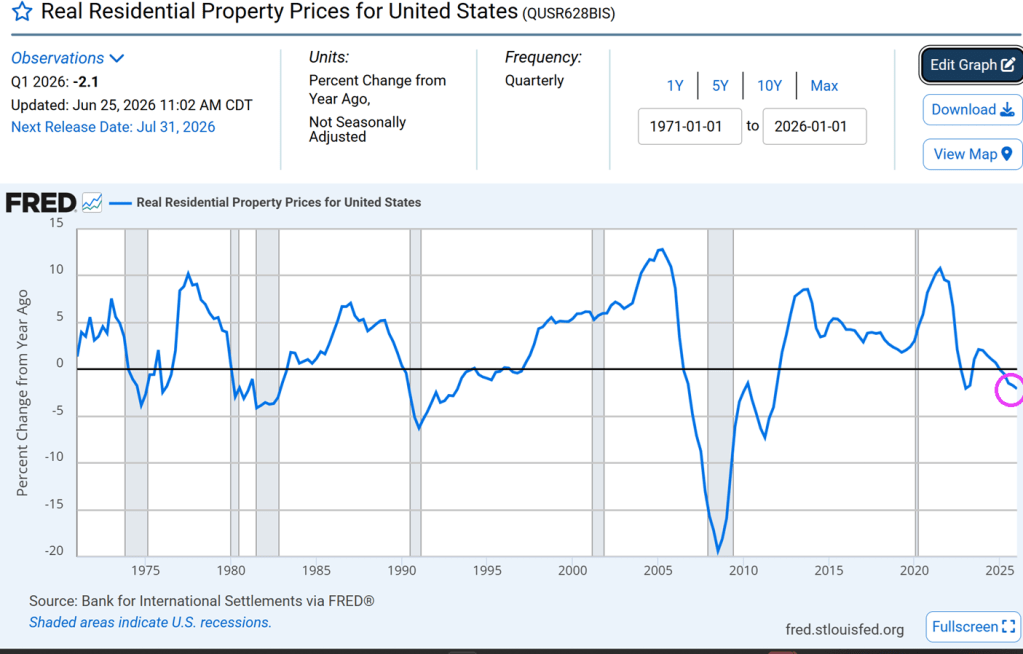

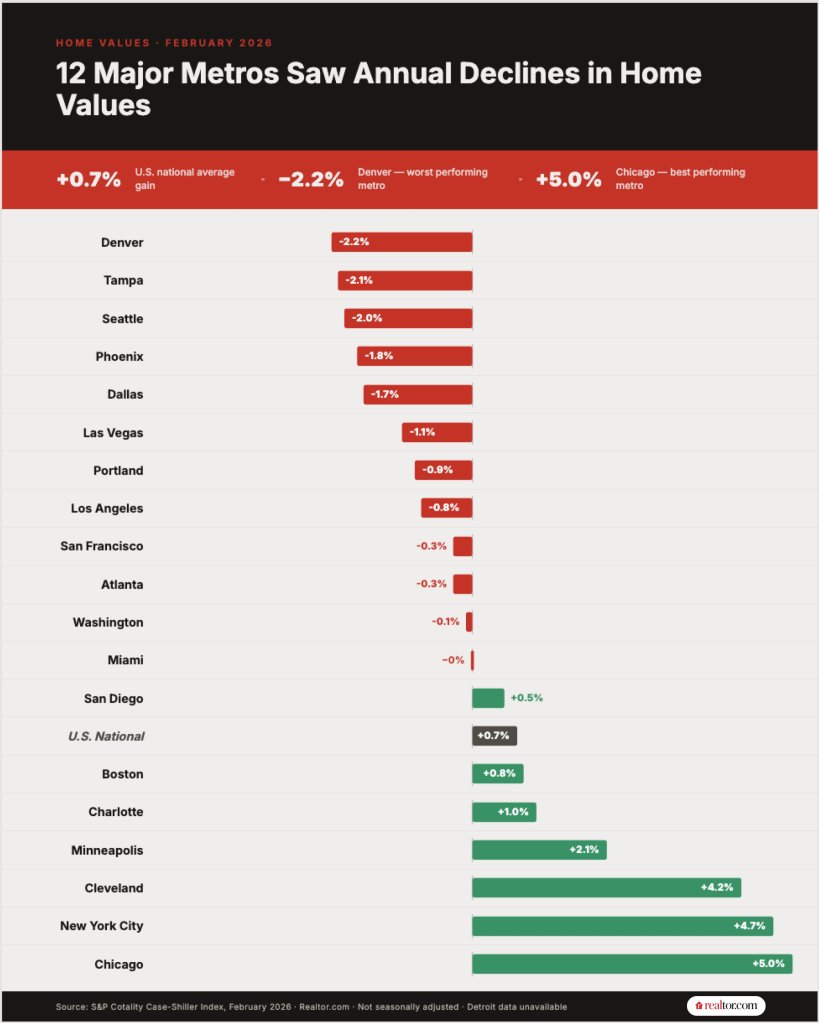

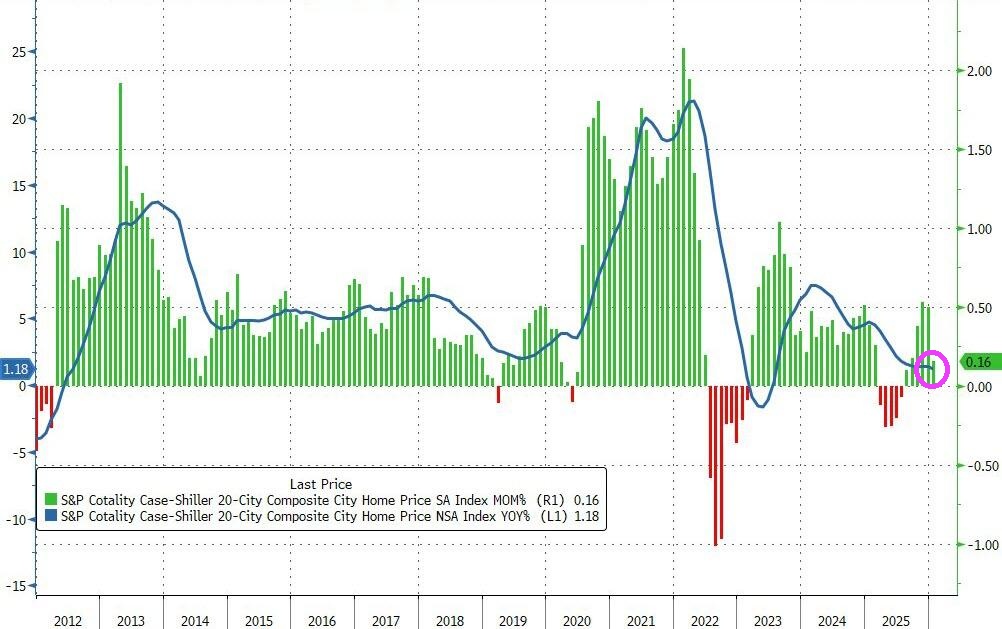

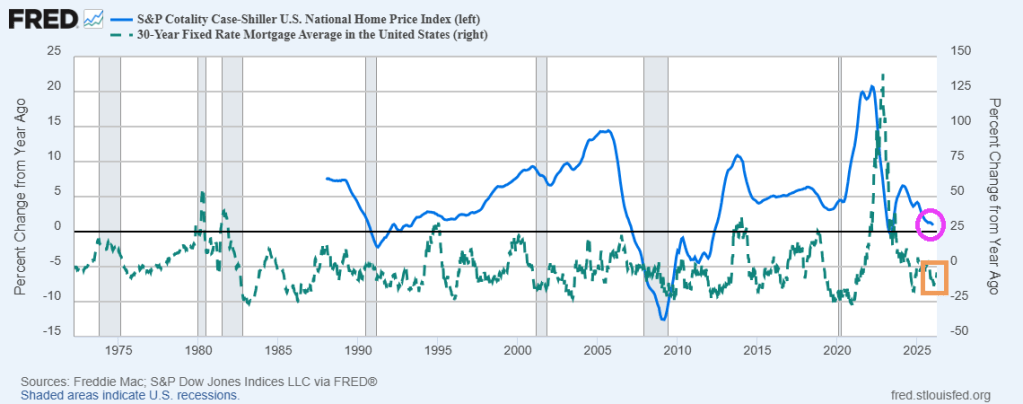

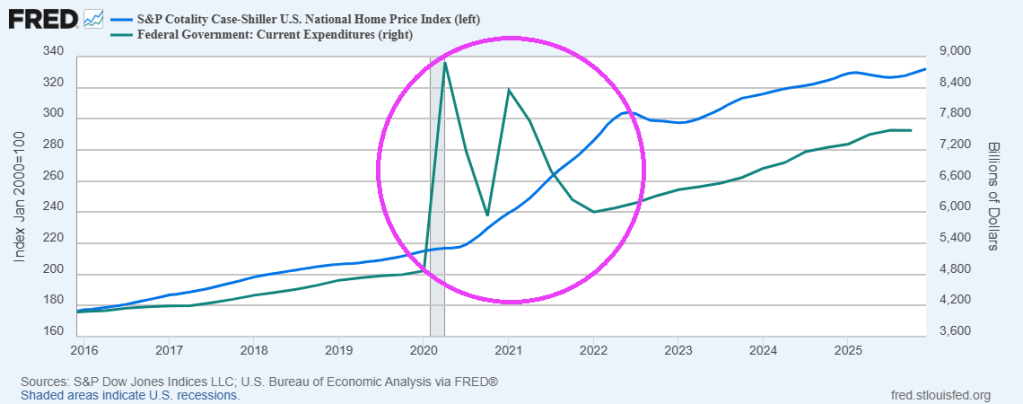

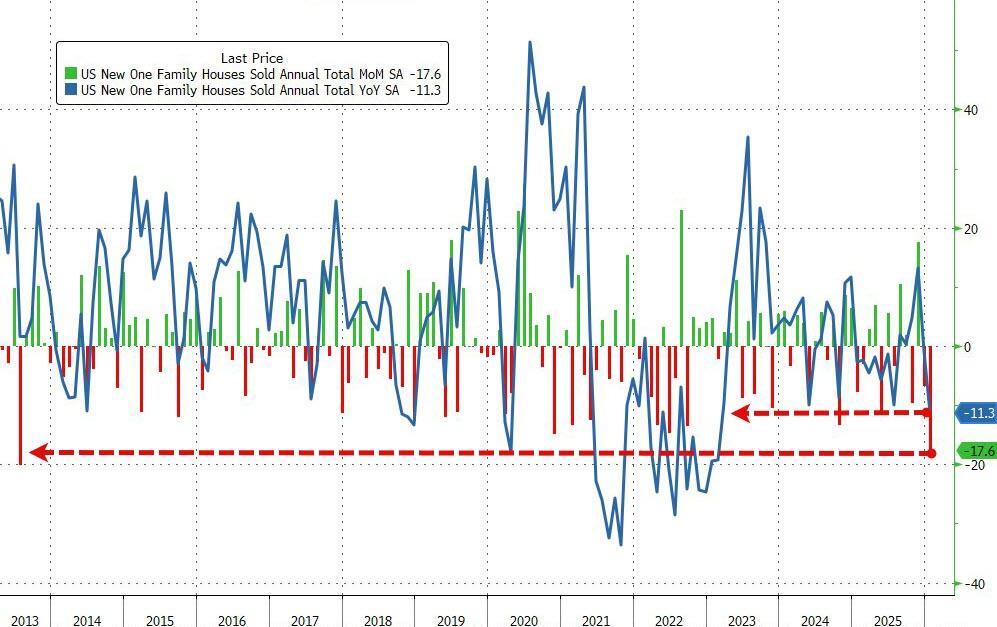

US home prices are clearly unaffordable for younger households, given the dearth of true starter homes. As of Q1 2026, REAL US residential property prices fell -2.1% YoY.

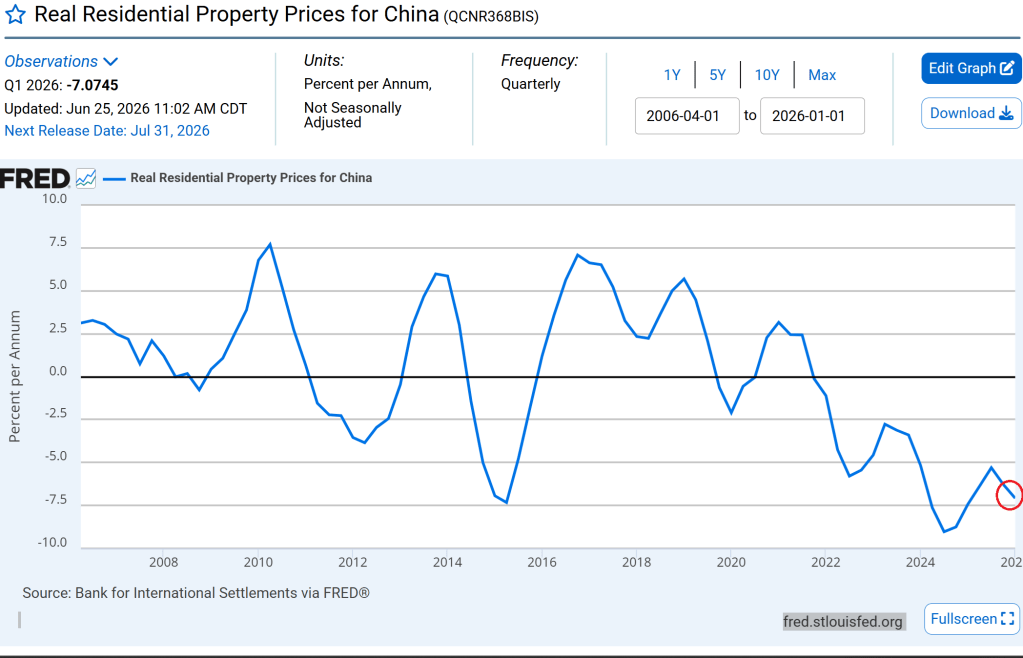

China’s real residential property prices are declining even faster than the US.

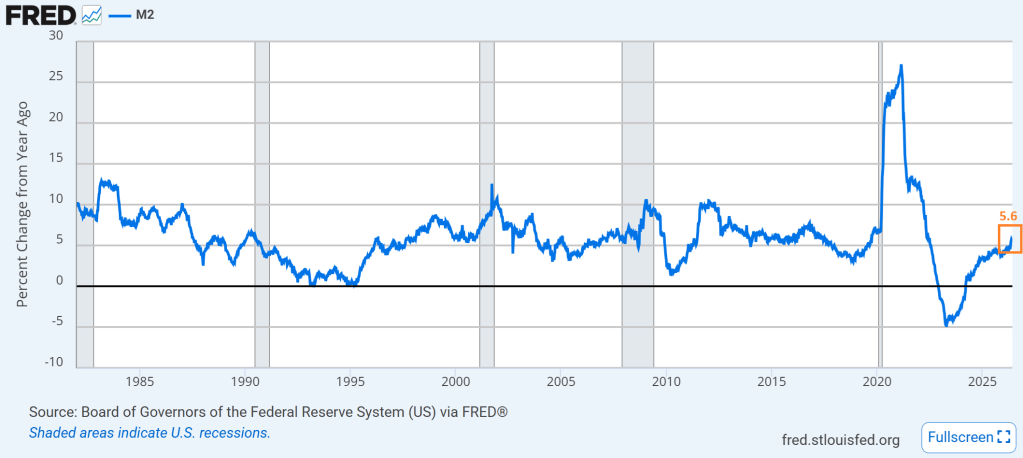

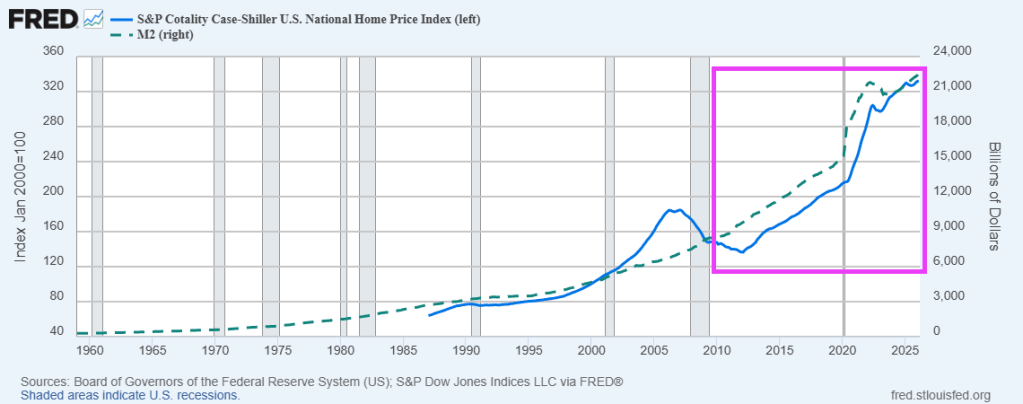

The US Federal Reserve is printing money M2 at a 5.6% YoY pace. Slower than during the Covid outbreak, and slower than the decade prior to Covid.

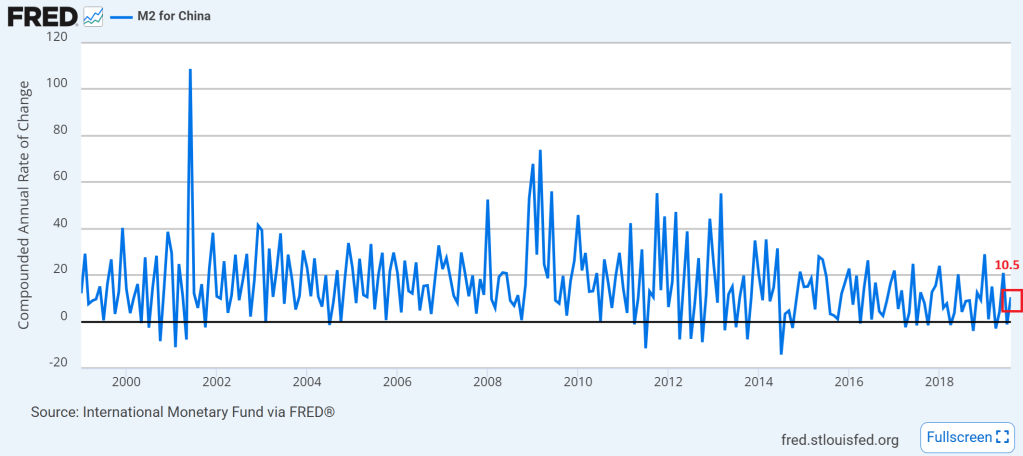

China is printing money at a gutwrenching pace (10.5% YoY as of August 2019). Note that China has historically printed money faster than The Federal Reserve.

Global Central Banks are the Neegans of the global economy.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.