As we are all aware, The Federal Reserve launched its monetary “stimulypto” in March 2020 to combat the Covid virus. Coupled with the surge in Federal stimulus, we have seen home prices rise over 20% since February 2020.

Specifically, New York City home prices are up 26.3% since February 2020, Chicago home prices are up 21.7%, and Los Angeles home prices are up 32.5%. Fed monetary stimulypto is up 113% since February 2020.

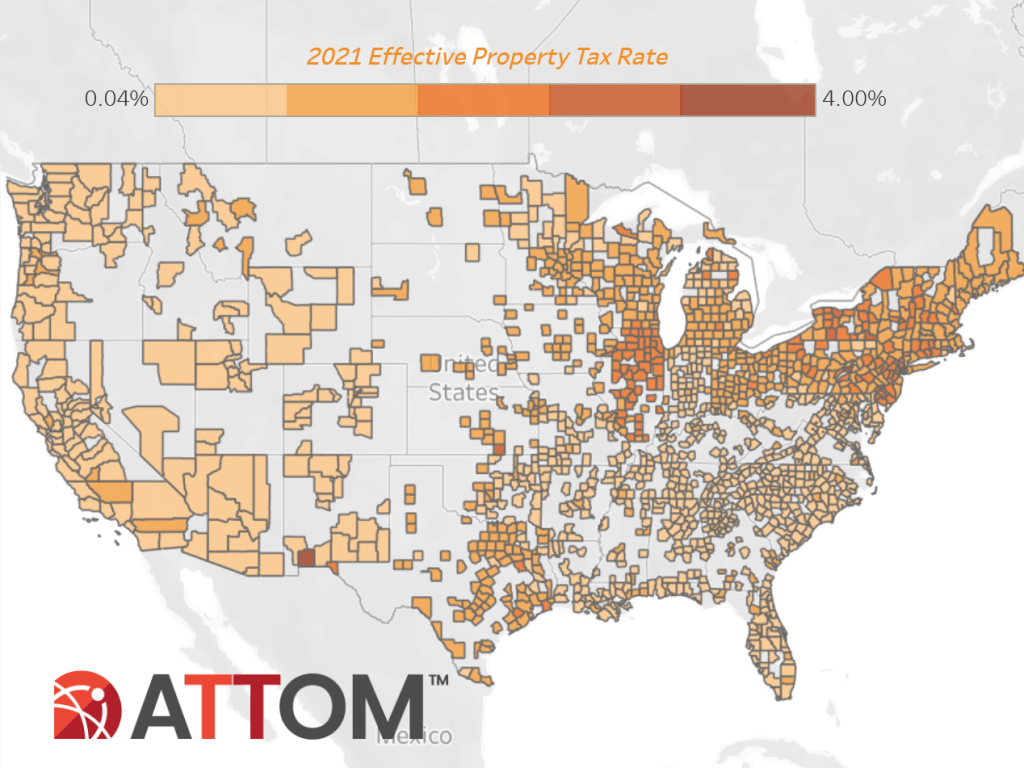

Of course, this has resulted in soaring PROPERTY TAXES as well. According to Attom Data Services, “Among 1,481 U.S. counties with at least 10,000 single-family homes in 2021, 16 had an average single-family-home tax of more than $10,000, including 12 in the New York City metro area. The top five were Kings County (Brooklyn), NY ($13,734); Marin County, CA (outside San Francisco) ($13,719); Westchester County, NY ($13,674); Essex County, NJ ($13,116) and Nassau County, NY ($13,095).”

Of course, not all metro areas raised their property taxes. Major markets with the largest decreases in average property taxes included Pittsburgh, PA (down 35.1 percent); New Orleans, LA (down 20.2 percent); Houston, TX (down 18.7 percent); Dallas, TX (down 12.2 percent) and Austin, TX (down 7.7 percent).

States with the highest effective property tax rates in 2021 were Illinois (1.86 percent), New Jersey (1.73 percent), Connecticut (1.67 percent), Vermont (1.55 percent) and Pennsylvania (1.37 percent).

Even if The Federal Reserve removes its massive monetary stimulypto (MMS), property taxes will remain elevated unless cities reduces their property tax rates. But Democrat-controlled cities tend to be addicted to spending much like The Federal government.

You might as well face it, they’re addicted to gov.

You must be logged in to post a comment.