Rate-cut expectations have surged (dovishly) higher this week (along with tumbling Treasury yields) amid a mixed macro picture (Labor market ‘good’, Retail sales bad, Housing ugly).

Today could change all that as CPI for January prints with risk skewed to the upside. January brings annual resets and they tend to surprise on the high side.

Despite the ‘hot’ whisper numbers (and 4 previous Januarys in a row of upside surprises), headline consumer price inflation came in cooler than expected in January (+0.2% MoM vs +0.3% expected). That pulled the headline CPI down dramatically from +2.7% to +2.4% – near the lowest in 4 years.

Core CPI printed +0.3% MoM (in line with expectations), lowering the YoY change in core prices to +2.5% – the lowest since March 2021.

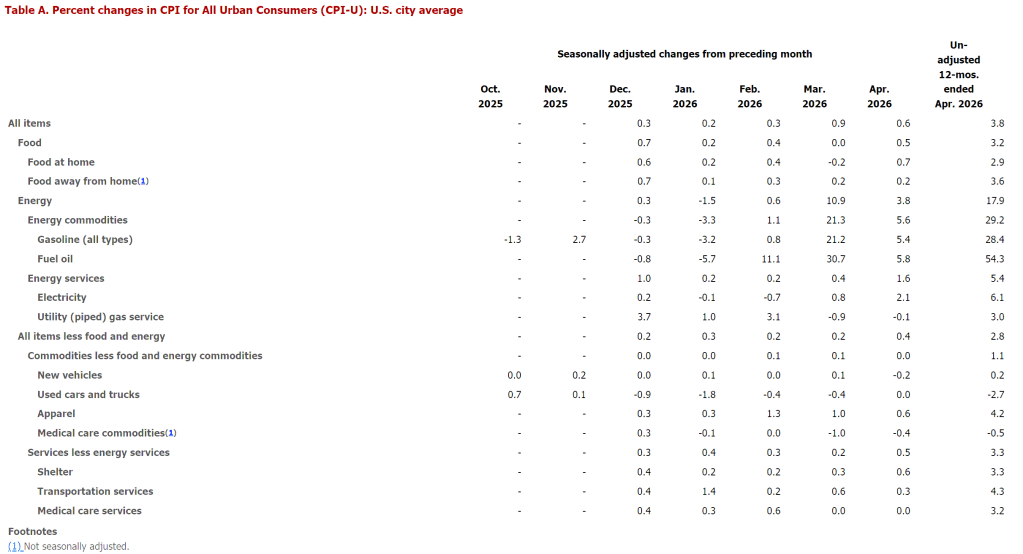

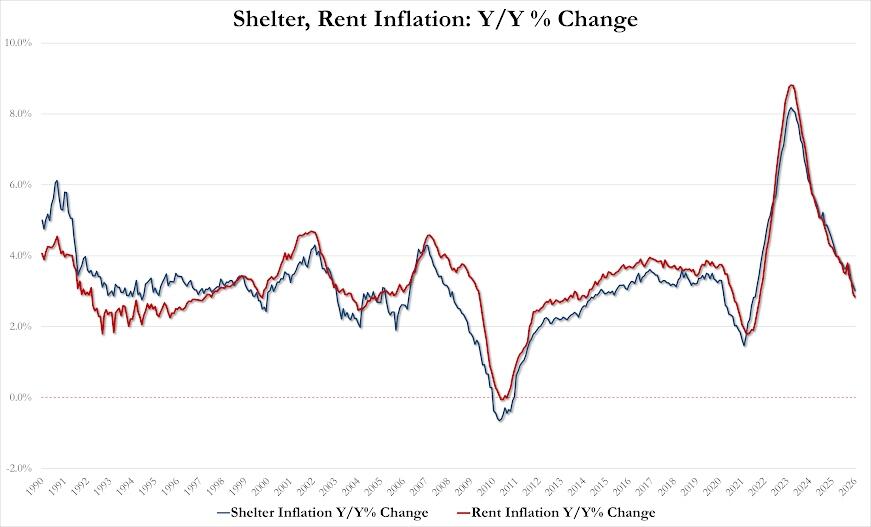

The Shelter index rose 0.2% in January and was the largest factor in the all items monthly increase. The food index increased 0.2% over the month as did the food at home index, while the food away from home index rose 0.1 percent. These increases were partially offset by the index for energy, which fell 1.5% in January.

January saw real average weekly earnings rise 1.9% YoY – its highest since March 2021…

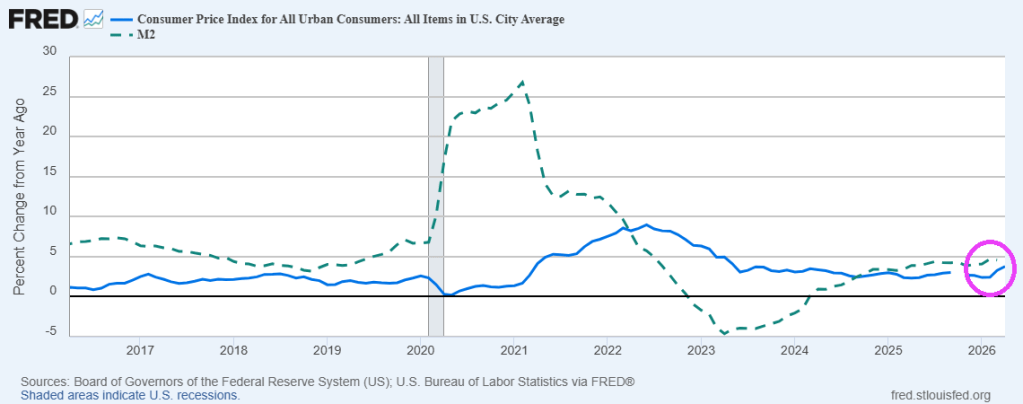

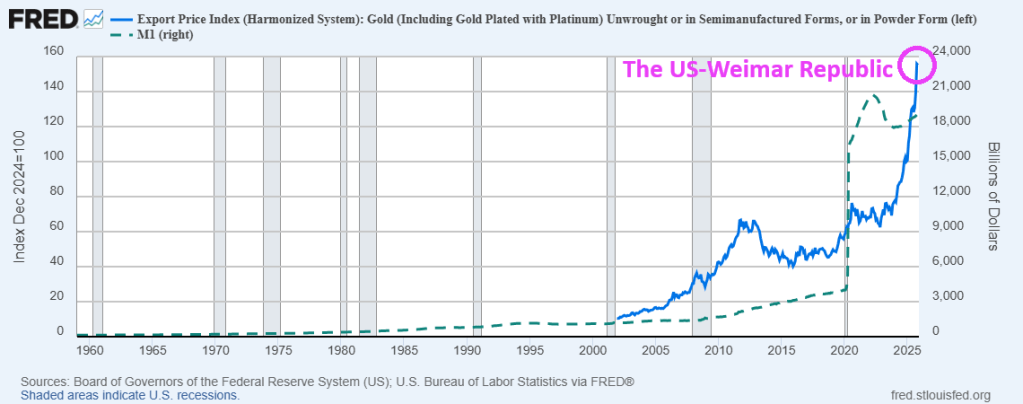

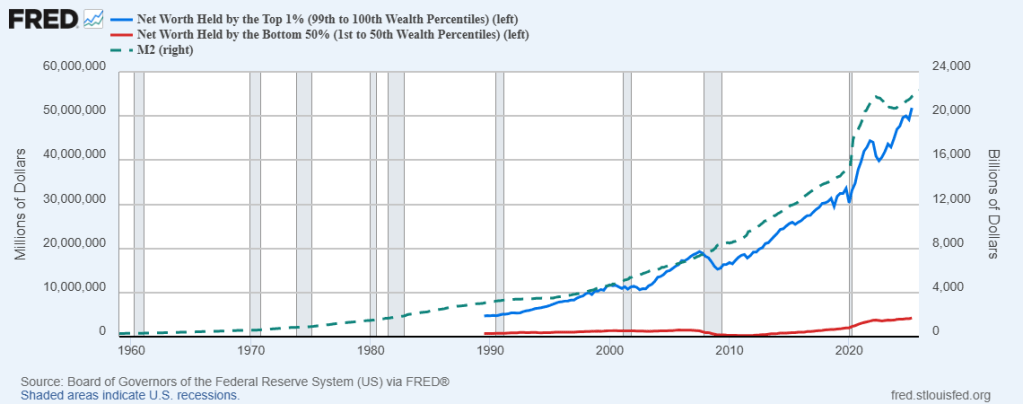

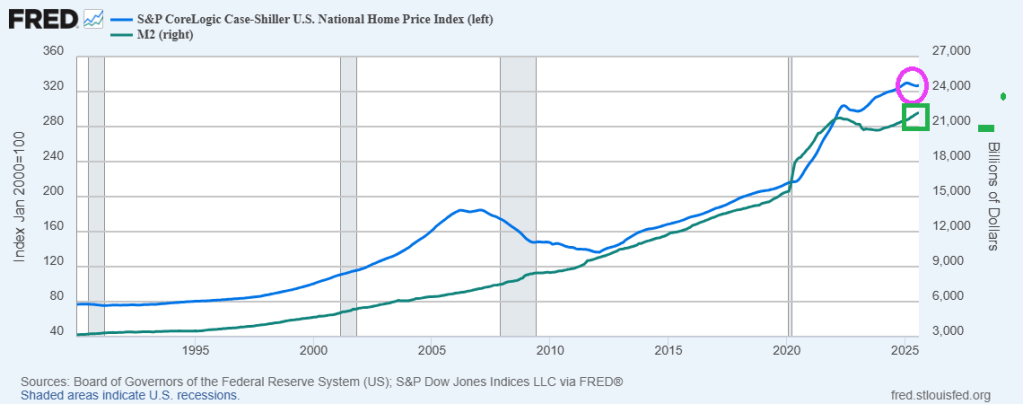

The Federal Reserve prints a lot of money (M2). Unfortunately, it largely benefits elites (the top 1%). The bottom 50% get some benefits, but the gains in net worth largely benefits the elite class.

This sounds like a legal Somali daycare scheme. Perhaps The Fed should be renamed “The Federal Quality Learing Center.”

Yes, Somalis have daycare centers in Columbus Ohio. Thanks Governor Dewine for doing absolutely nothing to reign in their fraud. /sarc

{kind=link}

You must be logged in to post a comment.