The South Florida housing market is sizzling with hot money from the North East, pushing up homes values sky high over the last year. One example of the mania is in Palm Beach, where a private island was bought in July and was relisted months later for a whopping 41% premium, according to WSJ.

One of Miami’s top real estate developers, Todd Michael Glaser, is taking advantage of the bubble, fueled by Wall Street bankers and other elites who have the economic mobility to leave the Northeast for the Sunshine State.

Glaser purchased 10 Tarpon Way, also known as 10 Tarpon Isle, for approximately $85 million in July and has since relisted the tiny 2.5-acre island for $120 million, or $35 million more than he paid a few months ago. The island was created by dredging crews in the 1930s and is only accessible by bridge. Glaser bought the island from private investor William M. Toll and his wife, Eileen, who paid $7.6 million for the property in 1998.

Tarpon Island

The real estate developer said potential buyers have two options: pay the $120 million now or wait ten months for a new renovation for $200 million.

Concept Drawing Of New Renovation

He said with all the hot money flowing into the Palm Beach area, “a $100 million house isn’t that crazy anymore, believe it or not,” adding that in the last 18 months, eight $100 million homes have been sold.

If a potential buyer wants to wait ten months and pay an additional $80 million. The developer will completely redesign the mansion by doubling it to 25,000 sqft, with 14 bedrooms, in addition to a hair salon, gym, and spa. A new pool, octagonal tennis pavilion, and a golf practice area will be installed on the outside.

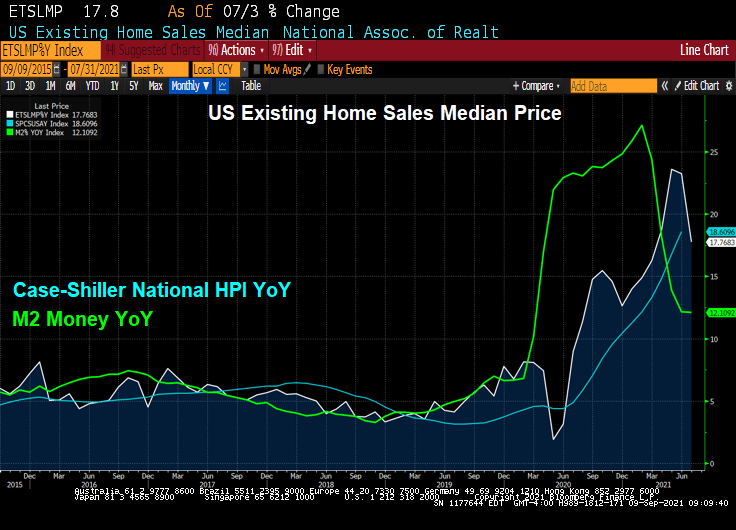

Some ask how long will this speculation fever last as the Federal Reserve could embark on tapering its extensive bond-buying program later this year or early 2022.

One real estate expert believes the peak of the South Florida housing market could be nearing:

Dr. Ken Johnson, a real estate economist with Florida Atlantic University’s College of Business, told local news WPLG that a peak in the housing cycle could have already arrived, but he believes a crash is not in the mix because demand still outpaces supply.

It remains to be seen if some greater fool will pay the $120 million for the island mansion or $200 million tens months later after renovations.

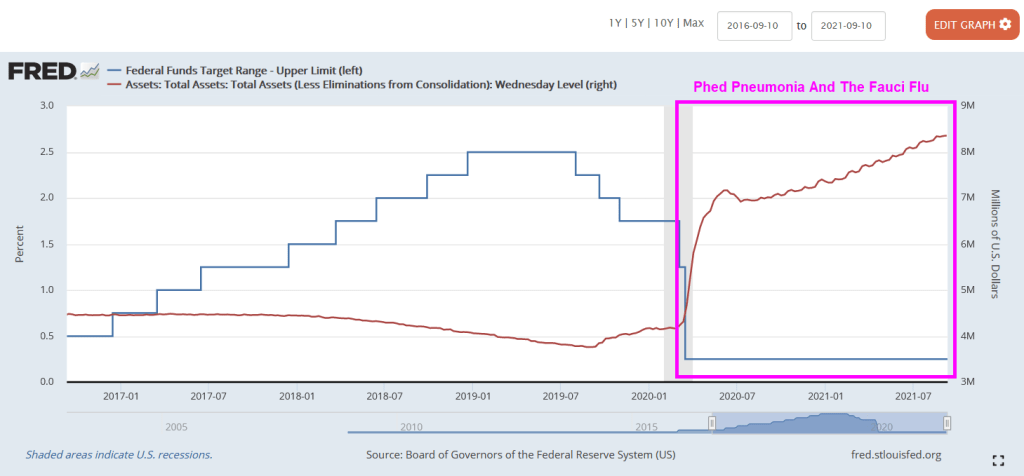

Time for The Fed to start tapering the punchbowl?

{kind=link}

{kind=link}

You must be logged in to post a comment.