Despite the slump in ‘soft’ survey data, analysts expected Empire Fed Manufacturing to bounce back from March’s tumble to one year lows and they were right with the headline index rising from -20.0 to -8.1 (considerably better than the -13.5), but still negative. However, while current conditions jumped, expectations plunged to the lowest since 9/11/.

US Treasury Secretary (and former Fed Chair) Janet Yellen says the US economy is in excellent shape. Is she a genius and sees something that rest of us don’t? Or is she a partisan thug like Shap Shot’s Gilmore Tuttle?

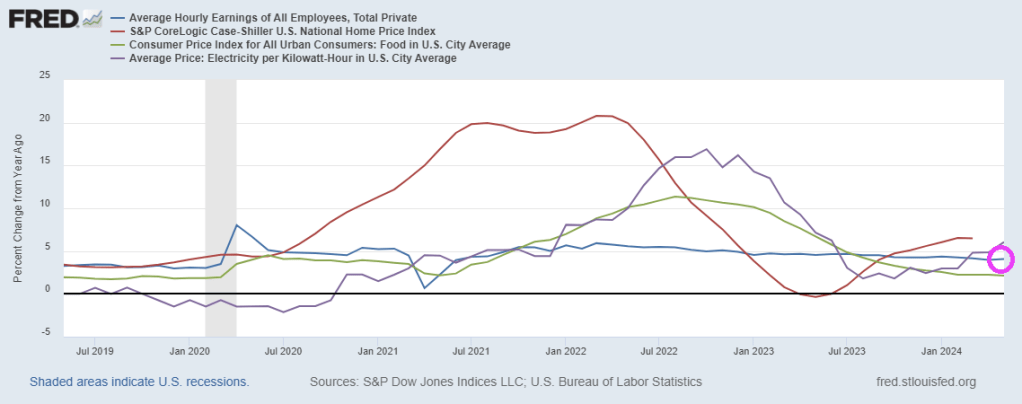

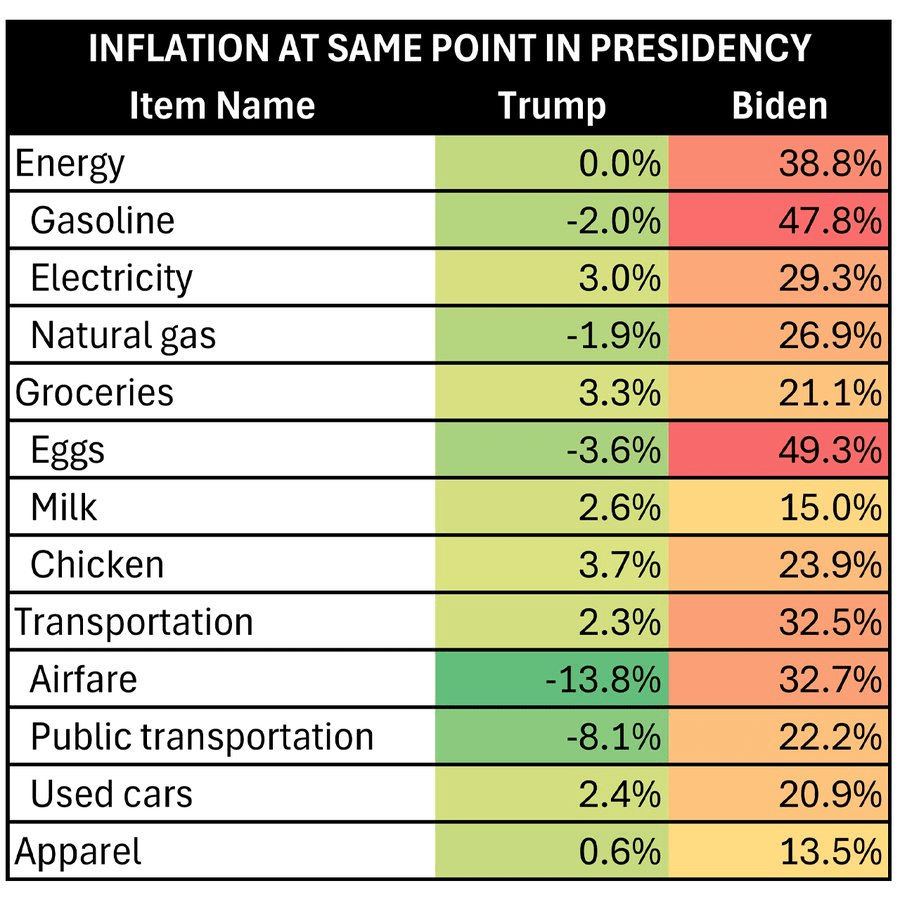

Yellen brags about rising wages and declining inflation. Well, average hourly earnings YoY are now 4.1%. However, home prices are growing at 6.5% year-over-year (YoY) and electricity prices are up 6.1% YoY. Food CPI grew at 2.1% in May. Yellen ignores the string of 10%+ increases in 2022-2023 making eating unaffoprdable for millions.

I doubt if Yellen could run a lemonade stand in my neighborhood. But like Gilmore Tuttle, maybe she could run a donut shop!

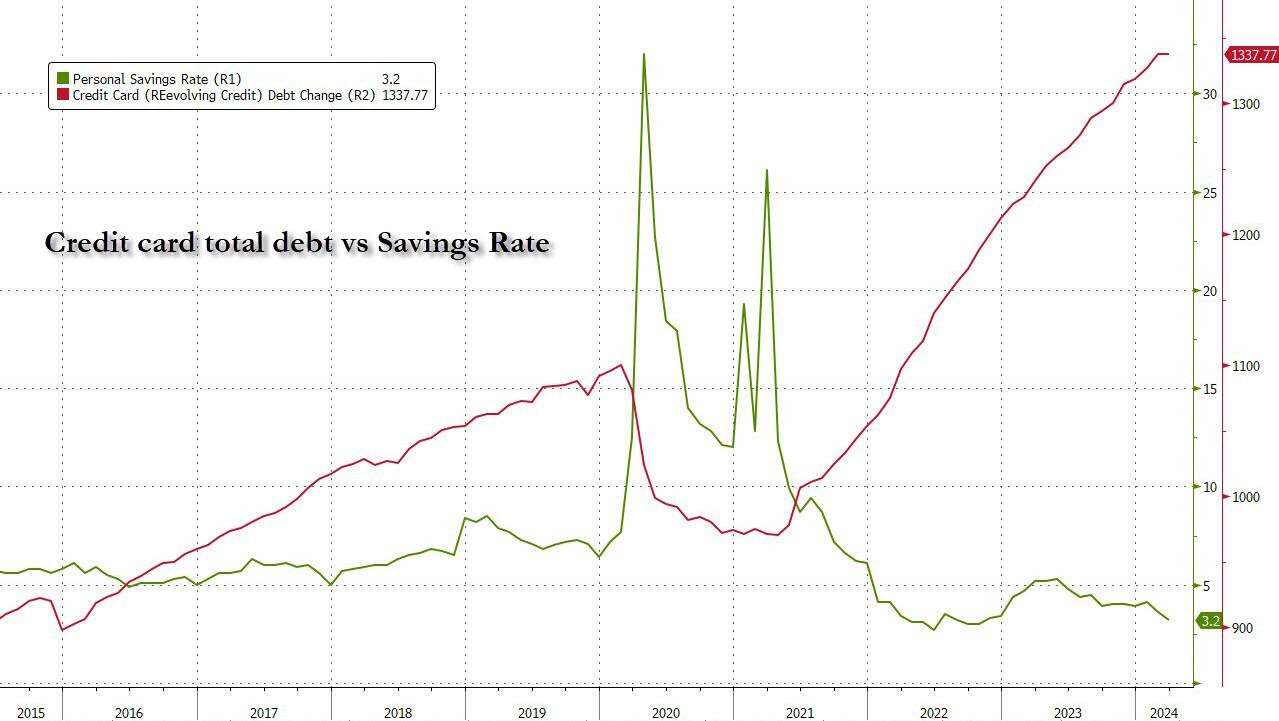

To be sure, credit card debt is just a small portion (~6%) of the total household debt stack: as the next chart from the latest NY Fed consumer credit report shows, the bulk, or 70%, of US household debt is in the form of mortgages, followed by student loans, auto loans, credit card debt, home equity credit and various other forms. Altogether, the total is a massive $17.5 trillion in total household debt.

But staggering as the mountain of household debt may be, at least we know how huge the problem is; after all the data is public. What is far more dangerous – because we have no clue about its size – is what Bloomberg calls “Phantom Debt“, and have repeatedly called Buy Now, Pay Later debt. How much of that kind of debt is out there is largely a guess.

But while it is easy to ensnare young, incomeless Americans into the net of installment debt where they will rot as the next generation of debt slaves for the rest of their lives, there is an even more sinister side to this extremely popular form of debt which allows consumers to split purchases into smaller installments: as Bloomberg reports in a lengthy expose on installment debt, the major companies that provide these so called “pay in four” products, such as Affirm Holdings, Klarna Bank and Block’s Afterpay, don’t report those loans to credit agencies. That’s why Buy Now/Pay Later credit has earned a far more ominous nickname:

It’s hard enough for central bankers and Wall Street traders to make sense of the post-pandemic economy with the data available to them. At Wells Fargo & Co., senior economist Tim Quinlan is particularly spooked by the “phantom debt” that he can’t see.

Which is not to say that we have no idea how much “phantom debt” is out there: according to the report, it is projected to reach almost $700 billion globally by 2028, and yet, time and again, the companies that issue it have resisted calls for greater disclosure, even as the market has grown each year since at least 2020. That, as Bloomberg accurately warns, is masking a complete picture of the financial health of American households, which is crucial for everyone from global central banks to US regional lenders and multinational businesses.

In fact, the recent explosion in installment debt may explain why the US consumer remains so resilient even when most conventional economic metrics suggest consumers should be struggling: “Consumer spending in the world’s largest economy has been so resilient in the face of stubbornly high inflation that economists and traders have had to repeatedly rip up their forecasts for slowing growth and interest-rate cuts.”

Still, cracks are starting to form. First it was Americans falling behind on auto loans. Then credit-card delinquency rates reached the highest since at least 2012, with the share of debts 30, 60 and 90 days late all on the upswing.

And now, there are also signs that consumers are struggling to afford their BNPL debt, too. A recent survey conducted for Bloomberg News by Harris Poll found that 43% of those who owe money to BNPL services said they were behind on payments, while 28% said they were delinquent on other debt because of spending on the platforms.

For Quinlan, a major concern is that economic experts are being “lulled into complacency about where consumers are.”

“People need to be more awake to the risk of BNPL,” he said in an interview.

Well, those who care, are awake – we have written dozens of articles on the danger it poses; the problem is that those who are enabled by this latest mountain of debt – such as the Biden administration which can claim a victory for Bidenomics because the economy is so “strong”, phantom debt be damned – are actively motivated to ignore it.

So why is this latest debt bubble called a “phantom”?

Well, BNPL is a black box largely because of a longstanding blame game among BNPL providers and the three major credit bureaus: TransUnion, Experian and Equifax. The BNPL companies don’t provide data on their installment loans that are split into four payments, which were used by online shoppers to spend an estimated $19.2 billion in the first quarter, according to Adobe Analytics, up 12.3% compared with the same period last year.

The BNPL giants say credit agencies can’t handle their information — and that releasing it could harm customers’ credit scores, which are key to securing mortgages and other loans. The big three bureaus say they’re ready, while two of the major credit scoring firms, VantageScore Solutions and Fair Isaac Corp. (FICO), say they’re equipped to test how the products will affect their figures. Meanwhile, regulation is looming over the industry, but this stalemate has left the status quo mostly in place.

In other words, not only do we not know just how big the BNPL problem is, it is actively masked by credit agencies which can’t accurately calculate the FICO score of tens of millions of Americans, and as a result their credit capacity is artificially boosted with far more debt than they can handle… and that’s why the US consumer has been so “strong” in recent years, defying all conventional credit metrics.

The good news is that despite the tacit pushback of the administration, there has been some signs of progress. Apple earlier this year became the first major BNPL provider to furnish transaction and payment data to Experian. As of now, it provides a snapshot of consumers’ overall debt load from Apple Pay Later transactions, but the information won’t be used for consumer credit scores. In separate statements to Bloomberg, Klarna, Affirm and Block said they want assurance that consumers’ credit scores and their data would be protected before reporting customer information. Representatives for TransUnion, Experian and Equifax said they’ve updated their structures and the data would be secure.

Still, the lack of transparency has researchers at the Federal Reserve Bank of New York, which publishes a comprehensive quarterly report on the $17.5 trillion in US household debt, convinced they’re missing some of what’s happening in the economy.

“They’ve reached a certain scale that they could impact economists’ assumptions about their economic outlooks,” said Simon Khalaf, Chief Executive Officer of Marqeta Inc., a firm that helps BNPL providers process their payments.

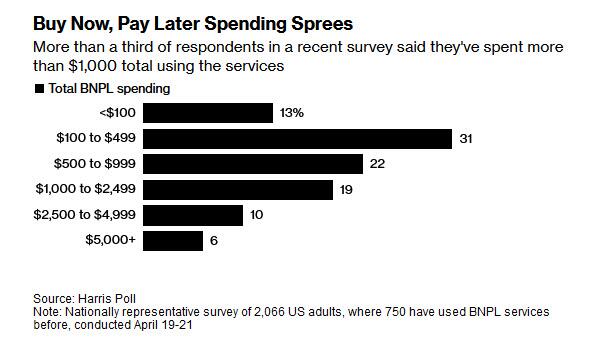

Meanwhile, the pernicious effects of BNPL credit are piling up: the Harris Poll survey conducted last month, provides some crucial clues about how Americans use BNPL. For one, splitting payments into smaller chunks encourages more spending, obviously.

More than half of respondents who use BNPL said it allowed them to purchase more than they could afford, while nearly a quarter agreed with the statement that their BNPL spending was “out of control.” Harris also found that 23% of users said they couldn’t afford the majority of what they bought without splitting payments, while more than a third turned to the services after maxing out credit cards.

The findings also show that the spending, which for more than a third of users has exceeded $1,000, isn’t entirely on big-ticket items. Almost half of those using BNPL say they’ve started, or have considered, using it to pay bills or buy essential items, including groceries.

Translation: Americans are no longer even charging everyday purchases they traditionally used cash and savings to pay for; now they are using installment plans to pay for bread!

It’s not just the lower classes that are abusing BNPL credit: while whatever small pockets of consumer distress have emerged so far in the US, have been chalked up to a bifurcated economy where working class Americans struggle to make ends meet, the survey found that middle-class households are relying on BNPL, too. The shocking punchline: about 42% of those with household income of more than $100,000 report being behind or delinquent on BNPL payments!

“BNPL essentially lets people dig a deeper and deeper hole of credit, which will be harder and harder to climb out of,” said Ed deHaan, a professor of accounting at Stanford Graduate School of Business, adding that it happens “more easily when there’s no transparency.”

Of course, installment debt is nothing new: the option to pay in installments using short-term loans has been around for a ong time, but it exploded in popularity during the pandemic, especially with younger, digitally savvy consumers who gravitated to the services as an alternative to credit cards. The pioneering BNPL companies, including Afterpay, Klarna and Affirm, launched with trendy retailers, partnered with social media influencers and became a common option on apps and online checkouts.

BNPL offers quick credit approvals and lets consumers pay in installments. The first is usually due right away, and the others are often collected once every two weeks for the popular “pay in four” loans. There’s typically no interest or fees, as long as payments are made on time. Like credit card companies, BNPL firms make money on fees from merchants — and some have steep penalties for missed payments.

While normally larger banks would avoid this kind of “new and much more dangerous subprime”, this time is different: the rapid adoption of the products has enticed major financial institutions to offer the option to split payments, even as regulators warn them of the risks. That includes PayPal, U.S. Bancorp and Citizens Financial. Even big banks like Citigroup and JPMorgan have similar capabilities on their credit cards.

The industry has branded itself a financial equalizer. They argue that “soft-credit checks” — when a lender runs a consumer’s credit history without affecting their score — expand credit access to those underserved by traditional lenders, while zero-interest provides a better deal than many cards.

Affirm said its customers have an average outstanding balance of $641, while Afterpay and Klarna put the figure at $250 and $150, respectively. Unfortunately, there is no way to check these numbers. And while the average credit card balance was $6,501 in the third quarter of 2023, according to Experian data, the BNPL balances mean that most Americans can’t even afford a weekly outing to their grocery store without putting it on an installment plan, a truly terrifying scenario.

Critics naturally argue that BNPL is particularly attractive to the financially vulnerable. The Consumer Financial Protection Bureau has flagged risks to consumers, including surprise late fees and “hidden interest” — or when BNPL purchases are made with credit cards charging high interest rates. The CFPB has also expressed concern about “loan stacking,” when individuals take out several BNPL loans at once with different providers, which is most of them.

Some BNPL services, including Afterpay and Klarna, require borrowers to agree to “mandatory autopayment,” meaning the companies can automatically charge the credit card or bank account on file when a payment is due. Those who link the latter are potentially vulnerable to overdraft fees.

Meanwhile, as rates remains sky high, even Wall Street’s perpetually cheerful analysts are wondering where is all the consumption coming from?

Robust consumer spending and low unemployment rates have many economists convinced the US consumer remains strong, making Wall Street bullish on the economy. But lately, stubbornly persistent inflation has dialed back expectations for imminent interest-rate relief.

That’s set to ramp up pressure on households that are already stretched thin by higher prices for everything from gas and food to rent and apparel. As of the end of December, almost 3.5% of credit-card balances were at least 30 days past due, according to the Philadelphia Fed, the most since the data began in 2012. Nominal card balances also set a new high.

For those who are falling behind, BNPL offers what appears to be a no-brainer decision: space out payments… at least until this last credit buffer fills up and bankruptcy is the only possible outcome.

That was the thinking of Hayden Waschak, a 23-year-old in Pittsburgh. Even though he said it felt “dystopian” to use BNPL to pay for food, he began using Klarna in February to spread out payments on a grocery delivery app. It helped his finances — at first. After he lost his job as a documents processing specialist at University of Pittsburgh Medical Center in March, he relied more heavily on the service. And without any income, he became delinquent on payments and started racking up late charges. He eventually paid off the nearly $200 balance, but he said his credit score dropped.

“Unexpected life events caused me to lose income,” Waschak said. “I ended up paying more than if I had paid for it all at once.”

Meanwhile, the fact that BNPL balances do not count against your credit rating, means users get little upside when it comes to their credit — paying on time won’t help them build up their score. On the other hand, the downside is still there for falling behind: not only can they get charged late fees, but delinquent BNPL loans can be turned over to debt collectors.

The latter is what Fabrizio Lopez said happened to him. He used Affirm to split up a $500 online payment for used-car parts in 2019. The Long Island-based mechanic, who doesn’t have a traditional credit card, said that while he received the items a week later, he never got a bill. That is, until debt collection letters started pouring in from across the US.

Lopez said he primarily relied on cash before that purchase, so the unpaid loan stands out on his credit profile. Now 30, he worries that a the BNPL purchase has created “invisible barriers” to the financial system.

“They hook you with the idea of no interest rates,” he said. “I thought that I would be able to build my credit if I paid it back — I was so wrong.”

He is not the only one who is “so wrong”: just as wrong are all those Panglossian economists at the Fed and Wall Street who believe that the US economy is growing at what the Atlanta Fed today laughably “calculated” was a 4.2% GDP, even as the DOE found that the most accurate indicator of overall economic strength, diesel demand, was the lowest since covid, an glaring paradox… yet glaring to all except those who refuse to see just how rotten the core of the US economy has become, and will be “absolutely shocked” when the next credit crisis destroys tens of millions of Americans drowning in what is now best known as “phantom debt.”

One year after regional banks crashed and burned due to the combination of tumbling debt/treasury prices coupled with cratering commercial real estate loans, fears about the current state of Commercial Real Estate – where most offices still see tenants at best 3 to 4 days a week and are literally burning through rents – appear long forgotten. Is that sensible?

For one answer, we turned to the latest report from Goldman’s REIT/CRE expert Chandhi Luthra who has published a visual assessment of the state of CRE in 2024 in terms of loan maturities, 2023 extensions, and property and lender groups. She also looks at the latest transaction and leasing volumes, and shares several key takeaways.

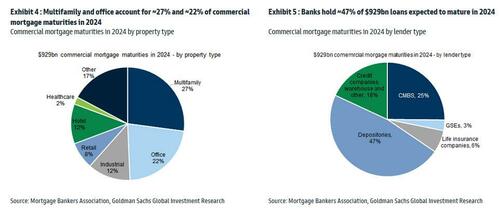

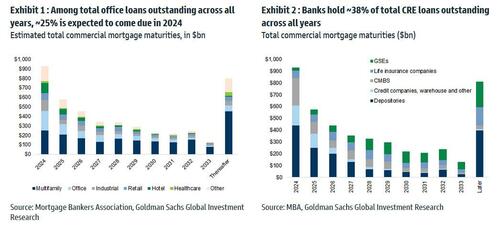

There are ~$4.7tn of outstanding commercial/multifamily mortgages outstanding, according to the Mortgage Bankers Association’s 2023 Commercial Real Estate Survey of Loan Maturity Volumes.

More specifically in 2024, $929bn of CRE mortgages are expected to mature, ~20% of ~$4.7tn total commercial mortgages outstanding. In terms of property type, multifamily and office account for ~27% and ~22% of commercial mortgage maturities in 2024 respectively. In terms of lender type, banks hold ~47% of debt maturing in 2024, followed by CMBS at ~25%.

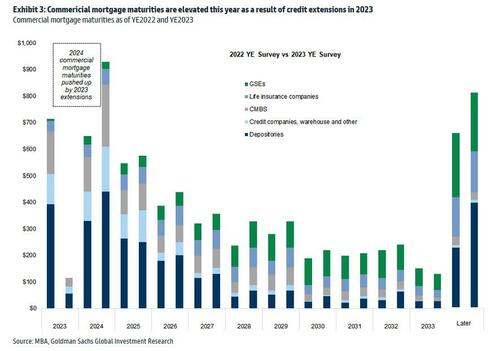

It is worth noting that 2024 commercial mortgage maturities are pushed up by 2023 extensions. As shown in Exhibit 3, among the CRE loans scheduled to mature in 2023, ~$610bn were refinanced, with ~$300bn pushed into 2024 and the remainder into future years. As a result, the total CRE refinancing volume is expected to be ~$929bn in 2024.

Of course, it does not end there, and since there has been no fundamental improvement, it is certain that extension volumes in 2024 will be high as well. However, as interest rates are expected to come down, demand for refinancing in 2024 may outpace that in 2023 according to the Goldman analyst (rates are still far, far higher than where they were when most of the loans were originated several years ago). At the same time, for loans that have already been extended in the past, it is also likely that future extensions could be harder.

Among the loans backed by office properties overall, ~25% is expected to come due in 2024. In terms of lender type, banks (primarily small, regional banks) hold ~38% of total CRE loan outstanding across all years, followed by the GSEs at 20%.

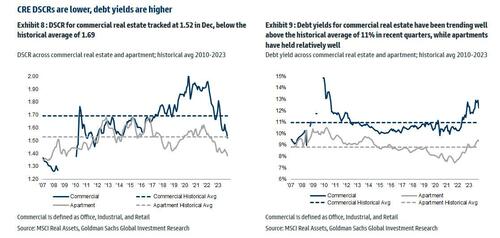

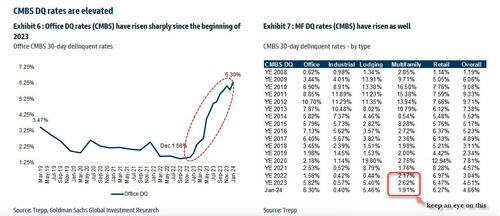

Looking at different debt metrics, DSCR for commercial real estate (office, industrial and retail combined) tracked at 1.52 in Dec, below the historical average of 1.69; debt yields for commercial real estate have been trending well above the historical average of ~11% in recent quarters, while apartments have held relatively well.

Office CMBS DQs have risen significantly, with Jan tracking at 6.3%, up significantly from 1.58% in Dec 2022. And while everyone knows the Office canary in the coalmine is dead and buried, keep an eye on Multifamily CMBS DQs which tracked at 1.91% vs 2.62% in December, with the sequential decline associated with a large San Francisco apartment loan that was recently disposed. The overall DQ rate tracked at 4.66% in January.

The Goldman strategist concludes with a word about CRE transaction and leasing: U.S. CRE transaction market continues to be muted, primarily driven by elevated interest rates, limited sources of capital, and the pricing gap between buyers and sellers. January volume was down -11% yoy, driven by easier compares in Jan 2023 (down -55%). In terms of leasing, Jan preliminary trends indicate weakness in activities, with office down -25% yoy and industrial down -28% yoy.

Here, Goldman trader Sara Cha chimes in (her report is also available to pro subs) and notes that we can see from the transaction data “why sentiment in CRE brokers is a bit more mixed of late – thought yesterday’s JLL print had mixed reception – while you’ve seen some signs of life in capital markets space broadly to start the year, not seeing that as much on the CRE front (remember those 3Q-4Q greenshoots?).“

Multifamily CRE

The commercial real estate sector continues to experience elevated stress . The latest crack to emerge is the increasing number of delinquencies on multifamily mortgages.

In April, about 8.6% of commercial real estate loans bundled into collateralized loan obligations were distressed, reaching the record high set in January, according to Bloomberg, citing new data from analytics firm CRED iQ.

The loans bundled into CRE CLOs were merged with funds from individual investors to acquire multifamily housing during the Covid era. After that, borrowing rates surged, catching many off guard. A significant portion of the deteriorating loans had floating-rate interest rates, putting massive pressure on landlords’ cash flows, diminishing the market worth of the properties, and obliterating equity in a large number of investments.

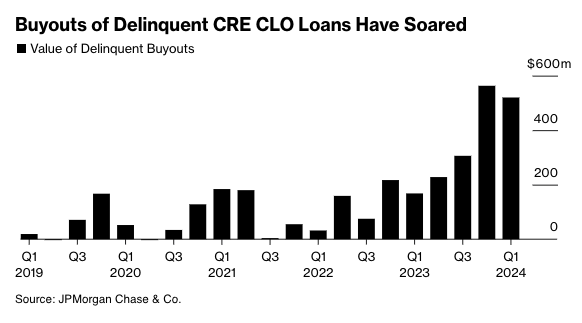

According to data provider Trepp, $78.5 billion of CRE CLO loans are outstanding. This means many CRE CLO issuers are racing to find ways to prevent a tsunami of bad loans from defaulting or risk losing the fees they collect on the securities.

Recent estimates from JPMorgan show lenders purchased $520 million of delinquent loans in the first quarter of this year. Lenders have been ramping up the number of buyouts over the last four quarters because of mounting bad loans in a period of elevated rates.

Source: Bloomberg

JPMorgan strategist Chong Sin said he’s surprised by lenders’ ability to obtain warehouse lines to purchase bad debt, given tightening credit conditions.

“The reason these managers are engaged in buyouts is to limit delinquencies,” Sin said, adding, “The wild card here is, how long will financing costs remain low enough for them to do that?”

Anuj Jain, an analyst at Barclays Plc, expects buyouts to continue as distress increases across the CRE CLO space.

“If the outlook for the Fed shifts materially to hikes or no rate cuts for a while, that might lead to a sharp increase in delinquencies, which can stifle issuers’ ability to buy out loans,” Jain said.

Bloomberg explains much of the CLO space derives from multifamily bridge loans originated around 2021-2022:

CRE CLO issuance surged to $45 billion in 2021, a 137% increase from two years earlier, when buyers of apartment blocks sought to profit from the wave of workers moving to the Sun Belt from big cities. Three-year loans would give them time to complete upgrades and refinance, the thinking went.

Fast forward to today and the debt underpinning many of the bonds is coming due for repayment at a time when there’s less appetite for real estate lending, insurance costs have skyrocketed and monetary policy remains tight. Hedges against borrowing cost increases are also expiring and cost significantly more to purchase now.

Those blows helped increase multifamily assets classed as distressed to almost $10 billion at the end of March, a 33% rise since the end of September, according to data compiled by MSCI Real Assets.

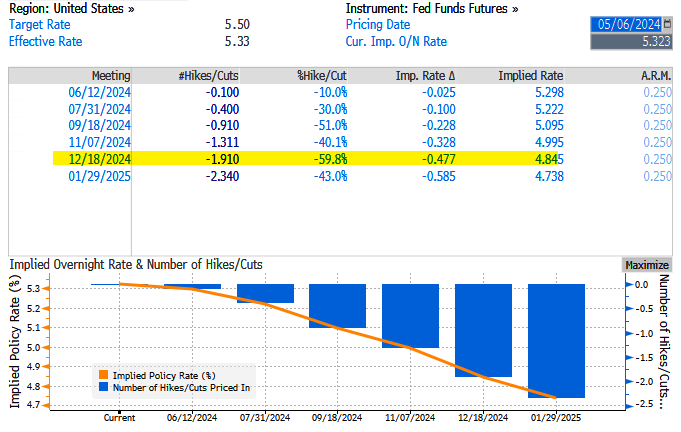

Last Wednesday, the Fed left interest rates unchanged at around 550bps as inflation data reaccelerates and economic growth tilts to the downside, stoking stagflation fears.

Fed swaps are pricing in just under two cuts – this is down from nearly seven earlier this year and about 1.14 before last week’s FOMC.

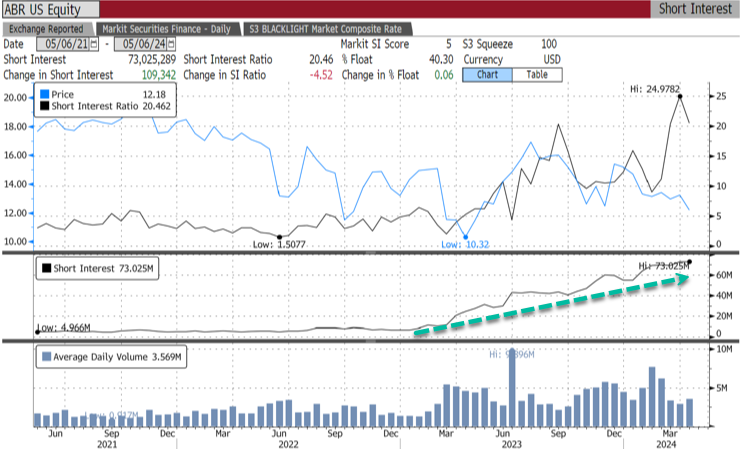

Meanwhile, bears are piling in on CRE CLO issuer Arbor Realty Trust Inc., with 40.3% of the float short, equivalent to 73 million shares short.

“The multifamily CRE CLO market was not prepared for rate volatility,” said Fraser Perring, the founder of Viceroy Research, which has placed bear bets against Arbor, adding, “The result is significant distress.”

The longer the Fed delays rate cuts, the worse the CRE mess will get.

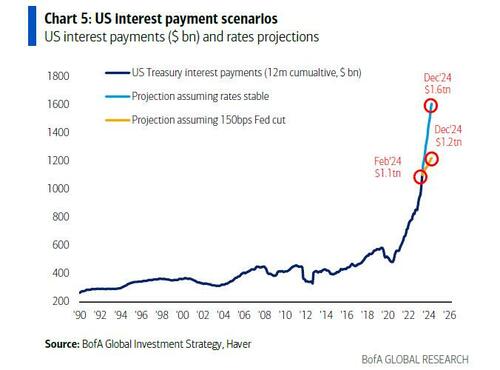

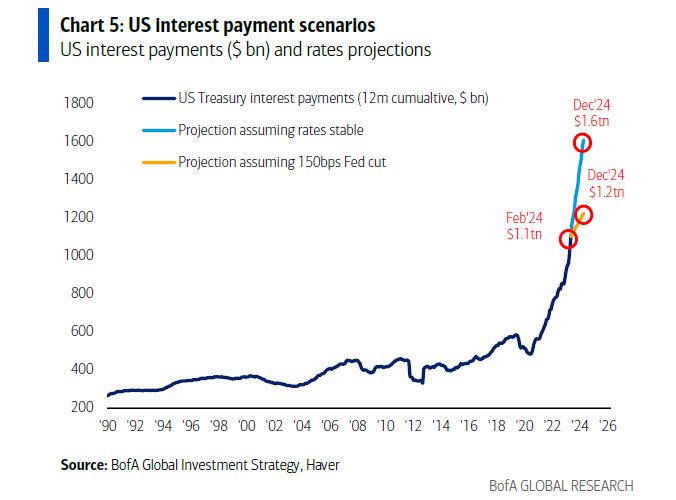

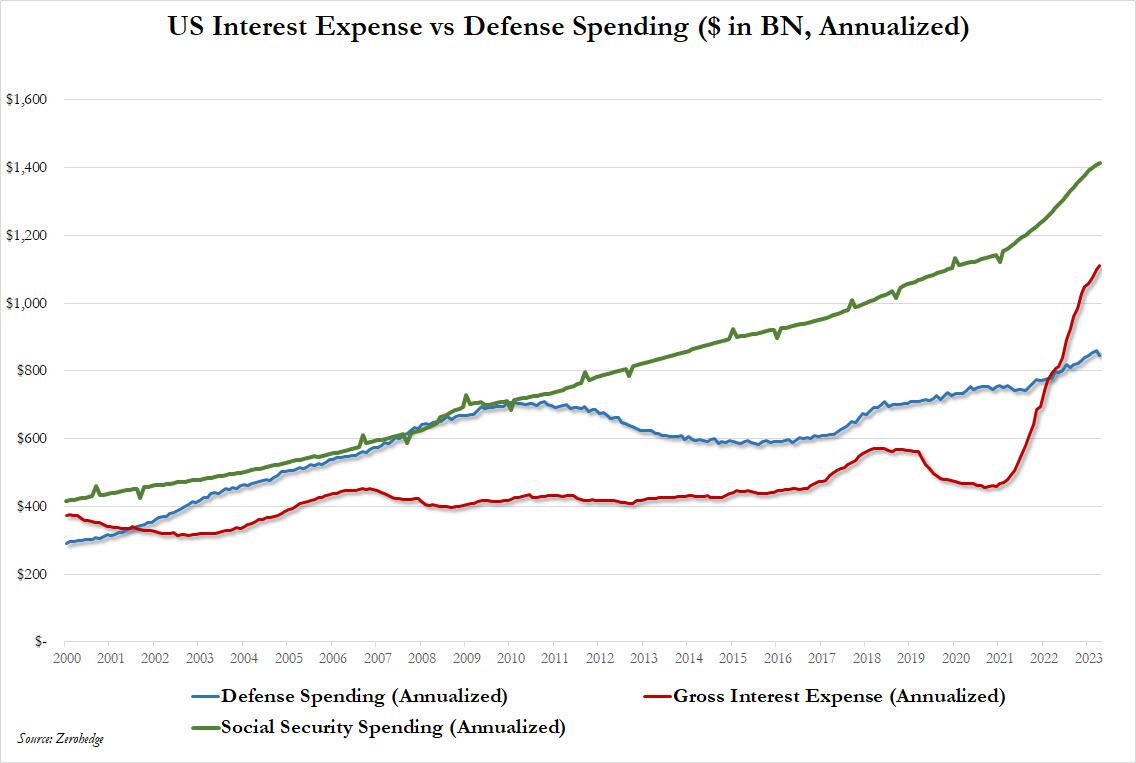

Under Biden’s “Reign of Error”, the interest on US debt just hit a record $1.1 trillion and the US deficit for just the first six months of fiscal 2024 is also $1.1 trillion.

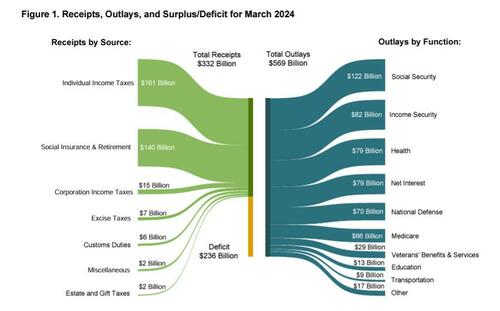

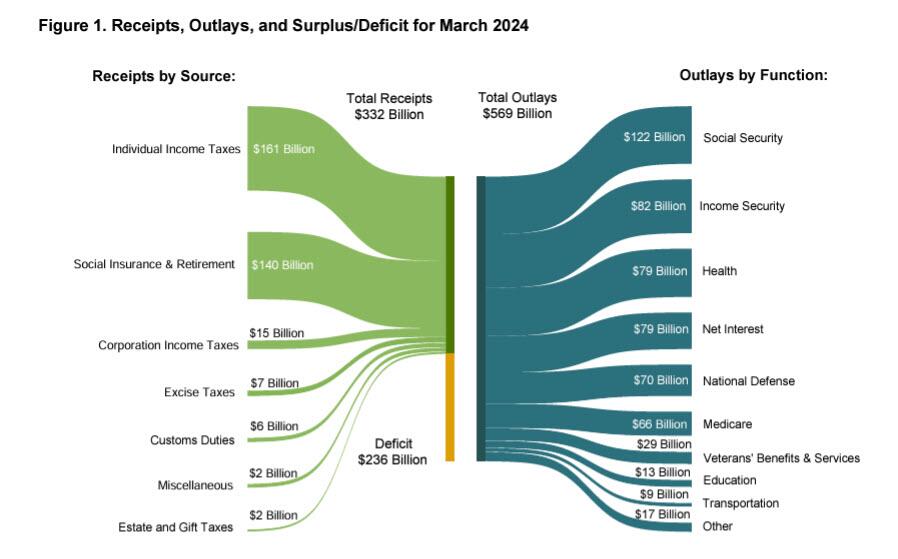

According to the latest Treasury Monthly Statement, in March the US deficit hit $236 billion, some $40 billion more than the $196 billion expected, if below February’s $296 billion…

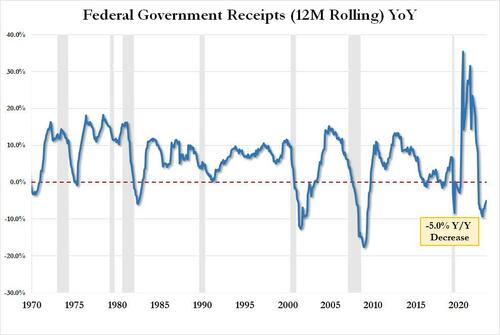

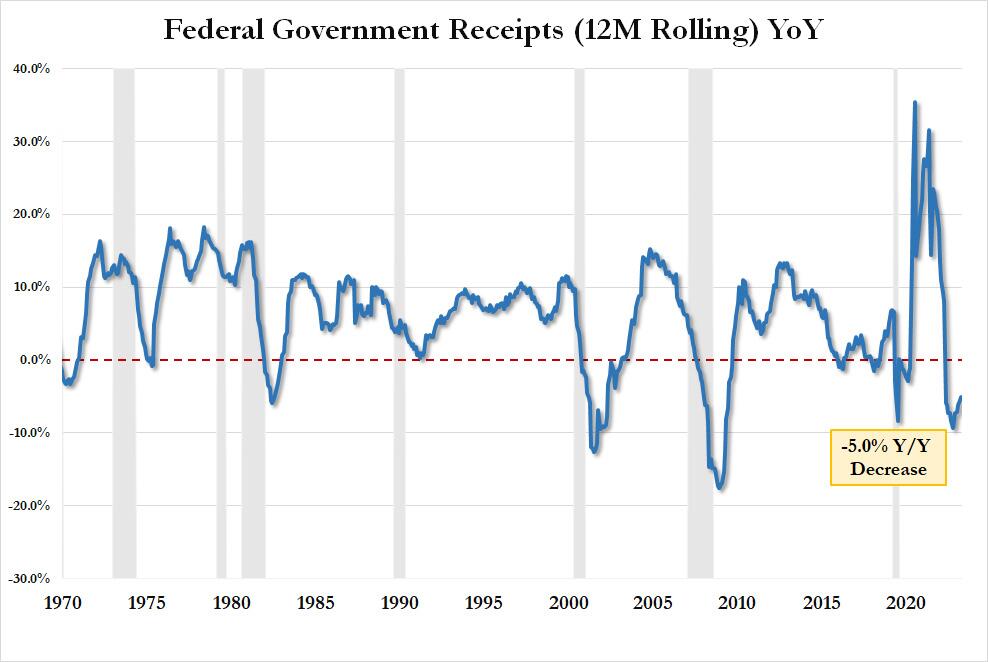

… which was the result of $332 billion in govt tax receipts – translating into $4.580 trillion in LTM tax receipts, and which was down 5% compared to a year ago…

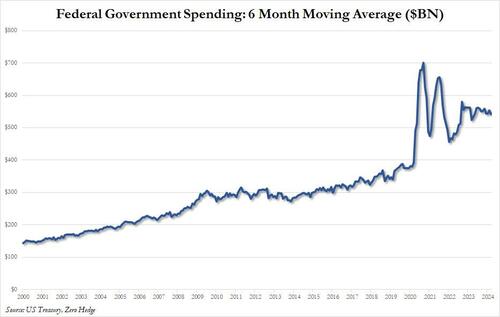

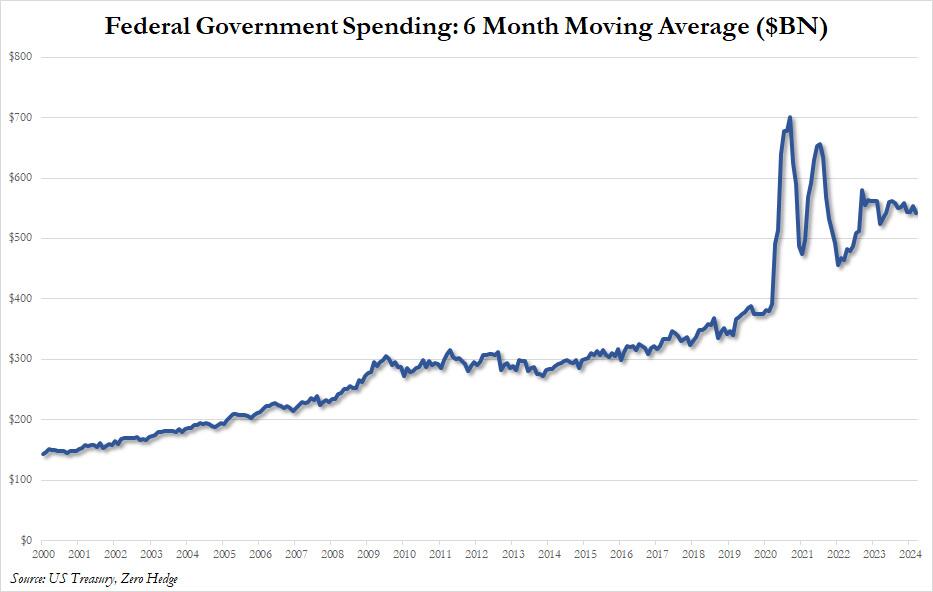

… offset by the now traditional ridiculous monthly outlays, which in March amounted to $568 billion, up from $567 billion in February and the highest monthly spending total in calendar 2024, which translated into a 6 month moving spending average (for smoothing purposes) of $542 billion. Take a wild guess what will happen to the chart below during and after the next recession.

This, incidentally, is a reminder that the US does not have a tax collection problem – it has a spending problem, and no amount of tax changes will fix it; in fact all higher taxes will do is force more billionaires to move to Dubai where they pay zero taxes.

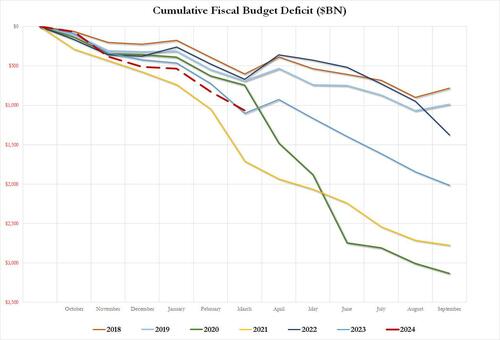

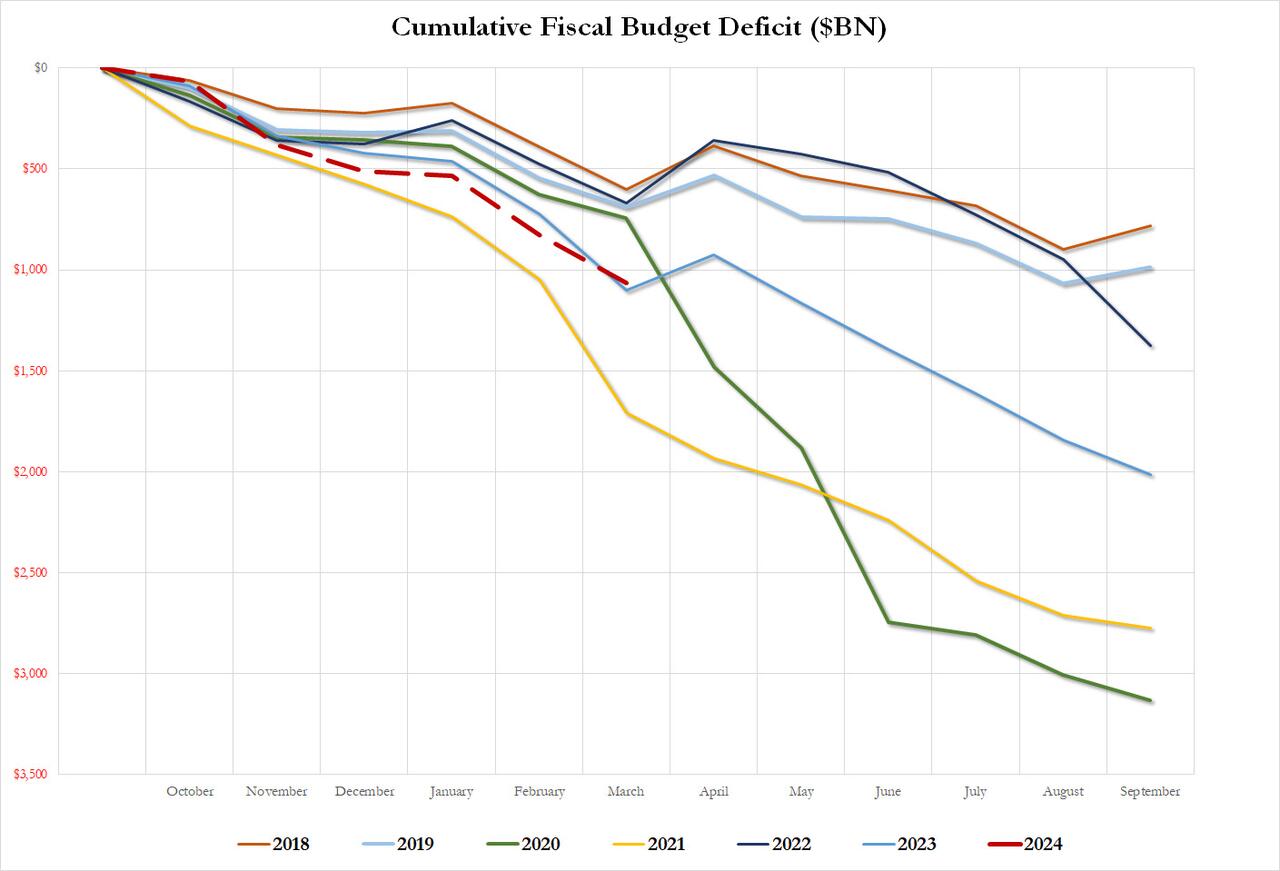

Putting the YTD deficit in context, in the first six months of fiscal 2024, the US deficit hit $1.065 trillion, just shy of the $1.1 trillion reached last year, which was the 2nd highest on record and only the post-covid 2021 was worse. Annualized, we expect total deficit to hit $2.2 trillion in fiscal 2024, a year when the US is supposedly “growing” at a nice, brisk ~2.5% pace. One can only imagine what the GDP growth would be if the US wasn’t set to have a wartime/crisis deficit…

… and we can’t even imagine what US deficit will be after the next recession/depression.

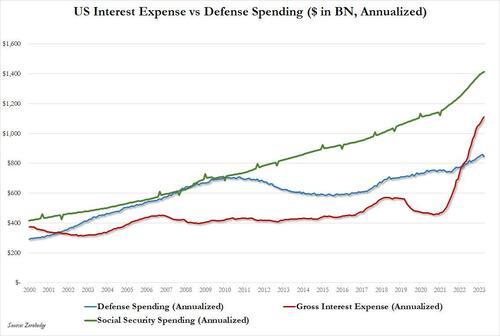

Meanwhile, as reported previously, total US interest continues to explode, and after surpassing total annual defense spending about a year ago, just the interest on US debt will soon become the single largest government outlay as it surpasses social security by the end of 2024, when according to BofA’s Michael Hartnett it hits $1.6 trillion…

.. and surpasses Social Security spending as the single largest spending category in the US government.

Biden has wanted to get rid of Social Security for a long-time and now wants to get rid of Medicare Advantage programs and put everyone on Medicare. Looks like Cloward-Piven!

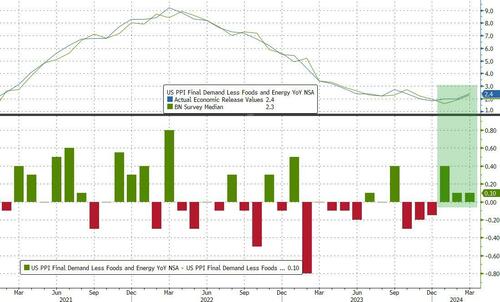

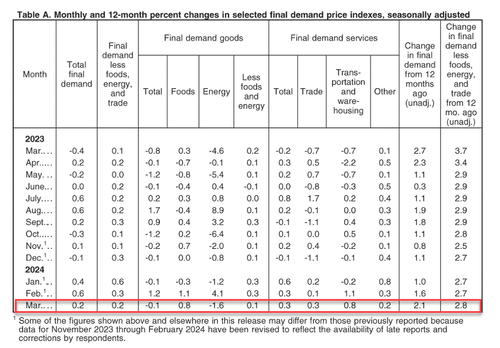

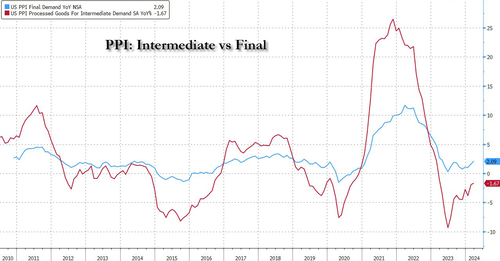

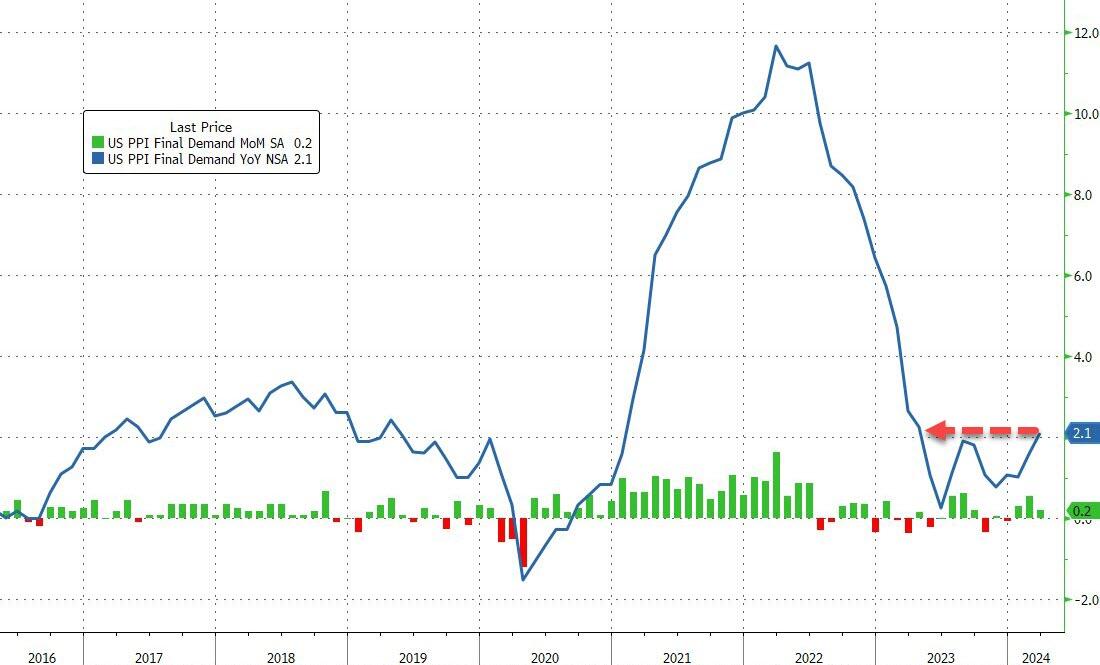

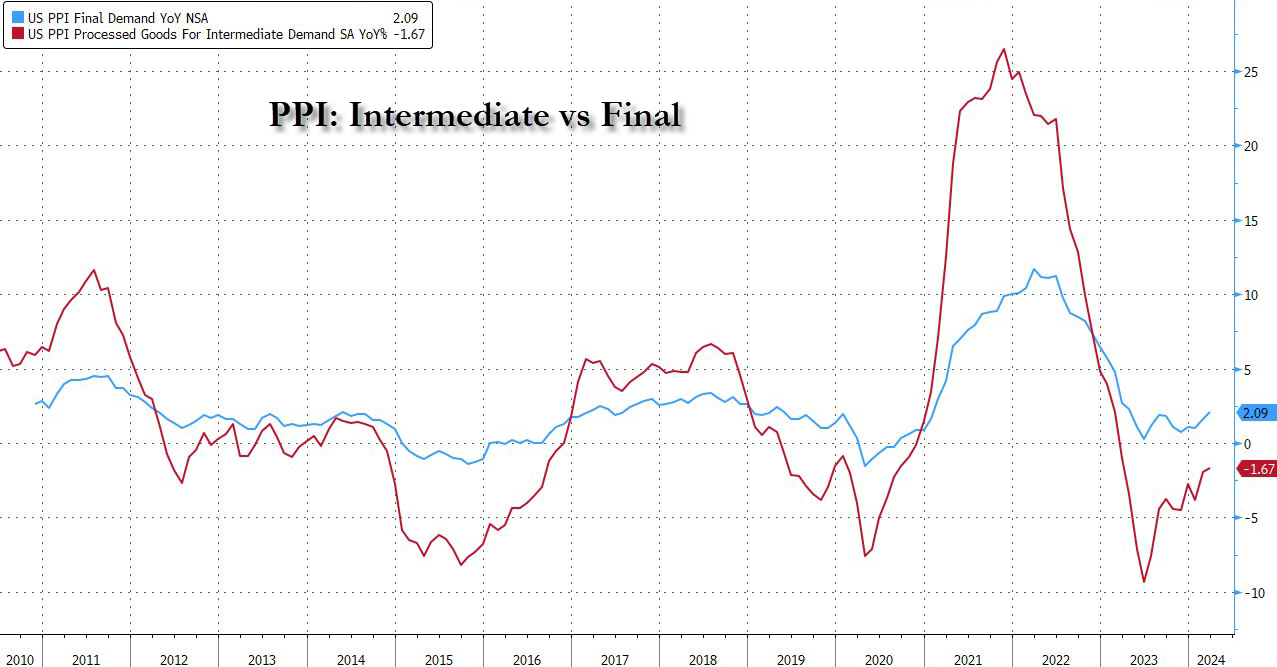

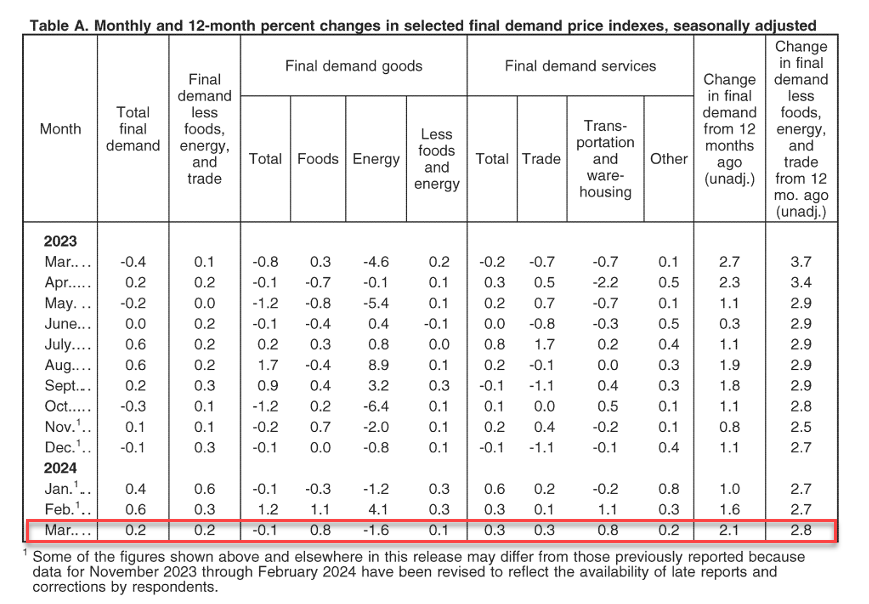

On top of skyroceting budget deficits, we have Producer Prices rising at fastest pace in a year in March.

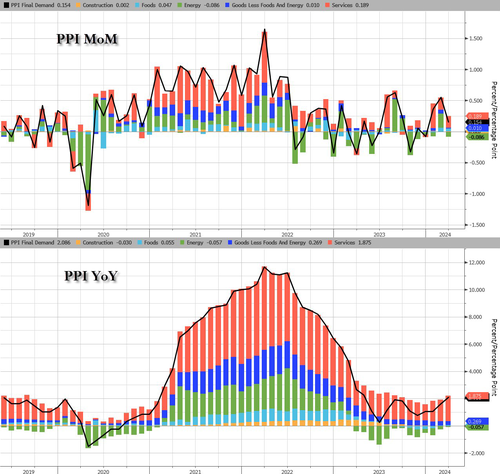

After yesterday’s CPI-surge, PPI followed along, with headline producer prices rising 0.2% MoM (+0.3% MoM exp), pushing the YoY PPI to +2.1% (+2.2% exp) from +1.6% – the highest since April 2023…

Source: Bloomberg

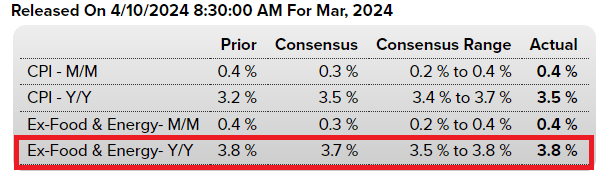

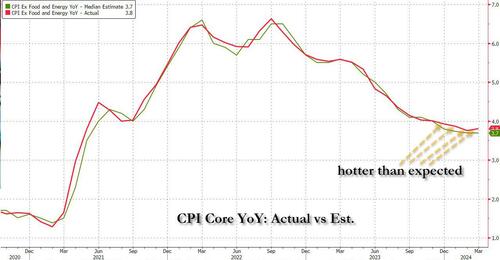

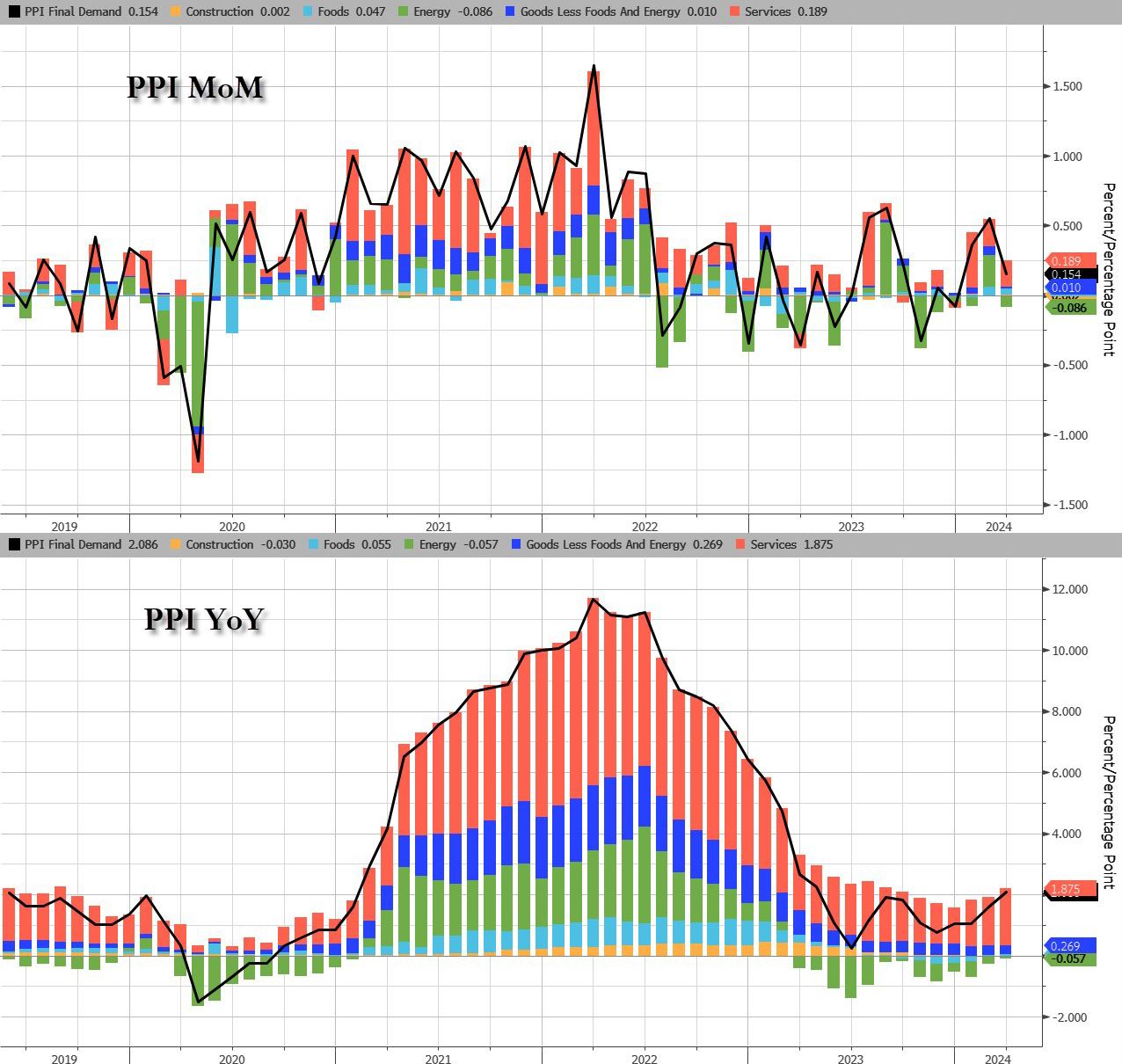

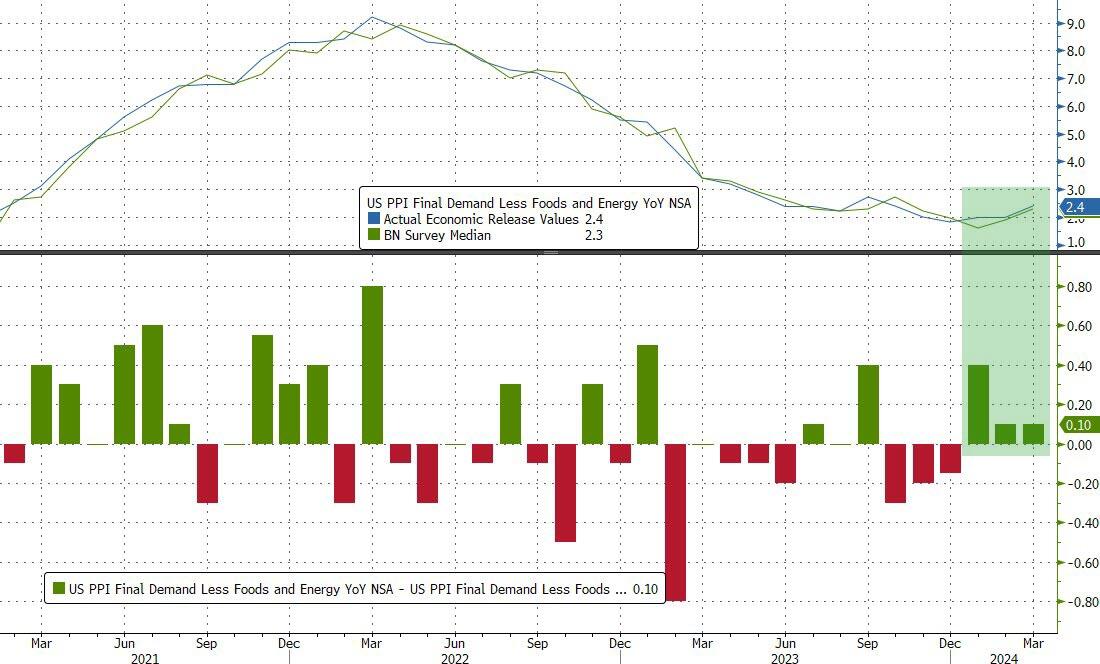

Core CPI rose 2.4% YoY (hotter than the expected 2.3%) – the third hotter-than-expected core PPI print in a row…

Under the hood, Services prices rose while goods prices declined MoM.

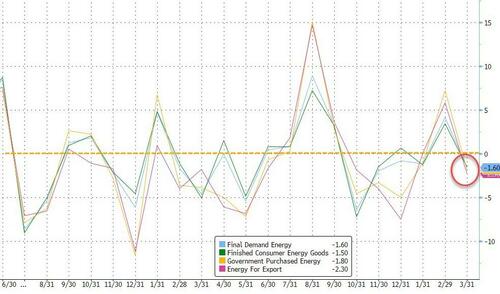

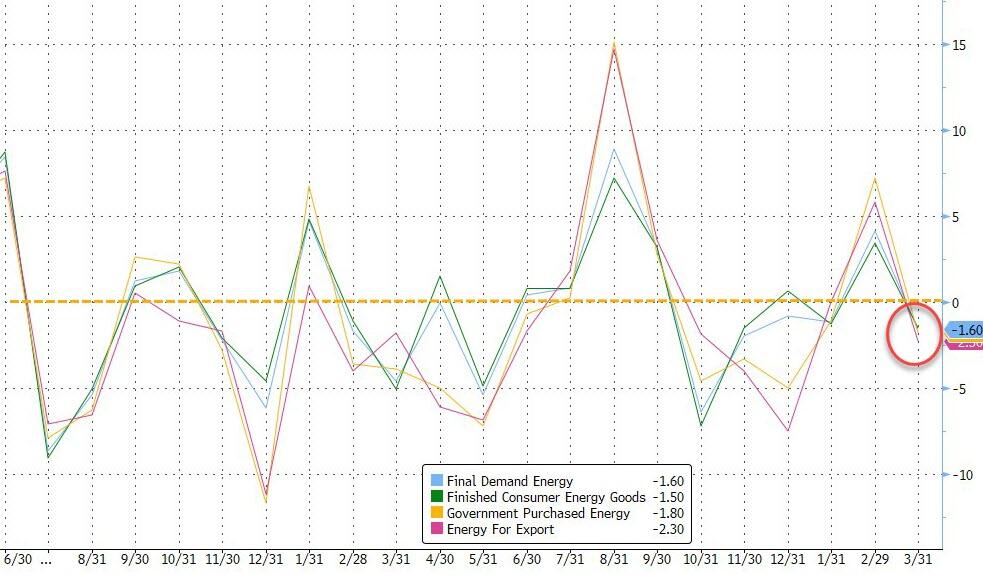

One thing that stands out as rather odd is the 1.6% MoM decline in Energy costs in the month… as prices soared for crude and gasoline?

Leading the March decline in the index for final demand goods, prices for gasoline decreased 3.6 percent…

And blame the markets for why the print was hot:

A major factor in the March increase in prices for final demand services was the index for securities brokerage, dealing, investment advice, and related services, which rose 3.1 percent.

And on a YoY basis, Services costs are accelerating…

Pressure continues to build in the inflation pipeline too…

While some may cling with grim hope to the ‘cooler than expected’ headline PPI print, core PPI is hot, damn hot, and headline PPI is rising. Not at all what The Fed, or Biden, wants to see – no matter how hard they spin it.

This is Victor Davis Hansen from Stanford’s Hoover Institute.

Funky cold Joe Biden is his reaction to inflation caused by his outragous spending. His legion of sycophants are now saying inflation is a good thing or don’t notice it. But Biden will never stop spending .

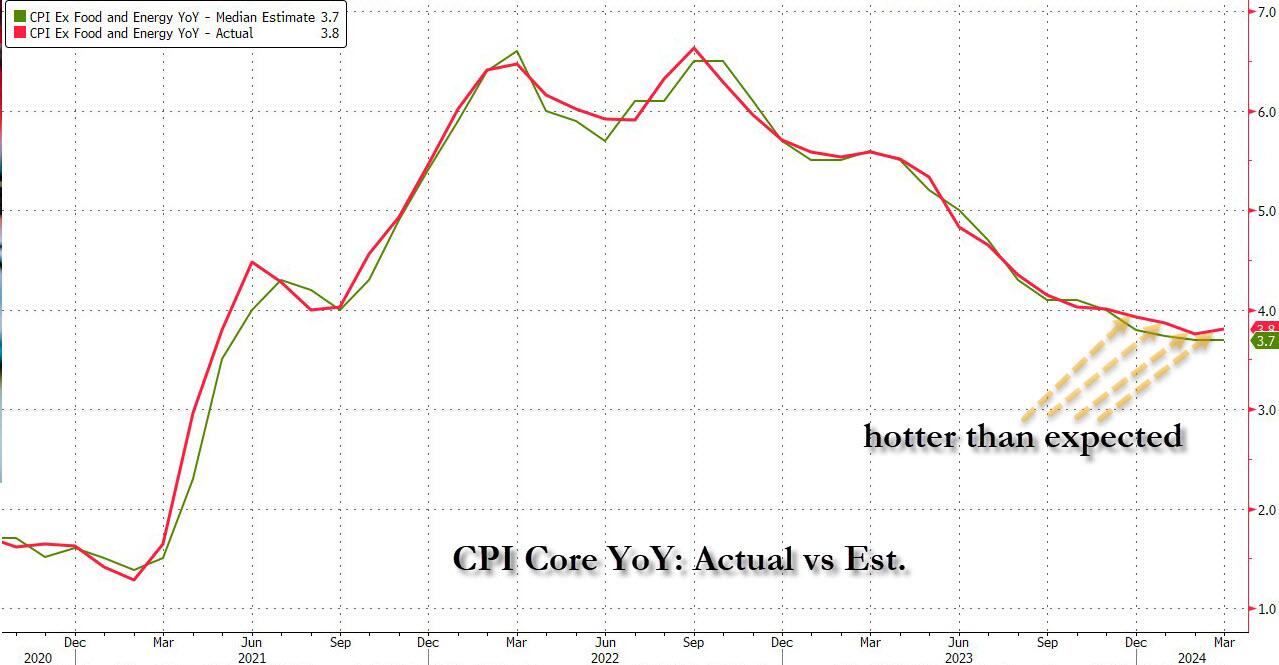

Coming into today’s CPI number, which followed three previous red-hot inflation prints, we said that it’s time for a “miss” (the first of 2024) not because the data demands it – on the contrary, prices continue to rise at a frightening pace – but because a dovish CPI print today would be the last opportunity for the Fed to set a timetable for a rate cut calendar ahead of November’s election.

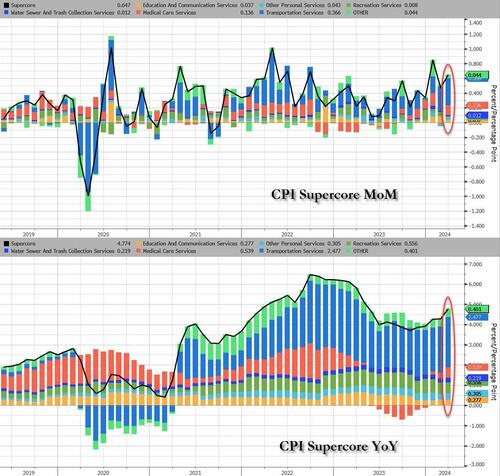

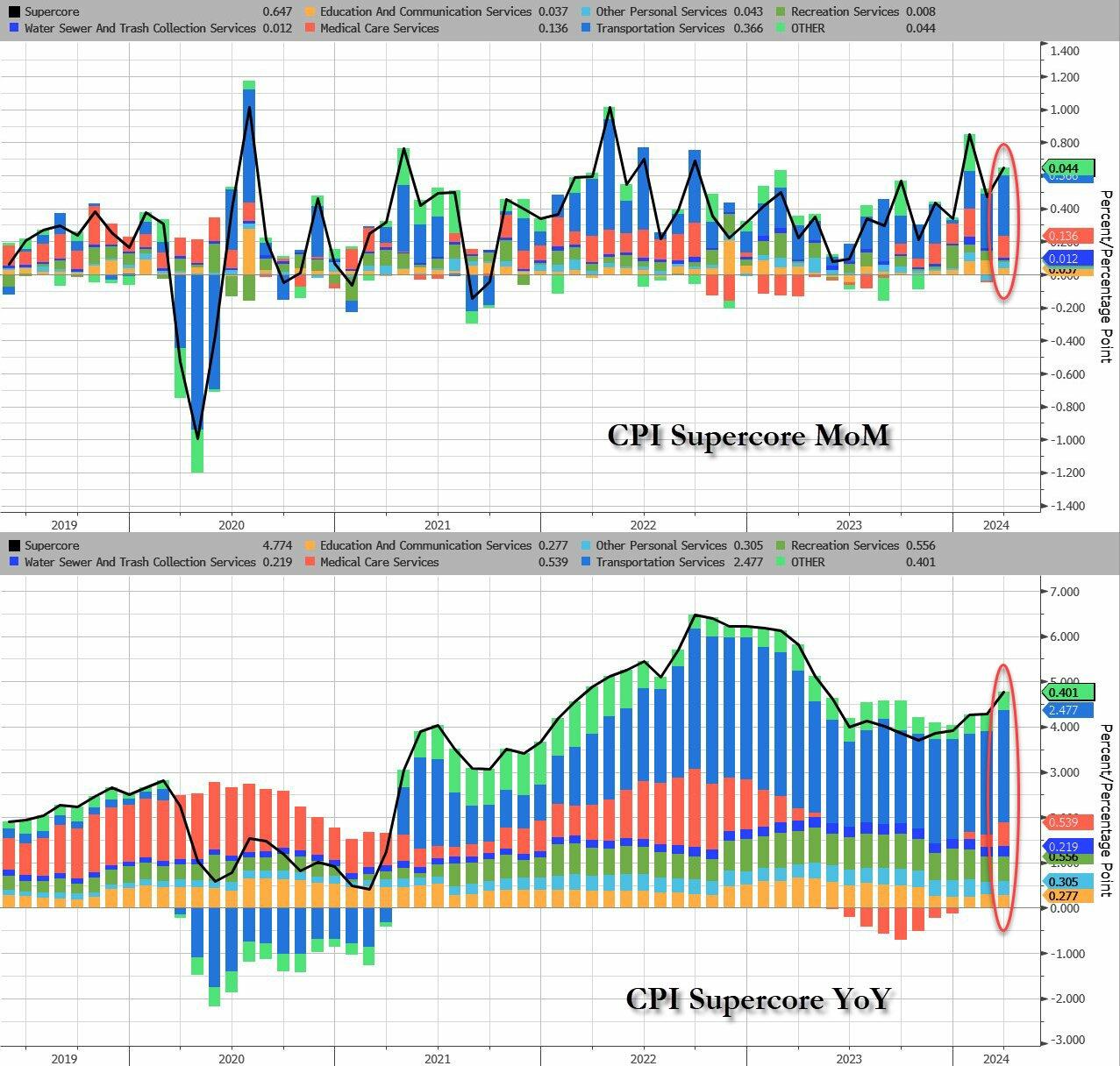

Well, you can wave goodbye to all that, because we just got the 4th consecutive “inflation beat” in a row…

… with supercore inflation coming in blazing hot…

… thanks to a boiling inflation print which saw every single CPI metric coming in hotter than expected – was a shock, not because it reflected reality, but because it effectively sealed Biden’s fate because as Bloomberg’s Chris Antsey writes, “obviously, this is very bad news for Joe Biden… we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.”Easy financial conditions continue to provide a significant tailwind to growth and inflation. As a result, the Fed is not done fighting inflation and rates will stay higher for longer.”

It’s about to get even worse: recall today we have a $39 billion 10-year auction which is already being dubbed “sloppy” and a definitive break of 4.5% could easily extend if underwriting dealers are left holding the bag. As it stands, the 10yr has popped above the 4.5% parapet. Ian Lyngen at BMO Capital Markets says:“We expect the setup to the auction will break 4.50% in 10-year yields with ease.”

Obviously, this is very bad news for Joe Biden. It’s still only April, and we’ll have another half-a-year’s worth of inflation reports before the election. But we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.

Joe Biden continues to act like a gangsta giving away student loan forgiveness despite being told no by the US Supreme Court. As I said, Funky Cold Joe Biden. But Biden’s gangstaism favors the top 0.5% of net worth people, not the masses.

As Biden gropes for more voters, claiming he was raised in Puerto Rican, Greek, Black, and every other race on the planet, he probably sings “Ride The White Horse” to The Presidency. Reminiscint of Hillary Clinton claiming she kept a packet of hot sauce in her purse when talking to a black commentator.

We are living in the USA where corruption, favoritism, open borders and an out-of-control Federal budget and debt are destroying this once great nation.

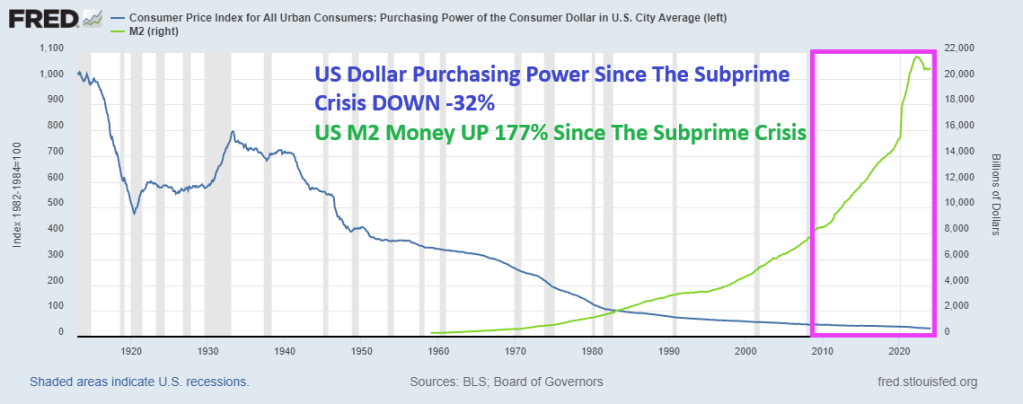

Former Kansas City Fed President Thomas M. Hoenig was absolutely right when he said recently that The Federal Reserve panders to Wall Street, Congress and special interest groups, prioritizing immediate relief over financial stability. Bernanke’s zero-interest rate policies (ZIRP) and Quantitative Easing (QE) were short-term fixes that never went away. Indeed, since the subprime mortgage crisis of 2008-2009, US Dollar purchasing power is DOWN -32% and M2 Money is up a staggering 177%. While Yellen stuck with zero-interest policies until Trump was elected, then raised The Fed Funds Target Rate 8 times. Yellen only raised the target rate once under Obama. Clearly playing political favoritism.

The Federal Reserve’s lack of transparency comes amidst reports that countries are removing their gold and other assets from the U.S. in the wake of the unprecedented Western sanctions imposed on Russia over its invasion of Ukraine. According to a 2023 Invesco survey, a “substantial percentage” of central banks expressed concern about how the U.S. and its allies froze nearly half of Russia’s $650 billion gold and forex reserves.Headline USA filed a FOIA request with the Fed for records reflecting how much gold the Federal Reserve Bank of New York currently holds in its vault, as well as records reflecting the ownership stake that each of FRBNY’s central bank/government clients have in that gold. The FOIA request also sought records about the Fed’s gold holdings prior to Russia’s February 2022 invasion of Ukraine. However, the Federal Reserve denied the FOIA request on Wednesday.

It influences the price of nearly everything, as well as the availability of jobs, the stability of our banking system, and the purchasing power of our money.

When the Fed Chair speaks, the entire world stops to listen.

But the average person has a poor understanding of how this colossally important entity operates. Or even why it exists.

And after a series of asset price bubbles — which some argue we’re in another one now — a chorus skeptical of the Fed’s actions has emerged.

So today we’re doing our best to shine as bright a light as possible on the Fed: how & why it operates, the good & as well as the shortcomings of its actions to date, what direction its policies are likely to take from here, and how all of this impacts the households of regular people like you and me.

Here are my top takeaways from from a speech by former KC Fed President Thomas Hoenig:

Dr Hoenig admits the Federal Reserve has experienced substantial “mission creep” since its creation as a lender of last resort. Its track record is very much “mixed” in terms of delivering on the intent of its policies. In Dr. Hoenig’s opinion, its efforts to add stability sometimes instead only create more instability.

While very critical of the Fed’s QE and ZIRP policies in the wake of the GFC, and more recently in the $trillions in monetary & fiscal stimulus unleashed post-COVID, Dr Hoenig thinks current Fed policy is “about right”. Though he expects the Fed to come under serious pressure soon as ebbing liquidity allows recessionary forces to build. He thinks the Fed will need to make an important decision within the coming year: return to QE and re-flame inflation, or allow a recession to occur.

Dr Hoenig criticizes the Federal Reserve for pandering to various interests, noting that short-term thinking and pressures from Wall Street, Congress, and interest groups often lead to decisions that prioritize immediate relief over long-term stability — a sort of “We’ll act now for optics sake and hopefully figure things out later”

In Dr Hoenig’s opinion, our fiscal policy is a runaway disaster. He criticizes both political parties of Congress for their roles in the cycle of ever-increasing deficits. Democrats advocate increased spending and tax hikes, while Republicans aim to keep taxes low but fail to curb spending. He warns of dire long-term consequences for future generations due to this impasse.

Dr Hoenig is very worried about the current stability of the banking system (and this from a former Direct of the FDIC!). He advocates for essential reforms to address government spending, prioritize essential areas without relying on future borrowed funds or inflationary measures, and communicate transparently with the public. He stresses the importance of reducing debt growth substantially below national income growth to avoid a full-blown crisis scenario in the future.

Dr Hoenig predicts the purchasing power of the US dollar (and other world fiat currencies) will continue to decline due to current policies and the lack of a “discipline” to money creation. Until such a discipline is restored (perhaps a return to some sort of hard backing of the currency), the dollar’s fall in purchasing power won’t abate.

Dr Hoenig suggests investing time in reading history and biographies as a valuable way to learn about leadership and gain insights into what strategies works and which don’t.

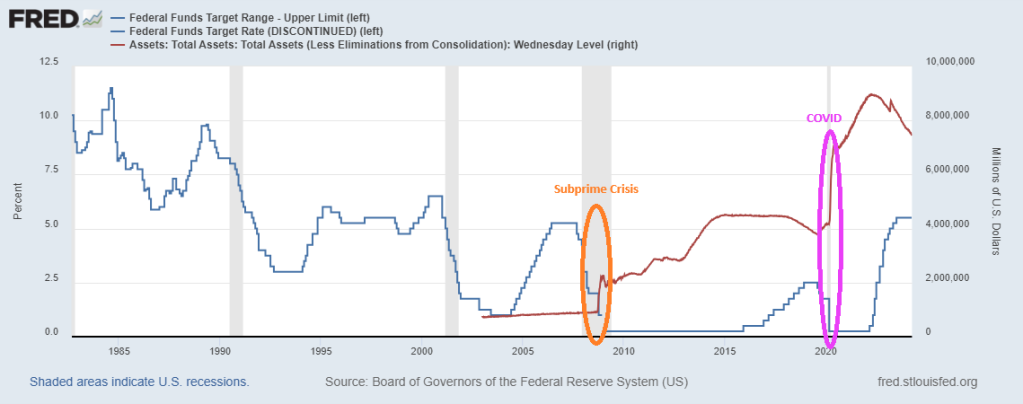

Here is the “Sound Money Parade” in 1896. By the aftermath of the subprime crisis, Janet Yellen (1993-2020) adopted the UNSOUND Money Fest, an orgy of printing and charging near zero interest rates. Powell in 2021 is ever-so-slowly unwinding The Fed’s balance sheet, but Powell has raised The Target Rate to its highest level since 1998 to fight inflation caused by Biden’s policies.

Combine The Fed not telling us how much gold they hold and their overprinting problems since 2008, and you can see why investors are turning to gold and silver and crypto currencies. The adoption of Central Bank Digital Currency (CBDC) is a step towards financial collapse.

Here is a parade you will NEVER see in Washington DC. A Sound Money Parade!

Powell is beginning to act like a sound money fan, but he still is taking his sweet time shriking the balance sheet.

I am thinking of fleeing to Lilliehammer Normay like Frank Tagliano.

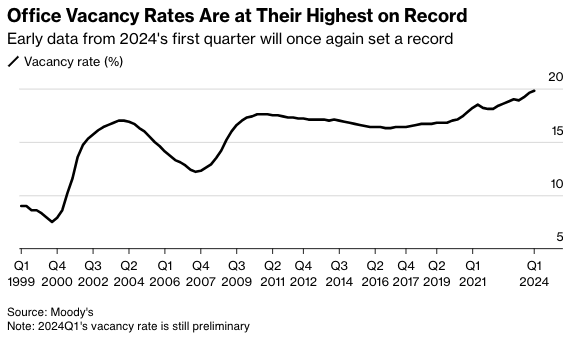

The rising supply of office space is due to a combination of surging remote and hybrid work that forces companies to reduce corporate footprints. Also, companies are exiting imploding progressive cities and high-taxed blue states for red ones while downsizing space. In the report, office tower vacancies rose to a record 19.8%, up from 19.6% in the fourth quarter of 2023.

Even with the increase, there is an eerily calm across the commercial real estate sector. This comes as the Federal Reserve’s interest rate hiking cycle is higher for longer, indicating that the pain train is nearing (perhaps after the presidential election).

“The office stress isn’t quite done yet,” Thomas LaSalvia, Moody’s head of commercial real estate economics and one of the authors of the report, told Bloomberg in an interview. He noted recent positive economic indicators stave off a “perfect storm in the office sector.”

“There are spots of light and there are spots of extreme darkness,” LaSalvia said, adding, “This is part of a longer-term evolution where we are seeing obsolete buildings in obsolete neighborhoods.”

The high office vacancy rate continues to be terrible news for landlords and developers eager to fill their buildings, and the Fed’s hiking cycle has made refinancing very challenging.

Viswanathan said there have been no major fireworks in CRE tower debt because the debt is being “extended and modified rather than refinanced,” which “mitigates a default wave and a sharp pick-up in losses on CRE loan portfolios.”

Yes, both residential and commercial real estate are thunderstruck under Bidenomics.

… in the process, sparking the biggest market meltup in a decade, we explained that there was no mystery behind the Fed’s sudden change of heart: it had everything to do with Biden’s woeful performance in the polls.

… maybe what that happened in the past two weeks had nothing to do with economic data, the state of the US consumer, or how hot inflation is running and everything to do with… phone calls from the increasingly angry White House, the same White House which after seeing the latest polling data putting Biden at the biggest disadvantage behind Trump despite the miracle of “Bidenomics” decided to pull its last political level, and had a back room conversation with the Fed Chair, making it very clear that it is in everyone’s best interest if the Fed ends its tightening campaign and informs the market that rate cuts are coming. It certainly would explain why despite keeping the 2026 projected fed funds rate unchanged at 2.875%, the Fed just as unexpectedly decided to pull one full rate cut out of the non-election year 2025 and push it into the pre-election 2024.

I don’t know why @federalreserve is in such a hurry to be talking about moving towards the accelerator. We’ve got unemployment, if anything, below what they think is full capacity. We’ve got inflation, even in their forecast, for the next two years above target. We’ve got GDP growth rising if anything faster than potential. We have financial conditions, the holistic measure of monetary policy, at a very loose level.

… to which we again replied that there is a very simple reason why the Fed is “moving toward the accelerator” and it again had to do with the fact that Biden approval rating is now imploding, so much so that even Time magazine has stepped in with an intervention.

But while once upon a time such a cynical, hyperbolic, and apocryphal view would have been relegated to the deep, dark corners of the financial blogosphere (duly shadowbanned and deboosted by the likes of such Democratic party stalwarts as Google, of course), that is no longer the case and in his latest note, SocGen’s in-house permaskeptic, Albert Edwards confirmed our view that the biggest driver behind the Fed’s decision making in recent months is neither the economy, nor the market, but rather the November presidential election, to wit:

The widening inequality chasm in this US election year will be a real issue for policy makers. What will the Fed do? Traditionally, the Fed would not pivot rates policy to cushion inequality, which is usually addressed by fiscal policy. But growing inequality has been a key issue ever since the 2008 Global Financial Crisis triggered a backlash against ‘The Establishment’ – most evident in the rise in popularism (although many, including myself, believe that the loose money/tight fiscal policy mix was primarily responsible).

Might the unfolding inequality crisis force the Fed to bow to intense political pressure to cut rates faster and deeper? I think that is entirely plausible. Indeed we on these pages have previously observed, somewhat cynically, that Powell’s recent ‘surprise’ December 2023 dovish pivot came exactly at a time when Donald Trump was pulling ahead in the polls – link. But it would be a diehard cynic who could contemplate that the Fed, as part of ‘The Establishment’, would balk at the thought of Trump winning in November and juice up the economy to try and lower the odds of such an outcome. (I am that cynic.)

To be fair, we find it remarkable that Edwards – a long-tenured and respected veteran of the SocGen macro commentariat – would confirm our own observations. We doubt he is the only one, of course, but the others are far more afraid of losing their jobs, at least for now.

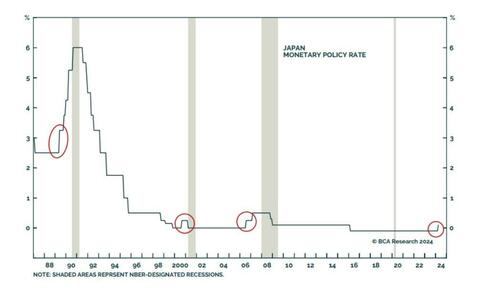

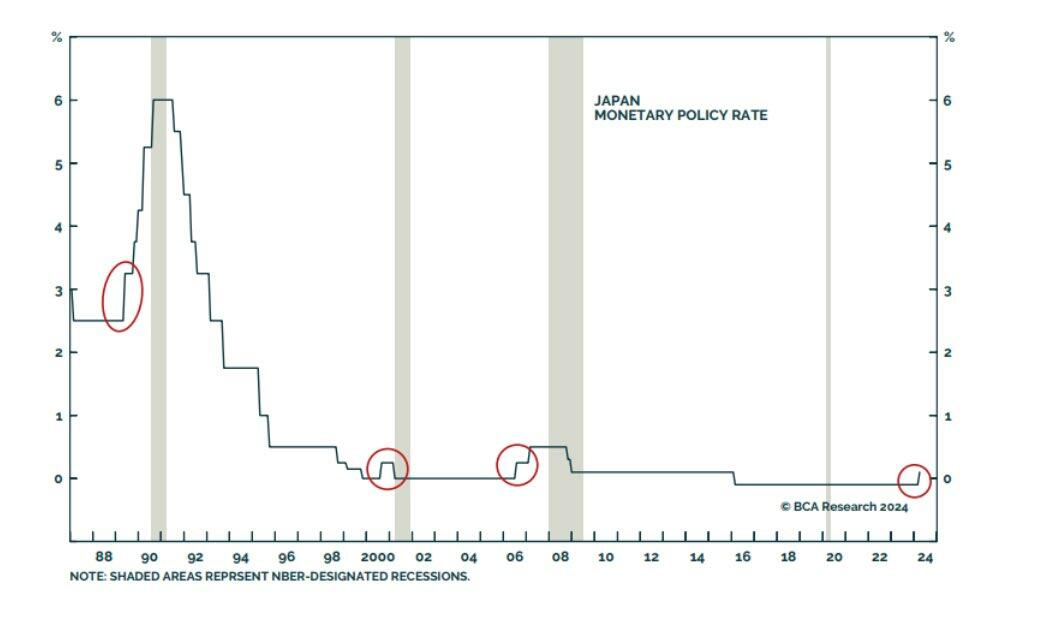

What we find less remarkable is that Edwards – whose job is to track down gruesome and painful ways for the market to die a miserable death – has done just that again and this time, in the aftermath of the BOJ’s long overdue exit from NIRP, ETF buying and Yield Curve Control, predicts that it is now only a matter of time before the YCC that was spawned in Japan will soon shift to the west.

Edwards starts off by observing what has long been a “foolproof” signal of imminent recession: BOJ tightenging:

Market sentiment is now especially vulnerable to weak economic data because, as we pointed out last week, it seems everyone (and their dog) has left their recessionary worries far behind. But as my favorite bear, David Rosenberg, pointed out this week, recent weak retail sales, housing starts, and industrial production data might be setting us up for a negative US Q1 GDP print. Let’s see how the Fed reacts to that. And if you want one reliable predictor of a global recession, @PeterBerezinBCA notes that “In the history of modern finance, no single indicator has done a better job of predicting when the next global recession will start than when the Bank of Japan starts raising rates. Foolproof!”

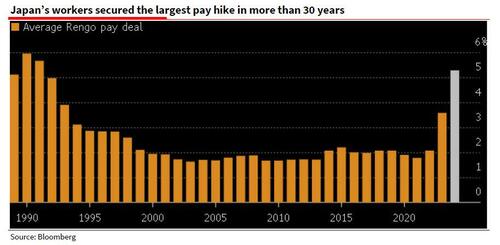

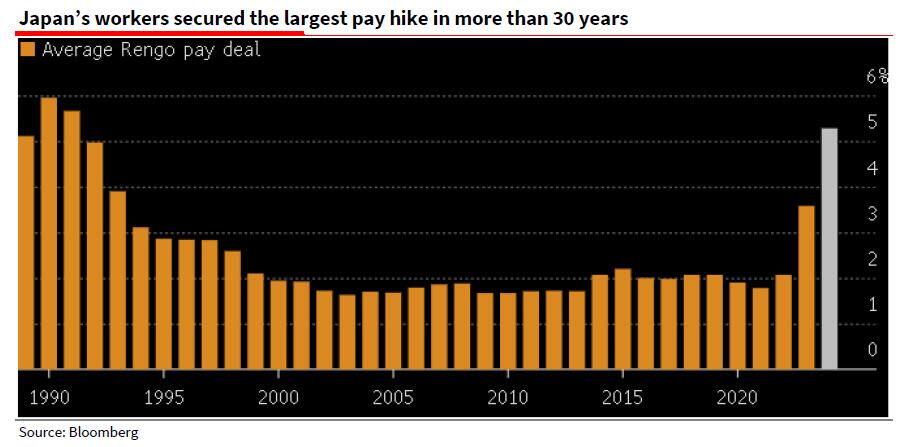

He then recaps last week’s main event, namely that after almost a decade, Japan finally exited negative interest rates and Yield Curve Control (YYC), primarily on the back of soaring (nominal, not real) wage gains: “Rengo, Japan’s largest trade union confederation, announced last Friday that its members have so far secured pay deals averaging 5.28%, far outpacing the 3.8% squeezed out a year ago — itself the highest gain in 30 years (see Bloomberg here and SG Economist Jin Kenzaki’s analysis of this data and the BoJ’s move here).“

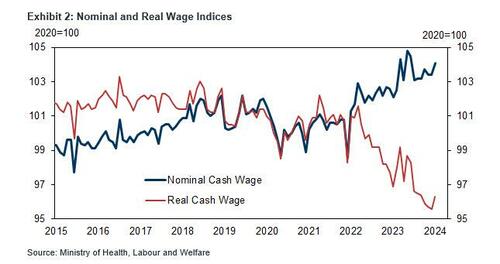

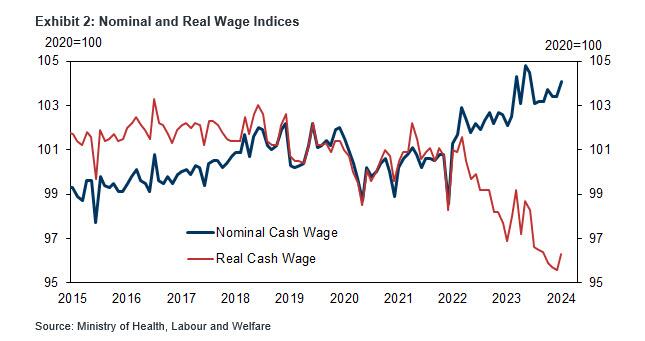

Of course, the problem in Japan is not that nominal wages are surging: it is that in real terms they are crashing, as the next chart clearly shows, and is why the BOJ will have to dramatically tighten – certainly much, much more than the laughable “dovish hike” it delivered last week which sent the yen plunging to a multi-decade low and inviting even more imported inflation – to avoid total collapse in Japan’s economy as it gradually accelerates toward hyperinflation:

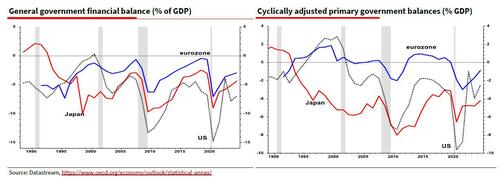

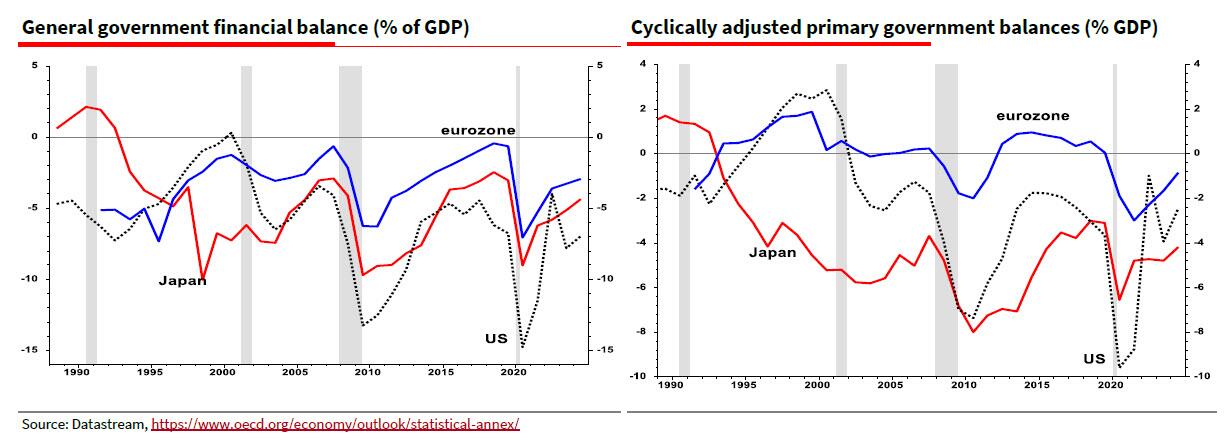

Of course, Japan can not actually tighten as that would instantly vaporize the economy and the bond market of a country whose central bank owns Japanese JGBs accounting for well more than 100% of GDP. But at least Japan has something goign for it: as Edwards notes, “the OCED estimates that interest on US debt amounts to 4½% of GDP, compared to only 0.1% of GDP for Japan (link). Hence the cyclically adjusted primary (ex-interest) deficit data show Japan as the most profligate borrower (see right hand chart). But the US still has to pay that interest somehow.” In other words, when adding interest payment, “it is the US that has been running the largest deficits since the 2008 GFC – bigger than even Japan (see left hand chart).”

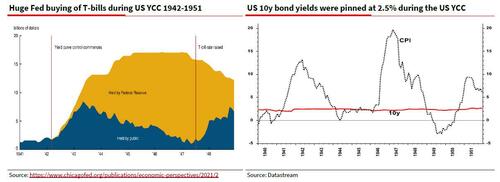

Which brings us to Edwards’ punchline: “decades of excessively loose monetary policy has allowed governments to ruin their fiscal situations to the point that public debt to GDP ratios are on wholly unsustainable trajectories. Just look at the CBO’s projections for the US here. Yet with an ever-intensifying populist backlash against high levels of inequality, I can only see one way out of this mess for western economies. Nothing less than Financial Repression including Yield Curve Control – yes, the very same YCC that Japan has just abandoned.”

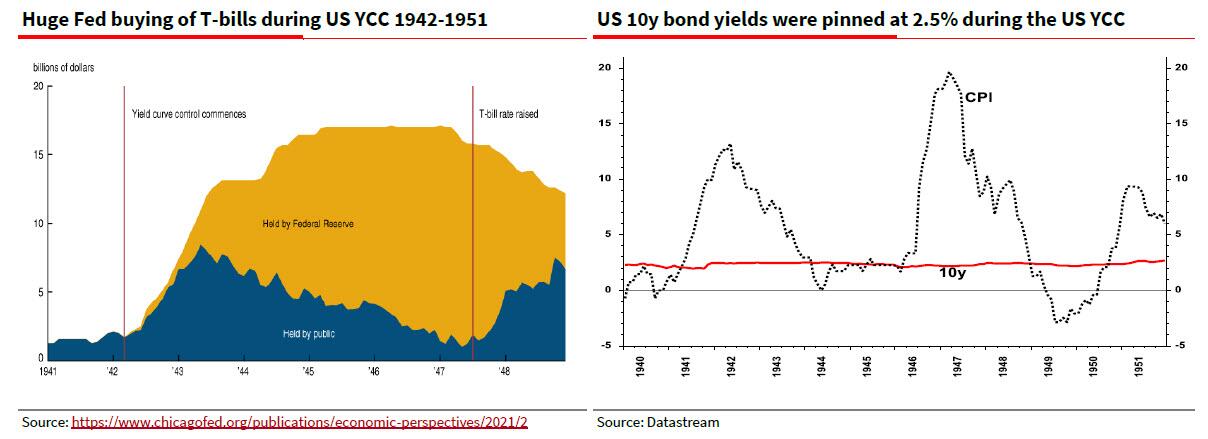

For those who may not have been around back in the 1940s when the US – and the Federal Reserve – was the first developed nation to utilize YCC to kickstart the US economy at a time of record debt to GDP, here is a quick primer from the SocGen strategist: “Financial Repression essentially entails holding interest rates below the rate of inflation for a lengthy period to allow debt to be ‘burned off’. This is a tried and trusted way for governments to wriggle free from excessive debt (eg the US after WW2). The leading economic historian Russell Napier explained how this works in an informative 2021 interview with The Market NZZ – link.”

And indeed, it was only a few years ago, just before the pandemic sparked a stimulus flood of epic proportions, that western policy makers were switching to average inflation targeting and stating that they would run economies hot to create that higher inflation (they got it but not because of AIT). That was the first notable attempt to shift toward Financial Repression, but as Edwards notes, “unfortunately they were too successful and let the rampant inflation cat out of the bag.”

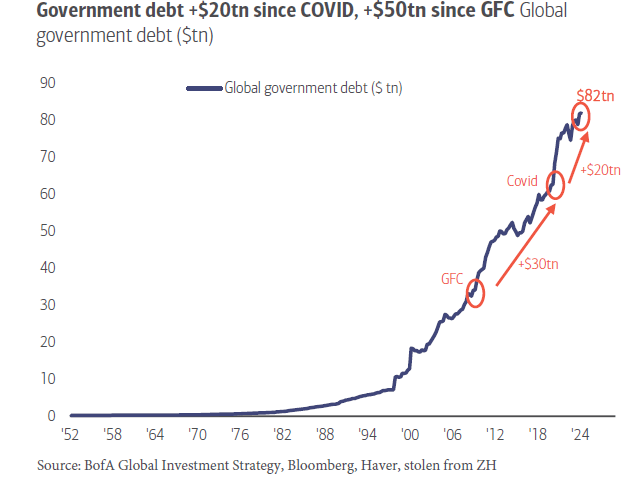

Which brings up the $64 trillion question: “Do the Fed and ECB really want inflation to return to pre-pandemic inflation lows?” Well, with global debt now about 7x higher in just the 21st century, and fast approaching $100 trillion, meaning it will all have to be inflated away somehow…

… Edwards’ answer is: “Not in my view.” And so while western economists deride Japan for its YCC policies, Albert says “that is where I think the US and Europe are heading as intractable government deficits drive up bond yields. During the next crisis, don’t be surprised to see yet more Japanification of western central bank policy. Plus ça change.” And don’t be surprised if the dollar – while appreciating against the rest of the world’s doomed currencies in the closed fiat-system loop – hyperdevalues against such finite concepts which mercifully remain out of the fiat system, such as gold and crypto.

Biden loves to blame Republicans for the border crisis. Although he has it in his power to close and secure the border, but won’t. It’s easier to blame the opposition, like “extreme MAGA Republicans.” Huh, I didn’t realize that as a conservative American I am considered extreme by the Biden Administration.

Unfortunately, Biden, Schumer and Johnson only provided financial support for Jordan, Lebanon, Egypt, Tunisia and Oman. In the form of $380 million.

As the US falls to 23rd in World Happiness ranking. Based, in part, on Biden’s idiotic open borders policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.