Today’s import and export numbers for the USA show a disturbing trend. US export prices rose +17.2% YoY in July. That is the third consecutive month of +16.9% and above export prices growth.

That begs the question: Is The Federal Reserve exporting inflation to US trading partners through its financial repression?

The University of Michigan survey of consumers is out and their buying conditions for housing (good) was a disasters. Only 32% on consumers view buying conditions for a house as good. That means that 68% think buying conditions are not good. Why? With the Case-Shiller National Home Price Index growing at a scorching 16.6% YoY making housing simply unaffordable for many Americans.

On a different note, The Fed’s overnight reverse repo facility (aka, the slosh” just breached the $1 trillion mark.

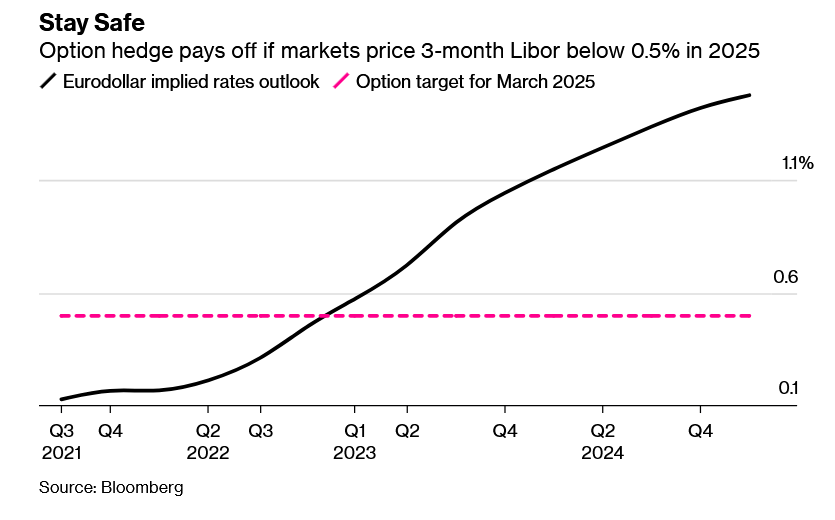

Treasury yields are rising amid optimism over the global recovery but there has been a run on Eurodollar options betting the Federal Reserve will opt not to raise interest rates at all.

Traders this week have been busy snapping up Eurodollar call options on underlying March 2025 futures that target three-month Libor to fix below 0.5%. These pay off if markets price the Fed keeping its benchmark at its lower bound until then. Futures markets are currently anticipating Libor will rise to about 1.47% by the first quarter of 2025.

So, it looks like The Fed (aka, Greenman) may not be going anywhere.

Mortgage rates in the U.S. surged to the highest level in a month.

The average for a 30-year loan was 2.87%, up from 2.77% last week and the highest since July 15, Freddie Mac said Thursday. Mortgage rates have been below 3% since the beginning of July.

Such a small increase in mortgage rates should have little impact on home purchases, but it will dampen mortgage refinancings.

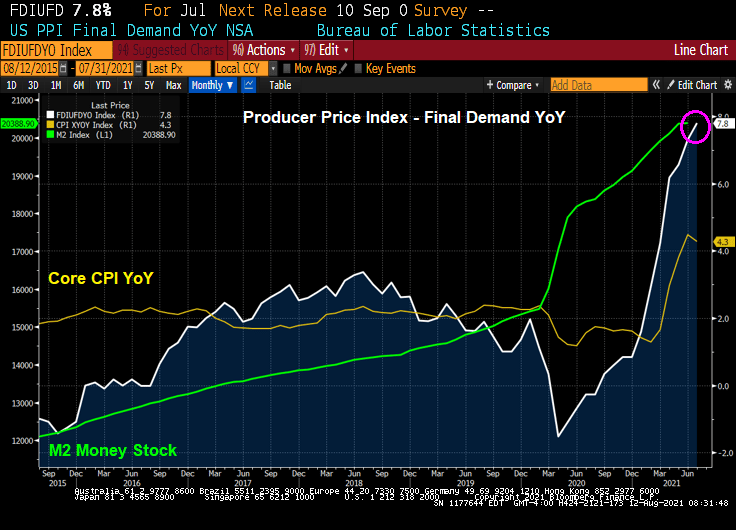

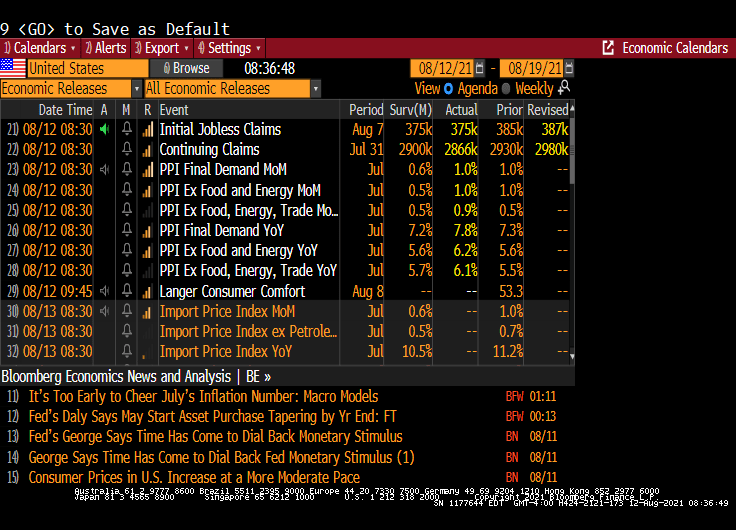

Well, economists were expecting a 7.2% YoY print of the Producer Price Index – Final Demand. But July’s print came in hot … at +7.8% YoY. Compare that with the Core Consumer Price Index YoY of +4.3%.

The month-over-month PPI Final Demand is showing a run rate of 12%! (1% in July x 12 months).

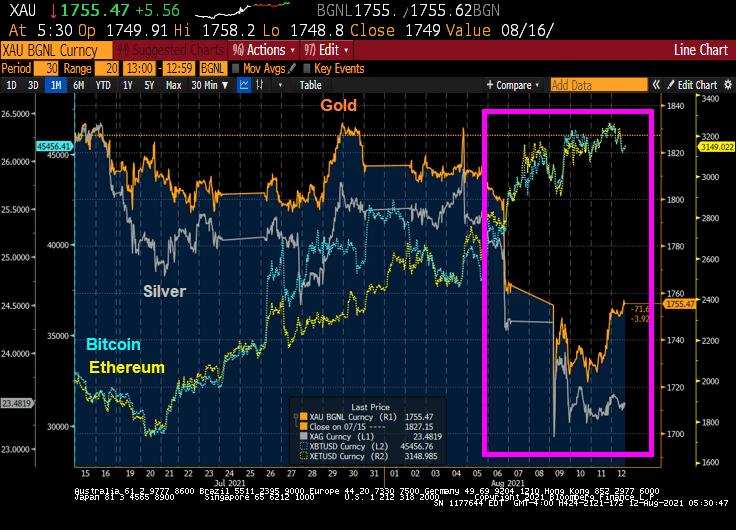

The Covid Delta Variant seems to be picking up steam, we are seeing “flight to safety” assets other than Treasuries rising.

Gold and Silver experienced some serious corrections last week, perhaps because things were looking up. Then we saw Anthony Fauci scaring everyone about Covid … again. So, there is enormous uncertainty about how this will play out. In other words, ALARM!

Bitcoin and Ethereum have been climbing since Gold and Silver corrected last week. But both are up this week, particularly Gold.

The US Dollar is down slightly since the same time last year and M2 Money Stock growth has slowed.

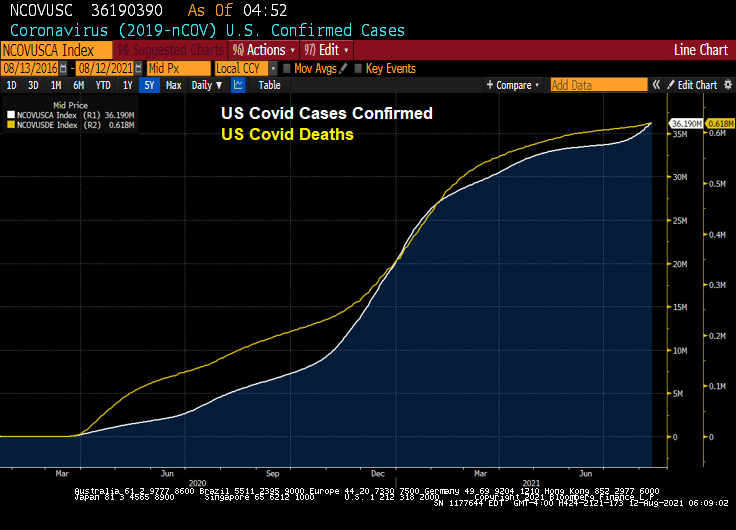

Here is a chart showing another fear factor: the rise of the Covid Delta Variant. Deaths are only 1.7% of confirmed cases (if we believe the actual cause of death).

Rents in the New York City metropolitan statistical area — which also encompasses northern New Jersey and Long Island — dropped in the 12 months through July for the first time since 1958, according to monthly data on consumer prices published Wednesday by the Labor Department. Before that, the series indicates rents in the region hadn’t fallen on a year-over-year basis since 1934. The figures underscore the historic nature of the pandemic and its impact on the U.S. economy.

On the other hand, New York City home prices are growing at a +15.3% YoY pace.

Apparently, in 1958 Americans liked Ike, but didn’t like living in New York City.

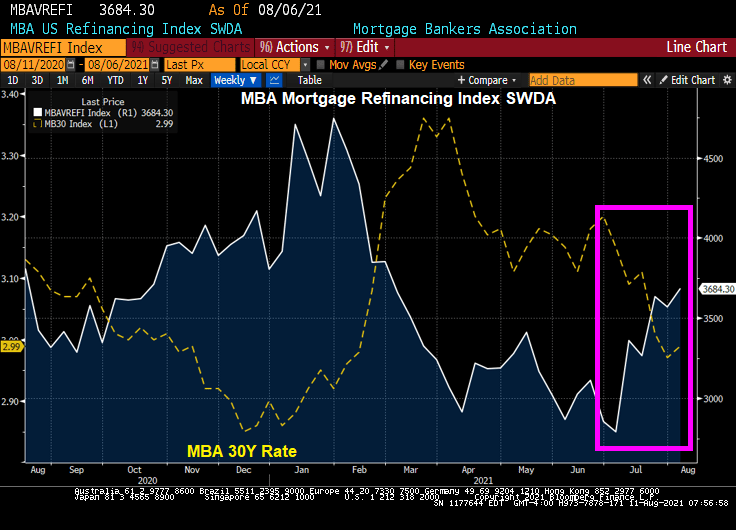

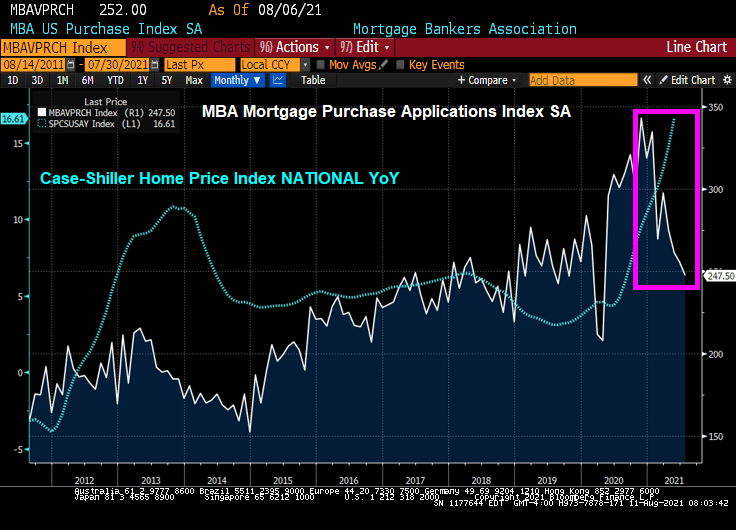

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 6, 2021.

The Refinance Index increased 3 percent from the previous week and was 8 percent lower than the same week one year ago. But recent declines in mortgage rates have produced a mini-refi wave (pink box).

The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 18 percent lower than the same week one year ago. But rapidly rising home prices have cooled mortgage purchase applications since the beginning of 2021.

Here is the data from the MBA showing a rise in mortgage applications from the previous week of 2.79%.

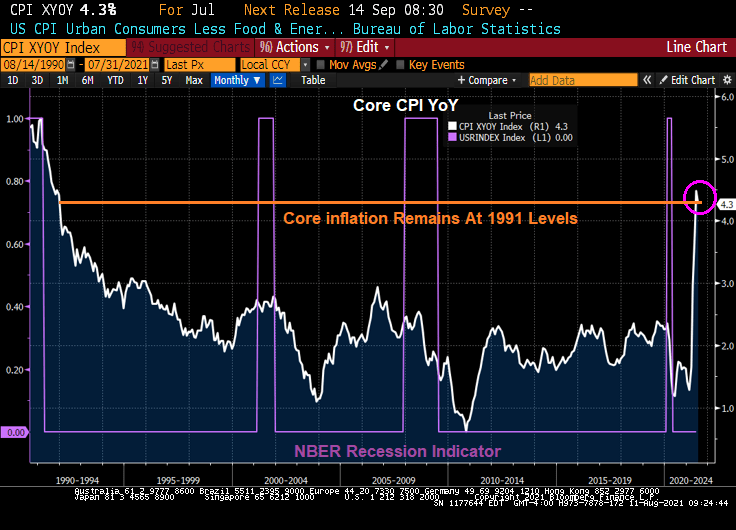

US inflation remains nears its highest level since 1991, but moderated slightly.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.5 percent in July on a seasonally adjusted basis after rising 0.9 percent in June, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 5.4 percent before seasonal adjustment.

The indexes for shelter, food, energy, and new vehicles all increased in July and contributed to the monthly all items seasonally adjusted increase. The food index increased 0.7 percent in July as five of the major grocery store food group indexes rose, and the food away from home index increased 0.8 percent. The energy index rose 1.6 percent in July, as the gasoline index increased 2.4 percent and other energy component indexes also rose.

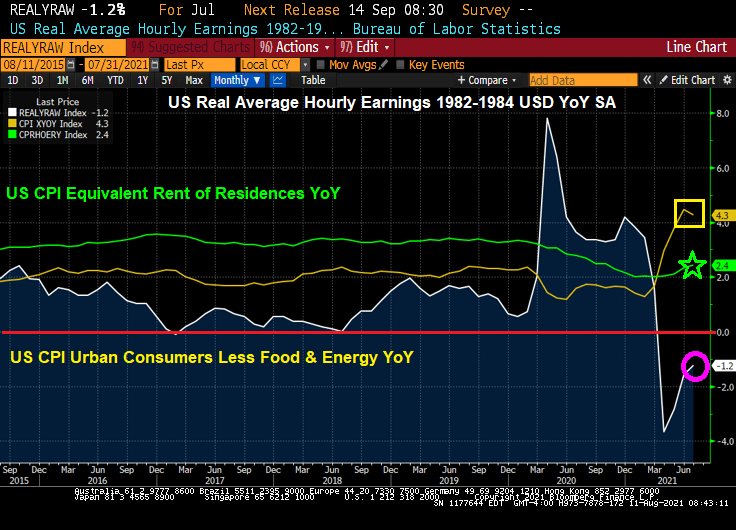

US Real Average Hourly Earning YoY “rose” to -1.2% as core inflation “moderated” to +4.3%, the second highest reading since 1991.

Core inflation remains at 1991 levels.

With core CPI growing at 4.3%, the baseline Taylor Rule model implies that the Fed Funds target rate should be 7.05%, not the current rate of 0.25%.

As The Fed keeps rolling the dice on zero-interest rate policies.

You must be logged in to post a comment.