Global uncertainty hits an ALL-TIME HIGH.

Higher than Covid, the 2008 financial crisis, and the dot-com crash COMBINED.

You know what that means!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Global uncertainty hits an ALL-TIME HIGH.

Higher than Covid, the 2008 financial crisis, and the dot-com crash COMBINED.

You know what that means!

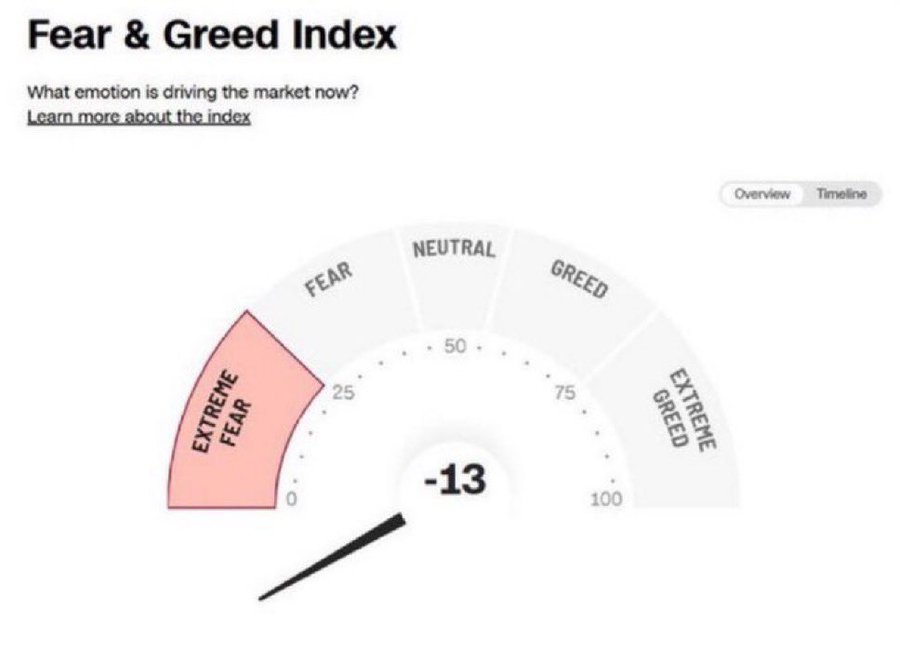

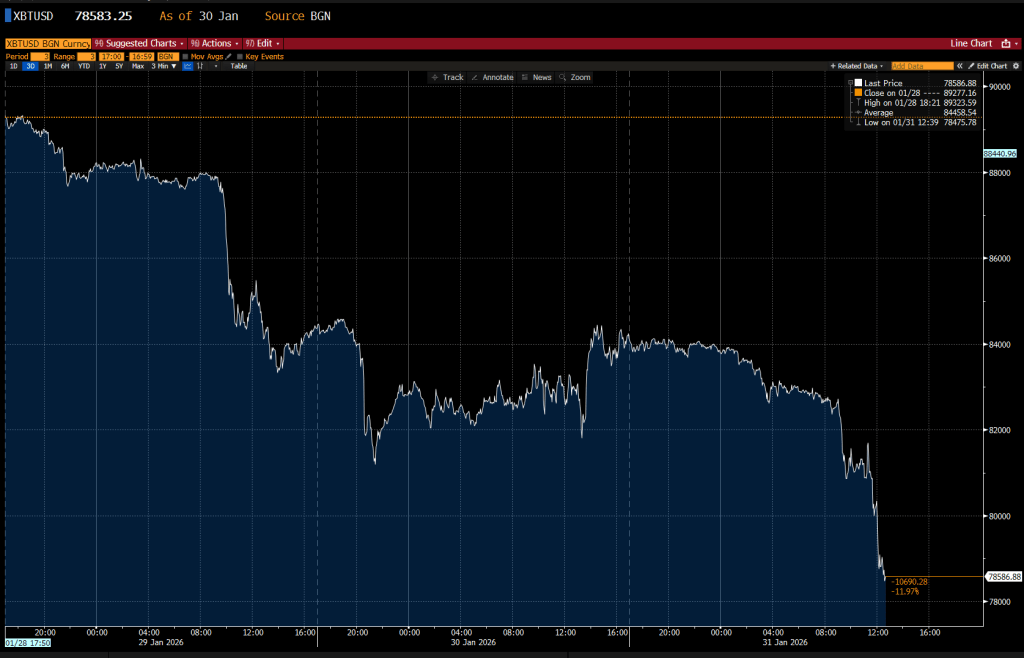

Collapsing crypto and metal prices coupled with a tanking stock market is pointing to EXTREME FEAR.

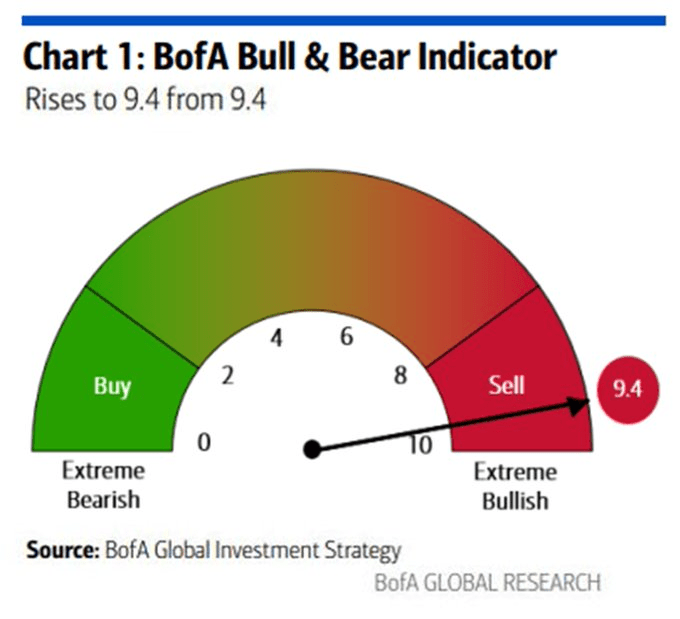

The BofA bull and bear indicator says the same thing.

The realization that government is just a money laundering operation for politicians and that The Fed is just a friend of the big banks says it all.

Call it the Post Powell Panic! After The Fed decided to do nothing at the FOMC meeting.

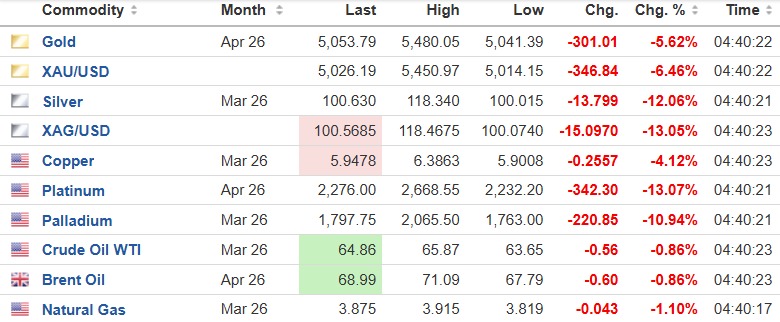

Gold is down -12% from the peak, trading below $5,000.

Silver is down -21%, trading below $100 for the first time since Friday, officially in a BEAR MARKET.

Rough night in the precious metals market space. An absolute BLOODBATH.

Is the top behind us?

Gold -6%

Silver -12%

Copper -4%

Platinum -13%

Palladium -11%

Trillions in market cap wiped out in a few hours.

Powell at The Fed FOMC meeting imitating former Fed Chair Janet Yellen. And Trump has nominated Kevin Warsh for Fed Chair who is expected to maintain Fed indepence.

Wipeout! $6 TRILLION ERASED IN 60 MINUTES

Gold wiped out nearly $3 trillion

Silver erased nearly $790 billion

S&P 500 lost nearly $780 billion

Nasdaq wiped out $750 billion

Crypto market erased $100 billion

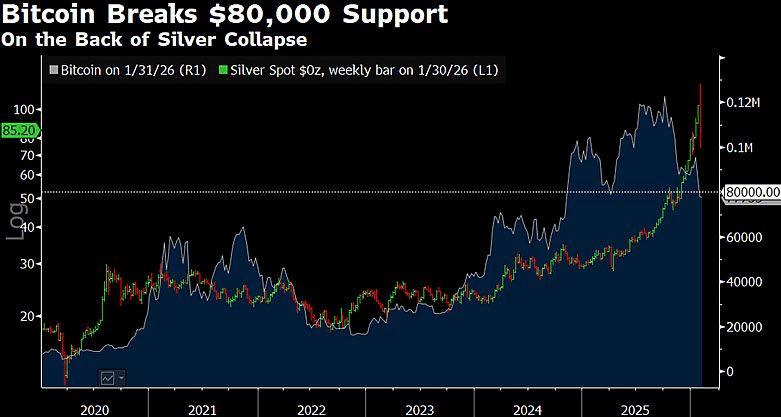

Insane crash at US market open.

Gold suffered too.

Along with Bitcoin.

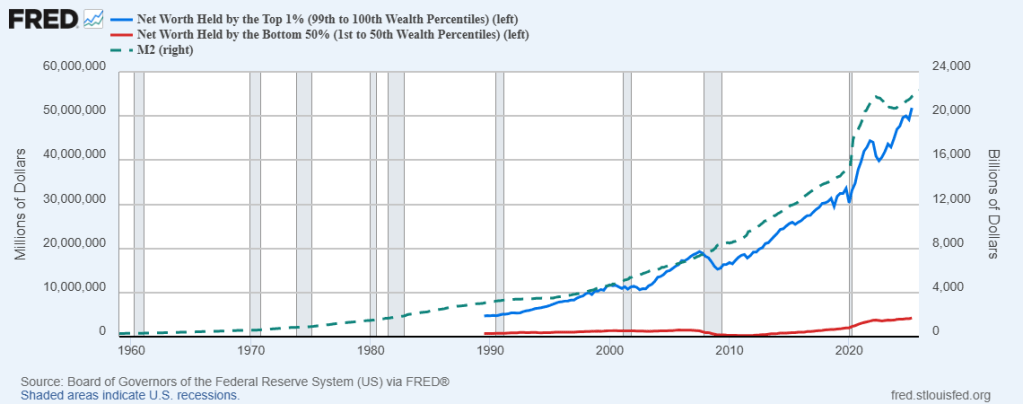

A good Federal Reserve don’t. Print money, that is.

The Federal Reserve prints a lot of money (M2). Unfortunately, it largely benefits elites (the top 1%). The bottom 50% get some benefits, but the gains in net worth largely benefits the elite class.

This sounds like a legal Somali daycare scheme. Perhaps The Fed should be renamed “The Federal Quality Learing Center.”

Yes, Somalis have daycare centers in Columbus Ohio. Thanks Governor Dewine for doing absolutely nothing to reign in their fraud. /sarc

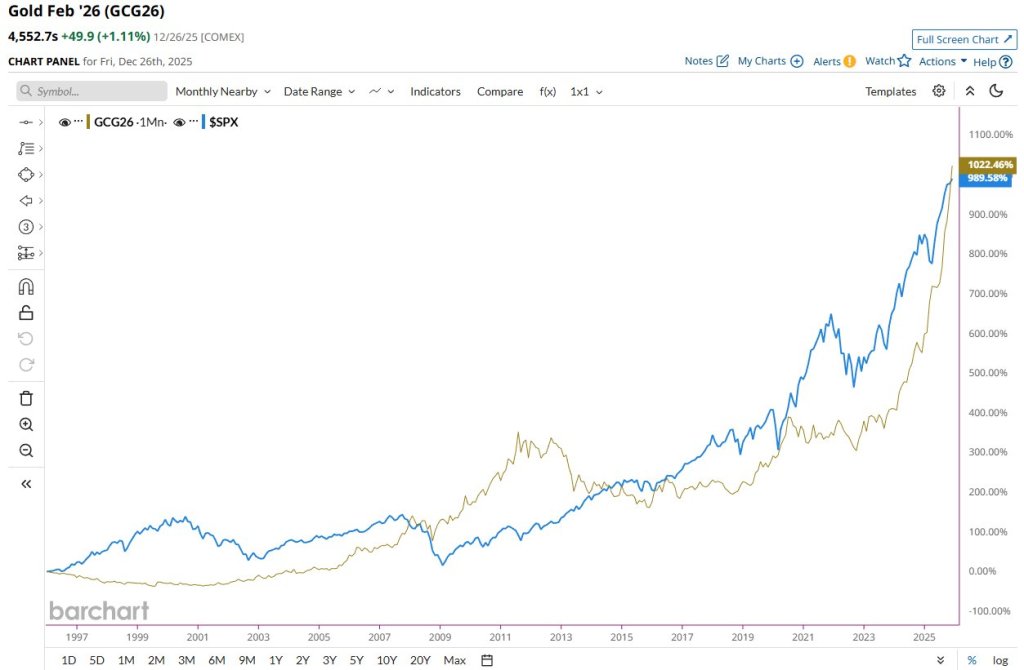

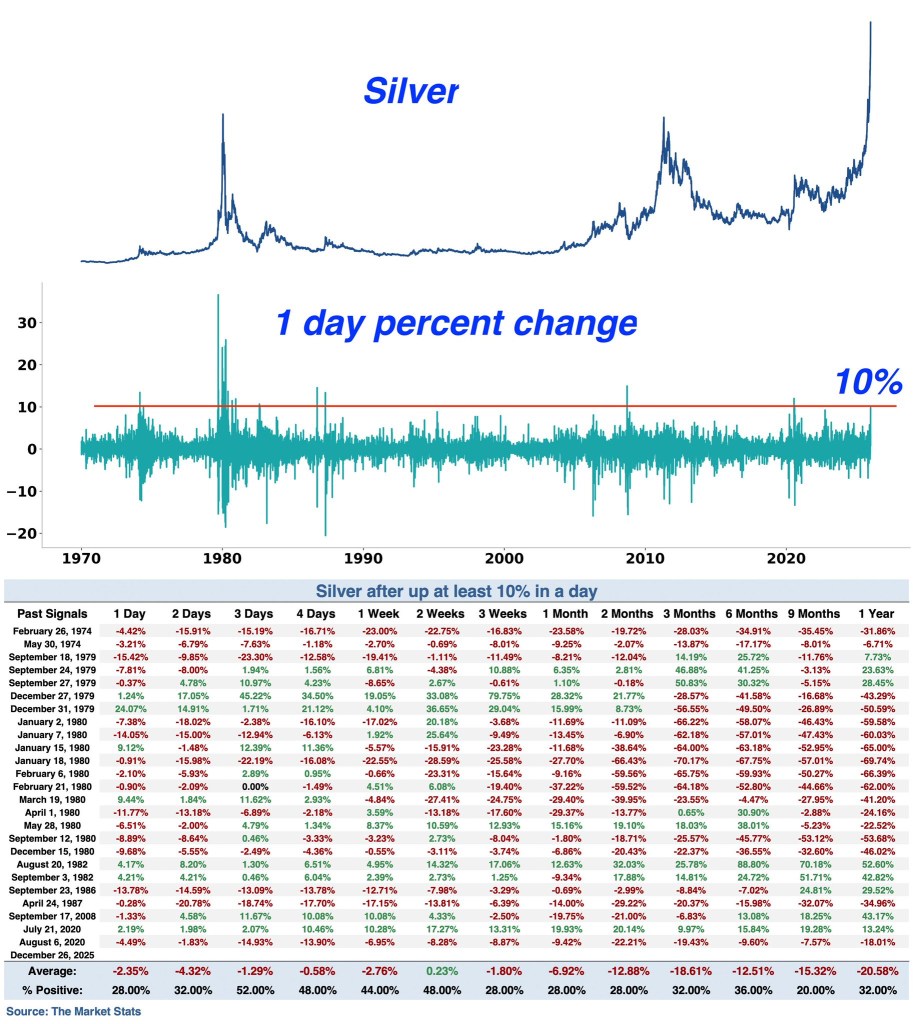

Gold and silver. Gold is now outperforming the Stock Market over the last 30 years.

Silver is up 10% on Friday.

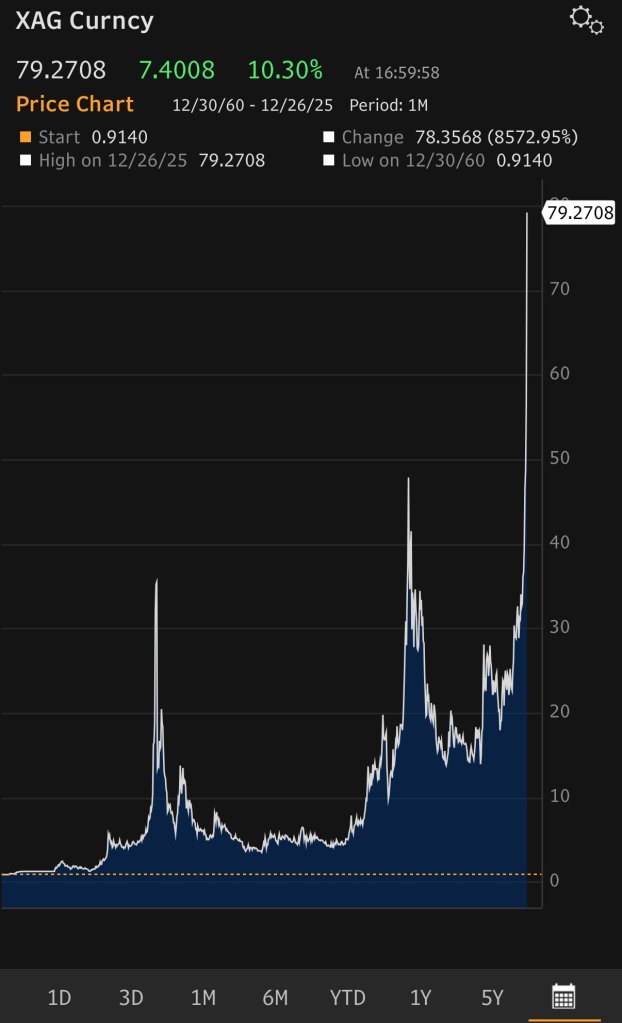

Silver (XAG) just hit the $79.2708 price point.

Dino’s song. A shout-out to David Freiberg on the Gibson SG bass and John Cipollina on the Gibson SG guitar. I love the Gibson SG!

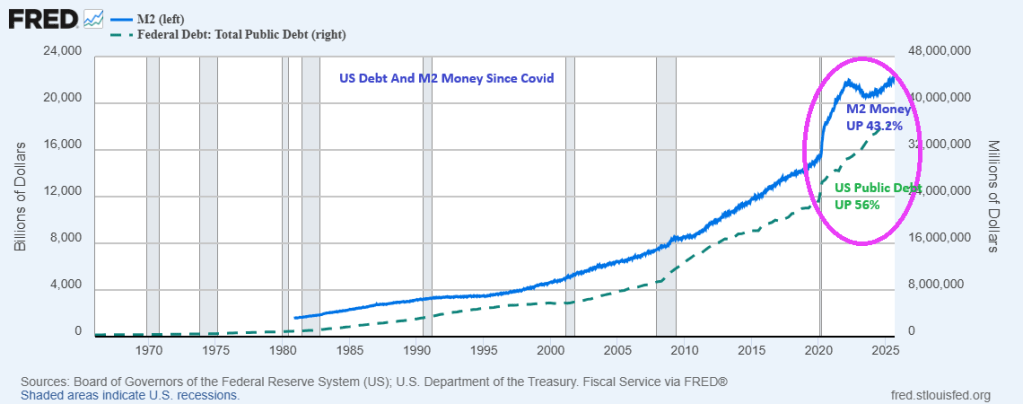

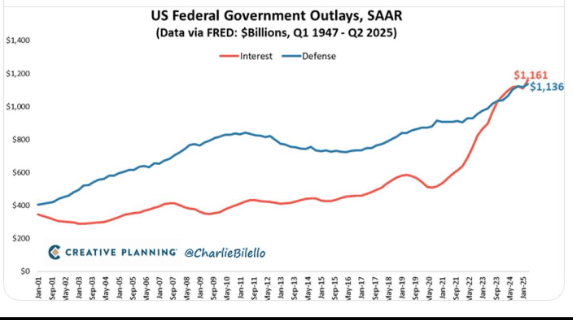

The Federal government is having a party! A spending party requiring massive growth in Federal borrowing AND Fed M2 money printing.

Federal borrowing has increased by 56% since Covid in 2020. And Fed M2 Money increased by 43.2% since Covid outbreak.

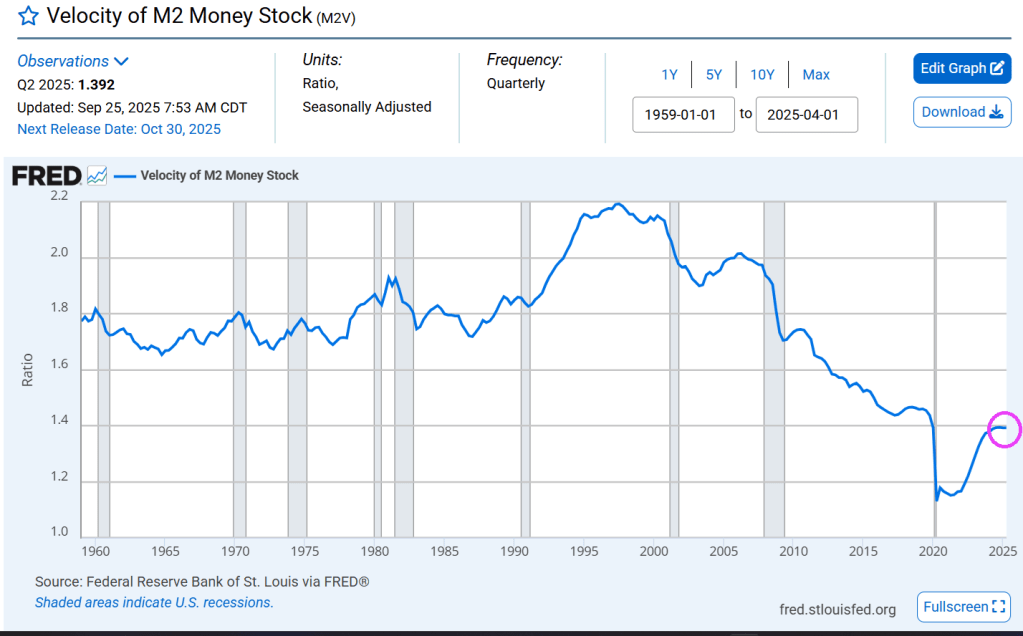

M2 money velocity (GDP/M2) is now at 1.392.

As of Q2, interest payments on the national debt exceeds spending on defense.

Despite being shut down by Democrats and Chucky Schumer, The Federal government and Federal Reserve continue to borrow and print money like crazy.

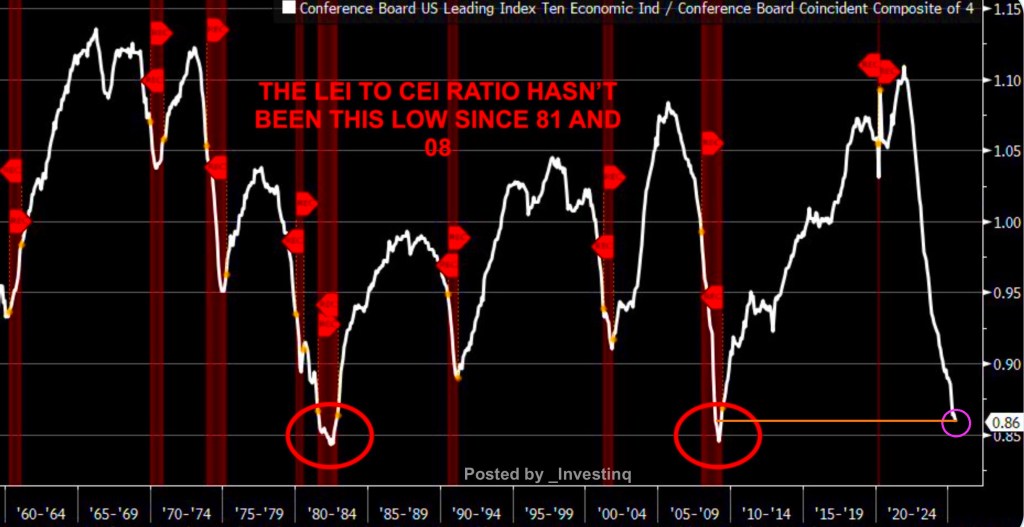

The Fed will have to whip it good with rate cuts if the recession warnings are an indicator of what lies ahead for the US economy.

The ratio of The Conference Board’s Leading Economic Indicators (LEI) vs. The Conference Board’s Coincident Economic Index (CEI) ratio hasn’t been this low since 2008.

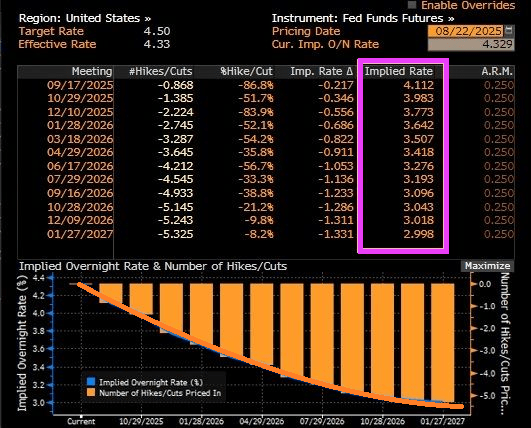

Fed Funds Futures are signalling rate cuts at the September 17th FOMC meeting and December 10th meetings.

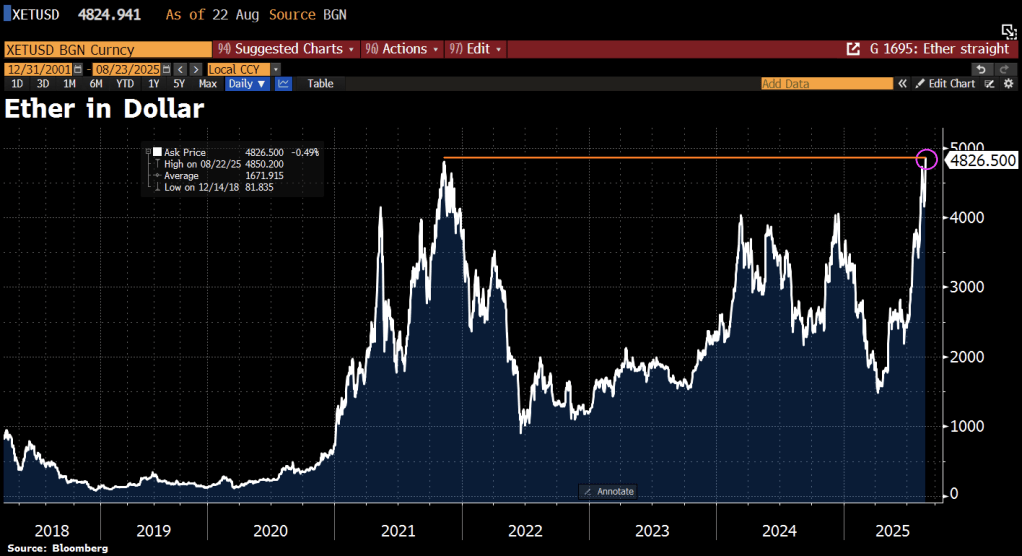

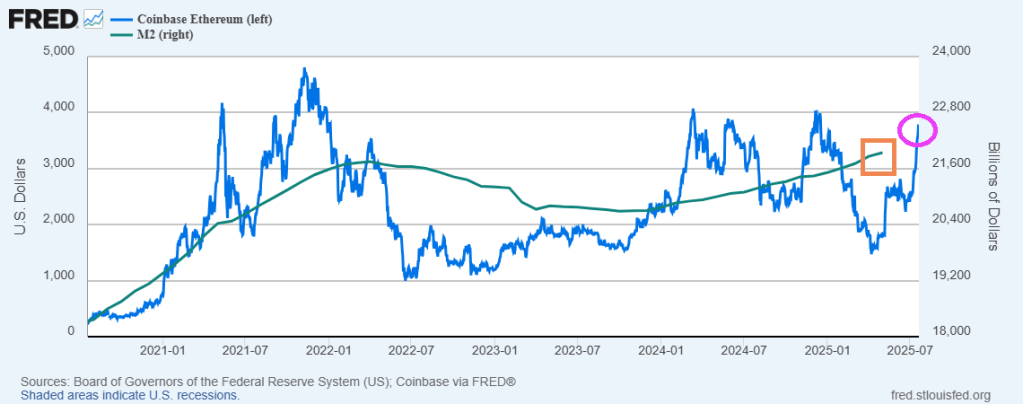

On the crypto front, Ethereum is soaring.

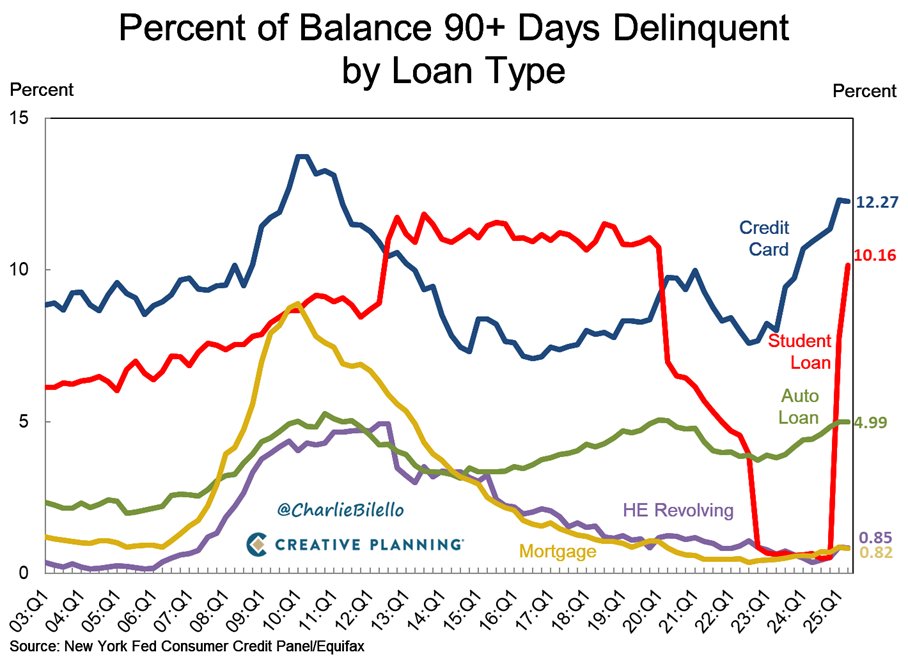

Debt stress is mounting!

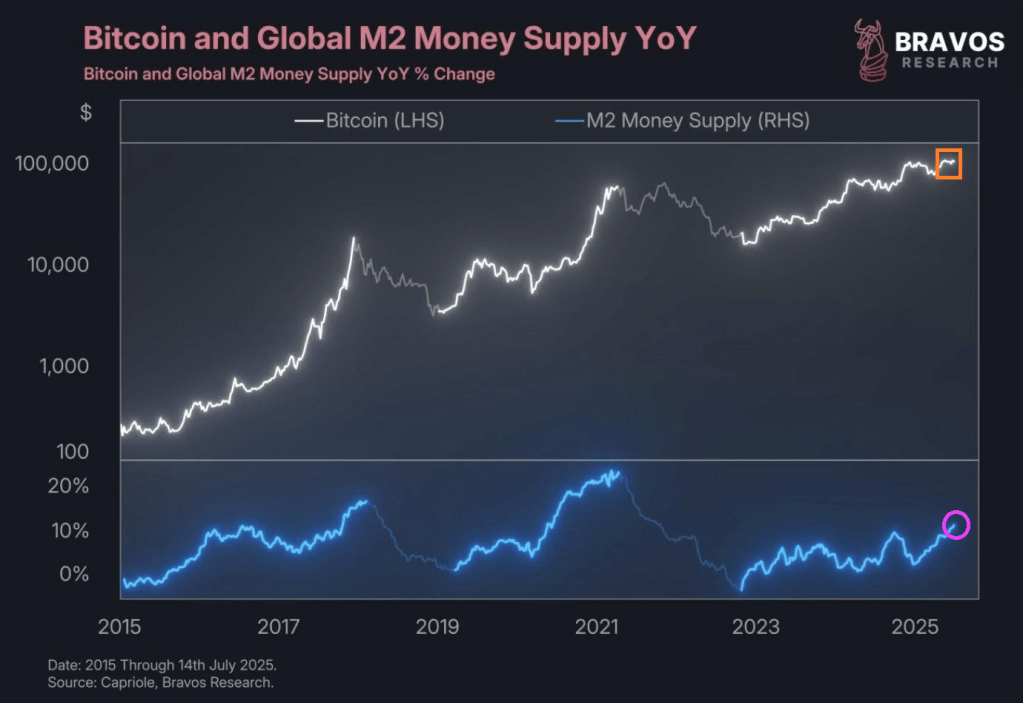

Keep on printing is the song of The Federal Reserve. But its the same all over the world as global central banks are printing zads of money too.

Bitcoin keeps on growing in price as global M2 Money supply keeps on growing.

And the same is true for ethereum. It keeps growing as M2 Money keeps growing.

It is another example of government gone wild!

You must be logged in to post a comment.