Welcome to the whacky world of employment in the AI era!

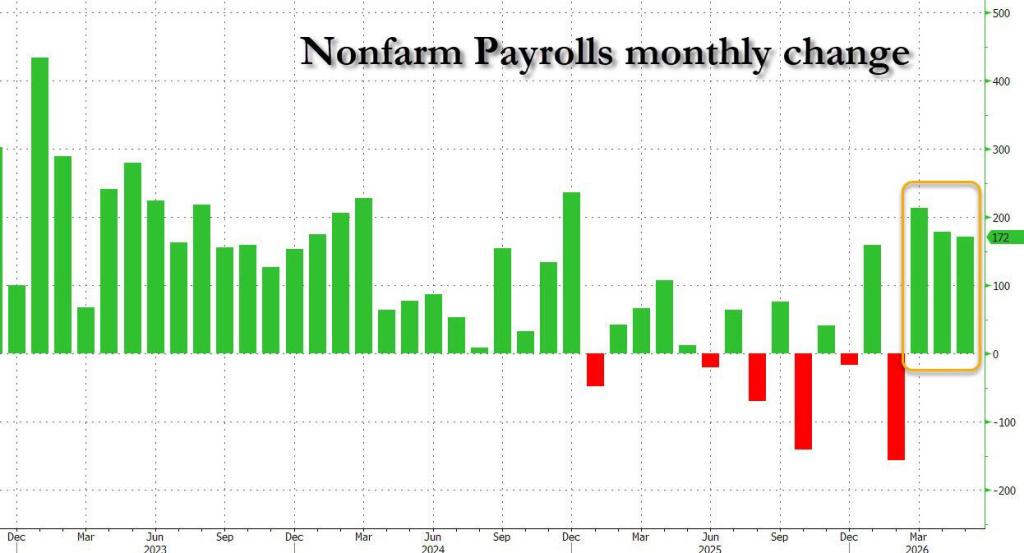

US jobs rose by 172K in May. Local government rose by 55K while finance/insurance jobs fell by -20.2K in May.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Welcome to the whacky world of employment in the AI era!

US jobs rose by 172K in May. Local government rose by 55K while finance/insurance jobs fell by -20.2K in May.

Trump has been President for 1 year and fighting against Biden and the Democrats economic misery.

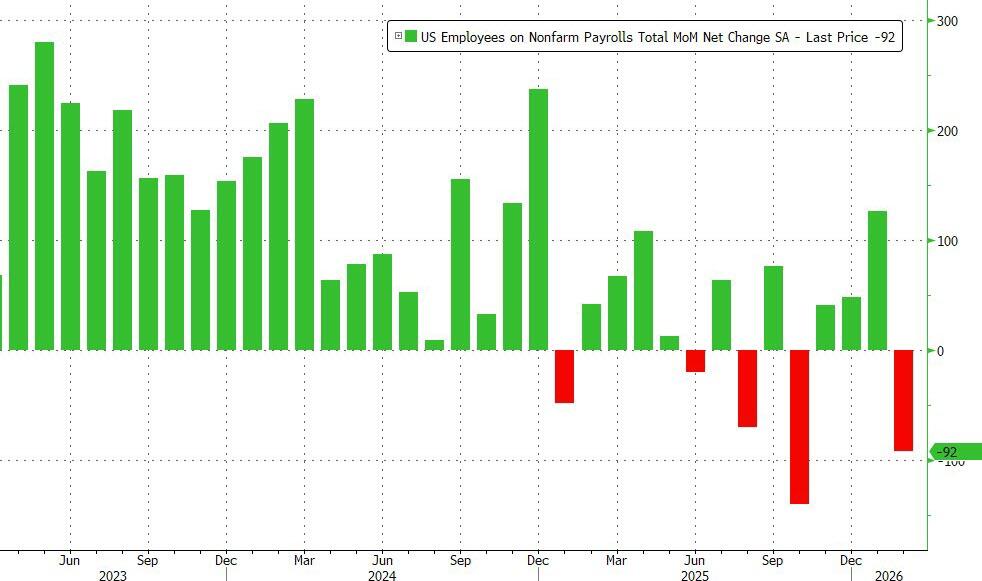

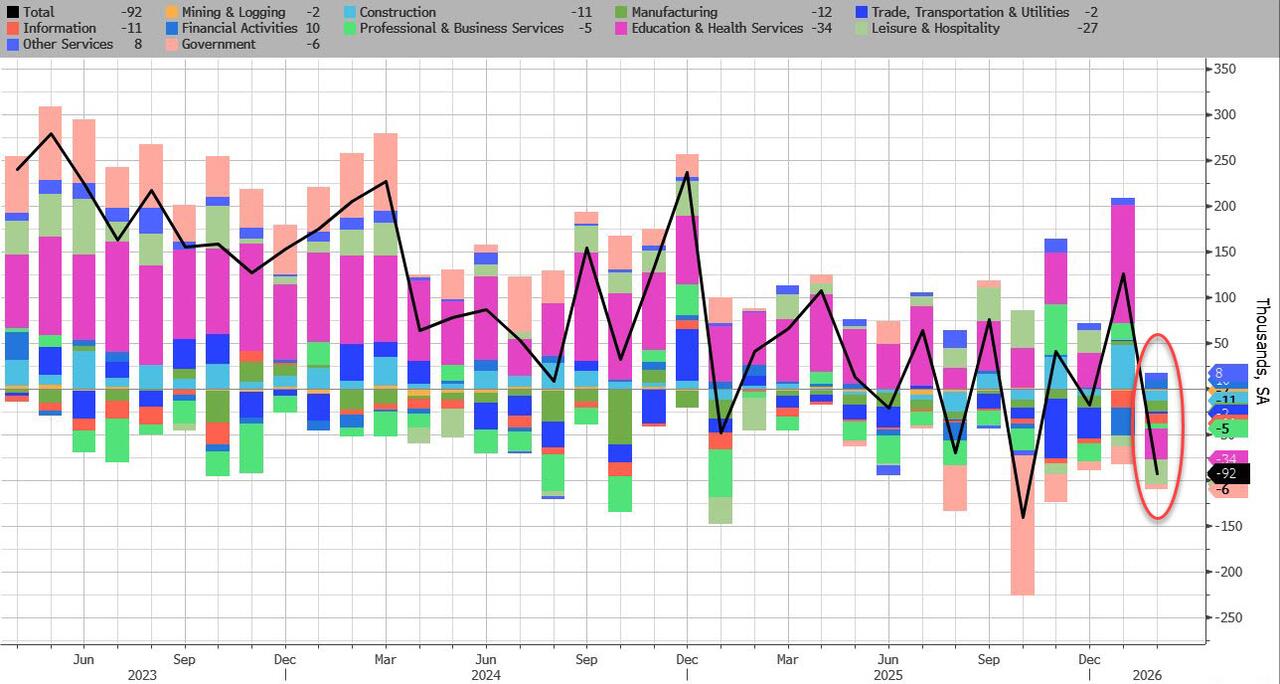

In February, the US lost 92,000 jobs, a huge drop from the downward revised 126K in January, and the second worst print since 2020 (only October’s shock -140K was worse), and this time, the massive drop can’t be dismissed as a one-time drop in government payrolls. The number of private payrolls dropped by 86K, also a huge miss to estimates of a 60K increase.

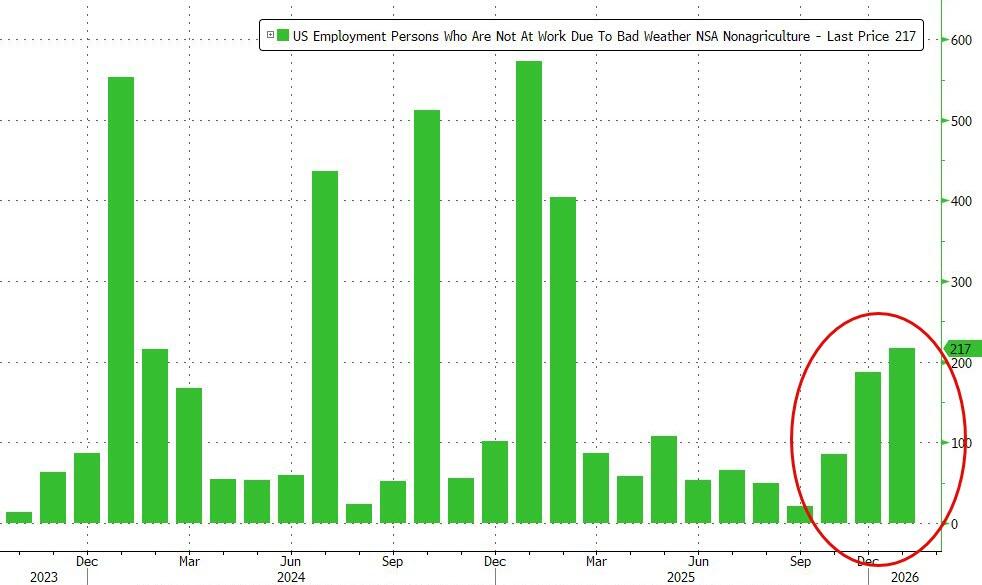

One potential mitigating factor: the number of people who were unable to work due to weather surged to 228K in February, well above last year’s level 167K, due to the powerful winter storms hitting the US.

Turning to the establishment survey, which unveiled the shocking February drop, the BLS reported a broad-based decline, driven by striking employment workers:

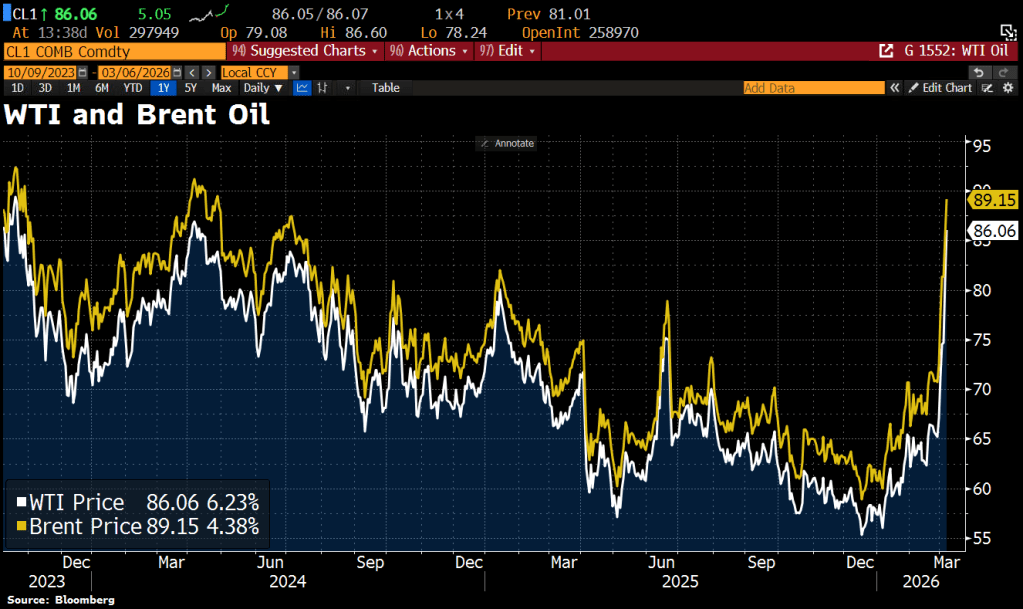

Switching to oil, we see the West Texas Intermediate and Brent Oil prices soaring on the attacks on Iran.

To soothe you.

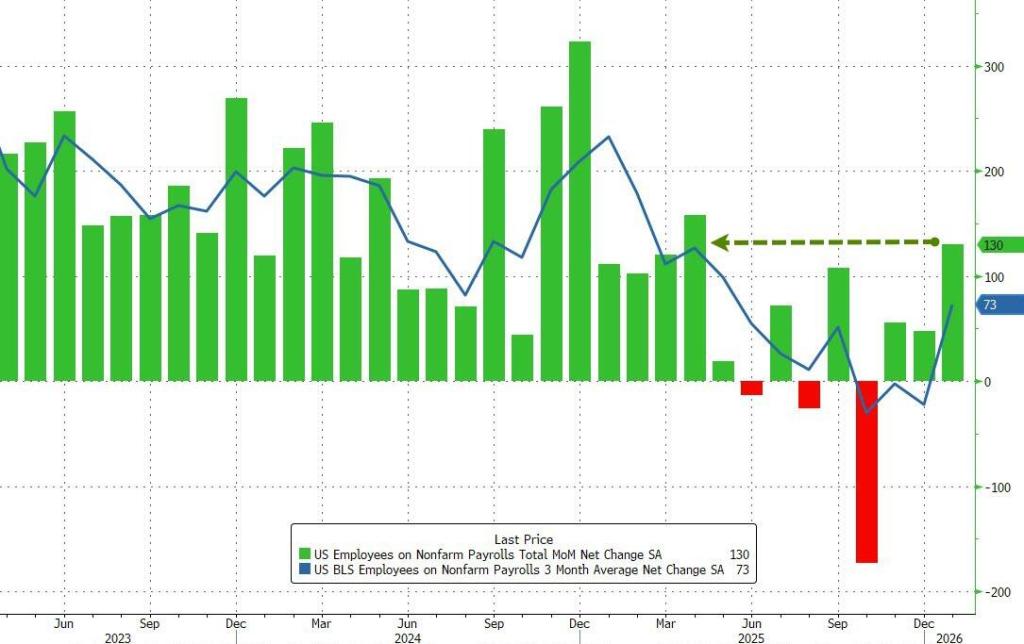

In January the US added 130K jobs, double the 65K median estimate and up from a downward revised December print of 48K (vs 50K previously). This was also the highest monthly jobs increase since December 2024.

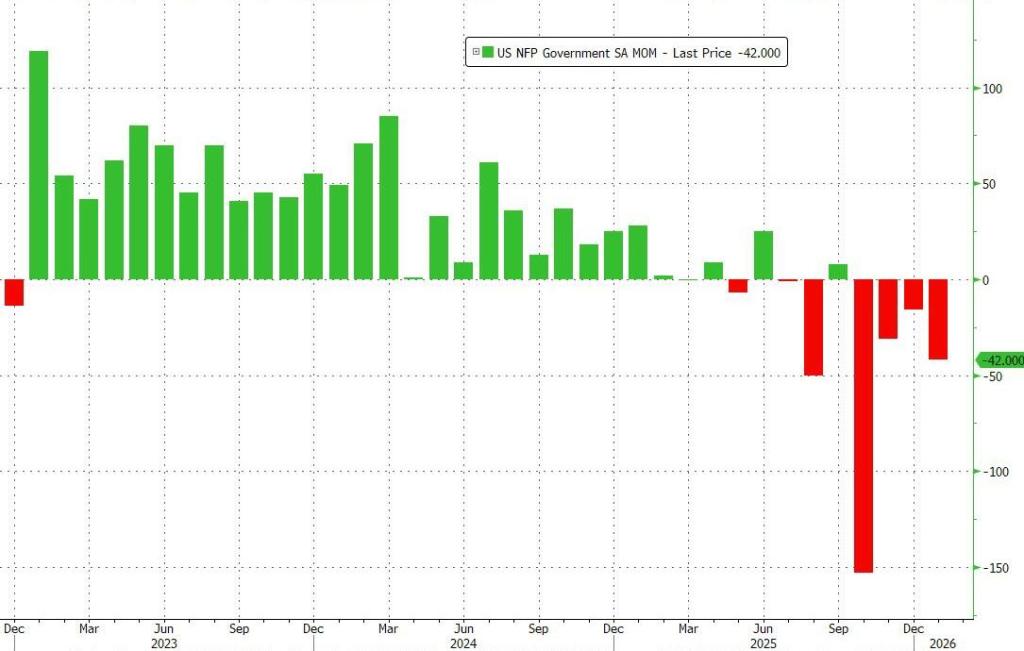

Government jobs fell by -42k. Furthering the trend for growing private sector employment and declining government employment.

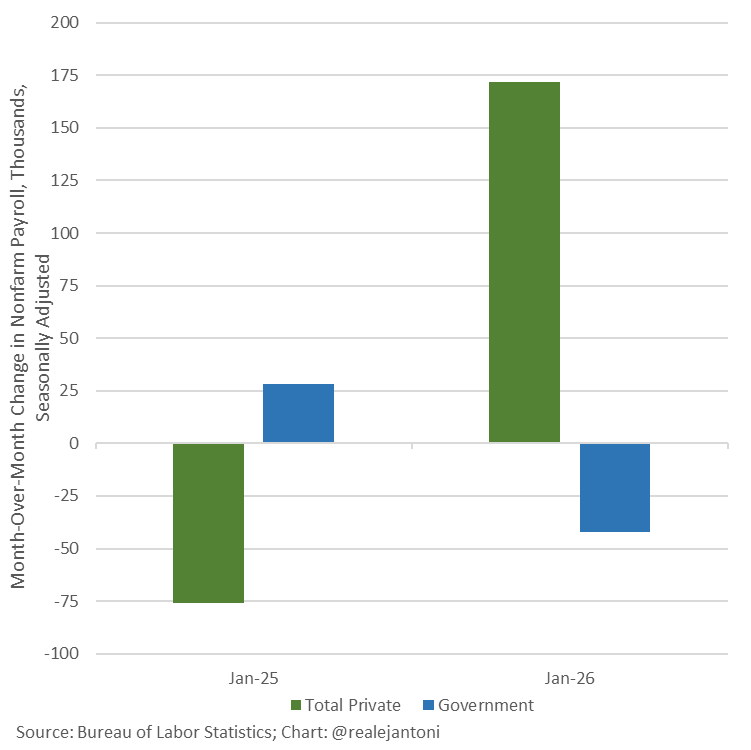

Compared to Jan 2025, we see the growth in private sector employment and decline in government jobs.

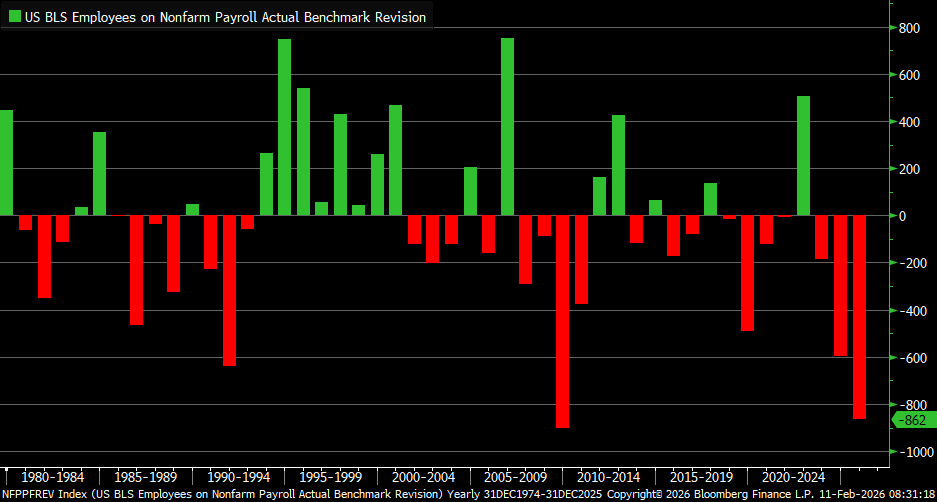

The jobs report comes with the largest jobs revision since 2009/2010.

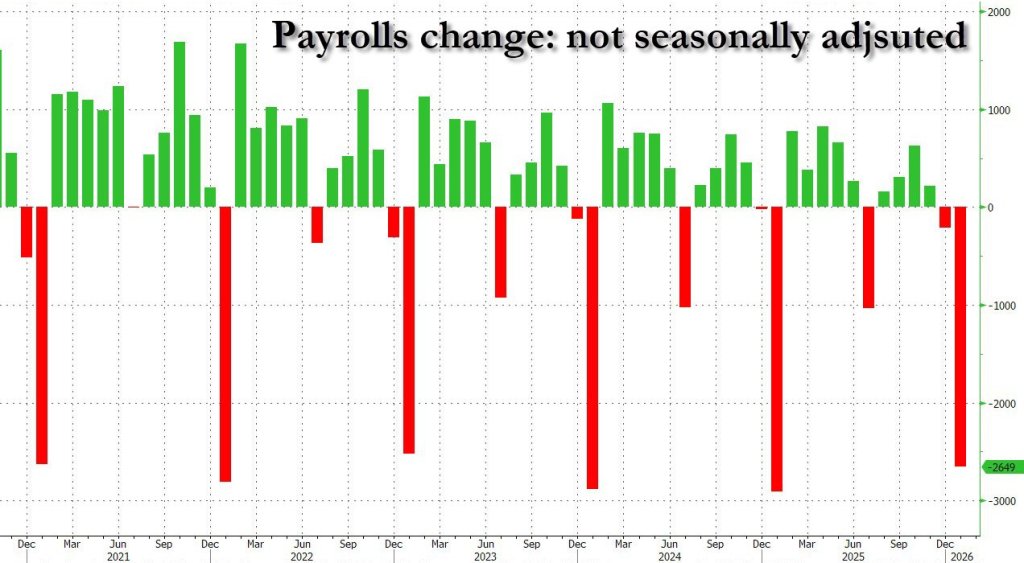

Now for the bad news, As my OSU/Chicago/GMU know, I prefer NON seasonally adjusted data when at all reasonable. While Seasonally adjusted jobs added SEASONALLY ADJUSTED was +130K, NOT seasonally adjusted jobs added was -2.649 Million.

Happy birthday to Tina Louis (Ginger from Gilligan’s Island) who turned 92 today.

Well, tariffs didn’t turn out to be a lethal weapon as Democrats predicted. The US economy continues to grow!

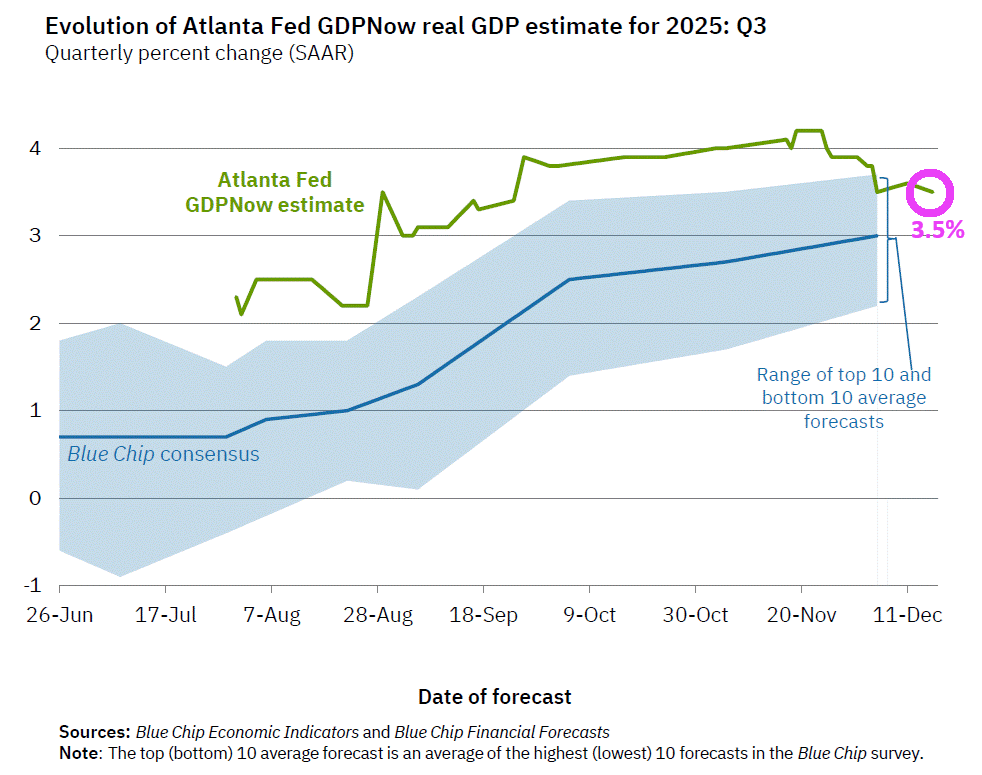

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.5 percent on December 16, down from 3.6 percent on December 11. After this morning’s releases from the US Census Bureau and US Bureau of Labor Statistics, the contributions of consumer spending and inventory investment to third-quarter real GDP growth fell slightly to 1.84 and 0.09 percentage points, respectively.

All signs except real estate construction and imports point to continued economic growth.

But as long as The Federal Reserve continues to print money (M2), the economy will continue to grow. Keep on printing?

Roll out the barrel! As in Fed money printing.

How can the current housing disaster be fixed? One answer is to build more homes (made difficult by local government zoning and building policies). Another is increase household income. But Fed money printing is the easiest way to increase home prices.

Since the Federal government spending spree associated with Covid ended, median household income has declined. But so have home prices.

But in terms of home price growth compared to median household income, you can see that home price growth has slowed after the Covid spending spike, but so did median household income.

Pray that The Fed doesn’t resort to trying to fix the housing market. They will only make things worse.

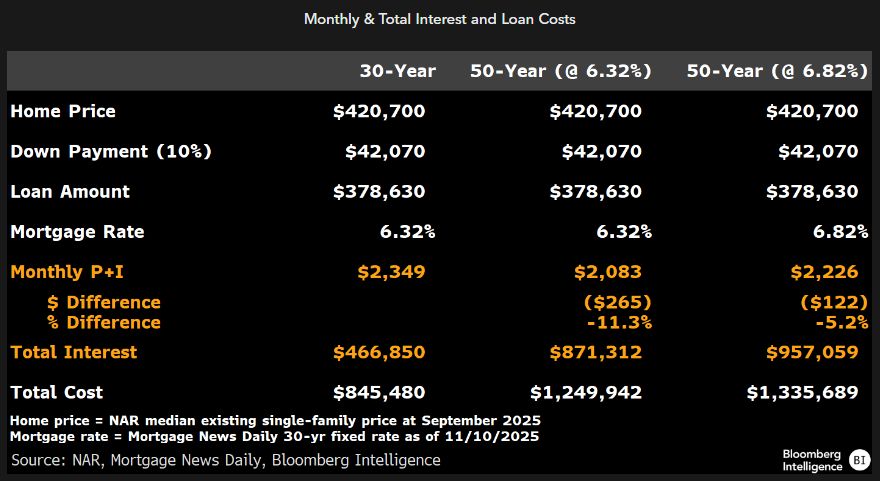

Every time the government tries to make housing more affordable, they make the problem worse. Some people should rent and not fall for the government’s latest folly, the 50-year mortgage.

True, the 50-year mortgage would lower the monthly payment by several hundred dollars (see the following example where the monthly payment falls from $2,349 to $2,083. Or from $2,349 to $2,226 if the most rate increases with the longer mortgage life. BUT total interest paid increases 87% if the 50-year rate remains the same and 105% if the rate rises.

Principal paydown slows to a crawl with a 50-year mortgage, leaving the lender (or mortgage holder) exposed to higher risk if home prices fall.

Government housing policies remind me of the Curly versus the oyster stew skit. where Curly can’t catch the oyster. Yet keeps trying.

The 50-year mortgage reminds me of the ill-fated National Homeownership Strategy under Bill Clinton. By prdering all Federal housing finance entities to work with HUD, the National Homeownership Strategy helped crash the housing market (watch The Big Short!)

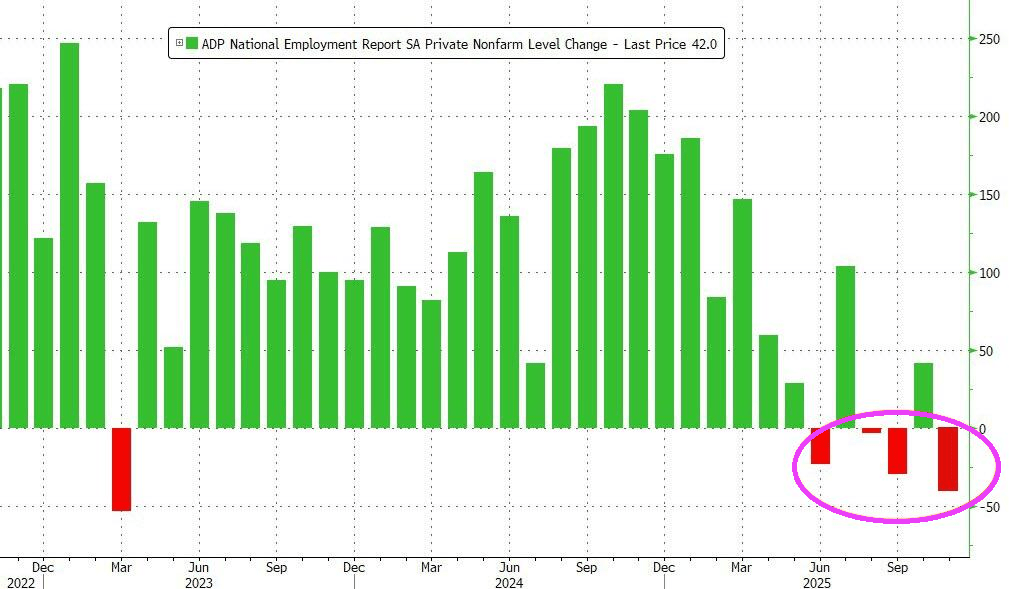

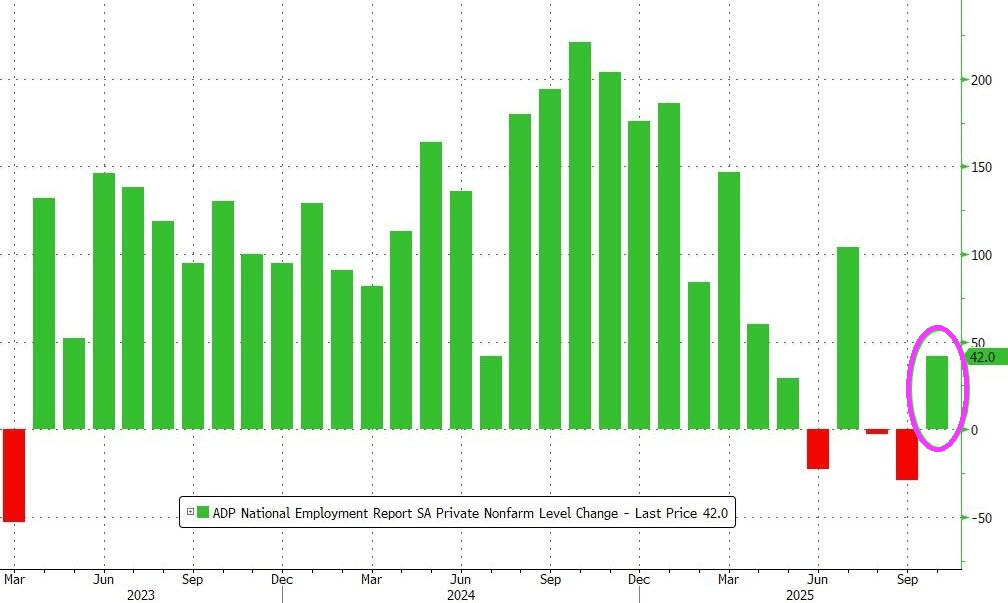

The Federal government is still shut down, so we have to rely on ADP for jobs numbers.

The ADP weekly jobless report pointed to a deterioration in US labor momentum, stating that “for the four weeks ending Oct. 25, 2025, private employers shed an average of 11,250 jobs a week, suggesting that the labor market struggled to produce jobs consistently during the second half of the month.”

Added together that is 45,000 job losses in the month (not including government workers), which would be the largest monthly drop in jobs since March 2023.

A sustained increase in layoffs would be particularly concerning now because the hiring rate is low and it is harder than usual for unemployed workers to find jobs.

It is likely that The Fed will cut rates to compensate. Rate cuts around the corner!

ADP is reporting 42k jobs added in October (better than expected).

The breakdown. Education and health care, and trade, transportation, and utilities led the growth.

Mandami, as expected, was elected Mayor of New York City. He does have a nice smile.

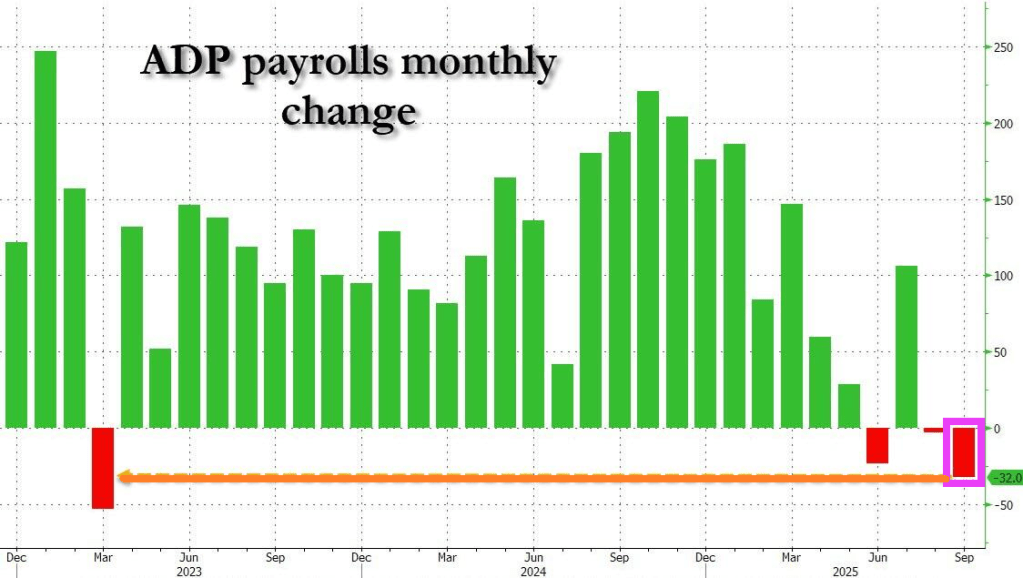

Due to the ongoing government shutdown – now in its third day – the BLS did not release the September jobs report this morning forcing traders and the Fed to “fly blind.” Or blinder than usual. And with ADP reporting earlier this week that some 32,000 jobs had been lost in September, putting markets and economists on edge and the US economy on the verge of a labor recession, the lack of data could not have come at a worse time. Luckily, private sector alternatives to the BLS do exist and, in many cases, are far more accurate and certainly less politicized.

The latest Revelio Labs number (+60.1k) is very notable as it suggests that the labor picture is nowhere near as bad as ADP indicated. In fact, as shown in the chart below, in September the Revelio Labs data set showed the best monthly increase in jobs in 2025!

The Federal Reserve will do what they want and will likely ignore the good report from Revelio. Besides, the Atlanta Fed GDPNow is at 3.8% for Q3.

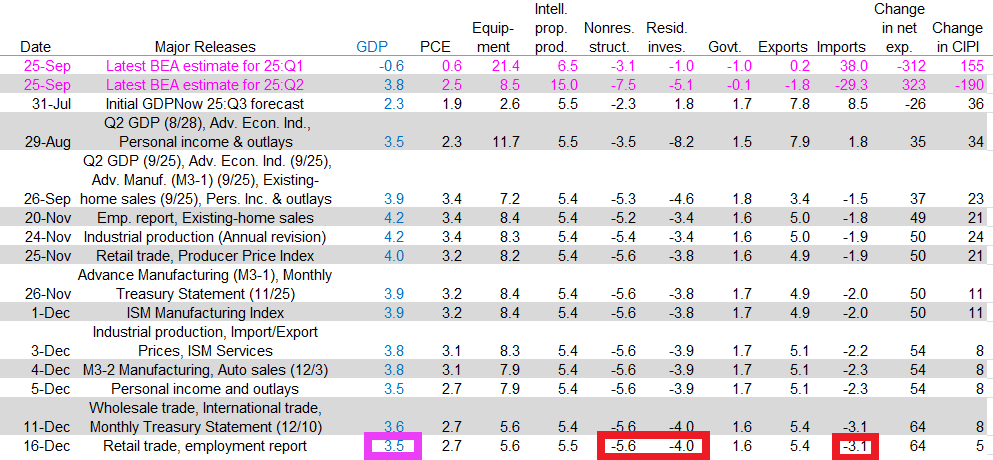

Here is the GDP breakdown.

This should get The Fed to cut rates! ADP reported that in September, the US private sector shed 32,000 jobs, the worst print since March 2023.

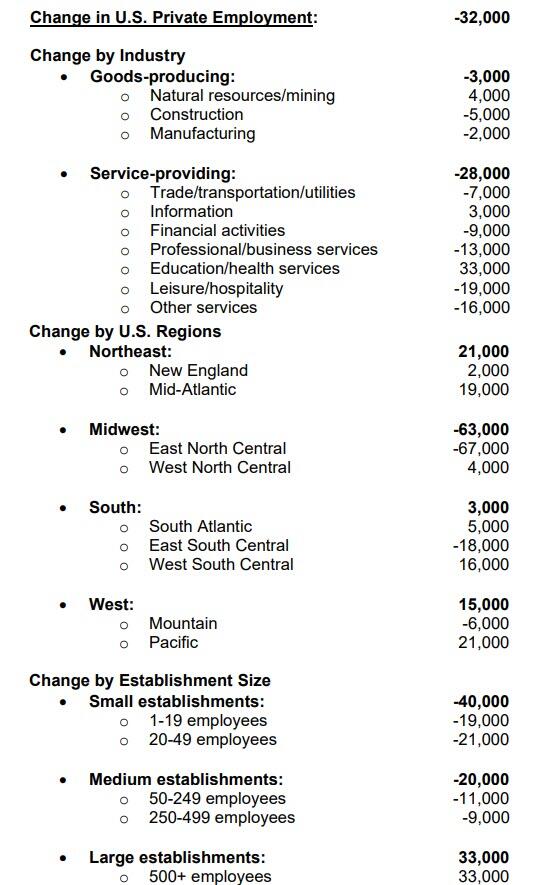

Here is the breakdown.

{kind=link}

You must be logged in to post a comment.