(Bloomberg) — The largest owner of U.S. rental houses isn’t seeing any let-up in demand, or in its ability to increase rents.

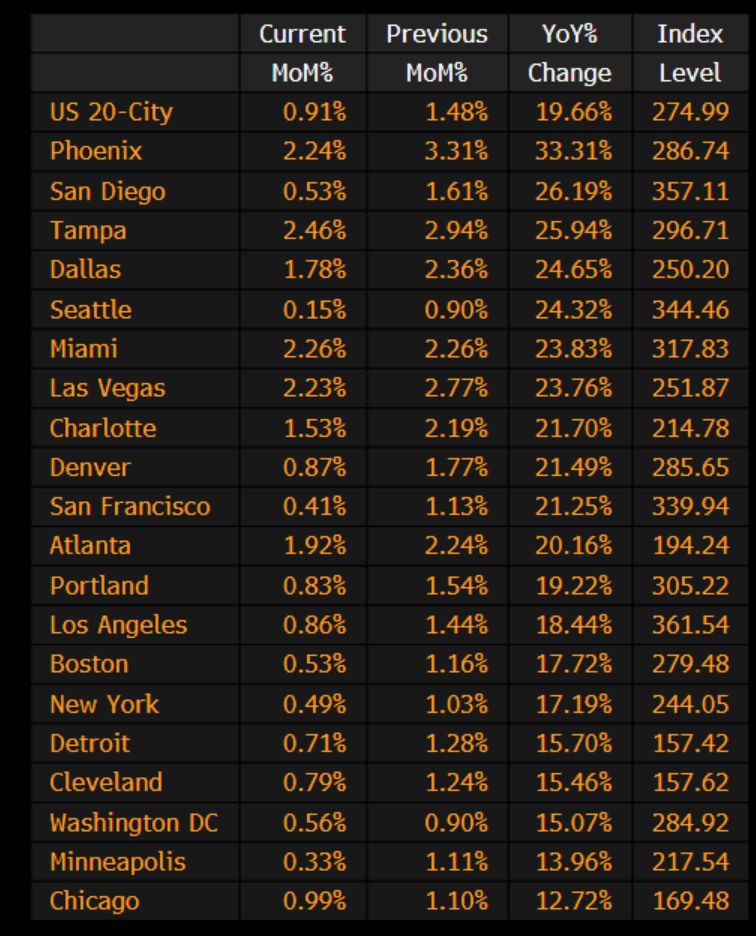

Invitation Homes Inc., which owns more than 80,000 single-family rentals, raised prices by nearly 11% in the third quarter, according to a statement. The company boosted rents by 8% on renewals and 18% when leasing homes to new tenants. Rates are rising fastest in the Southwest, where rents increased 30% on new leases in Las Vegas, and 29% in Phoenix.

“It’s a little bit crazy,” Chief Executive Officer Dallas Tanner said on a conference call with investors Thursday. “There just isn’t enough quality housing available right now.”

Rising rents have been a staple of the economy since early Covid lockdowns lifted in the middle of last year. Surging purchase prices have pushed homeownership out of reach for first-time buyers.

Invitation’s properties, which tend be more centrally located than those owned by other institutional landlords, have been especially popular. And tenants tended to stay put: The company had a record-low turnover rate in the quarter, which reduced the expenses associated with preparing a house for leasing.

Invitation’s shares rose slightly to $40.77 at 12:49 p.m. New York time after the company raised its expectations for full- year revenue and net operating income. The stock is up 37% for the year.

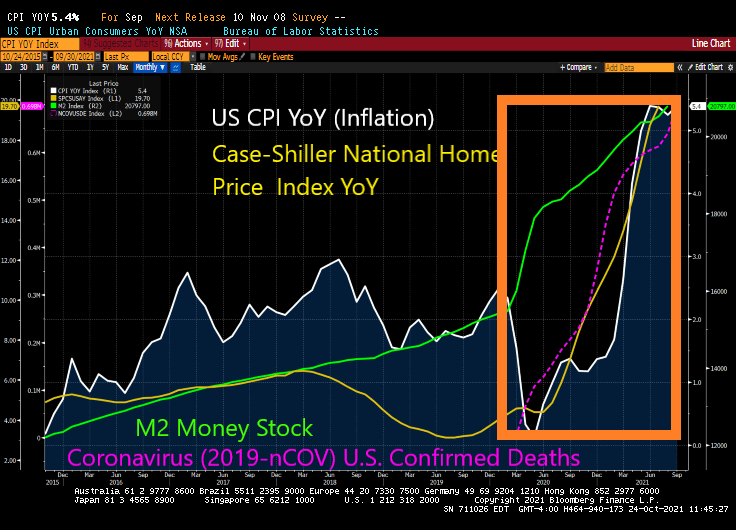

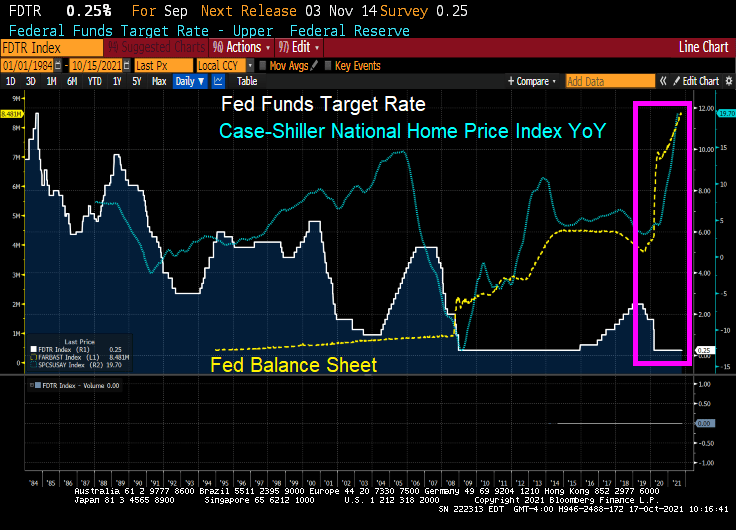

As Milton Friedman once said, “If you put the federal government in charge of the Sahara Desert, in 5 years there’d be a shortage of sand.” In this case, The Federal government and Federal Reserve were put in charge of the Covid epidemic and we have shortages of almost everything. Including housing.

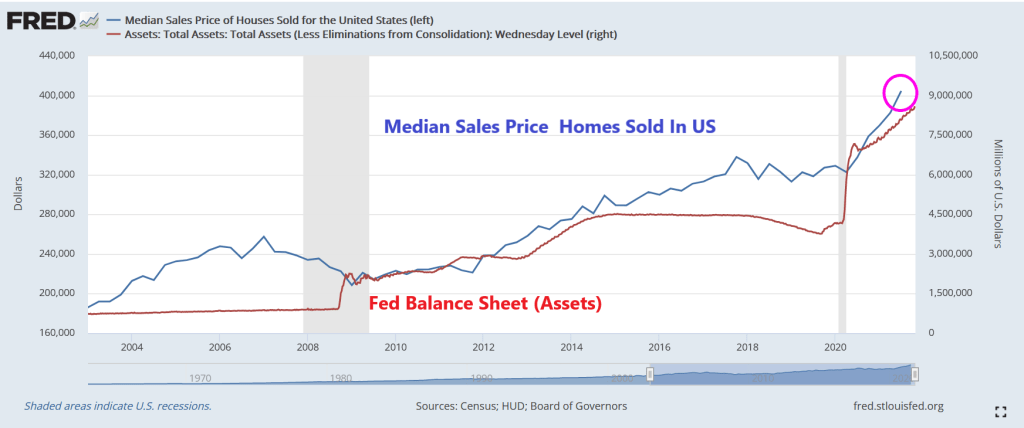

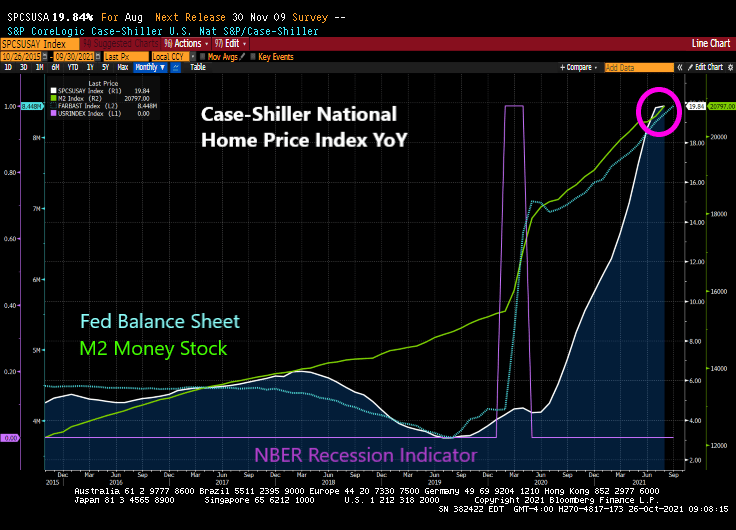

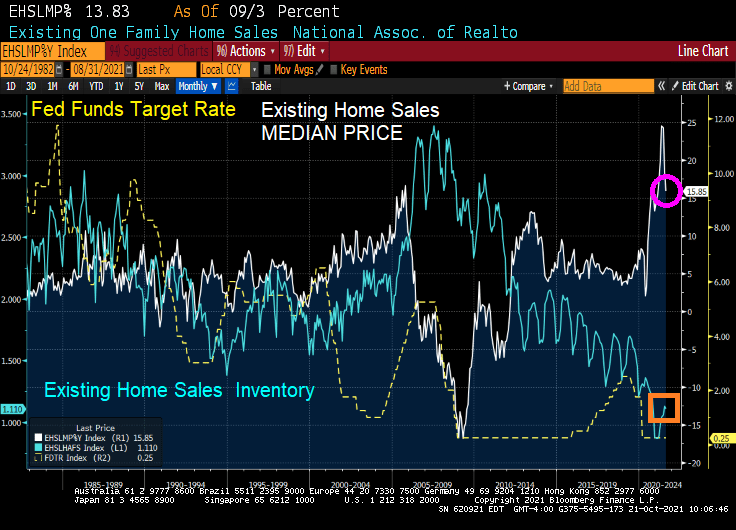

I don’t have Invitations rent growth chart, but here is Zillow’s YoY rent chart against The Fed’s balance sheet.

The good news? The 11% increase is almost half of the 20% YoY Case-Shiller National home price index.

Here is Treasury Secretary Janet Yellen making housing supply disappear.

You must be logged in to post a comment.