Somehow, Biden left this factoid out of his State of The Union (SOTU) address. In February, immigrants added 1,277 million jobs while native Americans lost -420,000 jobs according to the BLS. Or maybe Biden can change his campaign motto to “Make America Great Again … For Immigrants, NOT Natives.”

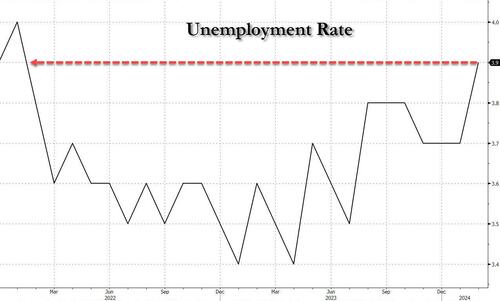

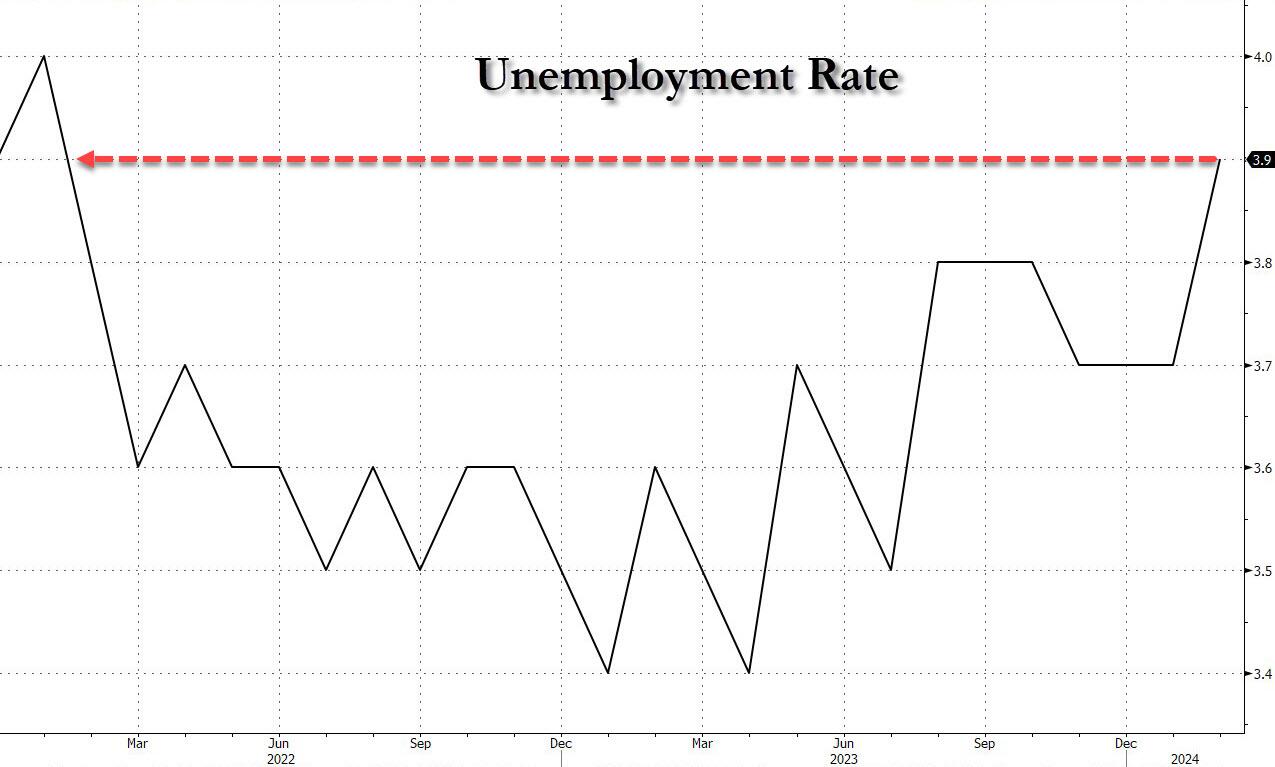

In February, the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%).

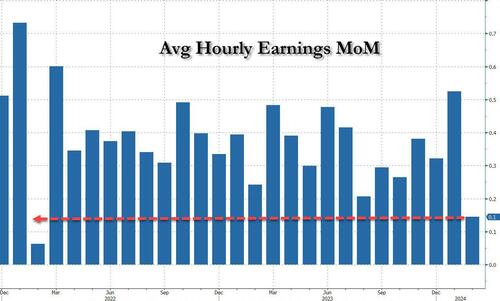

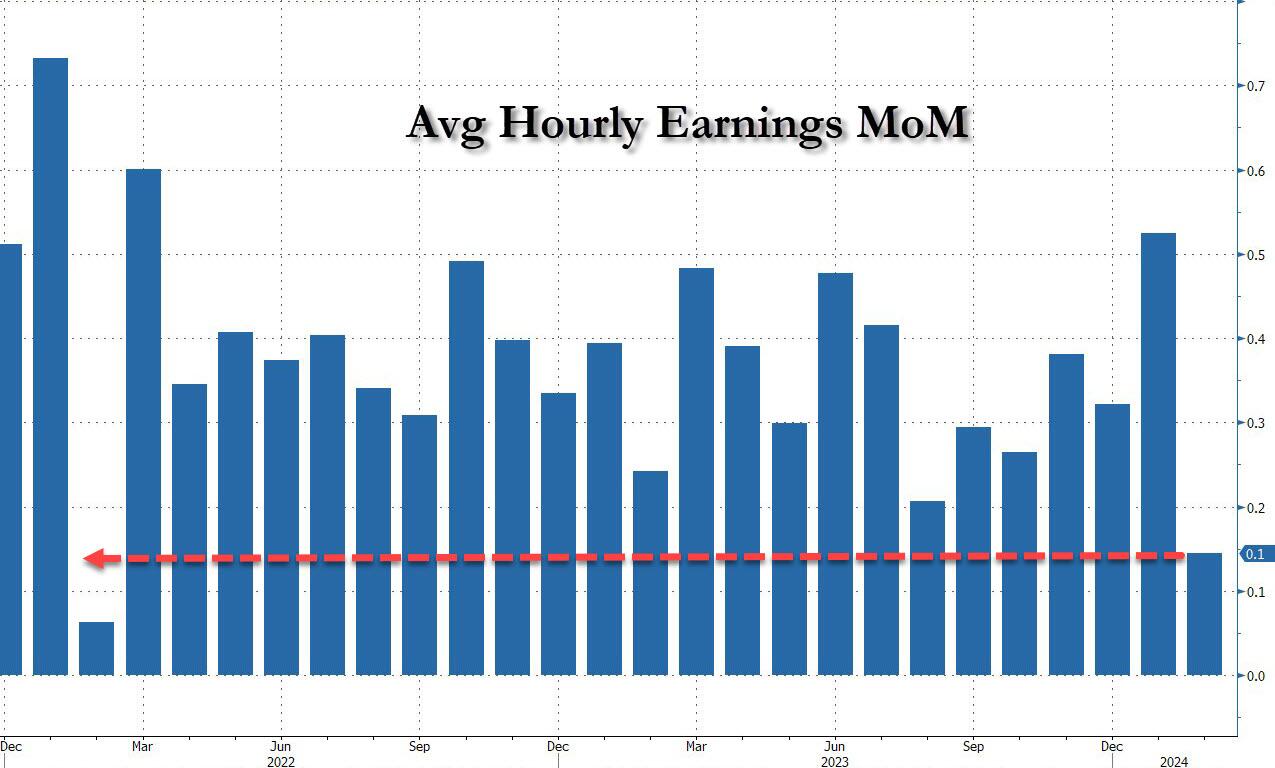

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years…

It is clear that the labor market is softening, but Biden/Mayorkas will continue to let millions of illegal immigrants pour across the border making the labor market even softer than before. But the top 1% are making out like bandits from the illegal immigration. Bandits benefitting bandits.

On a amusing or sad note, Biden campaign communications director Michael Tyler’s message to Americans who are worse off economically under Biden: “That’s precisely why we need another four years to finish the job.” OMG! What does “finish the job” mean?? I am afraid to ask.

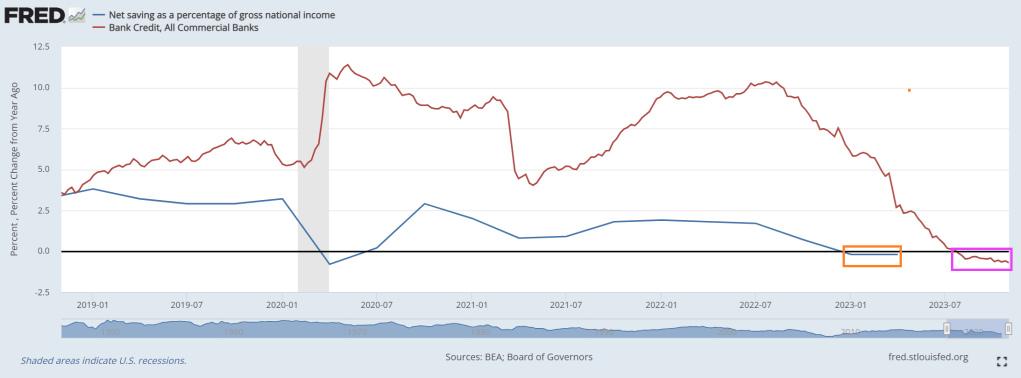

Where we currently sit is … bank credit growth is in the red (15th straight week of negative growth) and net savings as a percentage of gross national income has seen negative growth YoY for 2 consequtive quarters.

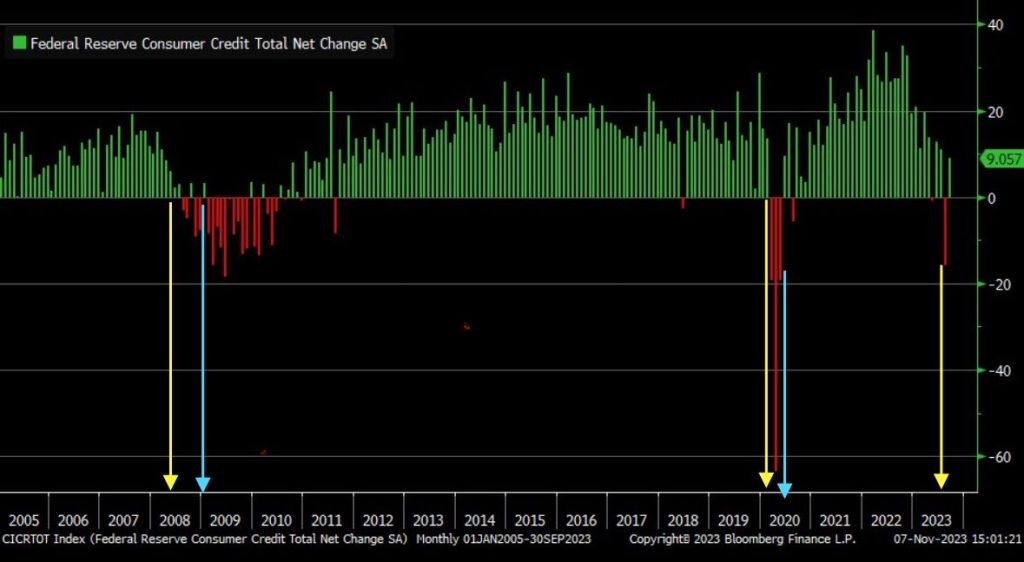

September marked the largest consumer credit drop since May 2020, signaling a significant recession warning.

And with Bidenflation (or Yellenflation) and The Fed’s counterattack, we are seeing bank stocks losing relative to the tech sector.

Proshares Bitcoin (BITO)’s assets have nearly doubled in the past 30 days.

Yes, the Three Stooges (Biden, Yellen, Powell) have put the US on a highway to hell!

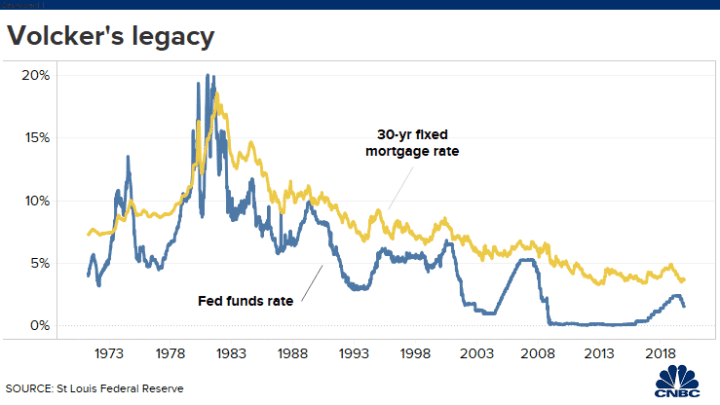

I had a wonderful time speaking at the Passive Investors Conference last night. One question I was asked was “Why doesn’t Powell (the current Fed Chair) pull “a Volcker” to cool inflation. She was referring to former Fed Chair Paul Volcker’s sudden raising of The Fed’s target rate which resulted in a cooling of inflation, but also an increase in the 30-year fixed mortgage rate to 16.63% in 1981.

Notice the trend in the Fed’s target rate and 30-year mortgage rate after Volcker’s rate shock. The trend in both has been downward as inflation was cooled.

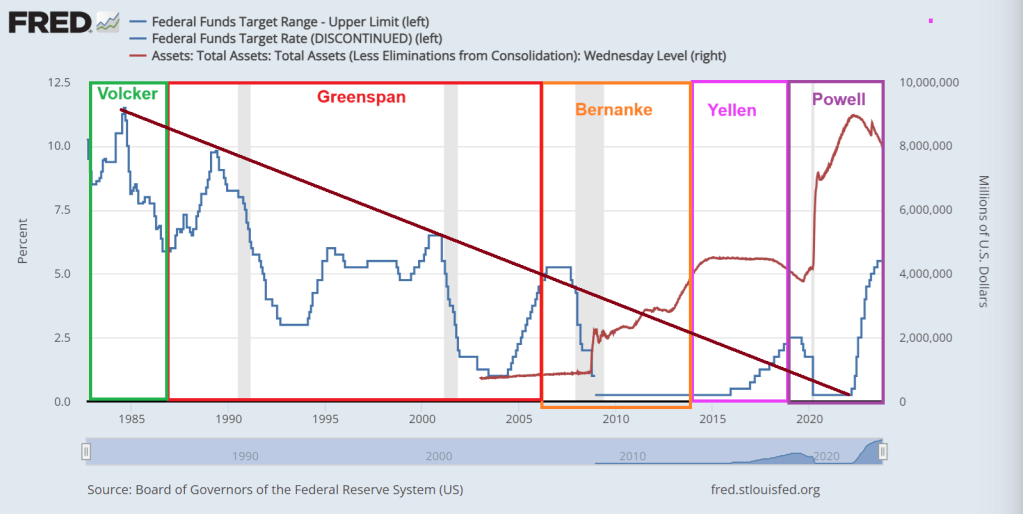

But, each Fed Chair ranged from hyperactive to hypoactive (meaning doing little). Volcker and Greenspan saw wild swings in The Fed’s target rate. Bernanke pretty much only lowered rates AND expanded the Quantitative Easing (QE) or asset purchases by The Fed. And nothing has been the same since.

Yellen, now Treasury Secretary, continued Bernanke’s practice of zero interest rate policies (ZIRP) and QE (asset purchases) … until Donald Trump was elected President. In fact, Yellen raise rates only once prior to Trump’s election as President. Then raises rates 8 consecutive times. This is why I call Yellen “TLTL Janet”. Too low for too long Janet.

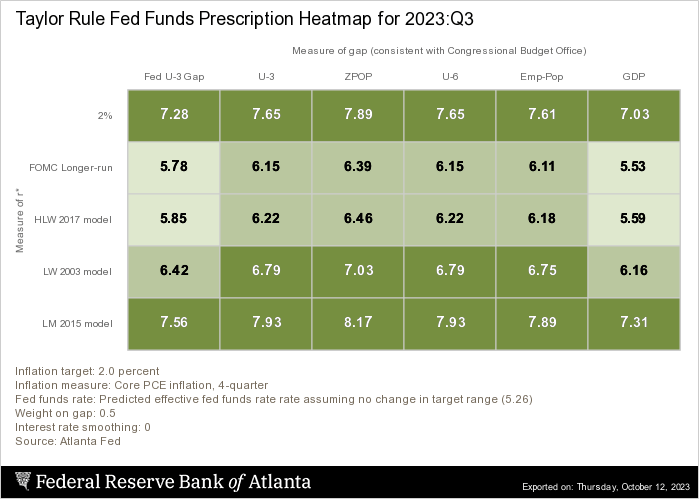

The she was replaced with DC insider Jerome Powell. Trump’s economy was strong (one explanation for Yellen trying to cool the economy with 8 consecutive rate hikes). But the Covid struck and Powell/Fed Open Market Committee overreacted, lowered the target rate back to 25 basis points and massively expanded the balance sheet. Powell also oversaw a rapid increase in the target rate, very Volckerish! But Powell stopped short of the rate suggested by The Taylor Rule of around 6.5% to 8.17%. The current target rate is 5.50%. So, Powell stopped far short of rates need to cool inflation.

But with Bidenomis came Bidenflation and a reversal of misfortunes for The Fed. They started rapidly raising rates … again.

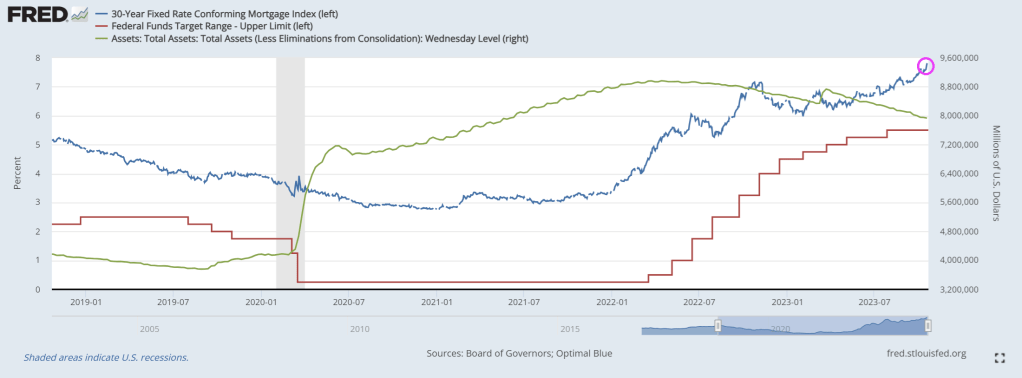

Mortgage rates continue to climb as The Fed stubbornly won’t reduce its balance sheet.

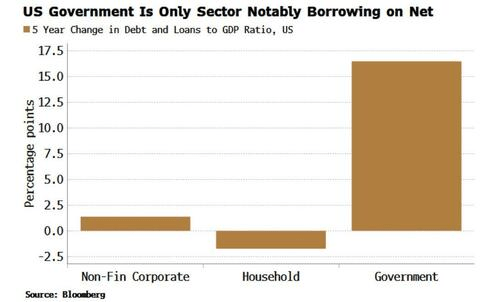

Biden/Congress have a broken fiscal model where spending is out of control. And The Fed can’t buy all the debt Biden/Yellen want to issue.

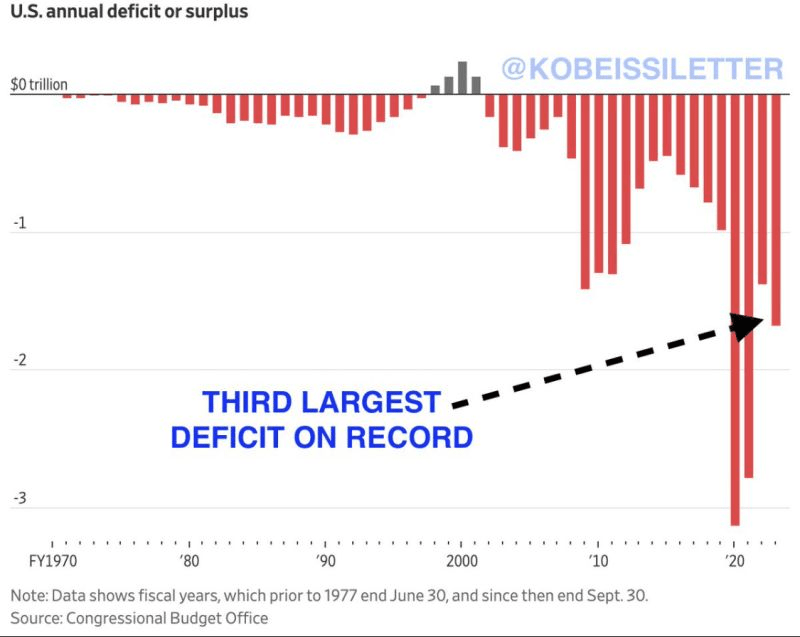

US deficits are the third highest on record.

We might as well have Taylor Swift as Fed Chair. And Travis Kelce as Treasury Secretary replacing TLTL Janet.

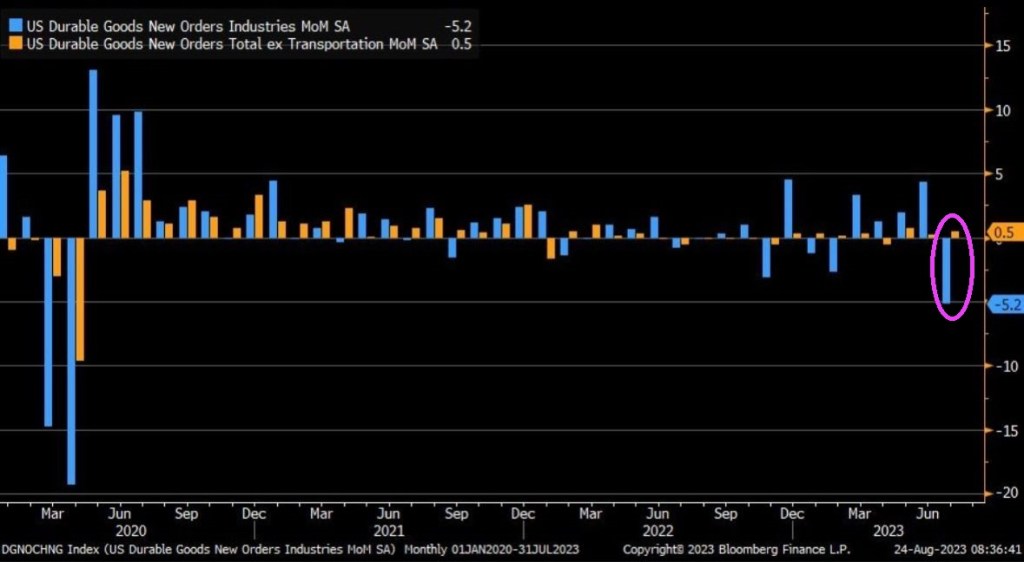

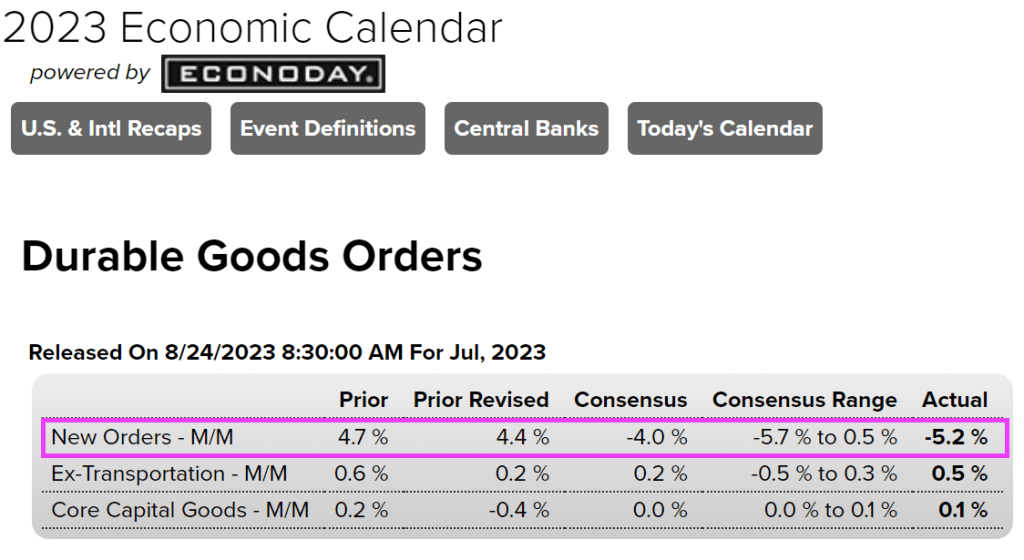

July durable goods [blue] new orders plummet, recording the worst month since C19 in April 2020. Durable goods fell on a MoM basis by -5.2%, versus -4% consensus estimate. Durable goods ex-transportation [orange] still rose on a MoM basis by +0.5%, perhaps highlighting the weakness in durable goods orders.

Ex-transportation, durable goods order rose slighlty in July by 0.5%.

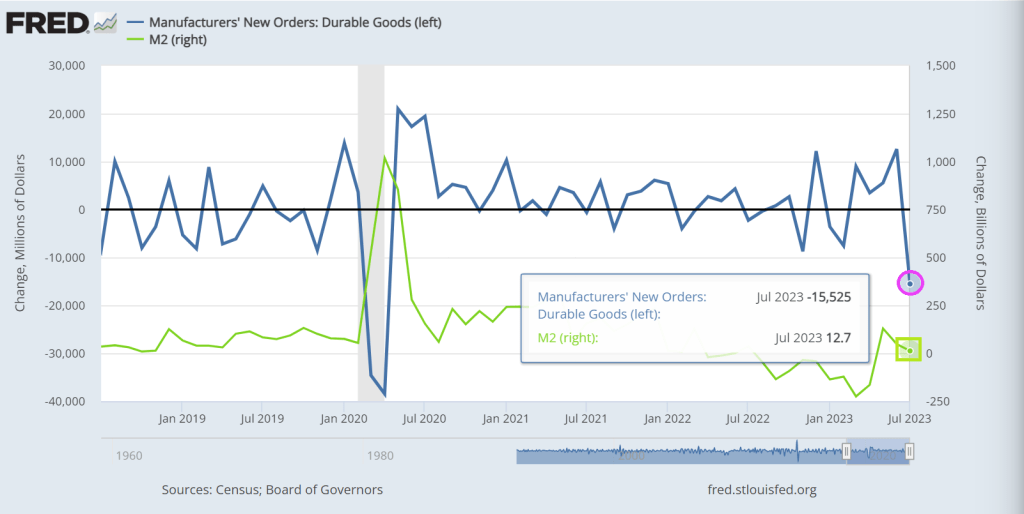

But according to The Fed of St Louis, durable goods new orders were down -15.525% from June to July (MoM) while M2 Money printing growth rose 12.7% MoM.

The themesong of Bidenomics is Randy Newman’s “Mr. President,” Have pity on the working man instead of paying off green energy BIG donors.

The massive green enegy spending spree by Biden and Congress (disguised as Inflation Reduction Act) is the keystone of Bidenomics. Or loadstone.

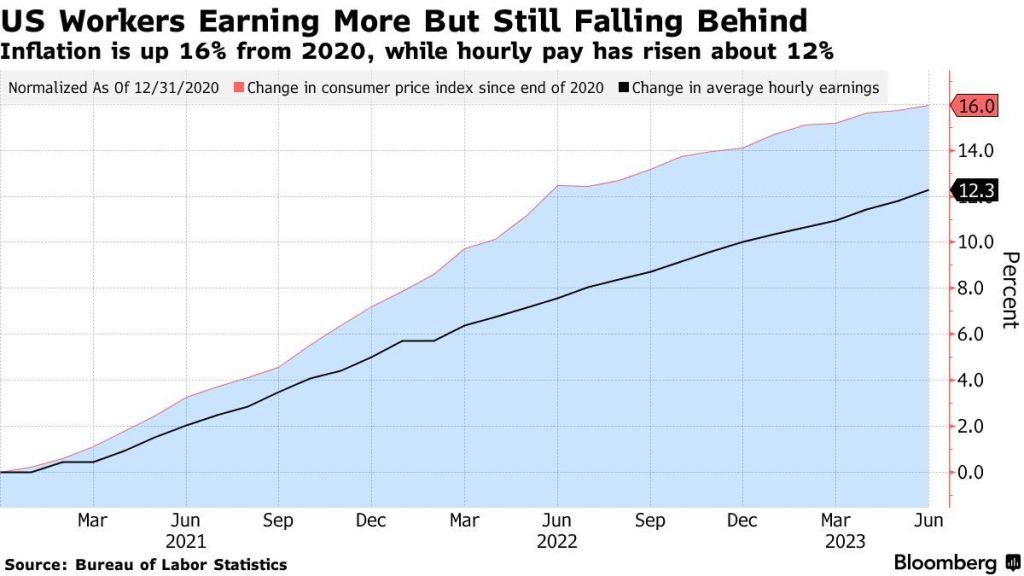

Since Biden became President, hourly pay has risen 12%! Unfortunately, Bidenomics spending spree (along with endless Fed monetary stimulus) has caused inflation to rise 16%. That is a net -4% decline in REAL earnings.

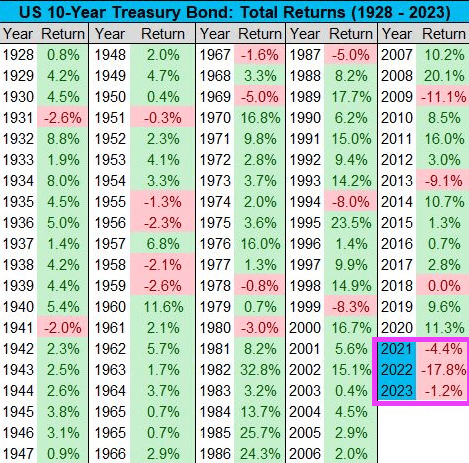

10-Year Treasury Yield is now 4.28%, the highest level since October 2007. From a total return perspective, the 10-Year Treasury Bond is now down 1% in 2023, on pace for its third consecutive negative year. With data going back to 1928, that’s never happened before. BUT we’ve never had Joe Biden as President before 2021.

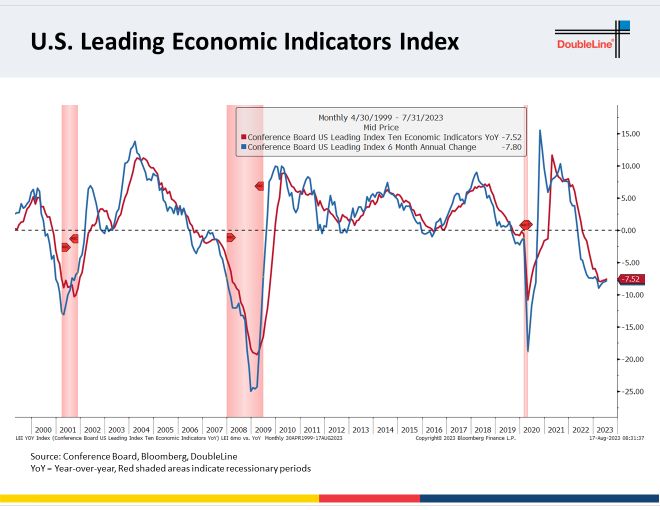

And then we have the Conference Board’s Leading Economic Idicators, sucking wind.

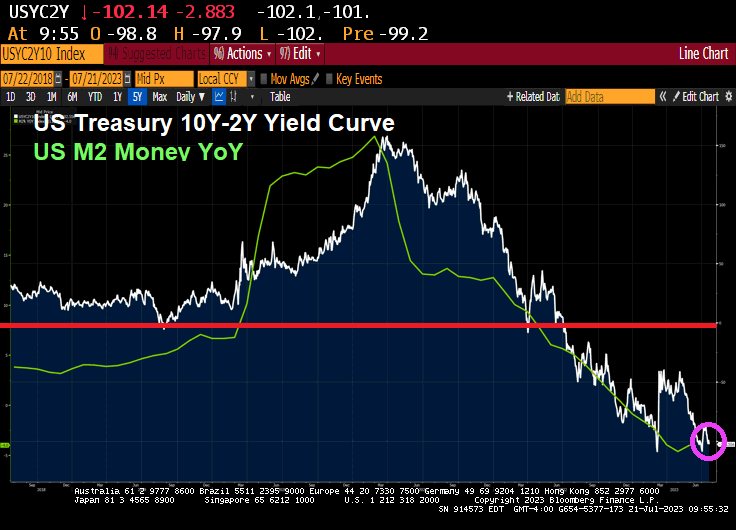

I have never seen anything like this. The US Treasury 10Y-2Y yield curve is deep in inversion and has had a negative slope for 265 straight days. Bidenomics is born under a bad sign!

On the commodities front, heating oil is up almost 2% this morning and nickel (an important element in Biden’s green energy mandates) is up 1.78%.

On the crypto front, Bitcoin is up 0.47% and Dogecoin is up 5.58%.

You can always buy Kamala’s Own Word Salad Dressing!

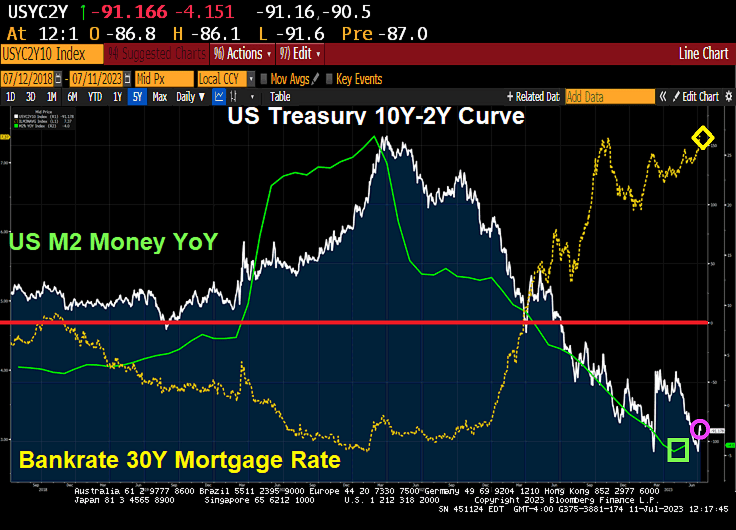

I am anxiously waiting for the US inflation report tomorrow, so I am just looking at the US Treasury yield curve, mortgage rates and cryptos today.

The US Treasury 10Y-2Y yield curve stumbled (just like Biden and Bidenomics) to -91.166 basis points as the turnaround in M2 Money growth has stalled. Bankrate’s 30Y mortgage rate is up to 7.37%, that is UP 156% under Bidenomics.

Bitcoin is down today. At least Solana is up.

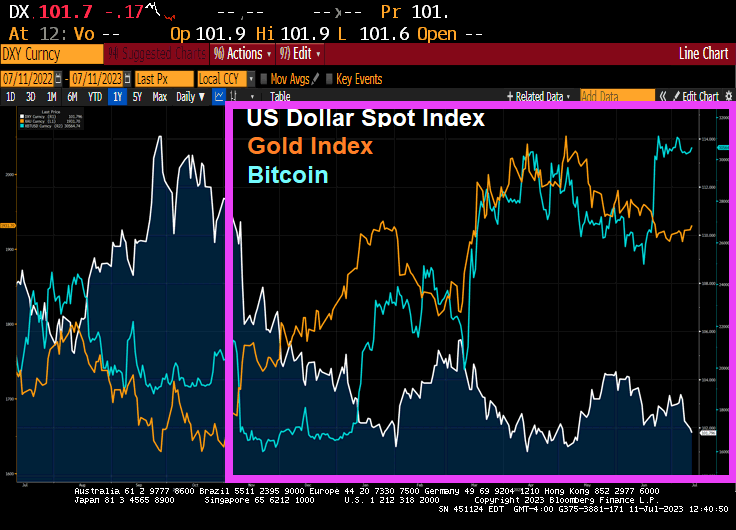

Since November 3, 2022, the US Dollar Index is DOWN -9.68%, Gold is UP 18.55% and Bitcoin (Elizabeth Warren’s latest obsession) is UP 51.11%.

I could have used 3 shades of Joe, but 50 shades of Joe sounds better!

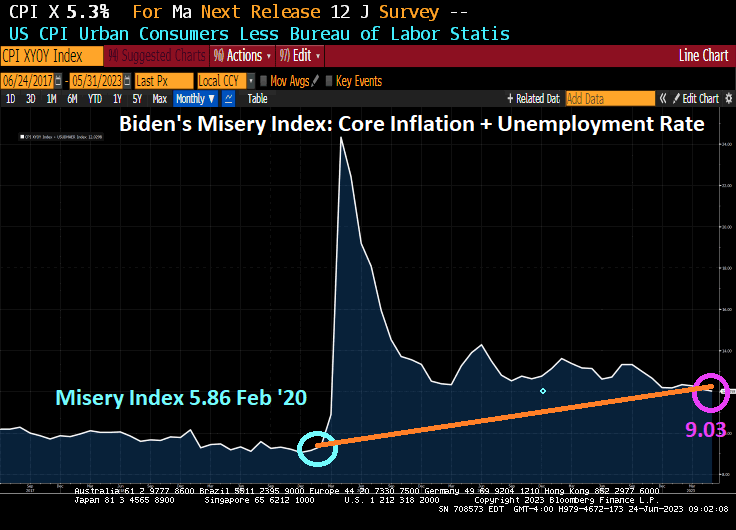

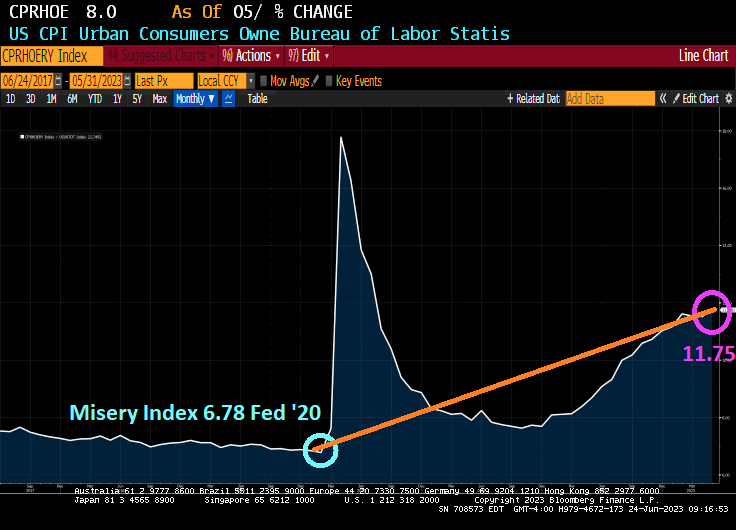

But the fact remains that Americans are far more miserable under Biden than they were under Trump before the Chinese Wuhan Covid virus was unleashed. 9.03 today (Core CPI YoY + U-3 Unemployment) than it was in February 2020 under Trump (5.86). While not twice as bad, inflation is continues to cause serious problems for America’s middle class and low-wage workers.

Speaking of the middle class and low wage workers, let’s look at the Renter’s Misery index (CPI Owner’s equivalent rent YoY + Unemployment rate). It was 6.78% in February 2020 under Trump and before Covid struck and is now 11.75% under Inflation Joe.

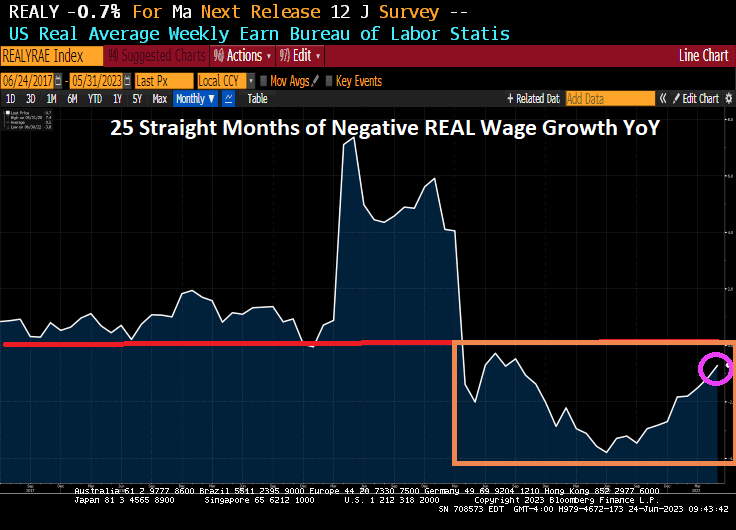

Speaking of misery, how 25 straight months of negative REAL wage growth? Real weekly wage growth went negative in April 2021, just a few months after Biden was installed as President.

Now, there was winners under Biden. Green energy donors, the big banks, big pharma, big tech, but media … essentially any big donors from big entities got massive payoffs. The middle class and low-wage workers? As Jerry Reid once sang, “They got the coal mine and we got the shaft.”

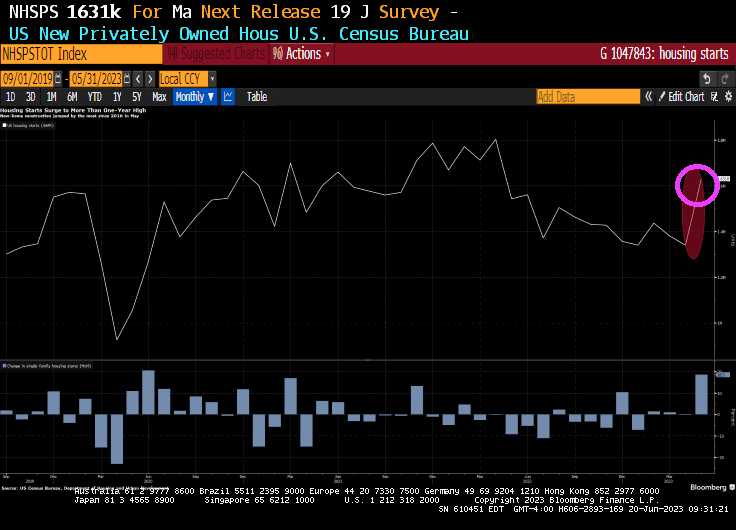

Well, not really unexpected since the housing sentiment index for home builders was above 50 yesterday. But with The Fed pausing rate hikes, housing starts are soaring!

US housing starts unexpectedly surged in May by the most since 2016 and applications to build increased, suggesting residential construction is on track to help fuel economic growth.

Beginning home construction jumped 21.7% to a 1.63 million annualized rate, the fastest pace in more than a year, according to government data released Tuesday. The pace exceeded all projections in a Bloomberg survey of economists. Single-family homebuilding rose 18.5% to an 11-month high.

Applications to build, a proxy for future construction, climbed 5.2% to an annualized rate of 1.49 million units. Permits for one-family dwellings increased.

Metric

Actual

Est.

Housing starts (SAAR)

1.63 mln

1.4 mln

One-family home starts (SAAR)

997,000

na

Building permits (SAAR)

1.49 mln

1.425 mln

One-family home permits (SAAR)

897,000

na

The figures corroborate Federal Reserve Chair Jerome Powell’s comments last week that the housing market has shown signs of stabilizing. Homebuilders, which are responding to limited inventory in the resale market, have grown more upbeat as demand firms, materials costs retreat and supply-chain pressures ease.

The housing starts data will feed into economists’ estimates of home construction’s impact on second-quarter gross domestic product. Prior to the report, the Atlanta Fed’s GDPNow forecast had residential investment subtracting about 0.1 percentage point from gross domestic product. Homebuilding last contributed to growth in the first quarter of 2021.

At the same time, elevated mortgage rates are crimping affordability, suggesting limited momentum in housing demand.

The increase in starts from a month earlier was the biggest since October 2016 and reflected gains in three of four US regions. Starts of apartment buildings and other multifamily projects jumped more than 27%.

The number of homes completed increased to a 1.52 million annualized rate. The level of one-family properties under construction were little changed at 695,000.

Existing-home sales data for May will be released on Thursday, while a report on new-home purchases is due next week.

Now only has The Fed paused, but the most recent Fed Dots Plot reveals that Fed open market committee (FOMC) members see The Fed slashing rates over the coming years. Just in time for creepy, demented Grandpa Joe to be reelected as President. In other words, the return of ZORP (zero outrageous rate policy).

Maybe The Fed should adopt the Coca Cola slogan “The Pause That Refreshes!”

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

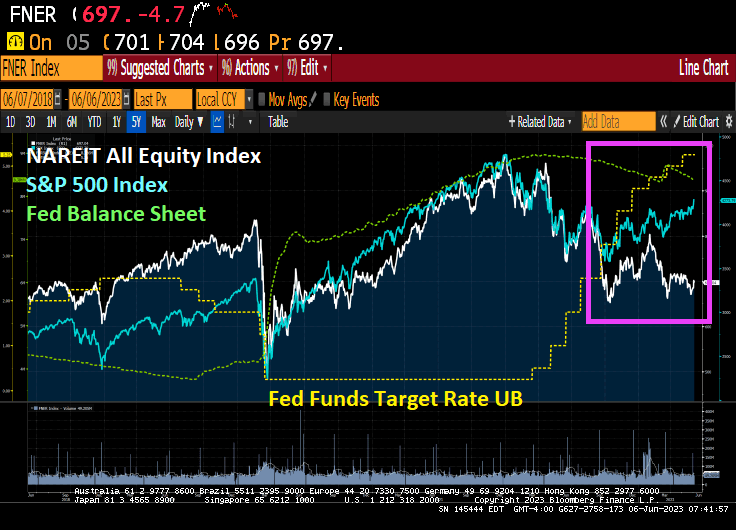

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.