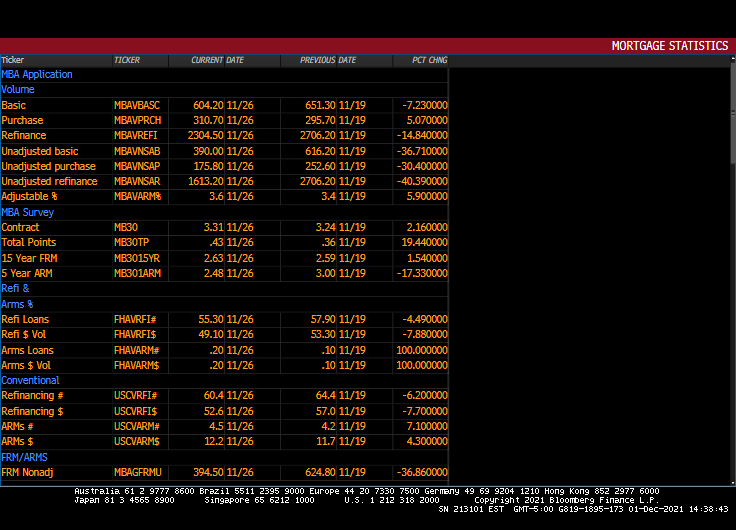

Its that time of year for mortgage purchases applications! Purchase applications usually decline during December and start to rise after the beginning of the year.

Mortgage purchase applications (white line) dropped -30.4% from the previous week, not usual for December. But what is surprising is the drop in REFINANCING applications: down -40.3% from the previous week.

30-year mortgage rates rose 2.16% from the previous week.

But between Omicron (or as the French say, “Oh! Macron!”) and The Federal Reserve, there is a good chance that mortgage rates will fall this week putting a quick end to refi application plunge.

Purchase applications? Nope, it is that time of the season when purchase applications drop like a rock.

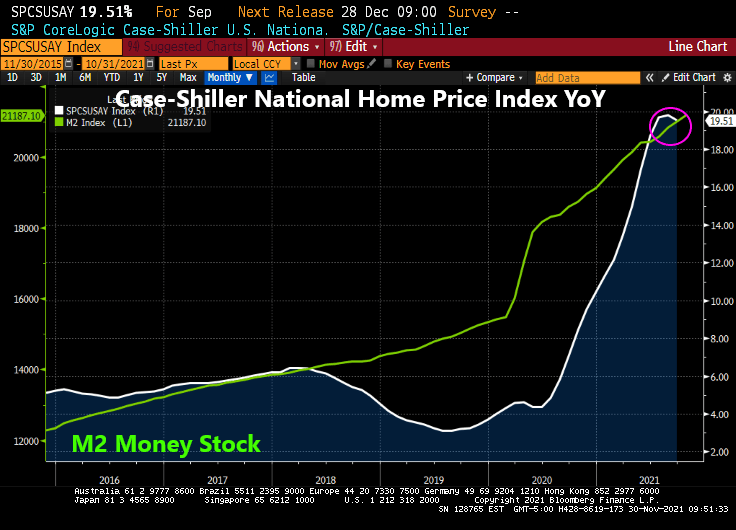

Once again, low available inventory of houses for sale coupled with outlandish Fed stimulus has resulted in a housing crisis where home price growth (+19.51%) exceeds hourly wage growth (+5.76%) by almost 4x.

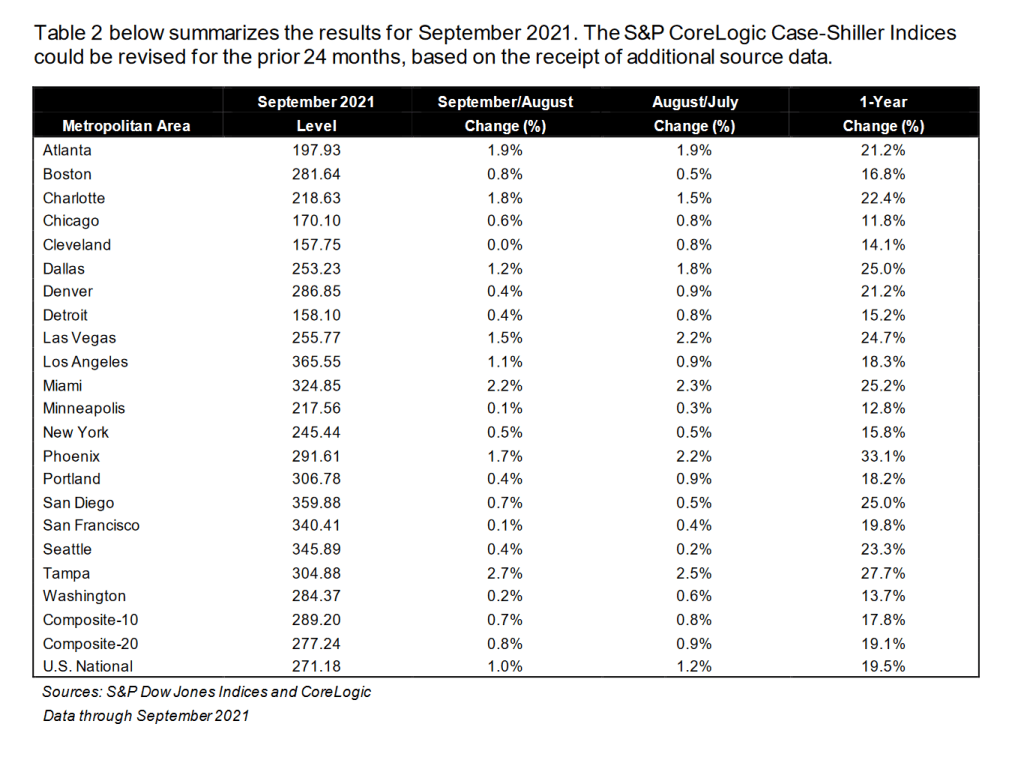

Where are all the home prices above 10% YoY? Every one of the 20 metro areas covered by Case-Shiller. Phoenix AZ leads at +33.1%. Chicago IL is the “slowest” at 11.8%.

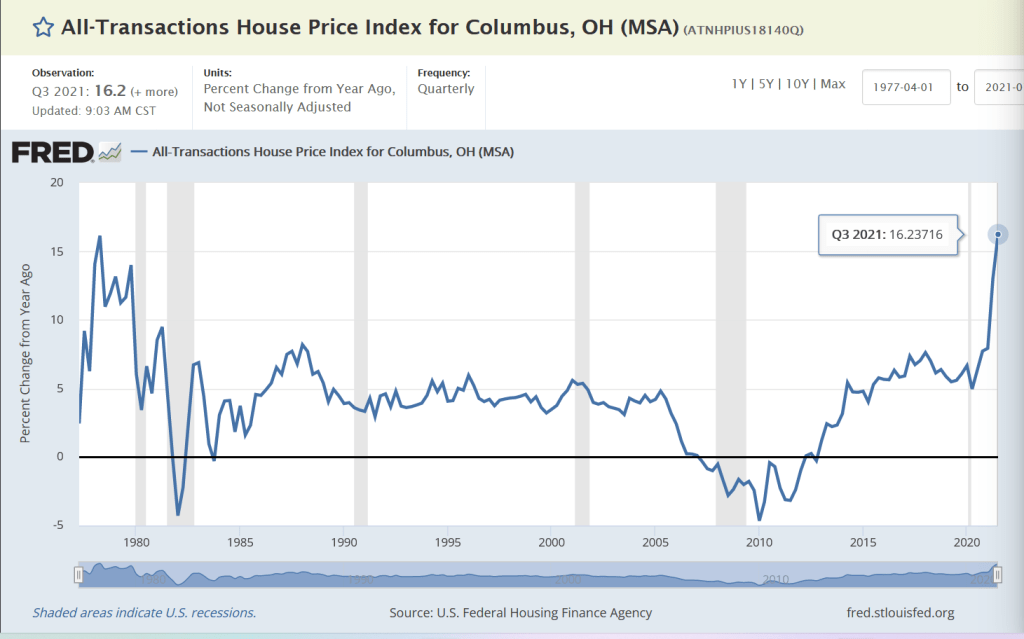

Although Columbus OH is the growth hub of the state, Case-Shiller only reports Cleveland. So here is Columbus’s all-transactions home price growth for Q3: +16.2% YoY placing Columbus at the top of the midwest metro areas of Detroit, Chicago, Minneapolis and Cleveland.

With the latest Omicron Variation (sounds like a Star Trek TV show episode), I will bet that The Fed will stay a little longer and keep rates low, leading to home price growth (with limited available inventory) to continue to grow at double digit speeds.

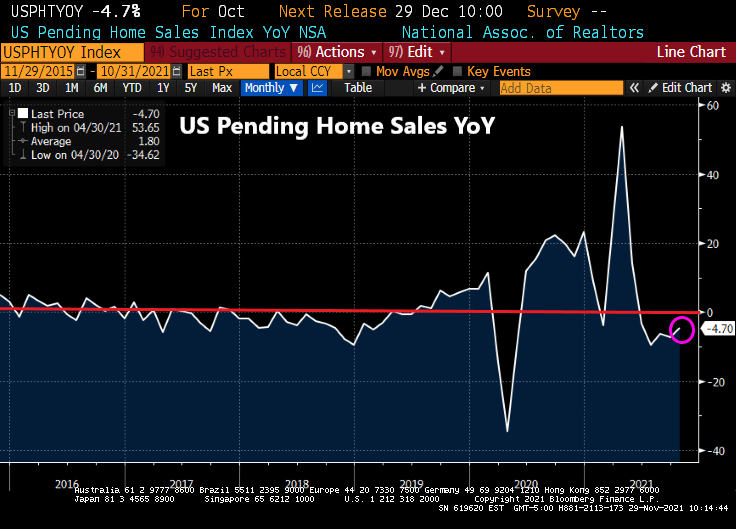

A forward-looking gauge of U.S. home purchases rebounded in October to a 10-month high, signaling steady housing demand despite growing affordability concerns among many prospective buyers.

The National Association of Realtors’ index of pending home sales increased 7.5% from a month earlier to 125.2, according to data released Monday. The median estimate in a Bloomberg survey of economists called for a 1% advance.

But it is the fifth straight month of year-over-year declines.

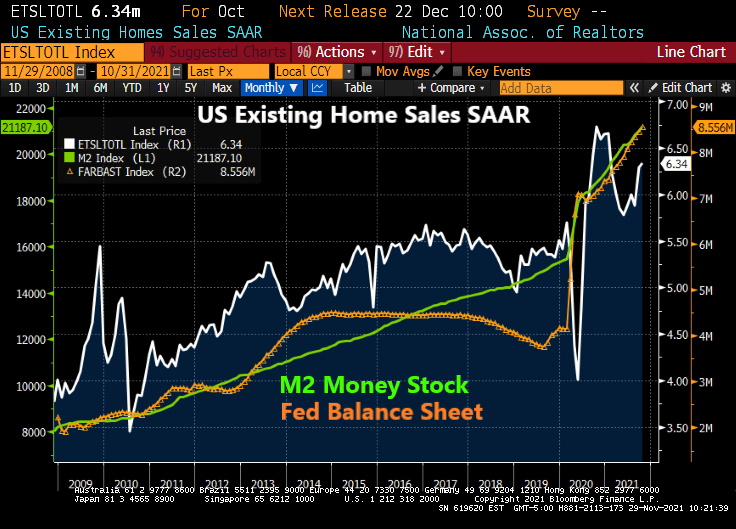

Low mortgage rates and solid job growth have supported housing demand this year as pandemic-weary buyers seek more spacious accommodations. Existing home sales are on track to exceed 6 million in 2021, which would be the strongest in 15 years, Lawrence Yun, NAR’s chief economist, said.

Yes, humongous stimulus from The Federal Reserve will help push existing home sales to exceed 6 million in 2021.

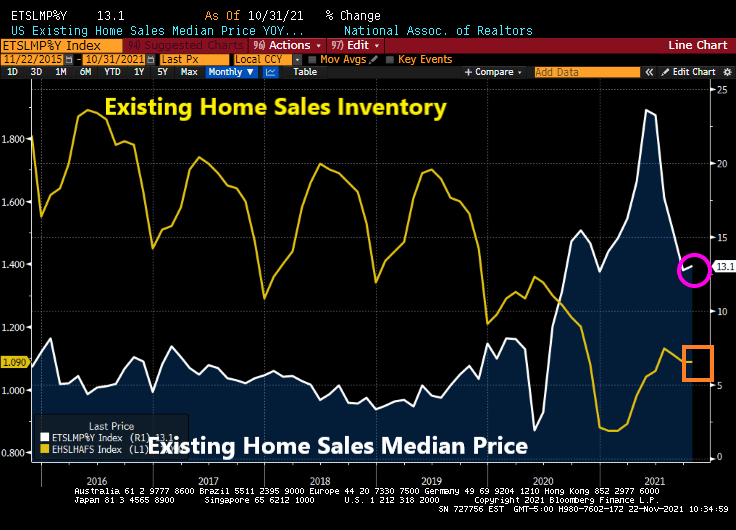

Still, competition over a scant number of listings — particularly on the lower, more affordable end of the resale market — has pushed prices out of reach for many prospective buyers. Builders have struggled to fill the void as supply-chain delays and labor shortages upend construction schedules, exacerbating the inventory crunch.

Yes, inventory of homes available for sale is almost 1/3rd of the homes available in 2010.

Ten years after ... and we have progressively less inventory available.

I have written numerous times about nothing has been the same since the housing bubble burst and ensuing financial crisis of 2008. The crisis led to bank bailouts (TARP) and banking legislation (Dodd-Frank) giving The Federal Reserve even more power. And then the COVID lockdowns led to even MORE power for The Fed. And a horrid decline in money velocity (the ability of printing money to increase economic growth … or GDP).

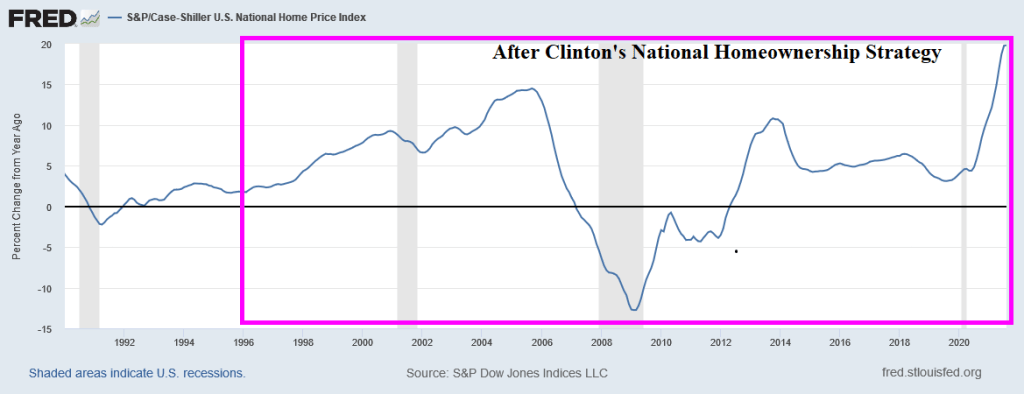

But let’s take one step backwards. One the causes of the housing bubble that burst was President Clinton’s infamous National Homeownership Strategy that encouraged “partners” with the Federal government to soften underwriting standards for mortgage lending, particularly for minority households. The intent was to increase the homeownership rate in the US and it worked! Too well. Along with increasing the homeownership rate came rising home prices, culminating with home price growth reaching 14.5% YoY in September 2005. Only to start slowing to a crash.

Of course, the housing bubble was associated with no/low documentation and subprime mortgage lending. But the relaxing of underwriting standards by the National Homeownership Strategy helped fuel the no/low doc and subprime lending crisis. But weakening underwriting standards to increase homeownership rates is a dangerous strategy.

Note the surge in M1 Money Velocity (GDP/M1) starting in 1994. M1 Velocity grew until Q4 2007, then crashed along with home prices. The second and more sudden crash in M1 Velocity occurred with the COVID outbreak in March 2020 and the ensuing economic lockdowns and the intervention of The Federal Reserve in terms of money printing. M1 Money surged 173% from October 2008 to February 2020 and then another 369% from March 2020 to today. THAT is a Fed Storm Surge!!

M2, the broader definition of money, has not grown as rapidly as M1, but it still grew at an alarming rate. Atlanta Fed President Raphael Bostic blamed inflation on COVID but not The Fed’s insane money printing or government lockdowns. C’mon man!

Finally, the banking crisis (and TARP bailouts) along with COVID have made consumer purchasing power of King Dollar even worse.

Be careful of government strategies to make housing more “affordable” because they seem to make housing more expensive and can help crash the financial system.

Renters in the US are getting clobbered by inflation.

The US Zillow Rent Index All Homes YoY + CPI YoY is one measure of renter misery.

The classic misery index (CPI YoY + U-3 unemployment rate) is 10.80%.

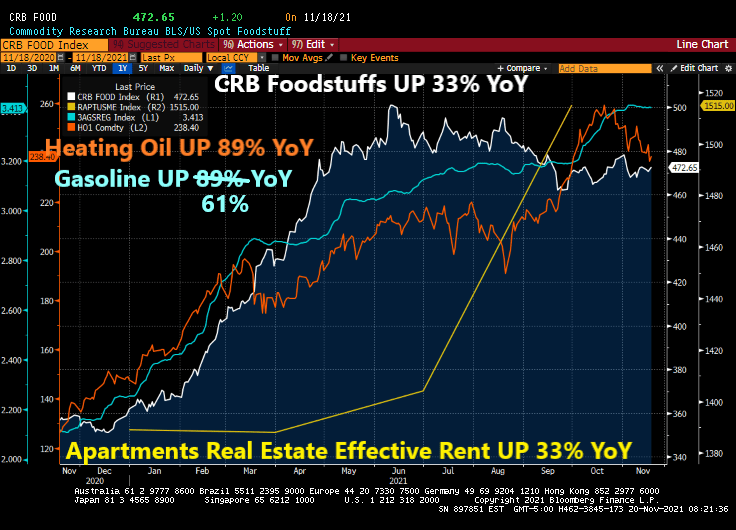

Then there is inflation in food prices, gasoline, heating oil, natural gas, etc.

While Biden is releasing the Strategic Petroleum Reserves (SPR) in order to mitigate the problem that he created by terminating the energy pipelines and oil/natural gas drilling permits in the name of “Going Green!” But on the announcement of tapping the SPR, crude oil futures actually rose.

President Biden has decided to nominate Fed Chair Jerome Powell for a second term in an effort not to rock the boat. Lael Brainard is nominated for Deputy Chair.

To quote Gomer Pyle USMC, “Surprise, surprise, surprise!”

The humongous spending bill awaiting Joe Manchin to sign off on it will cost almost double what the CBO said it would. Why? Because spending programs in Washington DC never get cancelled, they only grow.

“We estimate the House Build Back Better Act includes roughly $2.4 trillion of spending and tax cuts along with roughly $2.2 trillion of offsets.However, the bill relies on a number of sunsets and expirations to keep the official cost down. If the plan’s temporary policies were made permanent, we find the cost would increase by as much as $2.5 trillion.As a result, the gross cost of the bill would more than double from $2.4 trillion to $4.9 trillion.

The Build Back Better Act relies on a number of arbitrary sunsets and expirations to lower the official cost of the bill. These include extending the American Rescue Plan’s Child Tax Credit (CTC) increase and Earned Income Tax Credit (EITC) expansion for a year, setting universal pre-K and child care subsidies to expire after six years, making the Affordable Care Act (ACA) expansions available through 2025, delaying the requirement that businesses amortize research and experimentation (R&E) costs until 2026, and setting several other provisions – from targeted tax credits to school lunch programs – to expire prematurely.

Excluding changes to the state and local tax (SALT) deduction, we estimate the Build Back Better Act would cost $2.1 trillion as written. We estimate making all of these temporary policies permanent would cost roughly $2.2 trillion, more than doubling the gross cost of the bill to $4.3 trillion through 2031.”

When asked about the Center for a Responsible Budget saying the bill could be twice as expensive, Manchin replies “it’s concerning. Sure. It’s concerning.”

Surprise, surprise, surprise! And it is certainly more expensive than the estimate Biden gave: $0.

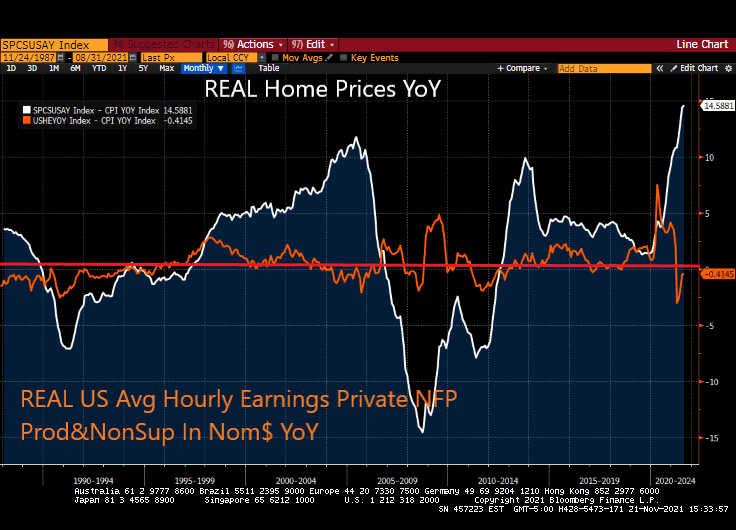

Welcome to The Fed’s Gilded Age … for housing! The gilded age refers to the thin-veneer of gold covering up problems in the late 1800s.

Today’s gilded age is largely fueled by The Federal Reserve’s uber-easy monetary policies combined with absurd Federal government policies. The result? Thanks to inflation, REAL home prices are growing at 14.6% YoY while REAL hourly earnings are declining (-0.41% YoY).

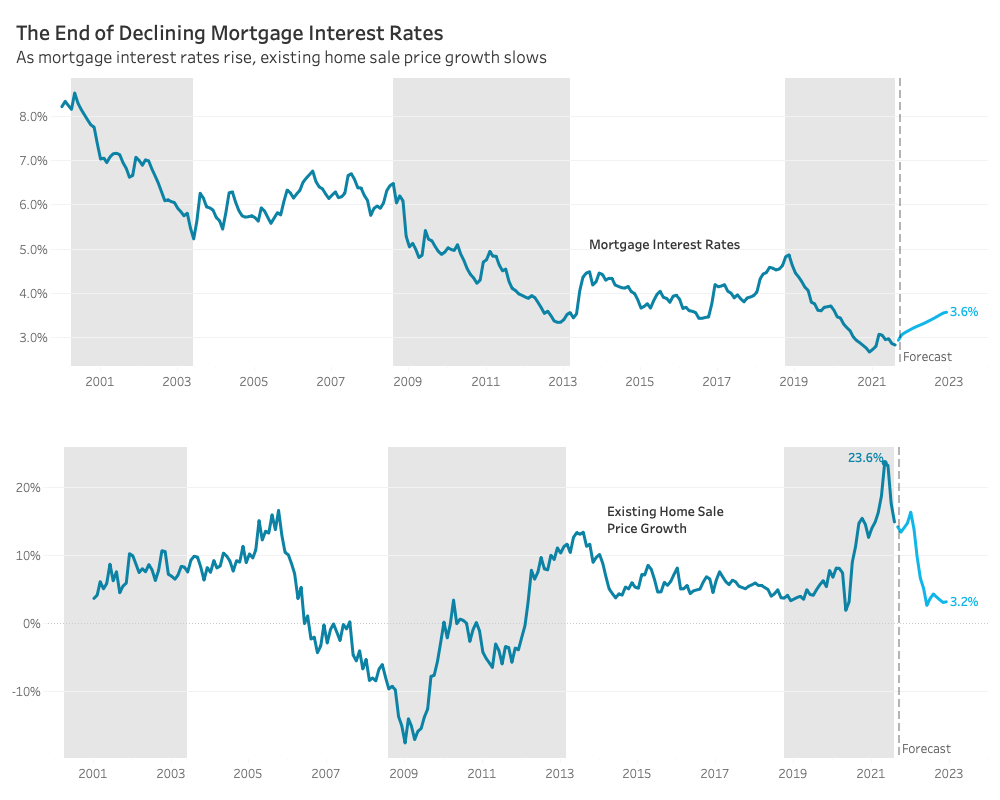

Redfin predicts a more balanced housing market in 2022. Part of their rationale is that they predict mortgage rates will rise to 3.6%. This growth in the mortgage rate is predicted to slow home price growth to 3.2% from double digit growth currently.

While this scenario is plausible, it will require a change in direction of the 10-year Treasury yield which has been declining since 1981. 5.39% YoY inflation may encourage The Fed to raise rates.

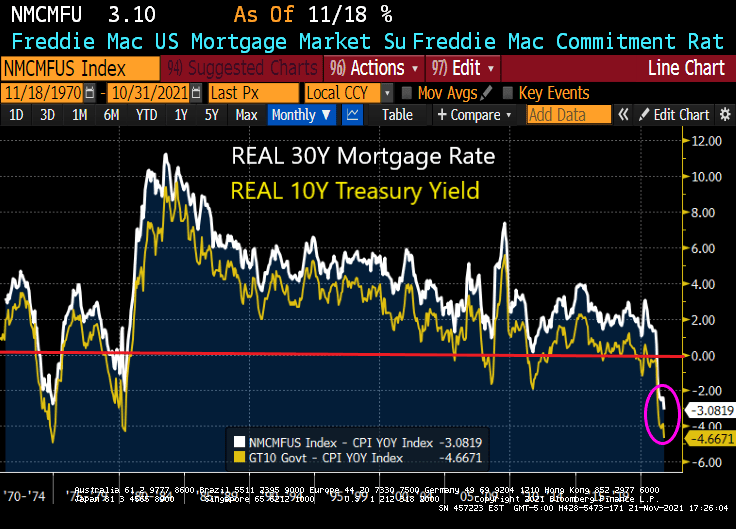

Today’s REAL 30-year mortgage rate is -3.08% while the REAL 10-year Treasury yield is -4.67%. It will require a reduction in inflation AND an increase in the nominal rate to get to 3.6%.

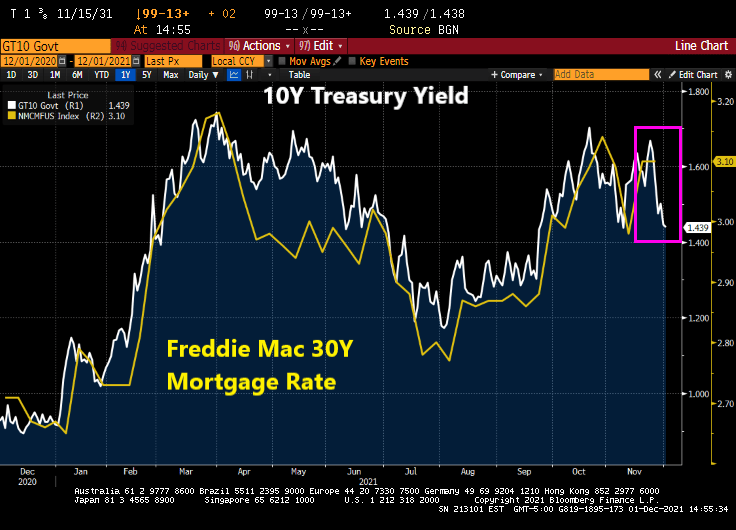

With the Freddie Mac 30-year survey rate at 3.10, will a 50 basis point increase in mortgage rates send the market crashing? Not likely.

After all, the US economy is under the thumb of The Federal Reserve.

The Marty Stuart/Travis Tritt song “This One’s Gonna Hurt You (For A Long, Long Time)” seems appropriate for the plight of the middle and lower income classes in the face of high inflation. How do you spell the combination of President Biden’s policies and The Fed’s inaction on inflation? T-R-O-U-B-L-E … for the middle and lower income classes.

Over the past year, since the election of Joe Biden, the household consumption bundle (food, rent, heating, gasoline) have all risen dramatically in terms of prices. Food is up 33%, heating oil is up 89%, regular gasoline is up 61%, and effective apartment rents are up 33%.

Meanwhile, the 1% are sitting high on a mountain top obvious to the pain caused by The Federal Reserve and Biden Administration. Here is the growth in wealth by the 1% since the housing bubble burst and financial crisis compared with the bottom 50%.

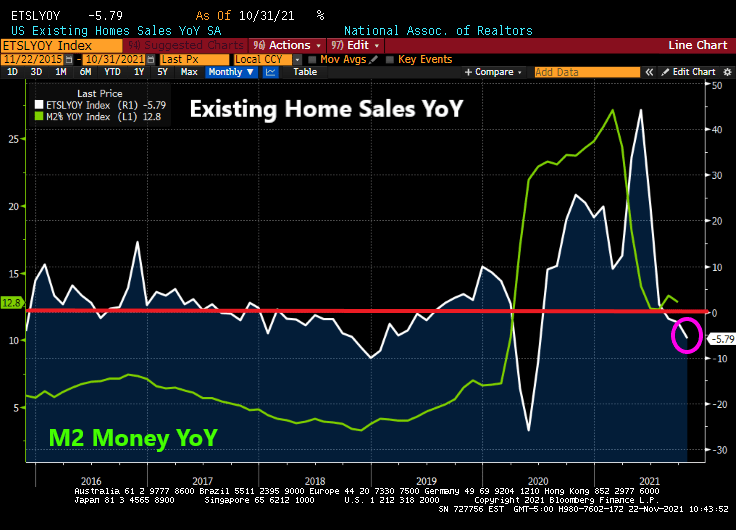

A problem facing renters is the rapid growth of home prices particularly since the COVID epidemic. At least M2 Money has “slowed” to 12.80% YoY while home prices are raging at almost 20% YoY. But hopefully home price growth will slow with declining M2 growth.

Compendium of Fed Chair Jerome Powell and President Biden on vacation.

US housing starts for October were less than expected. A 1.5% increase MoM was expected, but housing starts actually fell -0.7% MoM.

5+ unit (multifamily) starts were up 6.82% MoM. 1-unit single family detached units were down -3.89% MoM. Permits to build were up 4% MoM.

On a YoY basis, 1-unit start declined -10.6% as M2 Money growth continues to fall.

And 1-unit housing starts have fallen with the rapid decline in home buying sentiment.

1-unit starts have slowed to pre-COVID levels, thanks in part to The Federal Reserve’s money printing bonanza which may never end.

As housing sentiment crashes (due to rapid home price growth), we are seeing the demand for multi-family housing rise. 5+ unit (multifamily) starts were up 6.82% MoM in October.

You must be logged in to post a comment.