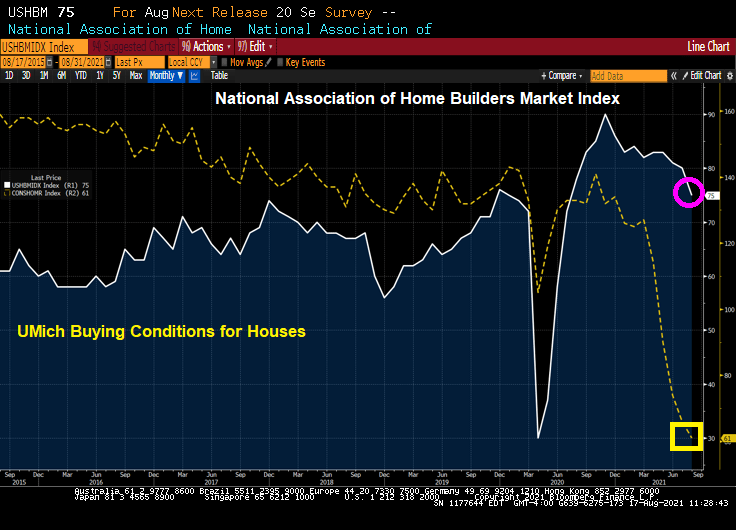

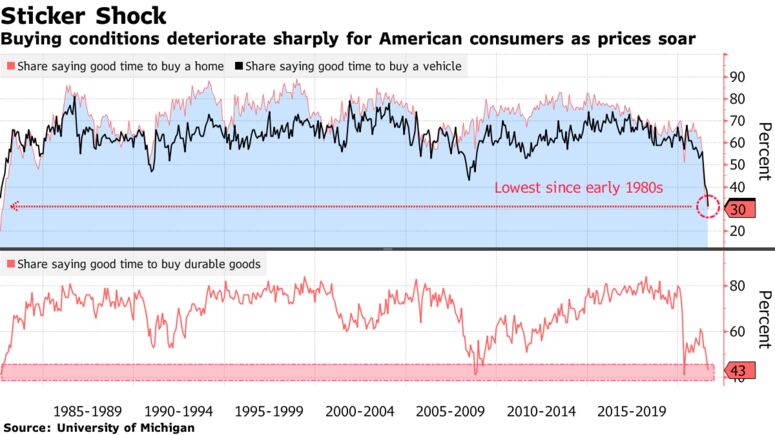

Of course, then we have the University of Michigan conditions for buying a home crashing as well.

Rising home prices and rising construction material costs? Yikes.

Of course, the NAHB had this to say:

“Our expectation is that production bottlenecks should ease over the coming months and the market should return to more normal conditions,” NAHB Chief Economist Robert Dietz said in a statement.

Perhaps, but The Fed needs to slow down its money printing as well.

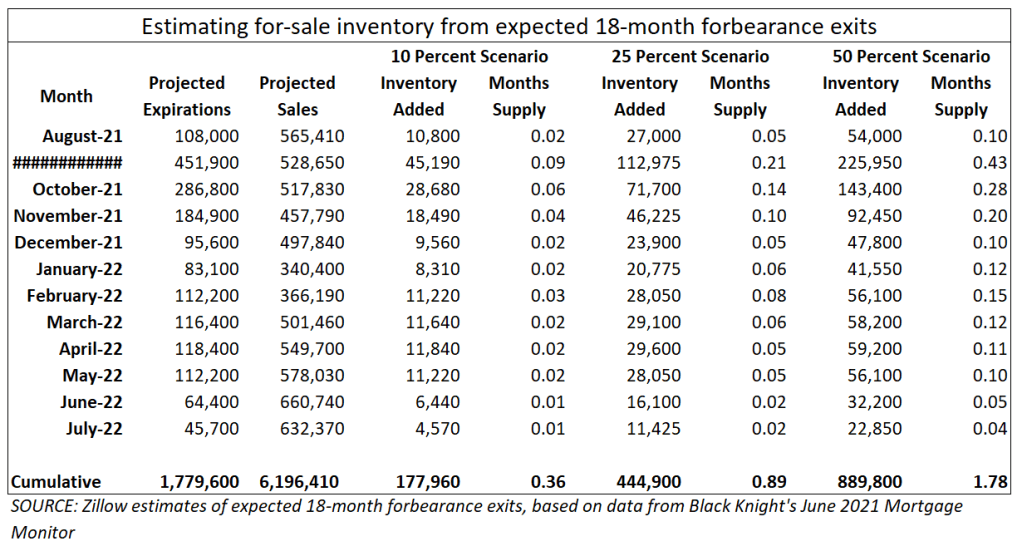

There will be more housing inventory hitting the market soon. As home prices are up and most are no longer in negative equity situations, some will decide to sell into this hot market. Obviously not paying your mortgage for 12, 14, 16, or even 18 months is a nice bonus that party is coming to an end.

Zillow’s research found that most are not going to bring their mortgage current. Assume someone took a forbearance and their monthly mortgage cost was $2,000 per month, some may be behind by up to $36,000 when the forbearance period ends. Okay, well what if you can’t make it current? You can defer the payments to the end of the mortgage but you still owe that and many got used to not even paying the regular monthly payment. So a sizable portion will be selling

Could this be the end of the 16.6% YoY growth rate in home prices? Or will Congress and/or The Biden Administration extend the forbearance? Or will The Fed expand their balance sheet even further??

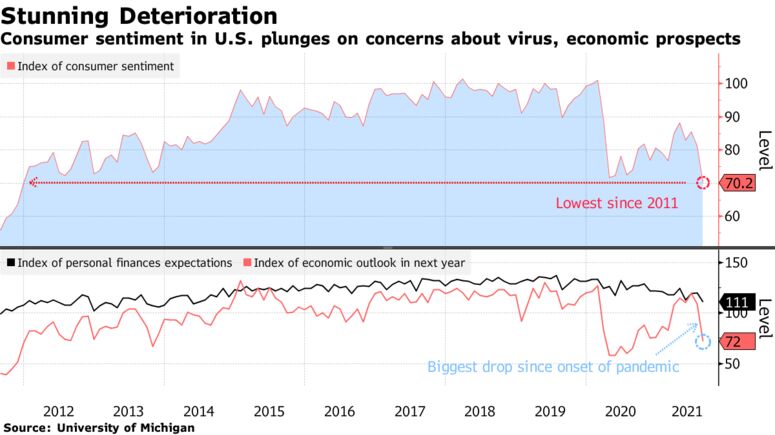

U.S. consumer sentiment fell in early August to the lowest level in nearly a decade as Americans grew more concerned about the economy’s prospects, inflation and the recent surge in coronavirus cases.

The University of Michigan’s preliminary sentiment index fell by 11 points to 70.2, the lowest since December 2011, data released Friday showed. The figure fell well short of all estimates in a Bloomberg survey of economists.

The slump in confidence risks a more pronounced slowing in economic growth in coming months should consumers rein in spending. The recent deterioration in sentiment highlights how rising prices and concerns about the delta variant’s potential impact on the economy are weighing on Americans.

“Consumers have correctly reasoned that the economy’s performance will be diminished over the next several months, but the extraordinary surge in negative economic assessments also reflects an emotional response, mainly from dashed hopes that the pandemic would soon end,” Richard Curtin, director of the survey, said in the report.

The expectations gauge plummeted almost 14 points to 65.2, the lowest since October 2013. A measure of consumers’ outlook for the economy over the coming year soured, falling the most since the onset of the pandemic in March 2020.

Only 36% of respondents expect a decline in the jobless rate, down from 52% the prior month, despite record job openings. Consumers also became decidedly downbeat about their income prospects. The gauge of expected personal finances fell to a seven-year low.

Rising prices are having a clear impact on Americans’ budgets, particularly among those with lower or fixed incomes. Nearly a third of those aged 65 or older complained that inflation had lowered their living standards, as did about a fourth of those with incomes in the bottom third or with a high school education or less.

The Michigan report showed buying conditions deteriorated to the lowest since April of last year.

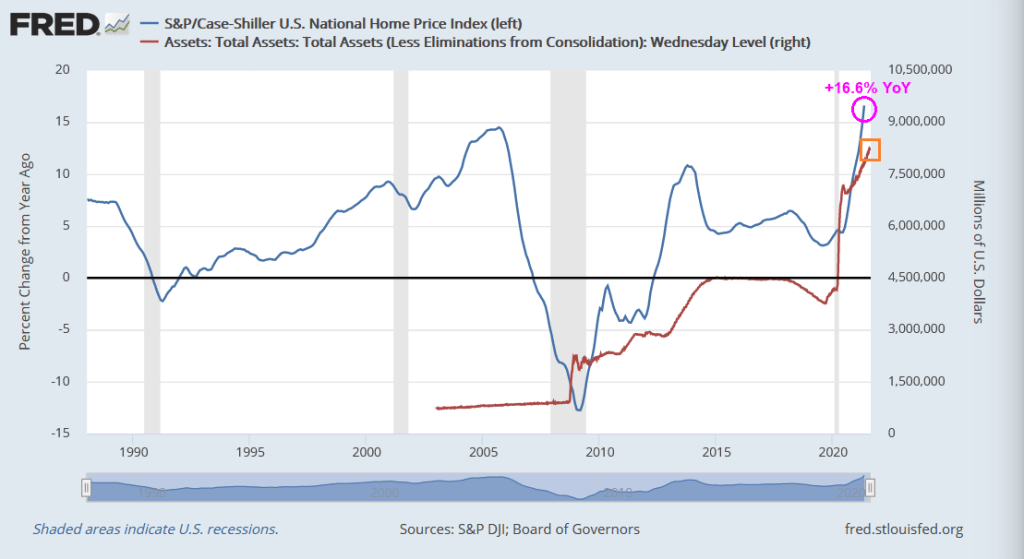

Yes, only 30% of respondents felt that it was a good time to buy a home. Particularly since home prices are rising at a 16.6% YoY pace, faster even than the peak of the infamous home price bubble of 2005. But this time, The Fed is blowing the bubble, not easy mortgage credit like in 2005.

Apparently, Treasury Secretary Janet Yellen does not inspire confidence in consumers.

Rents in the New York City metropolitan statistical area — which also encompasses northern New Jersey and Long Island — dropped in the 12 months through July for the first time since 1958, according to monthly data on consumer prices published Wednesday by the Labor Department. Before that, the series indicates rents in the region hadn’t fallen on a year-over-year basis since 1934. The figures underscore the historic nature of the pandemic and its impact on the U.S. economy.

On the other hand, New York City home prices are growing at a +15.3% YoY pace.

Apparently, in 1958 Americans liked Ike, but didn’t like living in New York City.

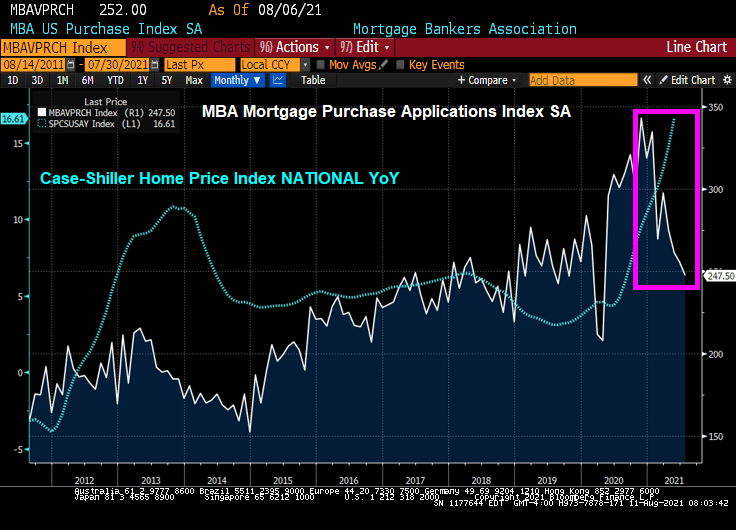

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 6, 2021.

The Refinance Index increased 3 percent from the previous week and was 8 percent lower than the same week one year ago. But recent declines in mortgage rates have produced a mini-refi wave (pink box).

The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 18 percent lower than the same week one year ago. But rapidly rising home prices have cooled mortgage purchase applications since the beginning of 2021.

Here is the data from the MBA showing a rise in mortgage applications from the previous week of 2.79%.

You must be logged in to post a comment.