August data for the US housing market has been ‘mixed’ to say the least with a surge in new home sales (thanks to a massive rise in incentives from homebuilders) and a small decline (near multi-year lows), leaving this morning’s pending home sales data as the tie-breaker (with expectations of an ‘unch’ shift MoM).

It appears the drop in mortgage rates is driving some purchase activity as pending home sales soared 4.0% MoM in August – the most since March – dragging sales up 0.5% YoY.

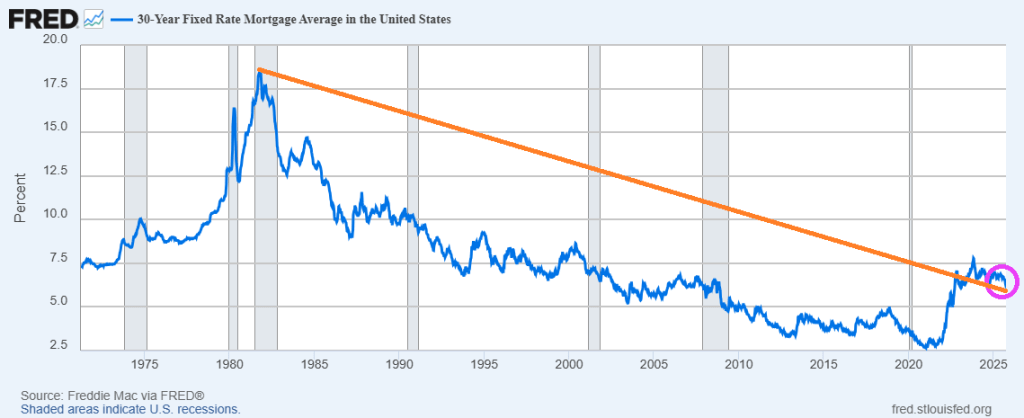

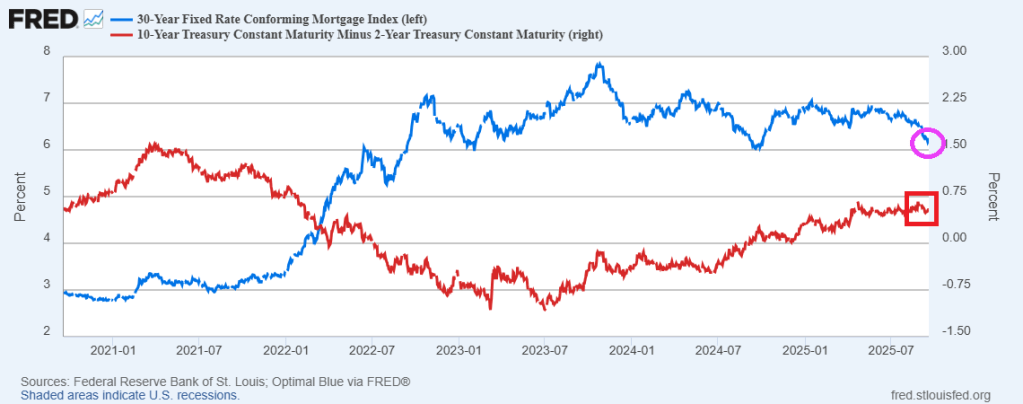

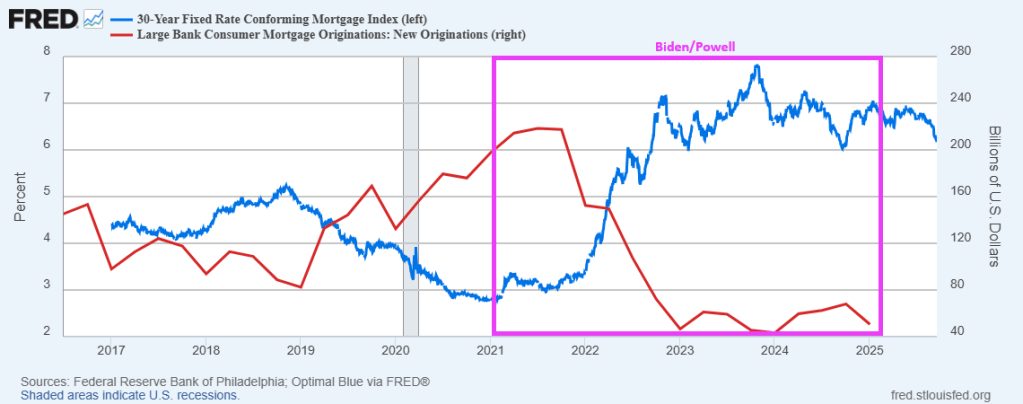

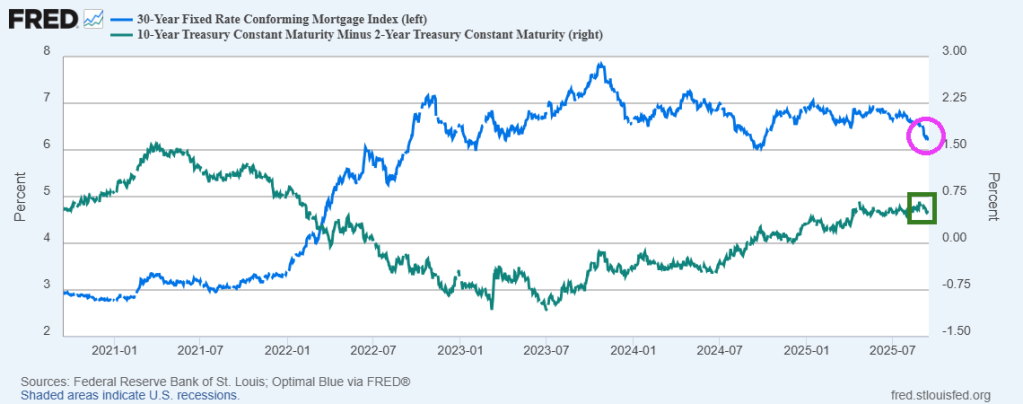

Mortgage rates are falling, helping existing home sales. Note that the 30-year mortgage rate peaked at 18.63% in 1981.

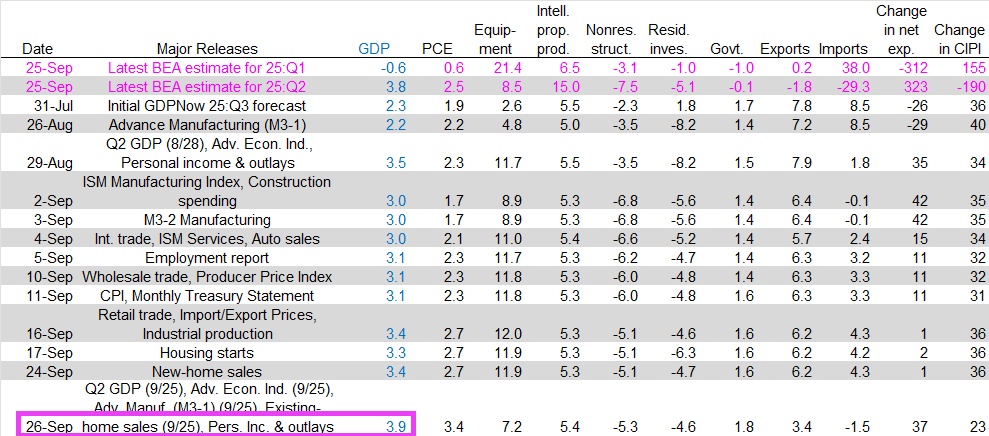

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.9 percent on September 26, up from 3.3 percent on September 17. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the National Association of Realtors, a decrease in the nowcast of third-quarter real gross private domestic investment growth from 6.4 percent to 4.1 percent was more than offset by increases in the nowcast of third-quarter real personal consumption expenditures growth from 2.7 percent to 3.4 percent and the nowcast of the contribution of net exports to third-quarter real GDP growth from 0.08 percentage points to 0.58 percentage points.

Existing home sales helped drive higher GDP growth.

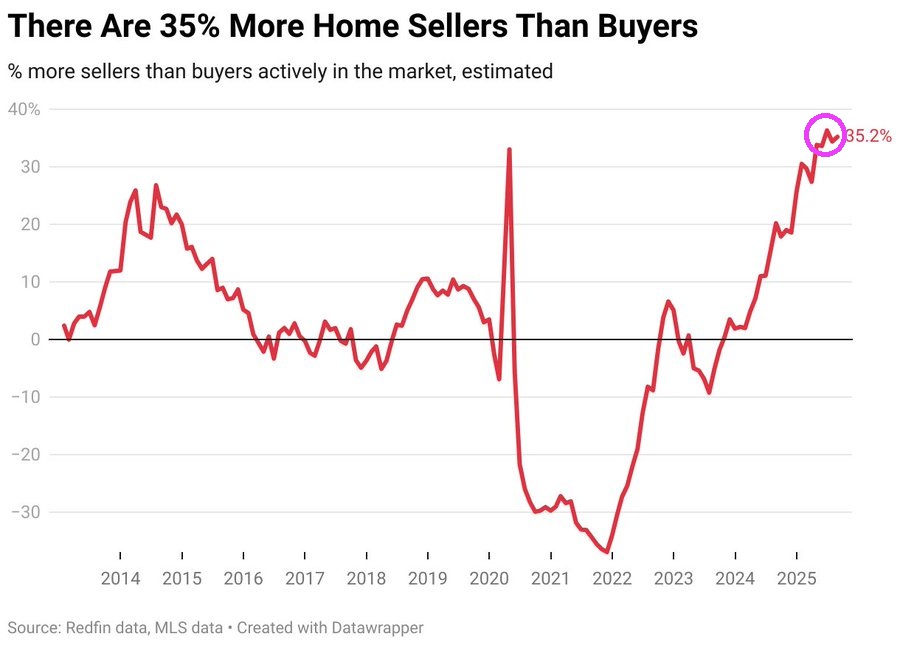

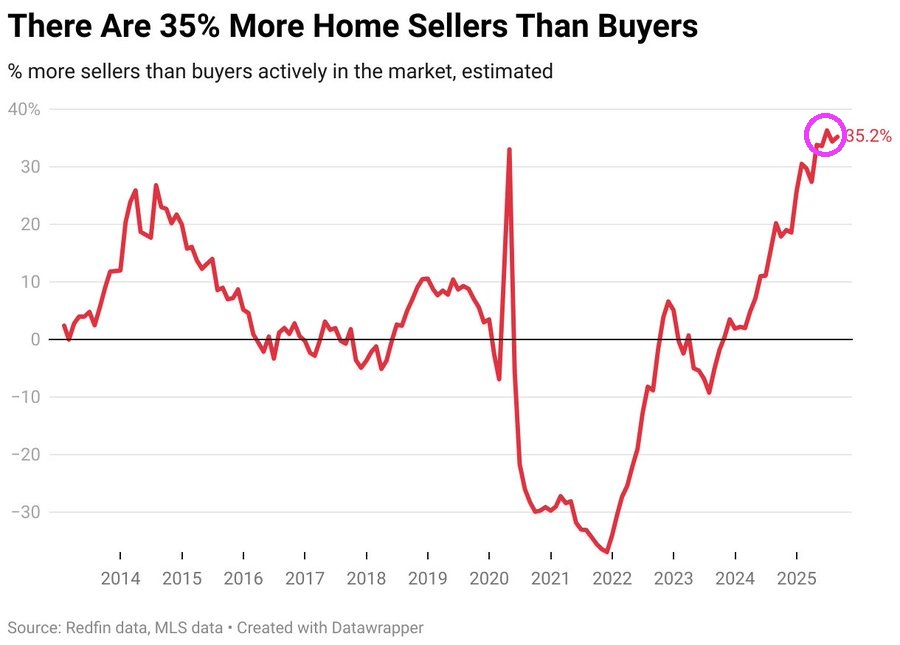

August represents a massive switch from 3 years ago when there were nearly 40% more home buyers and sellers in the US housing market. There are now 35.2% MORE home sellers than buyers!

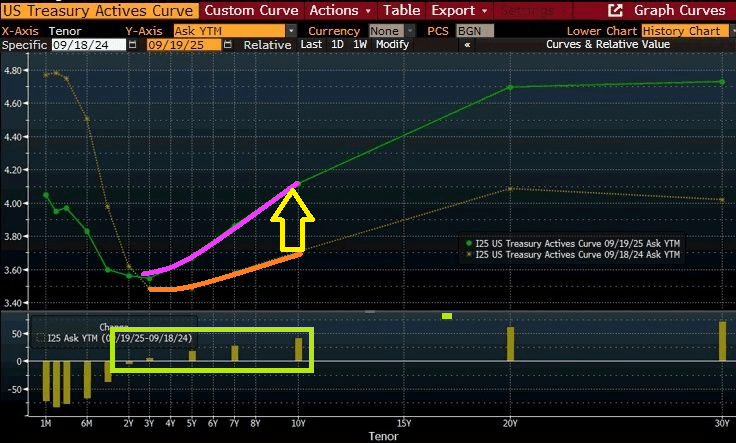

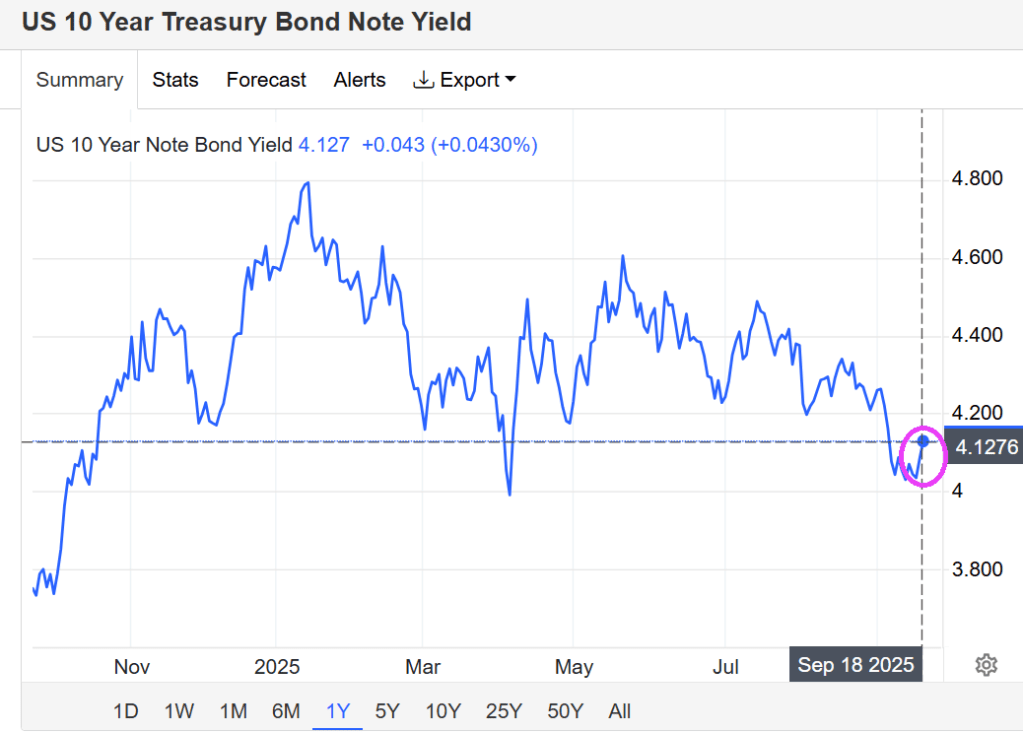

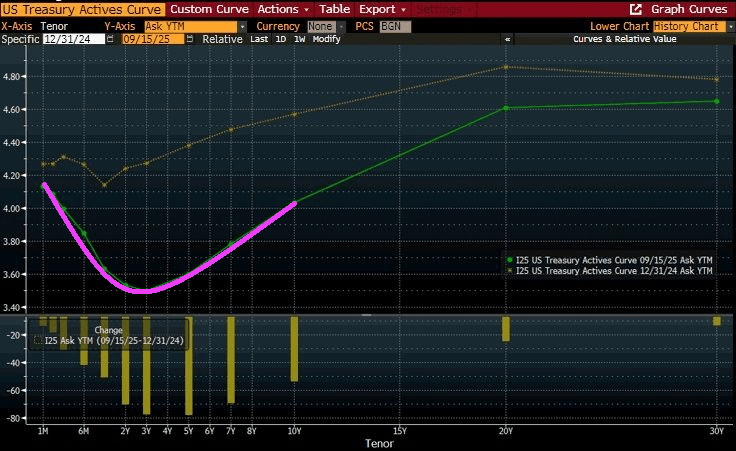

Fed Chair Jerome Powell is the God of Hellfire! We should always wait a day to digest Fed’s annoucements since they often make little sense. For example, yesterday the 10Y yield fell below 4% after The Fed’s announcement … then promplty rose above 4% again. And today, the US Treasury 10Y yield rose to 4.1276%

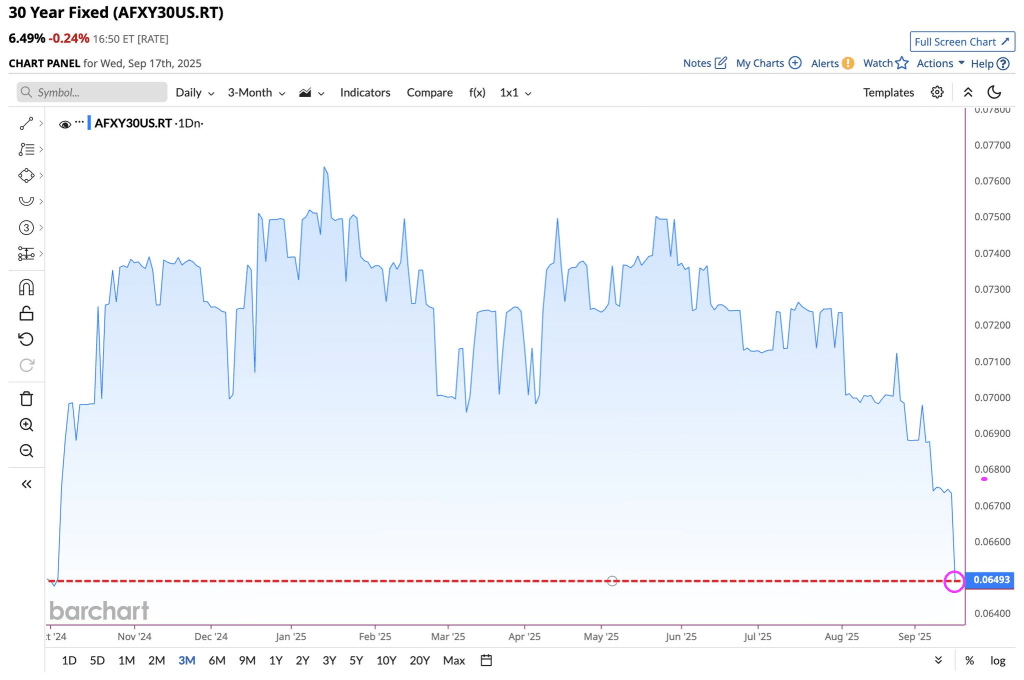

The 30Y US mortgage rate fell to 6.493%.

How about the US Dollar? Similar to the US 10Y yield, volatility reigned following Powell’s muddled message.

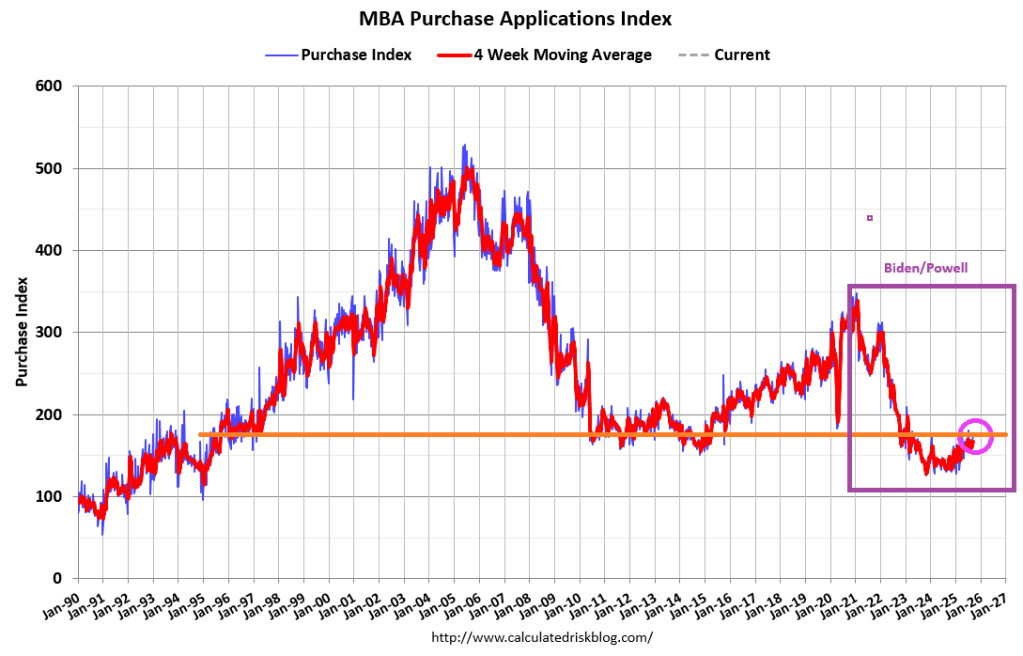

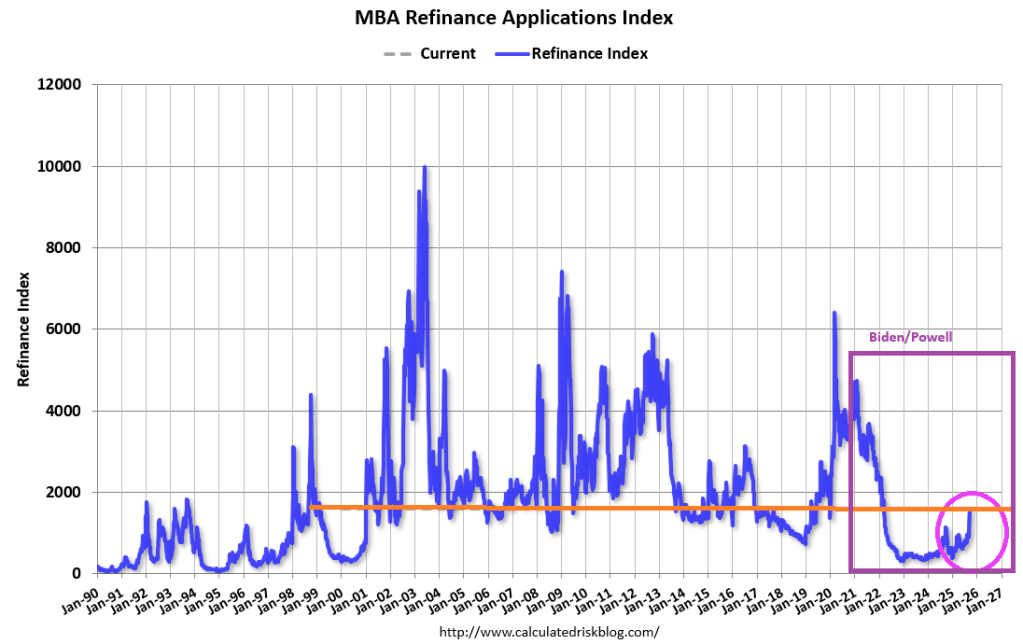

Mortgage applications increased 29.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 12, 2025. Last week’s results included an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 29.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 43 percent compared with the previous week. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index increased 12 percent compared with the previous week and was 20 percent higher than the same week one year ago.

The Refinance Index increased 58 percent from the previous week and was 70 percent higher than the same week one year ago.

Indicative of the weakening job market, and in anticipation of a rate cut from the Federal Reserve, mortgage rates last week dropped to their lowest level since last October, with the 30-year fixed rate declining to 6.39 percent. Homeowners responded swiftly, with refinance application volume jumping almost 60 percent compared to the prior week. Homeowners with larger loans jumped first, as the average loan size on refinances reached its highest level in the 35-year history of our survey. Almost 60 percent of applications were for refinances, but there was also a pickup in purchase applications.

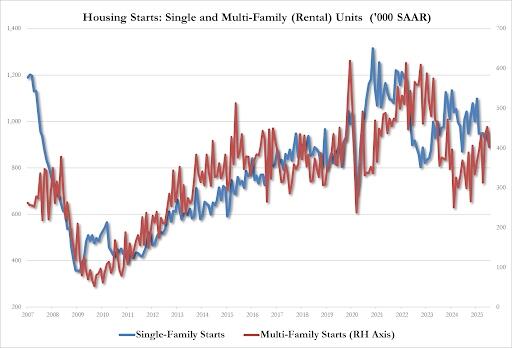

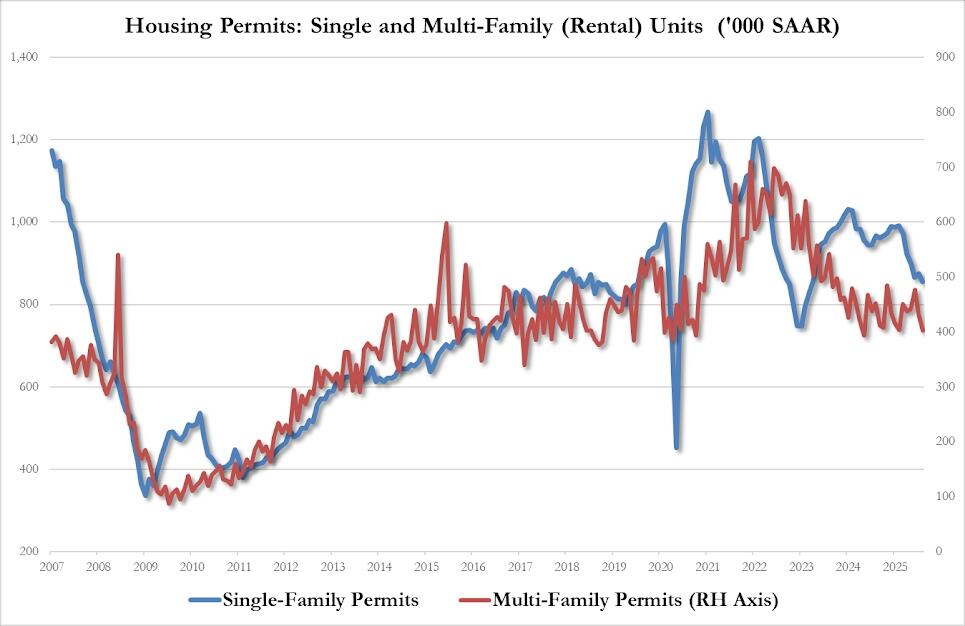

It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

Housing starts:

Single-family 890K SAAR, down 7.0% from 957K in July and the lowest since July 2024

Multi-family 403K SAAR, down 11% from 453K in July and the lowest since May.

Housing permits?

Single-family 856K SAAR, down 2.2% from 875K in July and the lowest since March 2023

Multi-family 403K SAAR, down 6.7% from 432K in July and the lowest since May 2024

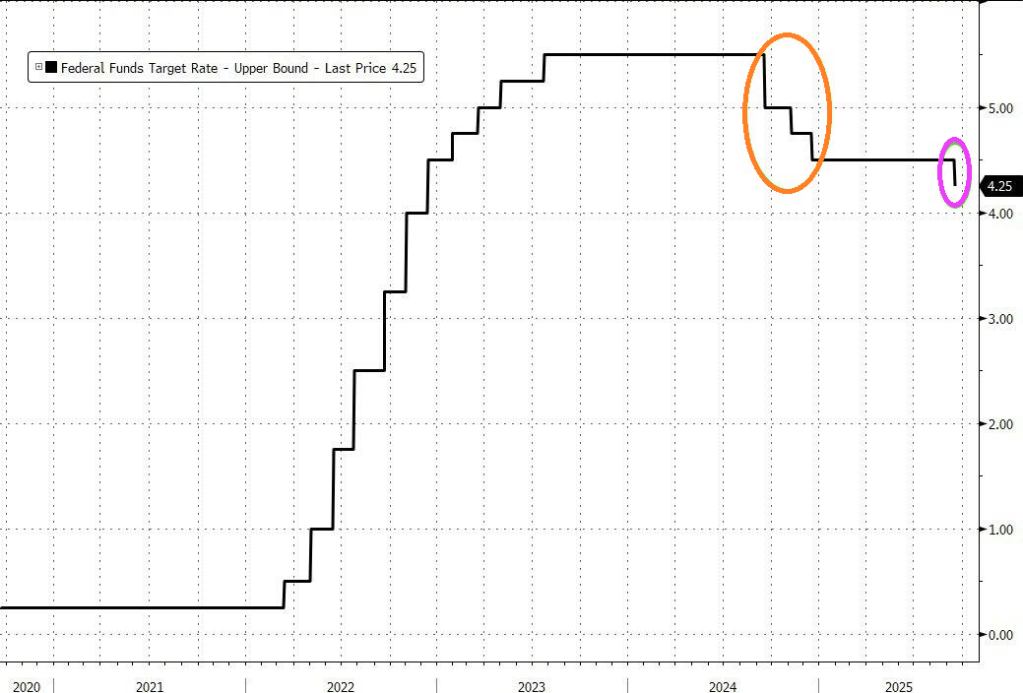

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

{kind=link}

{kind=link}

You must be logged in to post a comment.