The US Bureau of Labor Statistics released their Real Earnings Report for August yesterday. And is it pretty depressing for US workers.

Real average hourly earnings for all employees increased 0.4 percent from July to August, seasonally adjusted. This result stems from an increase of 0.6 percent in average hourly earnings combined with an increase of 0.3 percent in the Consumer Price Index for All Urban Consumers (CPI-U).

Real average weekly earnings increased 0.3 percent over the month due to the change in real average hourly earnings combined with no change in the average workweek.

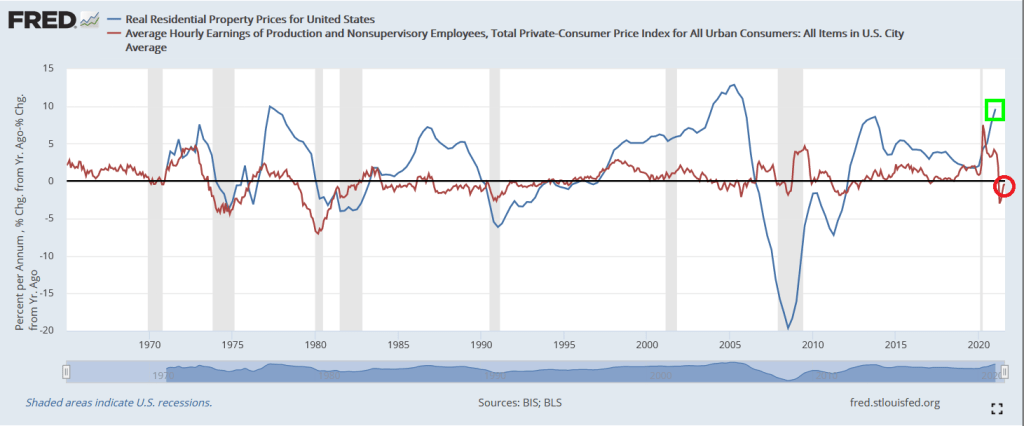

If we look at REAL US housing prices versus REAL average hourly earnings for production and nonsupervisory employees, we can see waves of imbalance between the two measures (also known as “bubbles”). Such as today.

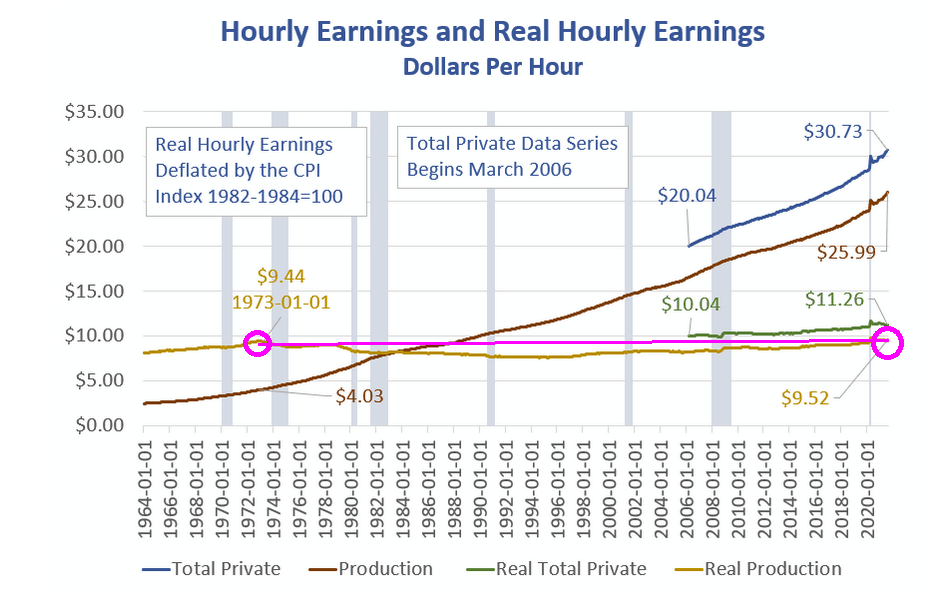

But the real horror chart is the following (courtesy of Mish). It shows that real hourly earnings have barely changed since January 1973.

Of course, labor outsourcing to lower labor cost countries is the chief culprit. Karsten Manufacturing, maker of Ping golf clubs, no longer makes their castings in Phoenix AZ thanks, in part, to EPA regulations. Ping clubheads are now made in Asia.

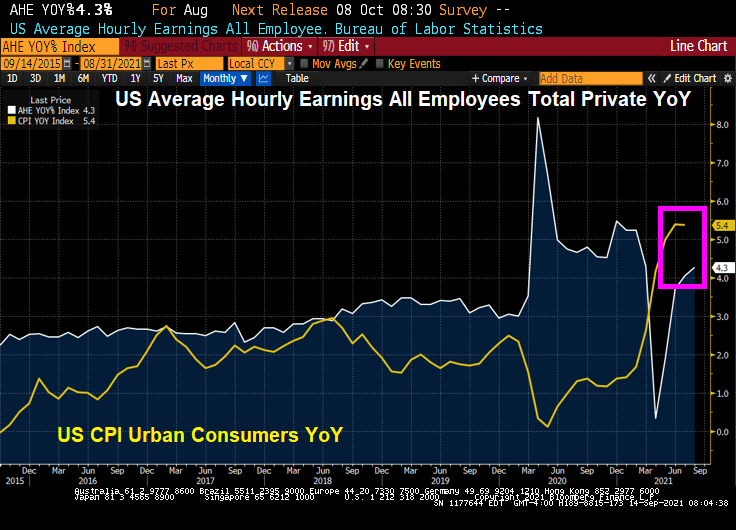

US inflation remained about the same in August as it was in July. CPI YoY fell ever so slightly from 5.4% in July to 5.3% in August. Real hourly earnings remain negative.

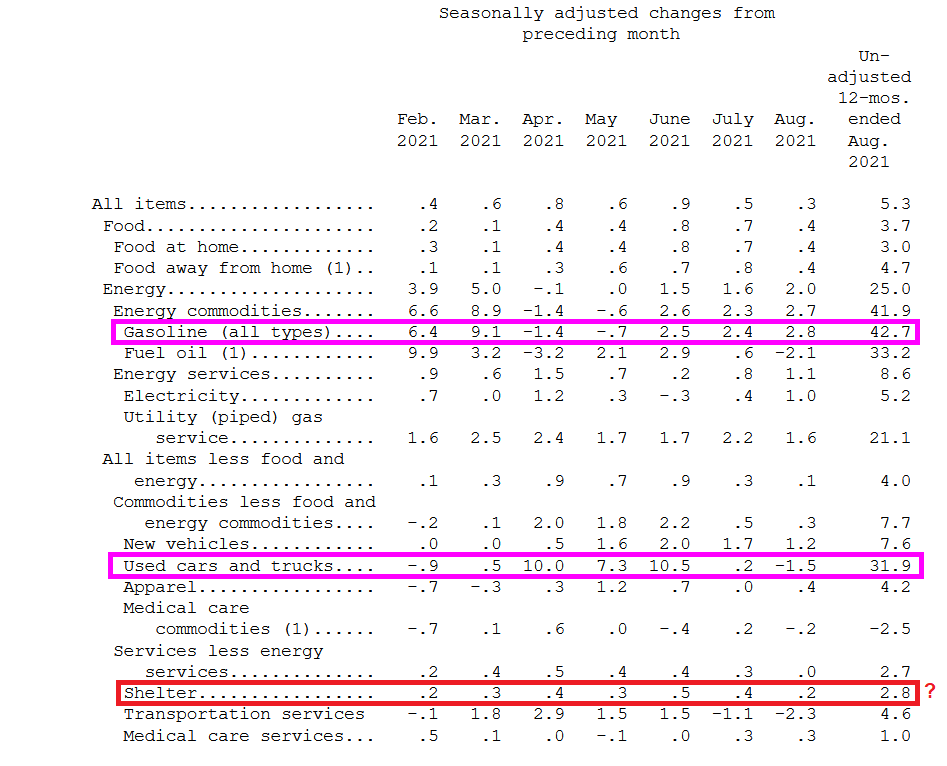

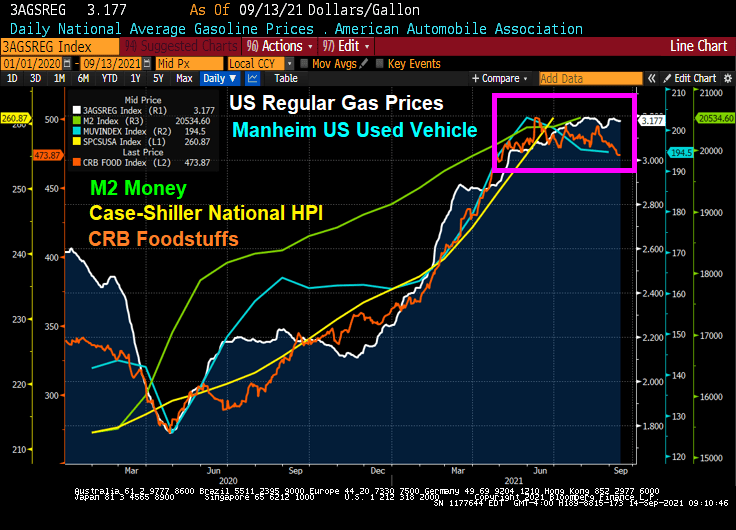

The source of consumer inflation? Gasoline prices rose 42.7% YoY while used cars and trucks rose 31.9% YoY.

Shelter rose 2.8% YoY. That is odd since the Case-Shiller national price index is growing at a torrid 18.61% YoY pace and the Zillow Rent Index YoY has recovered to a sizzling 9.24% YoY pace.

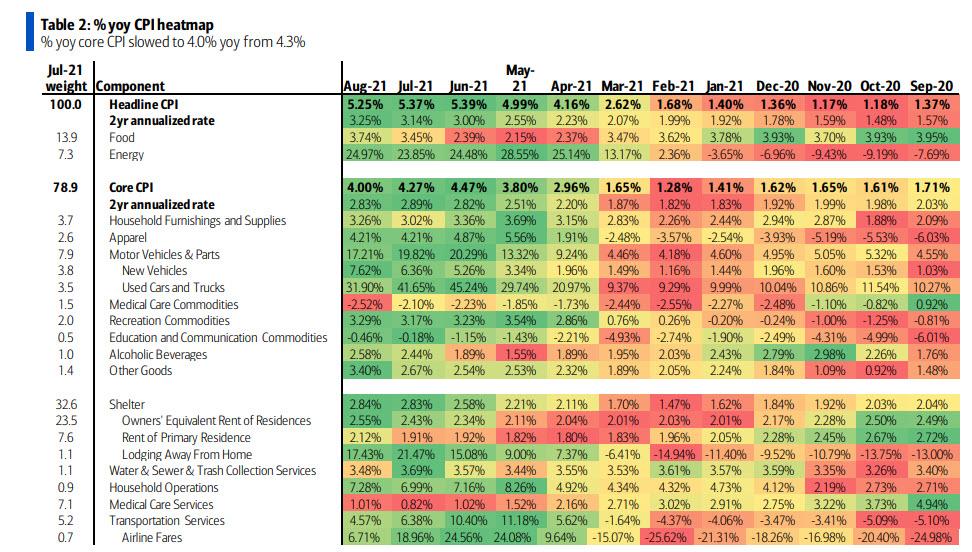

The YoY heatmap of inflation.

However, with the exception of home prices and rent, we are seeing a slowing of used car, foodstuffs and regular gas prices over the summer.

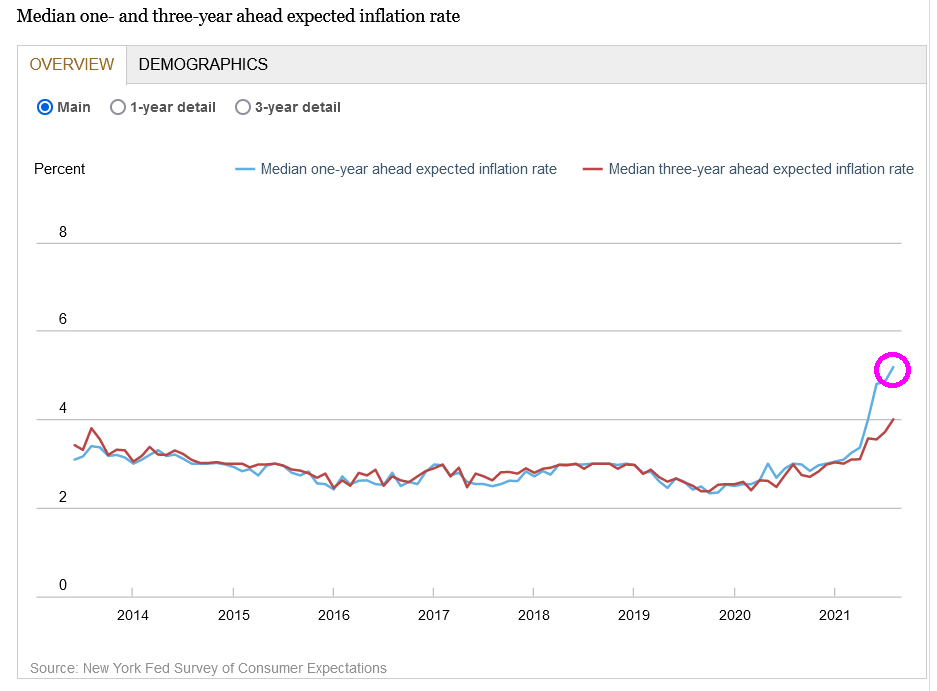

In its August Survey of Consumer Expectations, the bank said Monday that respondents see inflation a year from now at 5.2%, up from 4.9% the prior month. Three years from now, it is expected to be at 4%, up from 3.7% in July. Both readings mark record-high readings for data that goes back to 2013.

It is a shame that in that last reading that the CPI YoY exceeded Average Hourly Earnings YoY by a 5.4% to 4.3% margin.

Yes, inflation is hot, hot, hot and consumers are feeling it.

The South Florida housing market is sizzling with hot money from the North East, pushing up homes values sky high over the last year. One example of the mania is in Palm Beach, where a private island was bought in July and was relisted months later for a whopping 41% premium, according to WSJ.

One of Miami’s top real estate developers, Todd Michael Glaser, is taking advantage of the bubble, fueled by Wall Street bankers and other elites who have the economic mobility to leave the Northeast for the Sunshine State.

Glaser purchased 10 Tarpon Way, also known as 10 Tarpon Isle, for approximately $85 million in July and has since relisted the tiny 2.5-acre island for $120 million, or $35 million more than he paid a few months ago. The island was created by dredging crews in the 1930s and is only accessible by bridge. Glaser bought the island from private investor William M. Toll and his wife, Eileen, who paid $7.6 million for the property in 1998.

Tarpon Island

The real estate developer said potential buyers have two options: pay the $120 million now or wait ten months for a new renovation for $200 million.

Concept Drawing Of New Renovation

He said with all the hot money flowing into the Palm Beach area, “a $100 million house isn’t that crazy anymore, believe it or not,” adding that in the last 18 months, eight $100 million homes have been sold.

If a potential buyer wants to wait ten months and pay an additional $80 million. The developer will completely redesign the mansion by doubling it to 25,000 sqft, with 14 bedrooms, in addition to a hair salon, gym, and spa. A new pool, octagonal tennis pavilion, and a golf practice area will be installed on the outside.

Some ask how long will this speculation fever last as the Federal Reserve could embark on tapering its extensive bond-buying program later this year or early 2022.

One real estate expert believes the peak of the South Florida housing market could be nearing:

Dr. Ken Johnson, a real estate economist with Florida Atlantic University’s College of Business, told local news WPLG that a peak in the housing cycle could have already arrived, but he believes a crash is not in the mix because demand still outpaces supply.

It remains to be seen if some greater fool will pay the $120 million for the island mansion or $200 million tens months later after renovations.

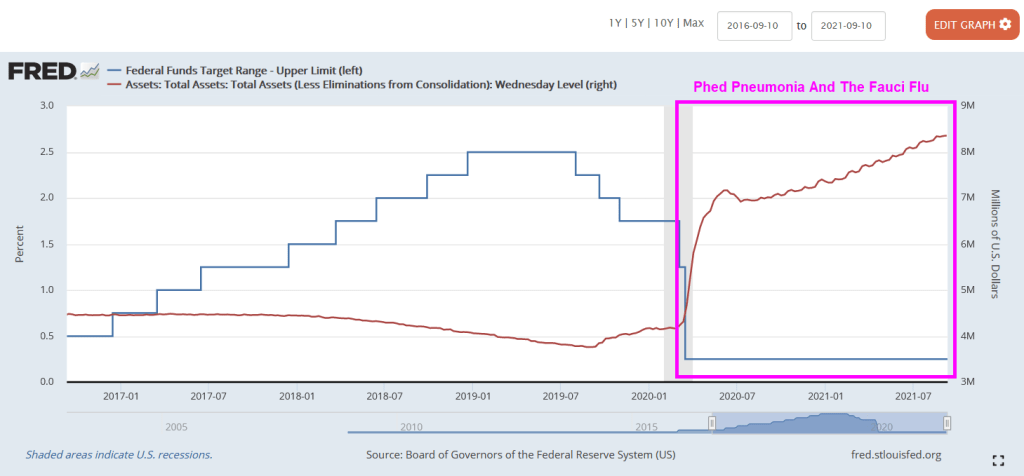

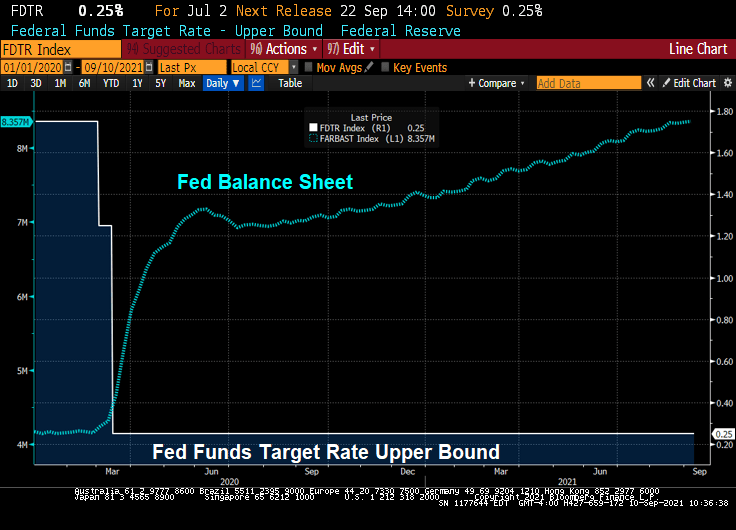

Since the Covid outbreak in early 2020, The Federal Reserve lowered their target rate and super-spiked their balance sheet. Helping to lower bank deposit rates to near zero.

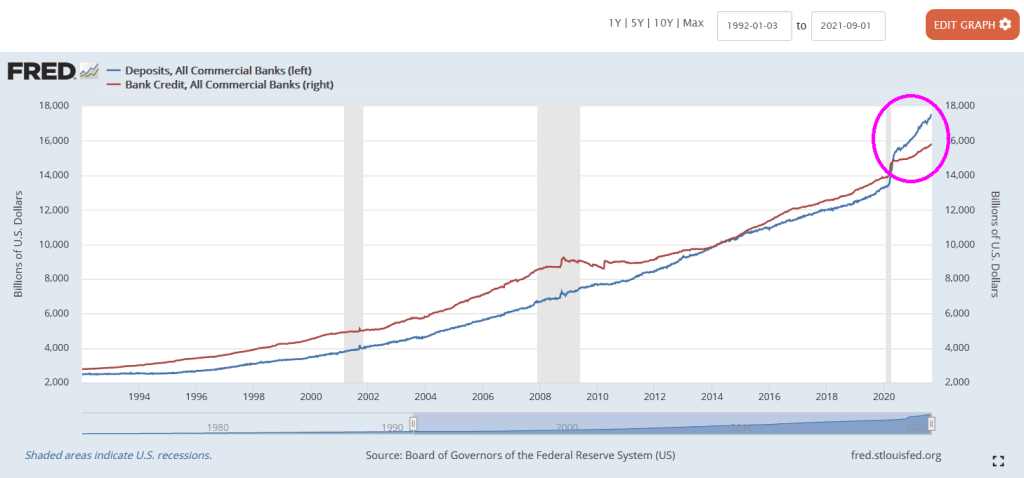

But despite near zero bank deposit rates, we seeing bank deposits are larger than bank credit such as commercial and industrial loans, residential mortgages loans, car loans, etc. Normally, bank credit EXCEEDS bank deposits.

The problem? One of them is negative growth in commercial and industrial lending. It declined 13.5% YoY in August. Of course, The Federal government extended emergency business loans that were counted as C&I loans, hence the spike in C&I loan growth in May 2020. But now we are seeing a real slowdown in C&I lending.

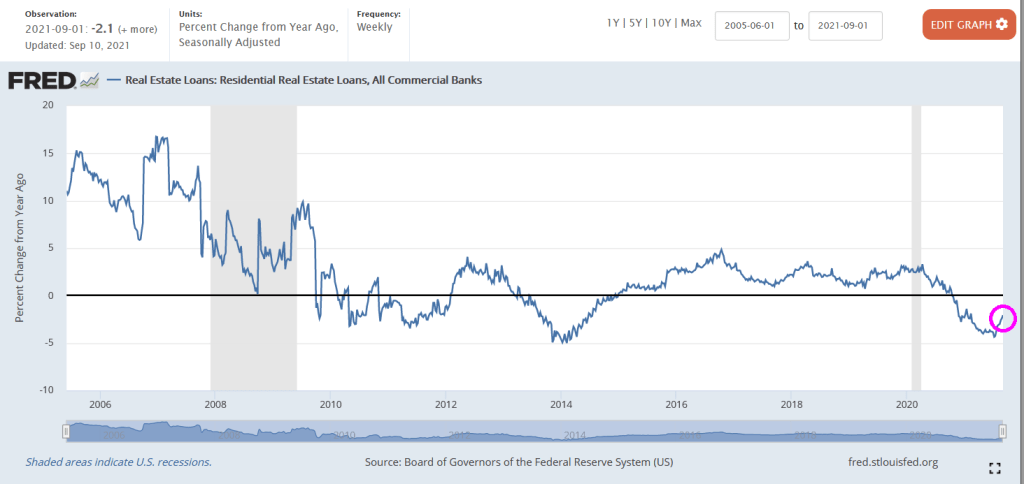

Residential lending is down 2.1% YoY as of September 10 (for August).

Commercial real estate lending? At least it is growing at a 2.9% YoY pace for August.

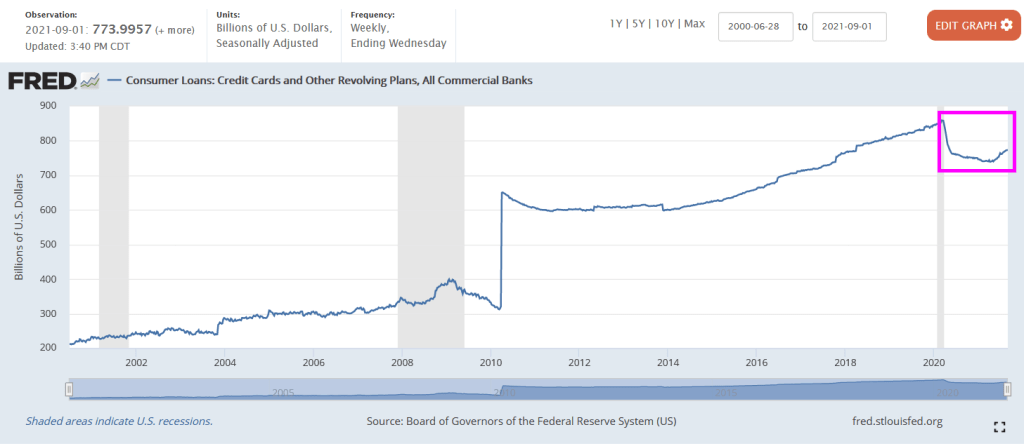

Credit cards and other revolving plans increase steadily since 2014 and then declined after the Fauci Flu struck. But credit cards and revolving credit has started to rise again.

The Fed’s massive overreaction to Covid caused a storm surge in C&I lending that has subsided. But other bank lending has slowed as well.

Lots of bank assets with nowhere to go.

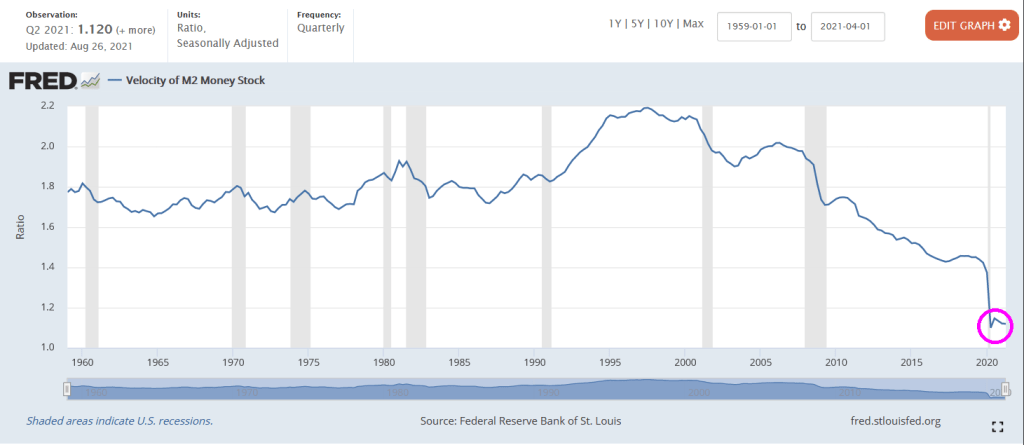

No wonder M2 Money Velocity (GDP/M2 Money) is at historic lows.

Remember, Federal Reserve Chair Jerome Powell is up for reappointment and President Biden must make a decision on his reappointment.

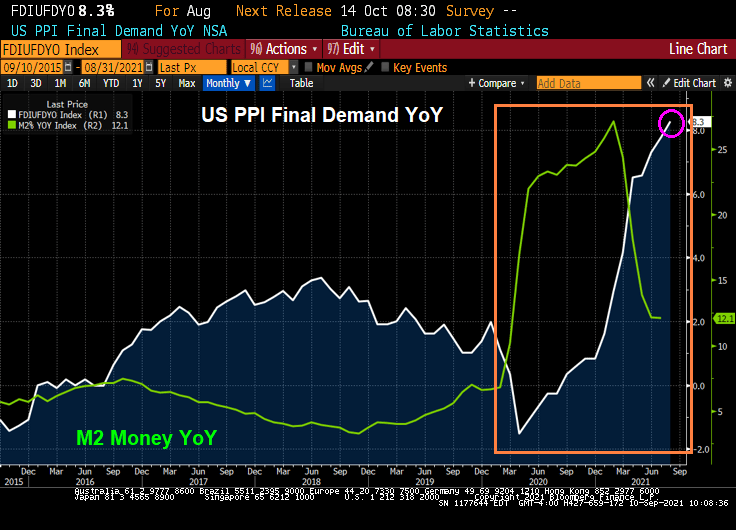

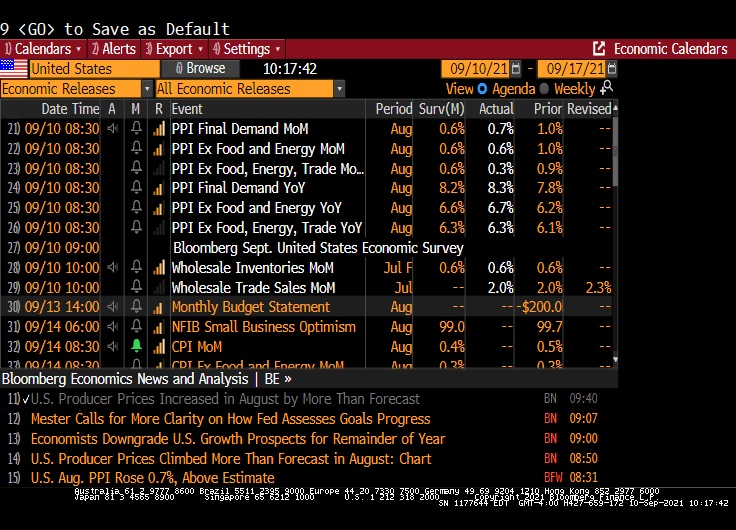

(Bloomberg) — Prices paid to U.S. producers increased in August by more than forecast as persistent supply chain disruptions squeeze production costs higher.

The producer price index for final demand increased 0.7% from the prior month and 8.3% from a year ago, a fresh series high, Labor Department data showed Friday. Excluding the volatile food and energy components, the so-called core PPI advanced 0.6%, and was up 6.7% from August of last year.

PPI Final Demand prices rose 8.3% YoY in August.

Given that there are shortages in the economy, why is The Federal Reserve pumping so much money into the system? It is like repeatedly flushing a clogged toilet hoping it will clear.

The correct way to clear a clogged economic toilet.

Not The Fed way of clearing clogged toilets. Pumping trillions of dollars into a clogged economic system.

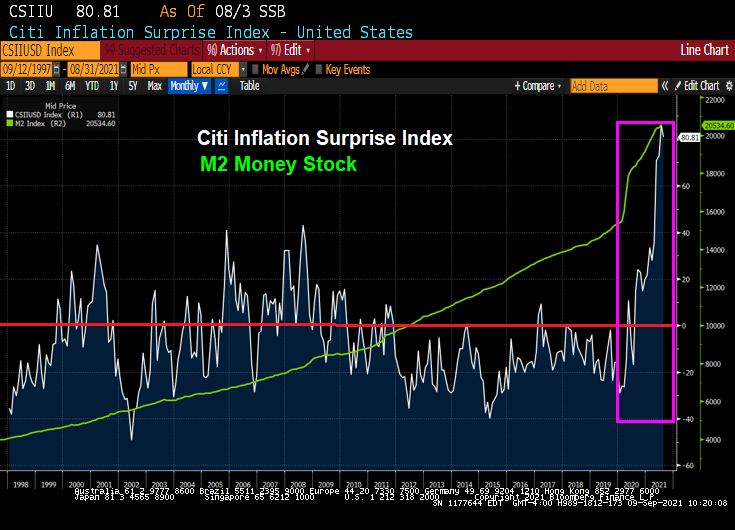

Covid struck in early 2020 and The Fed spiked the punchbowl with a massive surge in M2 Money. Like a storm surge.

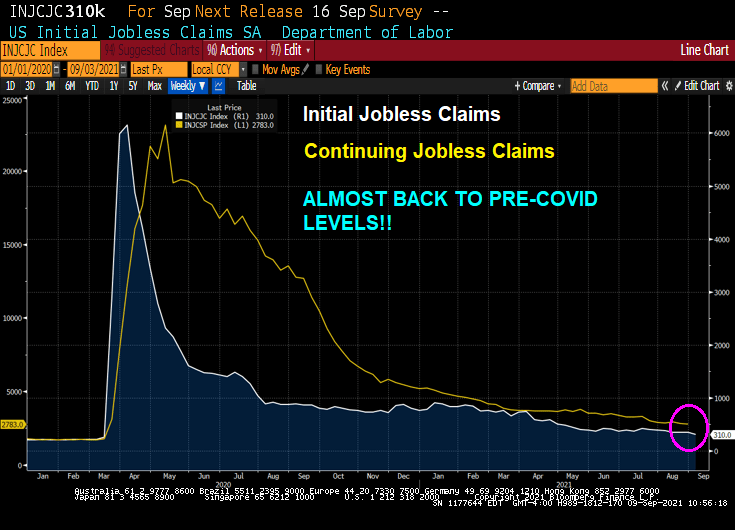

Today’s unemployment report showed initial jobless claims and continuing jobless claims ALMOST at pre-Covid levels.

So it appears that The Fed’s job is done (under the assumption that The Fed had anything to do with the recovery).

So did The Fed almost violently overreact to the Covid crisis? The Atlanta Fed’s Raphael Bostic says it is too early to withdraw while St Louis Fed’s James “Bully” Bullard says it is time to taper.

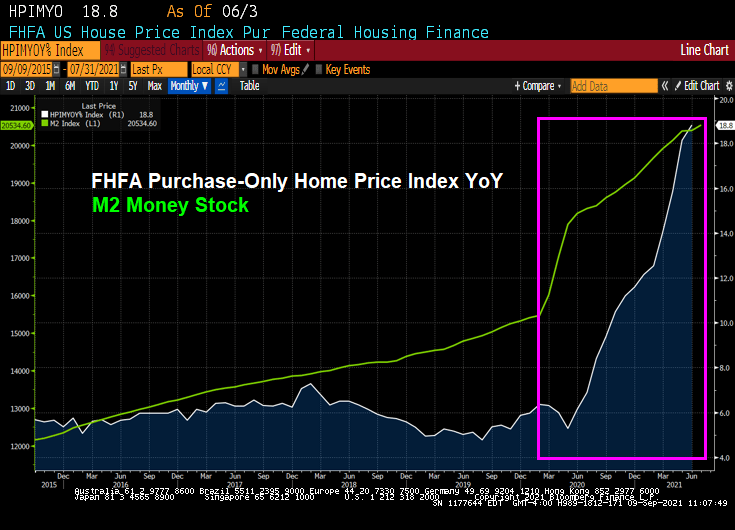

Really Raph? 18.8% price growth is not enough for you?

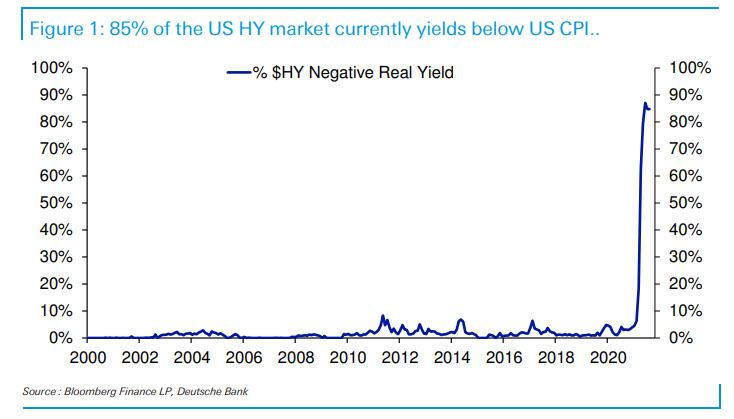

According to Deutsche Bank, 85% of the US High Yield market has a yield below the current rate of inflation.

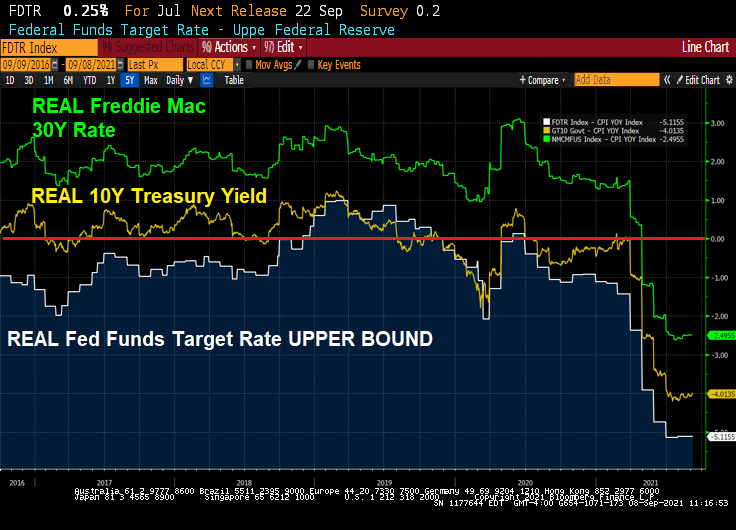

Its not only high-yield bonds that have negative REAL yields, but even The Fed Funds Target rate is negative at -5.12%. The real 10-year government bond yield is -4.01% and the REAL Freddie Mac 30-year mortgage survey rate is -2.5%.

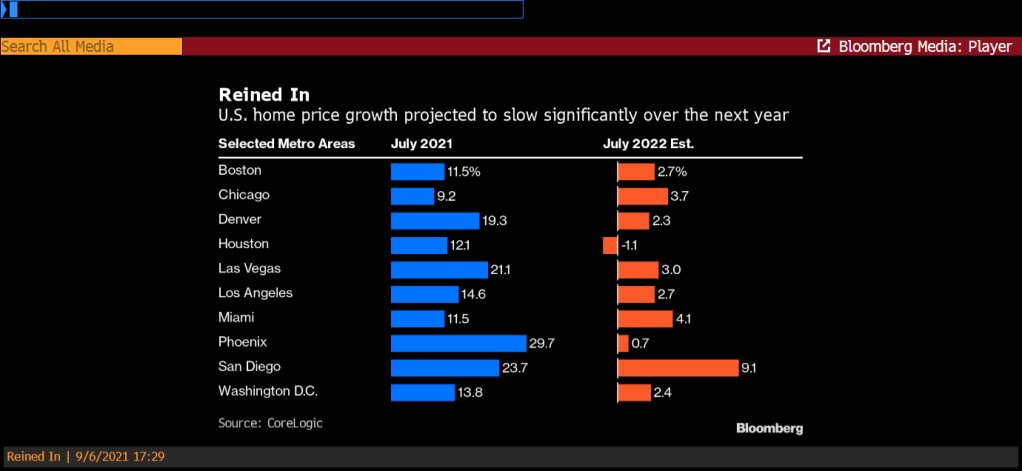

The jump is the largest 12-month gain in the index since the series began 45 years ago. On a month-over-month basis, home prices increased by 1.8% in July from June.

“Home price appreciation continues to escalate as millennials entering their prime home buying years, renters looking to escape skyrocketing rents and deep pocketed investors drive demand,” said Frank Martell, president and CEO of CoreLogic, a global property-information firm.

The rush of home buyers — amid extremely low mortgage rates — has caused a lack of supply, which is unlikely to be resolved over the next five to 10 years “without more aggressive incentives for builders to add new units,” he said in a statement.

But it is the forecast for July 2022 that is interesting. A slowdown in home price growth across the board.

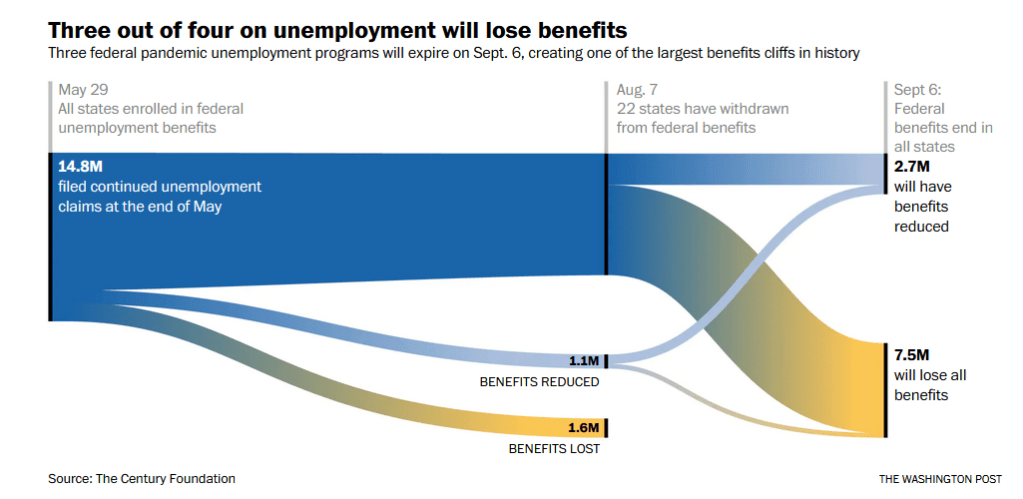

Lets see what happens to wage growth are three out of four Americans lose their Covid benefits as of today.

What if inflation is actually transitory like The Federal Reserve has been saying? Or is The Fed really telling us about an impending economic slowdown after the Fed’s and Federal government stimulypto wears off?

Iron ore prices have slowed noticeably after peaking earlier this year. Lumber futures (random length) have crashed to pre-Covid levels.

On the other hand, food stuffs and raw industrials remain elevated, but the growth in price has stalled (see pink box).

President Biden, aka The Kabul Klutz, is now recommending tax increases as a result of the terrible jobs report from Friday. Rather than focus on The Fed’s monetary stimulus not working for the labor market.

The problem with fiscal stimulus is that the debt lasts forever but the GDP effects are short-lived. And The Fed is a crazy train.

{kind=link}

{kind=link}

You must be logged in to post a comment.