Central banks are turning “hawkish” in the face of inflation.

(Bloomberg) — Treasuries fell, sending 10-year yields to a three-month high, as traders braced for a testing week of heavy bond auctions and continued to digest the prospect that central banks in the U.S. and Europe will step up the pace of policy tightening.

The yield on 10-year Treasuries reached 1.51%, the highest since June, before settling at 1.48%. The yield has climbed 16 basis points over the past week as the Federal Reserve signaled it may start reducing its asset purchases in November and raising rates as soon as next year. Yields on two- and five-year Treasuries hit their highest levels since early 2020, with a combined $121 billion of the securities set to be sold Monday. A seven-year auction is due Tuesday.

While Treasuries briefly extended the selloff after a report showed durable goods orders exceeded economists’ forecasts, they started to pare losses after U.S. equity futures soured.

Bond yields increased across the globe last week as central banks move to reduce pandemic stimulus. The Bank of England surprised markets by raising the prospect of increasing rates as soon as November, and Norway delivered the first post-crisis hike among Group-of-10 countries. In the U.S., traders pulled forward wagers on an interest-rate increase to the end of 2022 following last week’s Fed meeting.

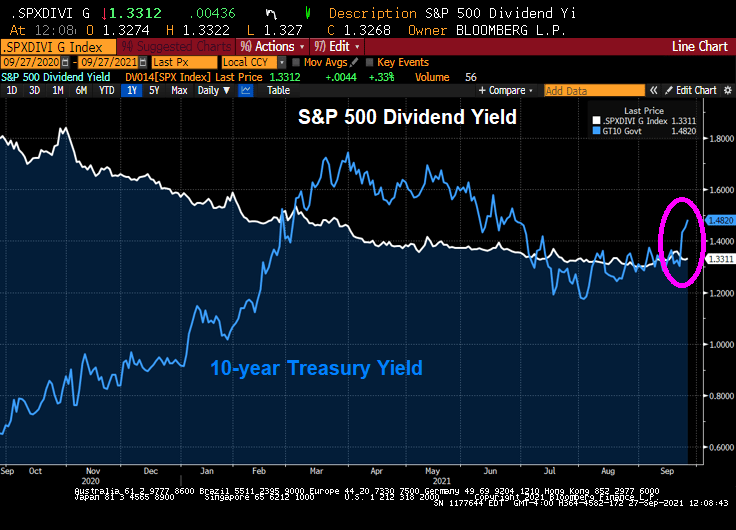

On the equity side, FAANG stocks trail the S&P 500 as 10-year Treasury yield climb.

We have the 10-year Treasury yield climbing above the S&P 500 dividend yield.

Phil Hall of Benzinga wrote a series of excellent articles in four parts for MortgageOrb (although “The Orb” has removed his name). Here are the links to his stories.

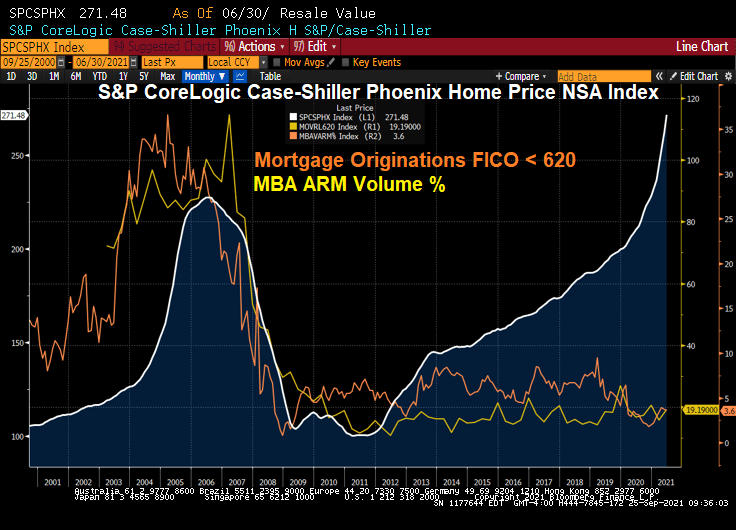

After re-reading these excellent articles on the housing bubble and crash, I thought I would take the opportunity to present a few charts to highlight the housing bubble, pre-crash and post-crash.

Here is a graph of Phoenix AZ home prices. Note the bubble that peaked in mid 2006. The Phoenix bubble correlates with the large volume of sub-620 FICO lending and Adjustable-rate mortgage (ARM) lending. Bear in mind, many of the ARMs prior to 2010 were NINJA (no income, no job) ARM loans.

What happened? Serious delinquenices at the national levels spiked as The Great Recession set in and unemployment spiked.

Since the housing bubble burst and surge in serious mortgage delinquencies, The Federal Reserve entered the economy with a vengeance. And have never left, and increased their drowning of markets with liquidity.

The Fed whip-sawing of interest rates in response to the 2001 recession was certainly a problem. They dropped The Fed Funds Target rate like a rock, then homebuilding went wild nationally and home prices soared thanks to Alt-A (NINJA) and ARM lending. But now The Fed is dominating markets like a gigantic T-Rex.

Oddly, then Fed Chair Ben Bernanke never saw the bubble coming. Or the burst.

Speaking of pizza, Donato’s from Columbus Ohio is my favorite. Founder’s Favorite is my favorite, but they do offer the dreaded Hawaiian pizza (ham, pineapple, almonds and … cinnamon?)

(Bloomberg) — The Federal Open Market Committee directed the New York Fed’s Desk to increase the size of the counterparty limit for the overnight reverse repo facility, according to a statement.

Per-counterparty limit increased to $160b/day from $80b/day, with the change taking effect Sept. 23

“The increase in the per-counterparty limit from the current level of $80 billion per day helps ensure that the ON RRP facility continues to support effective policy implementation,” according to statement. “All other ON RRP operation parameters remain the same”

And banks didn’t wait long to park $135.2b overnight at The Fed.

When combined with the ongoing expansion of the Fed’s balance sheet, we are seeing to see the expansion of the United States on Liquidity.

I certainly hope The Federal Reserve starts normalizing interest rates. Hold that Fed tiger!

(Bloomberg) — Sales of previously owned U.S. homes fell in August, suggesting that demand is moderating as lean inventory and high prices squeezed out some buyers.

Contract closings decreased 2% from the prior month to an annualized 5.88 million, in line with economists’ estimates, figures from the National Association of Realtors showed Wednesday. “Clearly the home sales are settling down but above pre-pandemic conditions,” Lawrence Yun, NAR’s chief economist, said on a call with reporters.

Lawrence Yun is correct. There was a huge spike in existing home sales (EHS) following the Covid outbreak and the overreaction by The Federal Reserve (aka, when the ain’ts went marching in). Despite continuing stimulus, but EHS has simmered down.

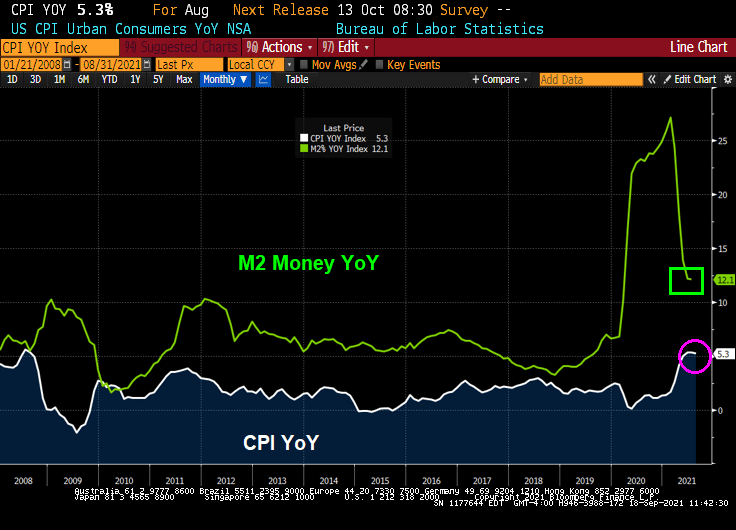

At least the median price of EHS YoY slowed to 12.1% YoY as The Fed slows M2 Money growth.

Inventory remains relatively low compared to historic levels while price zooms with Fed stimulus.

Want home price growth to slow its insane growth? Hold that tiger! That is, The Fed has to start normalizing interest rates.

Building materials copper and PVC (pipes) both surged with The Fed’s Cat 5 hurricane approach to liquidity. Then copper backed-off, but PVC rose when Hurricane IDA struck the gulf coast.

The Fed will announcing their plans (maybe) at 2pm today.

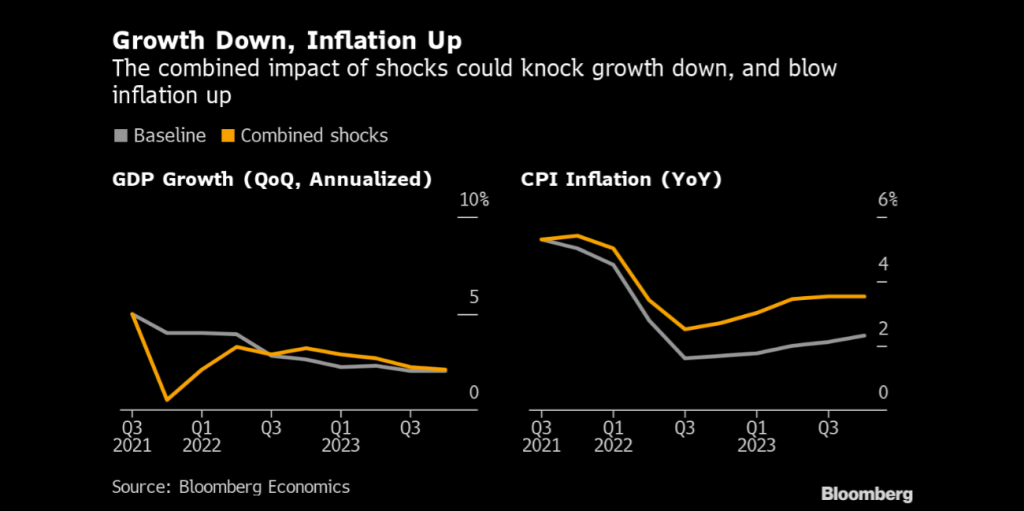

What would it take to knock the U.S. recovery off course and send Federal Reserve policy makers back to the drawing board? Not much — and there are plenty of candidates to deliver the blow.

From one direction: U.S. debt-ceiling deadlock, China property slump or simply an extension of Covid caution could hit growth and jobs — taking the Fed’s proposed taper of bond purchases off autopilot, and pushing its first interest-rate increase back to 2024 or later. From the other: Sustained supply-chain snarl-ups could keep inflation stubbornly high and unmoor inflation expectations — forcing an acceleration of the taper, and an early rate liftoff in 2022.

And if shocks arrive from both directions at once, the upshot could be a combination of weak growth and rapidly rising prices — not as severe as the stagflation of the 1970s — but still leaving Fed Chair Jerome Powell and his colleagues with no easy answers.

In the following, we use Bloomberg Economics’ new modeling tool SHOK to explore these scenarios. None of them represents our base case. At a moment of elevated uncertainty, it makes sense to pay more attention to the risks.

Is the U.S. Economy Headed for a Slowdown? Signs of a slowdown in the U.S. economy aren’t hard to find.

August payrolls — just 235,000 new jobs, one-third of the expected number — were a red flag. The delta variant has made consumers cautious again. The University of Michigan’s index of sentiment plunged in August; only six declines since the modern index was launched in 1978 have been bigger.

Add all these pieces together, and a recovery that looked unstoppable just a few weeks ago now appears to be losing steam. At Bloomberg Economics, we have cut our prediction for annualized third-quarter growth to 5%, from above 7% at the start of the quarter. Others have gone lower, with forecasters at some of the big banks anticipating growth closer to 3%. Even if delta subsides, it’s not hard to imagine scenarios where the slide continues.

One of them involves the partisan impasse over raising the U.S. debt ceiling. The U.S. government is expected to reach the limits of its debt-servicing capacity in October. Default, a potentially catastrophic event for the global financial system, still appears an outside possibility. But even without one, recent history shows that dancing around the possibility — triggering a persistent risk-off period in the markets — can have serious consequences. Separately, a government shutdown starting Oct. 1 would hardly be helpful when the recovery is already struggling to find its footing.

In the three weeks around the 2011 debt-ceiling standoff, the S&P 500 index plummeted more than 15% and corporate borrowing costs spiked. Using SHOK we estimate that a repeat performance would shave about 1.5 percentage points off annualized fourth-quarter growth — and ensure a rocky start to 2022.

Global Risks to the Fed’s Plan Not all the risks originate so close to home.

Fears of a China housing crash have long haunted global markets. Now, President Xi Jinping’s “common prosperity” agenda has turned that into a real possibility.

Regulators are cracking down on abuses that inflated property values, and tight controls on lending have helped push prices and new construction sharply down. That’s left Evergrande, one of the nation’s biggest developers, on the cusp of a default. The consequences of a wider slump could be severe, because real estate drives demand for everything from steel and concrete to furniture and home electronics — contributing as much as 29% of China’s GDP, all told.

It wouldn’t take a sub-prime style meltdown to send shockwaves around the world and move the dial for the U.S. China’s economy is currently forecast to enter 2022 with growth at around 5%. A property slump could take that down to 3%, triggering a blow to trade partners, a drop in oil and metal prices, and a risk-off moment in global markets. In that scenario, the U.S. would limp into 2022 with the recovery marked down and inflation back below the 2% target.

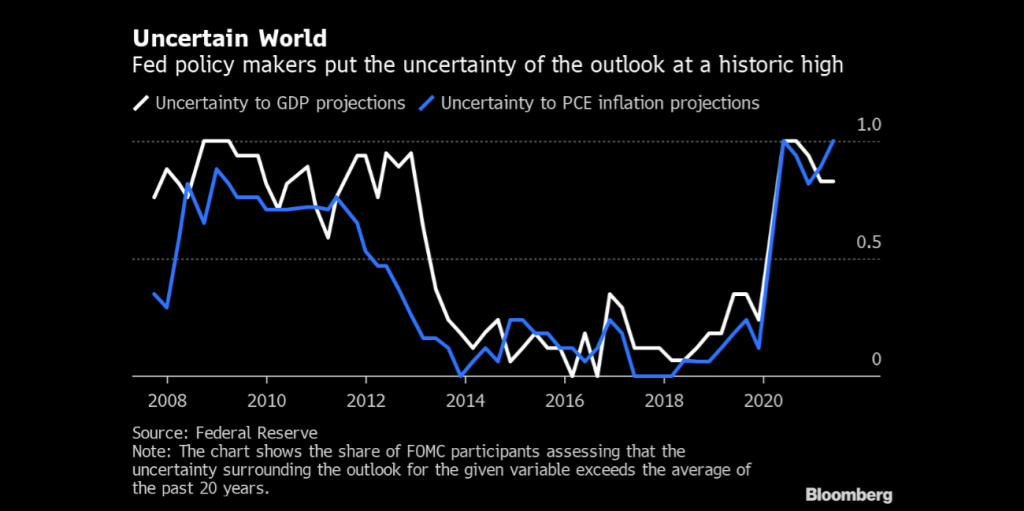

When Is Jerome Powell Likely to Raise Rates? Powell has set out the FOMC’s criteria for rates liftoff: maximum employment, and inflation that hits and is set to exceed the 2% target for some time. A blow to employment and demand from a debt-ceiling standoff or China shock might mean those criteria are not met. Rate hikes could be kicked into the long grass, with expectations moving from 2023 out to 2024 or beyond. The test for tapering is less stringent, and a start at the end of this year appears close to baked in. Even so, if the recovery stumbles the Fed might have to make a course correction, introducing discretion into a process that markets expect to run on autopilot.

In 2015, the stock-market and currency slump in China — and the sustained shift to global risk-off sentiment that triggered — was enough to delay the start and slow the pace of the U.S. tightening cycle. In 2021, the Fed might not have that luxury.

China’s residential property slowdown deepened last month, signaling that regulatory tightening and an escalating crisis at the country’s most indebted developer are hurting buyer sentiment.

Supply-chain breakdowns — from port closures to shortages of semiconductors and lumber — have been one of the main factors pushing U.S. inflation above 5% this summer. That’s enabled Powell to label the price jumps as “transitory” and soothe fears of an upward spiral. The lower CPI reading for August provides some support for that thesis.

It wouldn’t take much, though, for further supply shocks to keep inflation uncomfortably high. From home electronics to textiles, American consumers load their shopping carts with goods that are made in Asia and delivered via supply chains that crisscross the continent. When the inflation rate for used cars in the U.S. hit 45% this year, driven by semiconductor shortages that threw assembly lines into disarray, it illustrated what can happen when those fragile linkages break down.

All of this adds to the risk of further “transitory” shocks to inflation. One early-warning signal: according to press reports, semiconductor giant TSMC has announced plans for price hikes of as much as 20% next year.

The effects of pandemic-induced supply-chain disruptions are still rippling through businesses and households, reflected in higher prices for goods, delays in receiving them and flat-out shortages.

For the Fed, inflation running hot into 2022 would be troubling on its own, and worse if it triggers a shift in inflationary psychology. If businesses start to feel comfortable setting prices higher, and workers start demanding higher wages to compensate, the risk is a situation reminiscent of the wage-price spirals of the 1970s — when it took a recession engineered by the Volcker Fed to squeeze inflation expectations out of the system.

Unmoored inflation expectations would very likely trigger an early and aggressive response from the Fed: an accelerated taper, and a rate hike in 2022.

A no-win scenario would be if the two blows — to output and jobs, and to supply chains and prices — landed at the same time, leaving Fed officials in a quandary. Ease policy to support growth and they would add fuel to the inflationary fire. Tighten to bring prices under control, and they would exacerbate the drag on the recovery, throwing more Americans out of work.

Agreement in Congress, or decision by the Democrats to go it alone, could remove the default risk. China has in the past proved skillful at shifting gears to avoid a housing crash. Vaccination rates in Asia are rising. The latest U.S. data — inflation slowed and retail sales rose — have been encouraging.

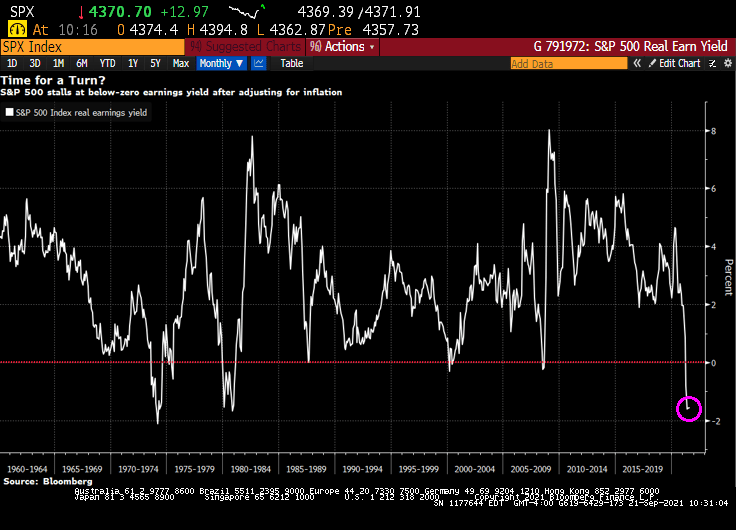

The stock market mildly rebounded from yesterday’s mild correction, but a glaring problem remains: S&P 500 real earning yields are negative.

With all the Federal government fiscal stimulus and Federal Reserve monetary stimulus, we are seeing inflation and that inflation is eating away at S&P 500 earnings yield.

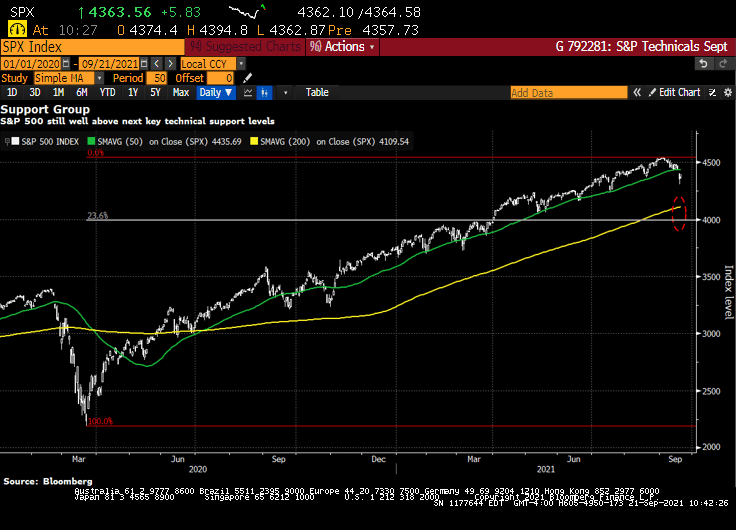

The S&P 500 is still well above key technical support levels.

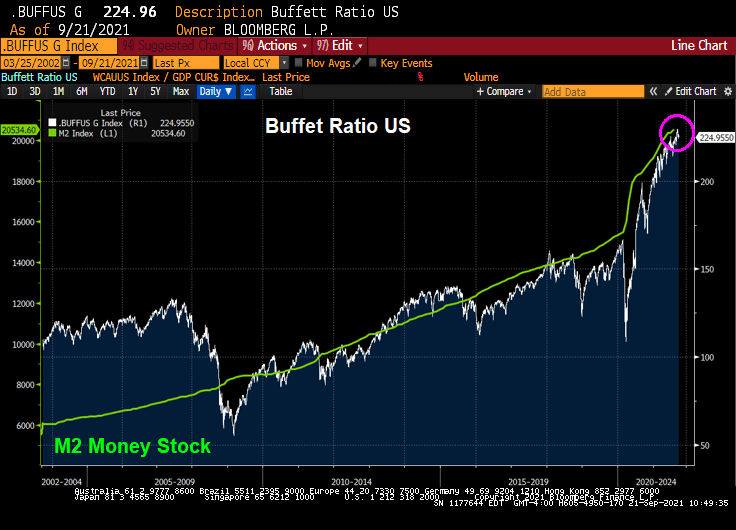

However, the Buffet ratio is raging along with Fed stimulus.

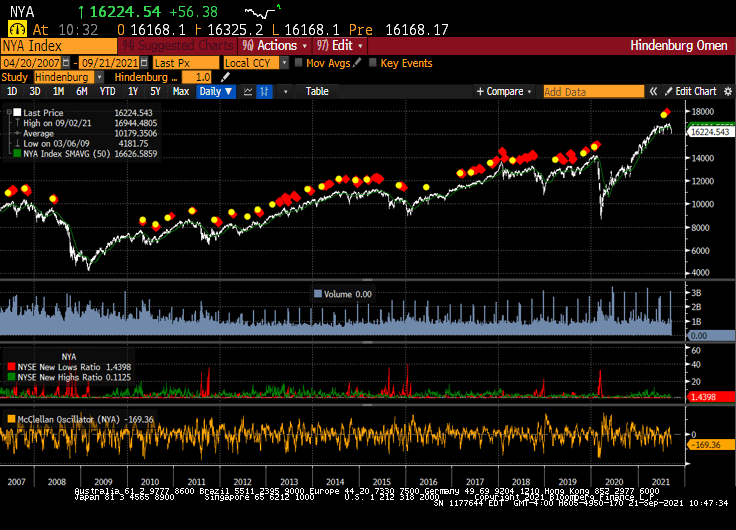

And the Hindenburg Omen is flashing RED!

The mystery of the Flying Fed is whether they will withdraw their massive monetary stimulus or not.

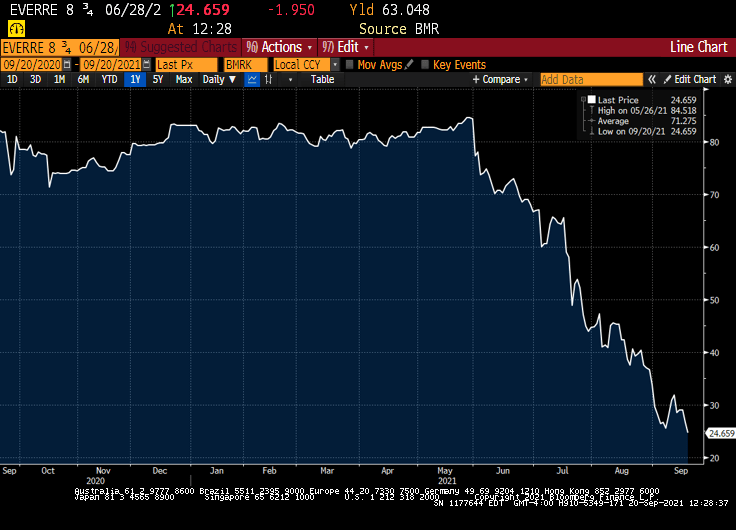

(Bloomberg) — The S&P 500 Index extended its decline past 2% Monday afternoon amid growing investor jitters about China’s real estate crackdown potentially sparking a financial contagion. And the Hang Seng fell 3.30% overnight.

The benchmark gauge was down 2.1% as of 12:08 p.m. in New York. All of the 11 major industry groups declined, with the energy, financials and materials sectors leading the losses. The tech-heavy Nasdaq 100 index slumped 2.4%, while the blue-chip Dow Jones Industrial Average retreated 1.9%.

By 2:33pm, the Dow is down 2.55%, NASDAQ down 3.15%.

Volatility also soared, with the Cboe Volatility Index — often called Wall Street’s “fear index” — jumping as much as 29% to 26.75, the highest level in over four months.

“While the Evergrande situation is front and center, the reality is, stock market valuations are overstretched and the market has enjoyed too long of a break from volatility and Monday’s stock market declines are not surprising,” said David Bahnsen, chief investment officer at the Bahnsen Group, a wealth management firm.

As Evergrande bonds continue to tank.

Meanwhile, most commodity prices are falling … except for UK Natural Gas Futures which are up 16.5%!

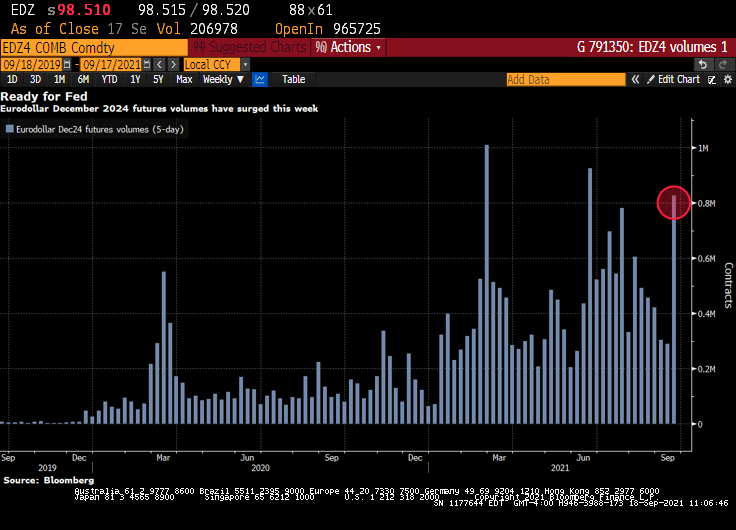

The next Federal Reserve Open Market Committee (FOMC) meeting is next week with an announcement on Wednesday, September 22nd.

(Bloomberg) — Volume in the December 2024 eurodollar futures contract has surged Friday, approaching 200k, highest in the strip. Weekly volume exceeds 800k ahead of next week’s FOMC meeting. The December 2024 contract is a proxy for the Fed’s taper timeline, similar to the belly of the Treasuries curve (aka, the belly of the beast).

As of 2:30pm ET, nearly 197k Dec24 eurodollar contracts had traded, bringing weekly total to 816k, third most in its lifetime; notable flows on the day have included three block trades for 5k each:

The contract also appeared in curve trades including 9.3k Sep24/Dec24 3-month, 18.9k Dec23/Dec24 12-month and 24.8k Dec22/Dec24 24-month

The Dec22/Dec24 eurodollar spread has been in the spotlight since Morgan Stanley recommended the steepener in June as a way to exploit the disconnect between expectations for the pace and timing of Fed rate increases

As of today, we see a kink in the US Dollar Swaps curve at 21m.

With inflation the highest since 2008, and M2 Money still growing at 12.1% YoY, it is time for The Fed to take it foot off the accelerator pedal.

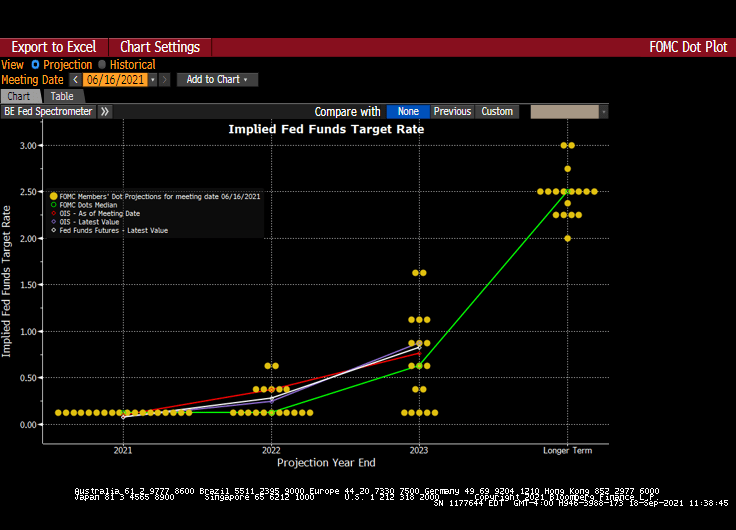

The Fed’s Dots Plot as of the last FOMC meeting indicates a willingness to let the Fed Funds Target rate start rising again after over a decade of rate suppression.

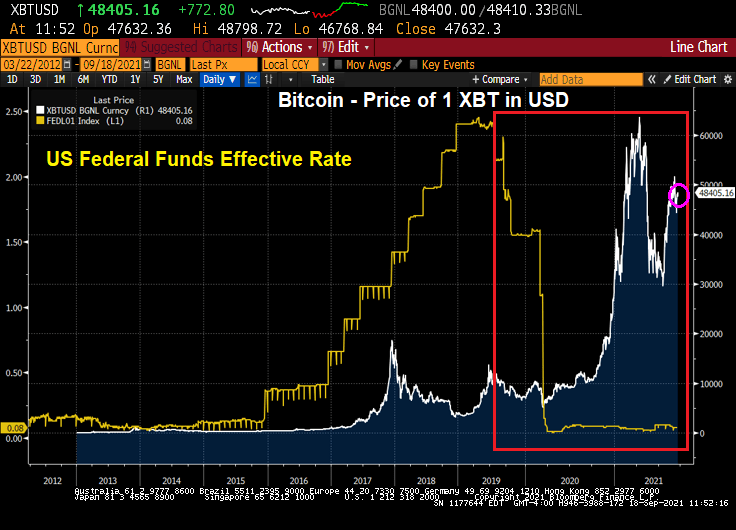

Given the fear of The Fed tapering (eventually), is it any wonders alternative investments such as Bitcoin have risen as The Fed cut rates?

This is the Steve Urkel economy where The Federal Reserve and Federal government screw everything up with their policies (or follicies) and say “Whoops! Did I do that?”

(Bloomberg) — U.S. consumer sentiment rose slightly in early September but remained close to a near-decade low, while buying conditions deteriorated to their worst since 1980 because of high prices.

The University of Michigan’s preliminary sentiment index edged up to 71 from 70.3 in August, data released Friday showed. The figure trailed the median estimate of 72 in a Bloomberg survey of economists.

Buying conditions for household durables, homes and motor vehicles all fell to the lowest in decades. The report said the declines were due to complaints about high prices. Consumers expect inflation to rise 4.7% over the coming year, matching the highest since 2008.

September’s UMich Buying Conditions for Houses fell to 60 … thanks to superheated house prices.

I can just picture Fed Chair Jerome Powell channeling Steve Urkel and saying “Whoops!! Did I do that?”

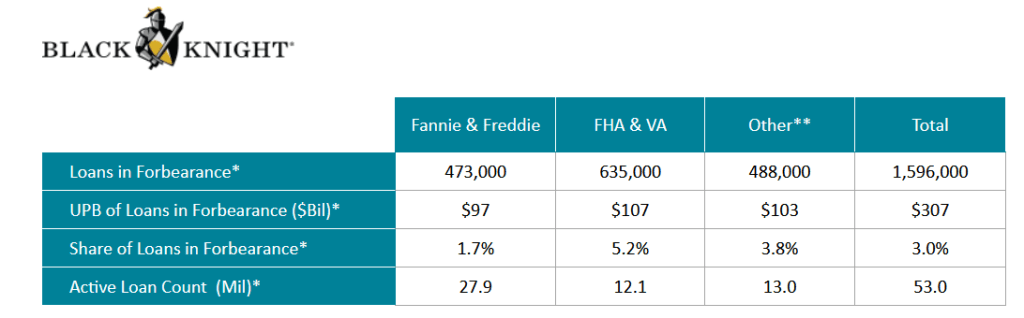

The Covid epidemic hit the single-family mortgage market hard in early 2020, leading mortgage lenders and servicers to offer FORBEARANCE to borrowers who were having trouble making their mortgage payments due to loss of hours or a loss of job.

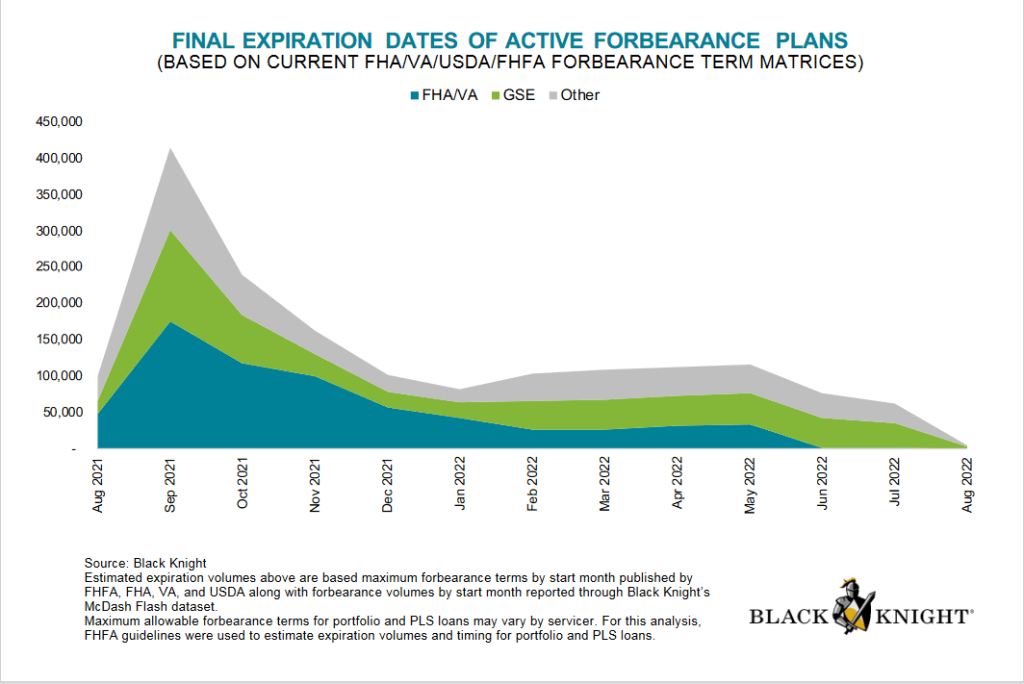

The good news? Active forbearance plans are much lower today than at their peak after the Covid epidemic struck in early 2020 with active forbearance plans peaking in May 2020.

Forbearance plans are due to expire in

What is forbearance, you ask? Forbearance is when a mortgage servicer or lender allows a borrower to temporarily pay their mortgage at a lower payment or pause paying your mortgage. The borrower will have to pay the payment reduction or the paused payments back later.

Despite forbearance, Fannie Mae still reported $7.2 billion in net income in Q2 2021. Notice the difference between single-family SDQ and the SDQ rate without forbearance. Freddie Mac reported $3.7 billion in Q2 2021 net income.

Here is a look at Fannie Mae’s net income over the past year and SDQ rates.

Under the existing seller/servicer eligibility requirements, the Agency SDQ Rate is defined as 100 multiplied by (the UPB of mortgage loans 90 days or more delinquent or in foreclosure for Fannie Mae, Freddie Mac, and Ginnie Mae/Total UPB of mortgage loans serviced for Fannie Mae, Freddie Mac, and Ginnie Mae). Beginning with the financial quarter ending Jun. 30, 2020, the Agency SDQ Rate will include an adjustment for mortgage loans in a COVID-19-related forbearance plan that are 90 days or more delinquent and were current at the inception of the COVID-19-related forbearance plan. The UPB of such mortgage loans shall be multiplied by .30 and added to the UPB for SDQ mortgage loans for the purposes of determining the numerator in the calculation of the Agency SDQ Rate.

You must be logged in to post a comment.