Headline! “Fed’s Kaplan says delta variant could cause him to rethink his tapering view”

Face it, the Federal Reserve may alter its growth path on asset purchases of Treasuries and Agency Mortgage-backed Securities, but it is doubtful that they will pare back their balance sheet. Call it “A Never-ending balance sheet for you” world.

Why? Seemingly never-ending Covid crisis, etc.

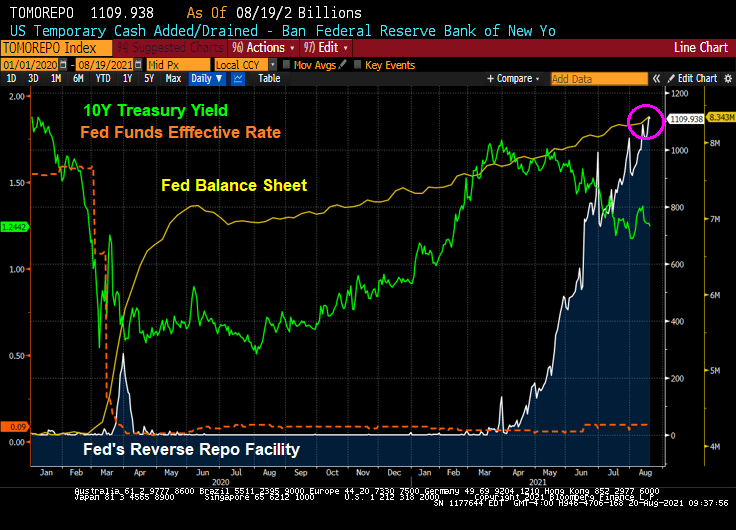

Let’s look at US Treasury yields today. The 10-year Treasury yield is up slightly to 1.25% as of 10am EST.

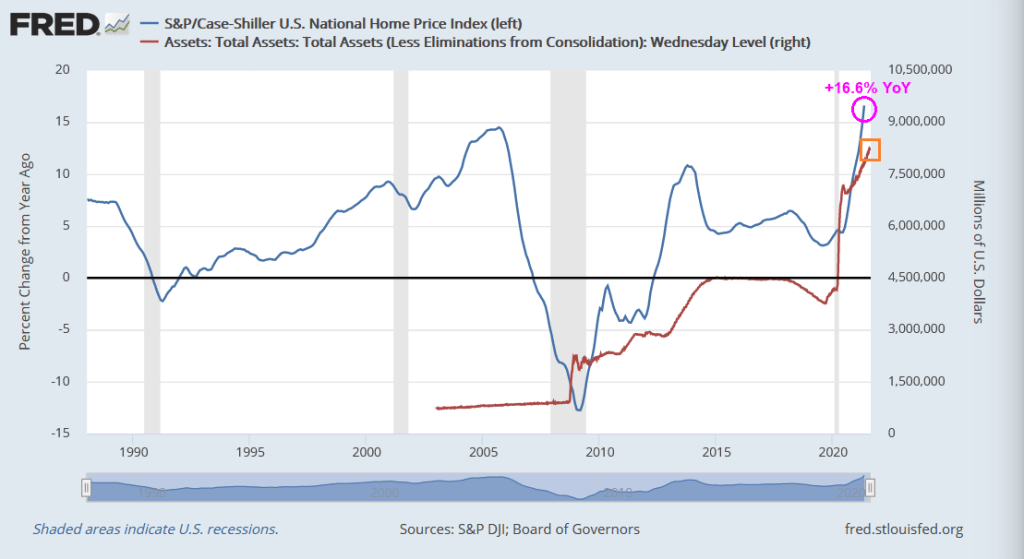

Here is a chart of the 10-year Treasury yield, Fed Funds effective rate, Fed Balance sheet and reverse repos since the Covid outbreak and Fed massive intervention. Bottom line, the have repressed the short-term interest rates and put downward pressure on the 10-year Treasury yield.

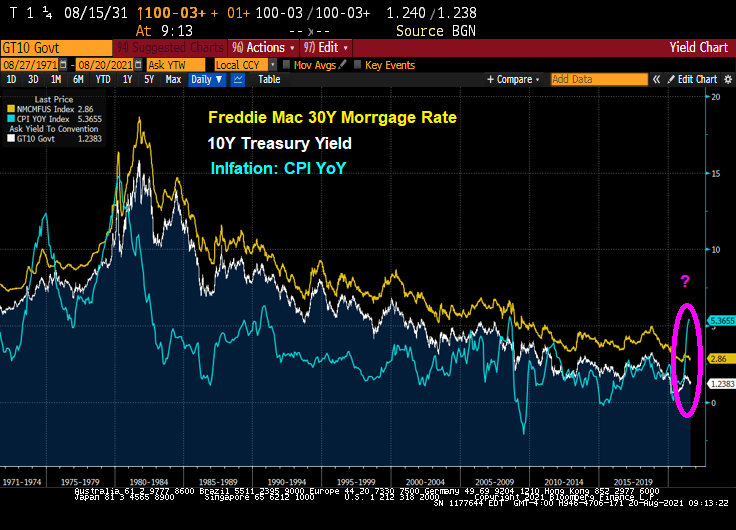

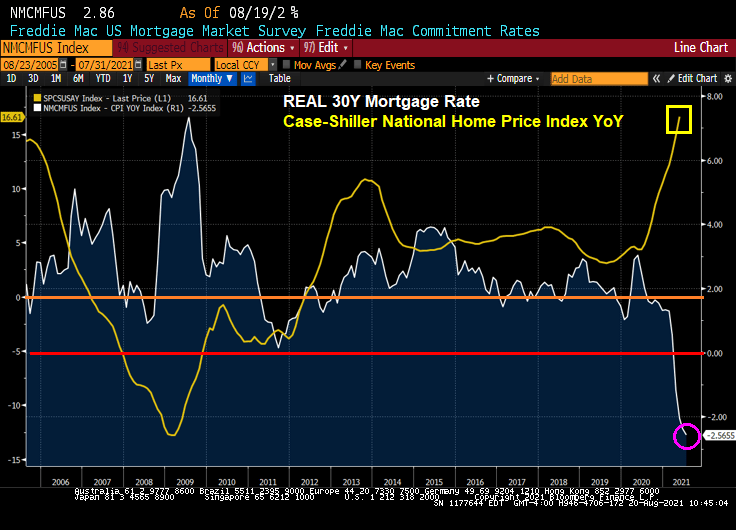

As the 10-year Treasury yield remains repressed DESPITE HIGHEST INFLATION RATE SINCE 2008, the Freddie Mac 30-year mortgage rate remains repressed as well. Yes, that mean NEGATIVE REAL MORTGAGE RATES.

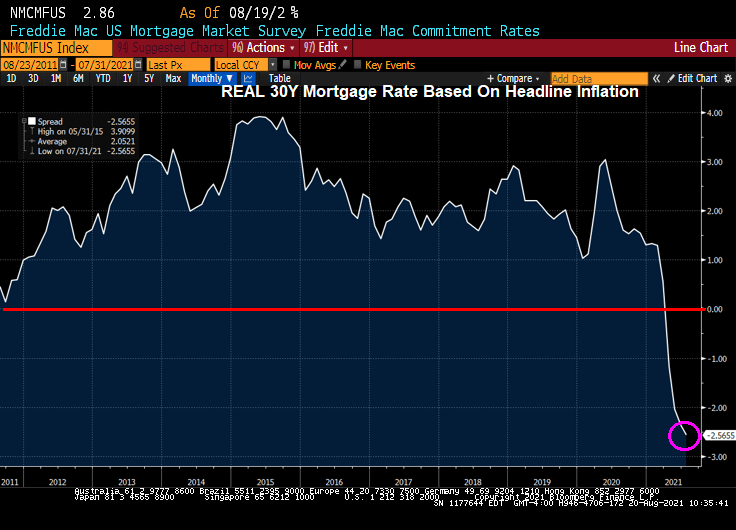

This produces a REAL mortgage rate of -2.56%.

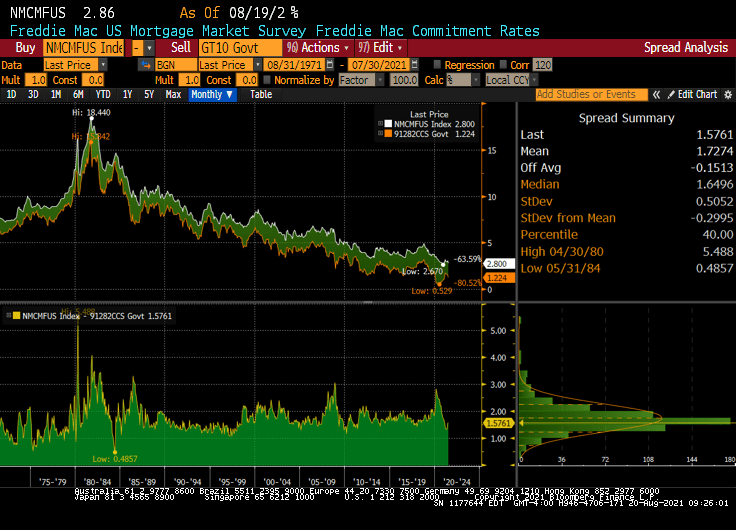

The spread of mortgage rates over the 10-year Treasury yield is about 173 basis point since 1971.

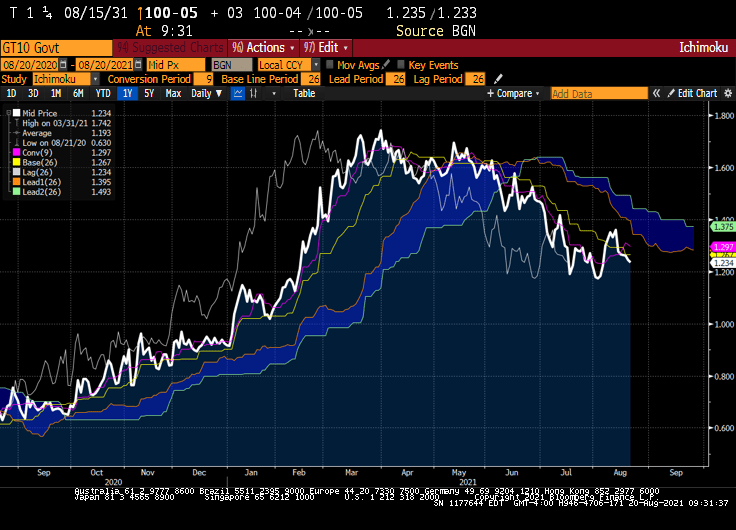

Where will Treasury yields go from hear? If we believe technical analysis like the Ichimoku Cloud, the 10-year Treasury rate will likely rise.

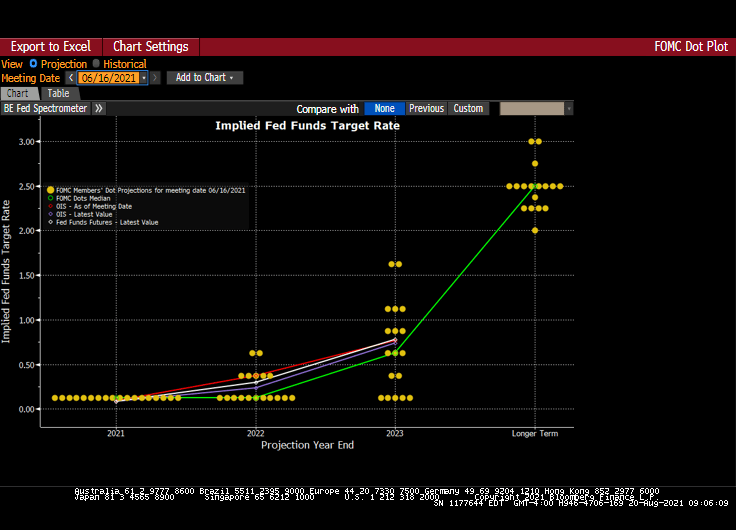

And The Fed’s Dots project also see rates rising (at least on the short-end.

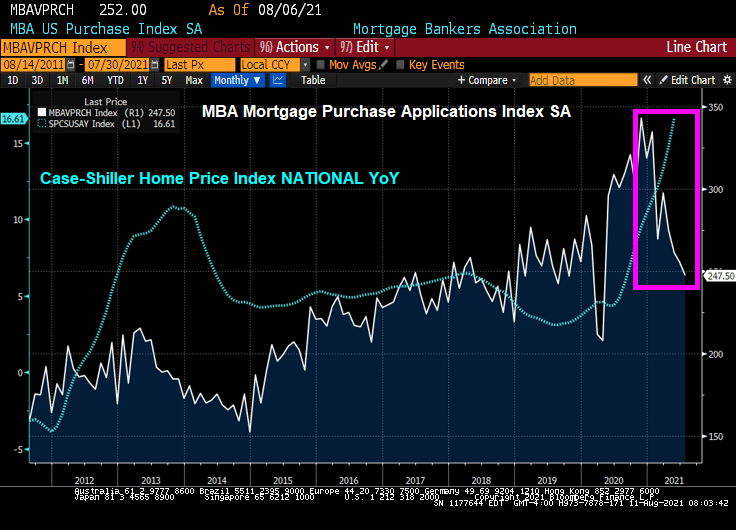

Negative real mortgage rates and blistering home price growth?

Will the attendees at the KC Fed Jackson Hole conference discuss these matters? Or will it just be a Federal Reserve Soul Shake (dance)?

You must be logged in to post a comment.