I call this “lending into the storm.”

A national mortgage lender has just introduced a 105 Loan-to-value (LTV) ratio loan and a lowering of FICO scores from 660 to 620.

Now, the loan still requires 97% LTV with downpayment assistance and gift funds permitted to boost CLTV to 105%.

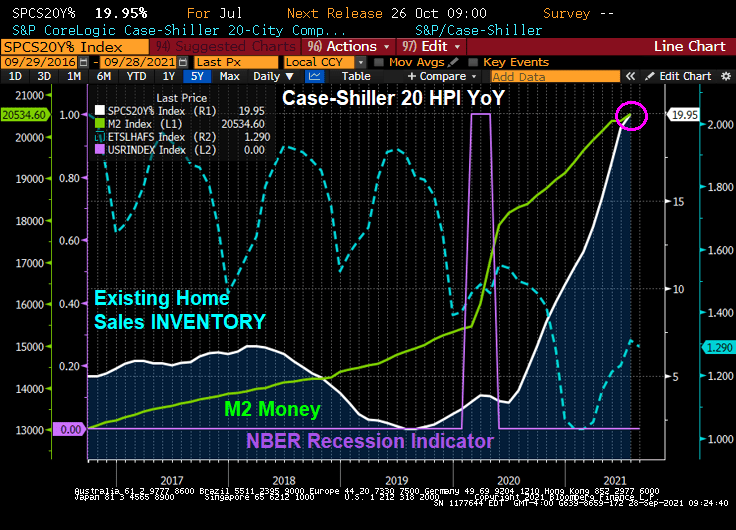

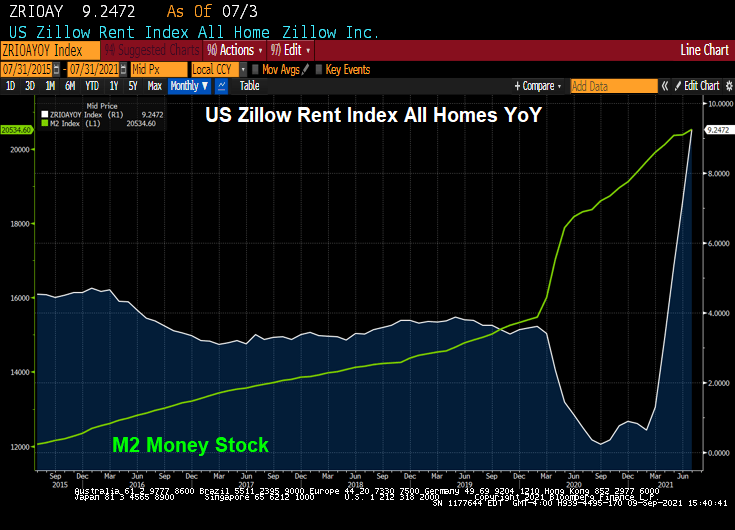

With The Fed helping to raise home prices at a whopping 20% YoY, …

lenders are trying to find loan products for lower-income households so they can get in on the bubble! Hence, a 105% CLTV mortgage product with reduced credit requirements and increased Debt-to-income requirement rising from 43% to 45%. Also, borrowers can avoid the 3% downpayment requirement and put down only $500.

This is lending into the storm: softening of underwriting requirements as the house price bubble surges. Sound like 2005. This was not supposed to happen. After the housing bubble burst and the financial crisis, The Fed was supposed to encourage counter-cyclical lending (tighten credit standards as a housing bubble worsens). Instead, lenders are lowering credit standards, feeding the house price bubble.

If this was just one lender, I would have barely noticed. But this mortgage is being offered by most banks. And then sold to our GSEs: Fannie Mae and Freddie Mac.

Government mortgage giant Fannie Mae purchases these mortgages in their 3% down programs.

Eligibility and Terms

- Desktop Underwriter® (DU®) underwriting required

- 1-unit principal residence, including eligible condos, co-ops, PUDs, and MH Advantage® (Standard manufactured housing: max. 95% LTV/CLTV)

- Fixed-rate mortgages with a maximum term of 30 years and ARMs are eligible (restrictions apply)

- Reserves (if required per DU) may be gifted

- Combined LTV up to 105% provided subordinate lien is an eligible Community Seconds® loan

- Downpayment assistance found here.

Speaking of lending into a storm, as part of the raft of new legislation designed to spur first-time homeownership in America, a remarkable bill has joined the fray: its sponsors propose creating a new subsdizied 20-year-fixed-rate mortgage program through Ginnie Mae, HousingWire reports.

According to the bill, Ginnie Mae in tandem with the Department of the Treasury would subsidize the interest rate and origination fees associated with these 20-year mortgages, so that the monthly payment would be in line with a new 30-year FHA-insured mortgage. The move – which is an explicit subsidy of one share of the population by another – could, in theory, “allow qualified homebuyers to build equity-and wealth- at twice the rate of a conventional 30-year mortgage.” Instead, what it will do is lead to is an even bigger housing bubble.

As I said, lending into a storm.

You must be logged in to post a comment.