I spoke at the American Action Forum in Washington DC on the future of government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. Speaking with me was Laurie Goodman from The Urban Institute. Laurie loves Fannie Mae and Freddie Mac and argued passionately against shutting them down. I argued to shrink their retained portfolios to zero and privatize them.

When Trump was elected President for the second time and the House of Representatives was controlled by Republicans, there was hope that Fannie Mae and Freddie Mac would be privatized. But alas, it was not to be.

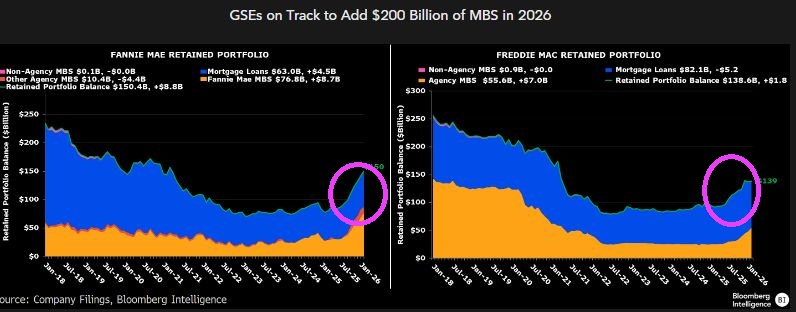

In fact, the retained portfolios for Fannie Mae (left) and Freddie Mae (right) are increasing, not decreasing.

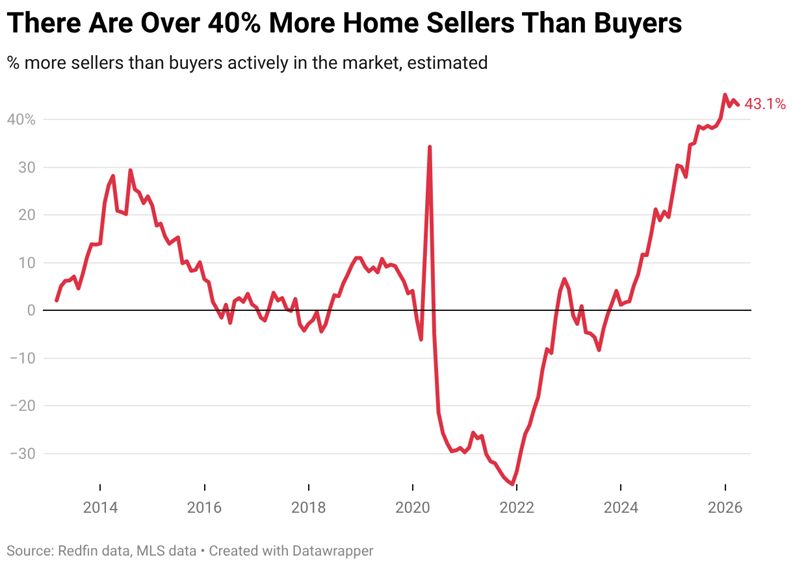

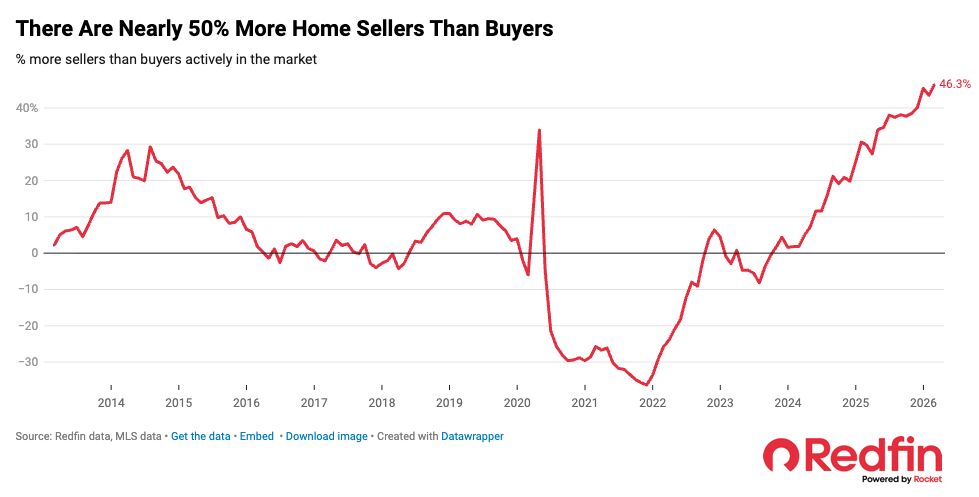

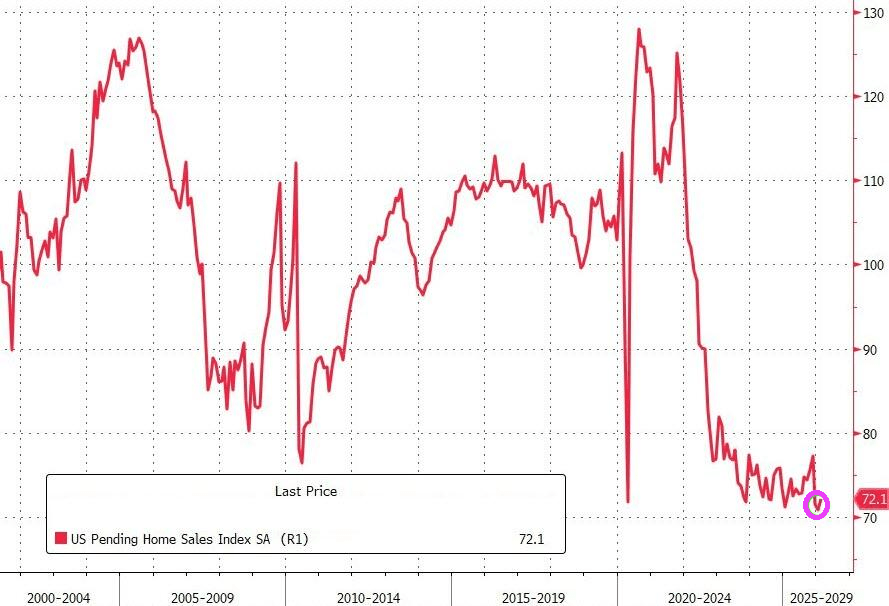

Nothing has been the same in the US housing market since the Covid outbreak of 2020. According to Redfin, there are nearly 50% more home sellers than buyers.

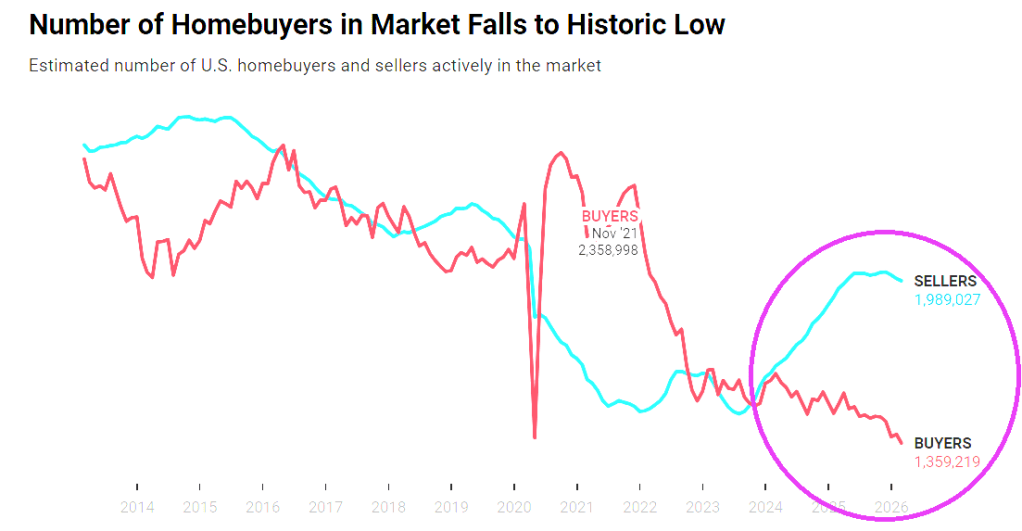

And the number of homebuyers has fallen to historic lows.

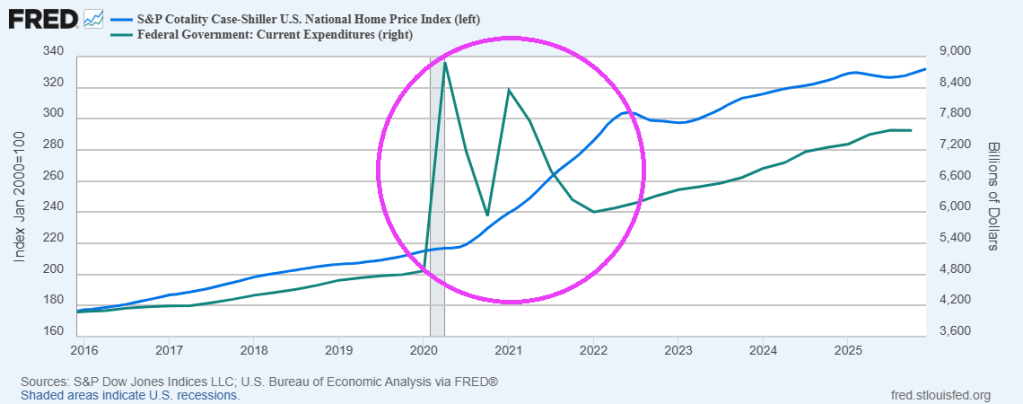

A good reason there are so few buyers is that home prices has soared after the Federal government’s spending spree after Covid.

Prayers for the soul of Noelia Castillo Ramos, murdered by the Spanish government. For being gangrape TWICE by immigrants then attempted suicide.

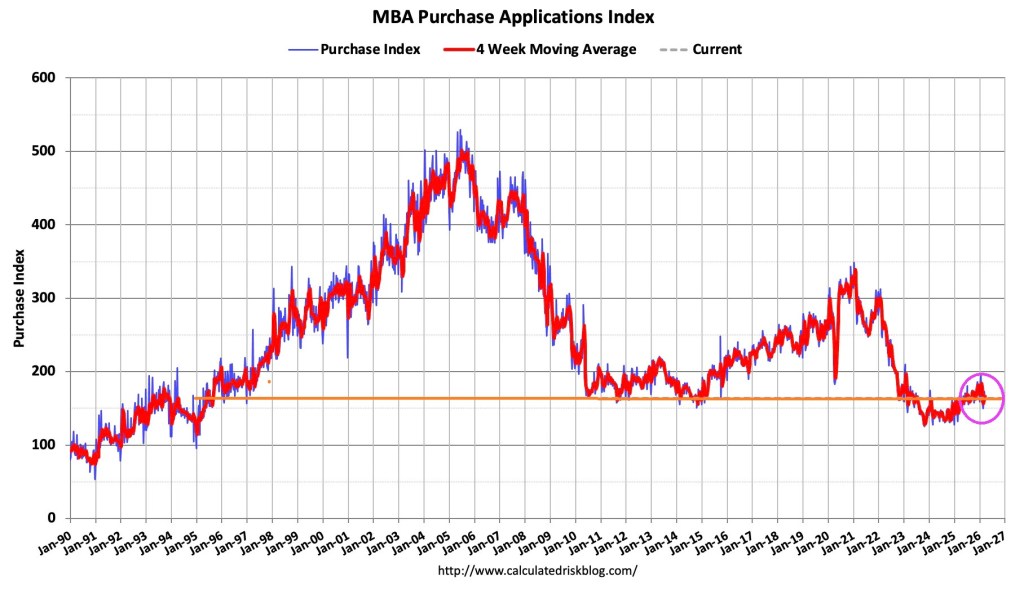

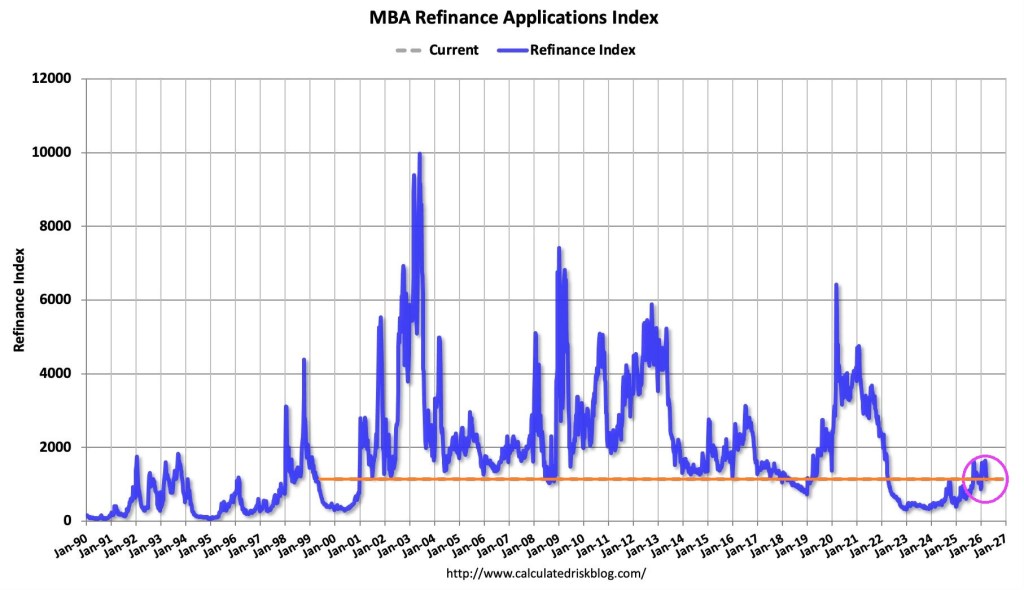

Mortgage applications decreased 10.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 20, 2026.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 10 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 5 percent higher than the same week one year ago.

The Refinance Index decreased 15 percent from the previous week and was 52 percent higher than the same week one year ago.

Nothing has been the same since Covid outbreak in 2020 and the resulting Federal government spemding spree.

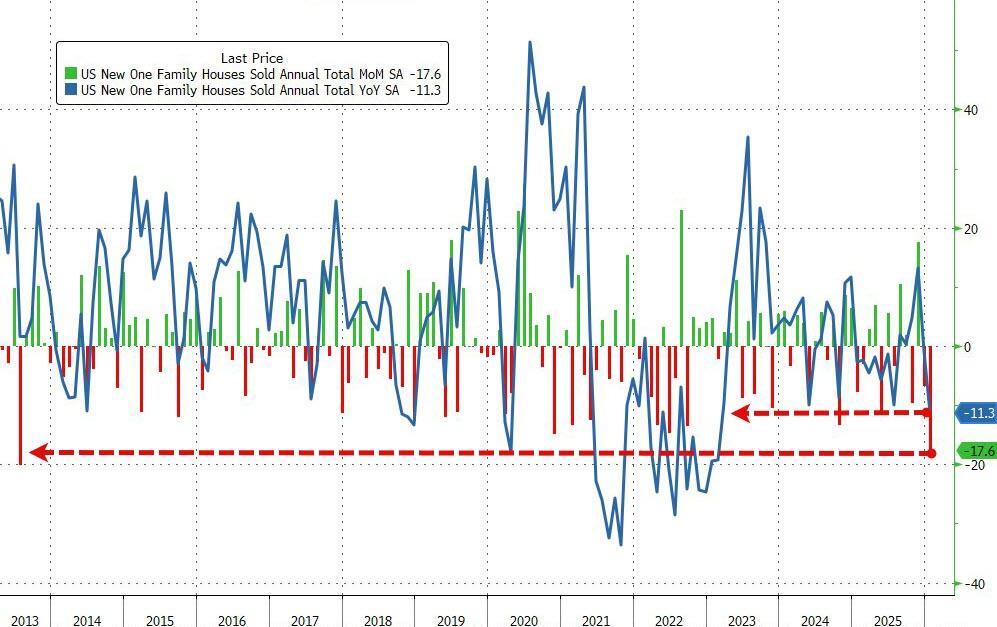

Despite falling mortgage rates, analysts expected December’s drop in new home sales to accelerate in January… and accelerate they did… crashing a stunning 17.6% MoM (-2.7% MoM exp) – the biggest MoM drop since July 2013.

This huge MoM drop dragged sales down 11.3% YoY – the worst slide in three years.

Source: Bloomberg

This huge drop dragged the new home sales SAAR down to its lowest since 2022, catching down to existing and pending sales…

Inventories are up (Houses for sale in Jan. rose 0.4% m/m to 476,000), prices are down (Median down 6.8% YoY at $400k – lowest since 2024)…

…and remember these deals were signed in January – meaning this is not mortgage related (some suggesting weather impact – Northeast sales down 44.7% MoM, MidWest -33.9% MoM, but the scale is immense).

Moral of the story: US home prices are too high for millions of households to afford.

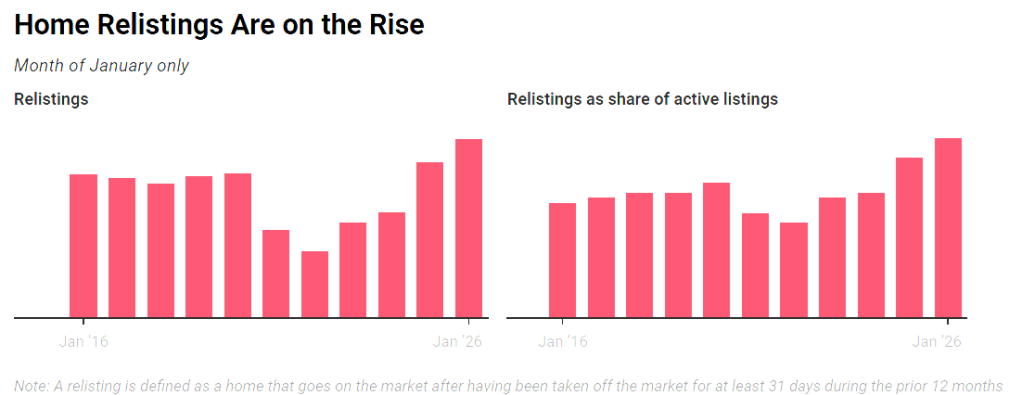

Delistings soared in 2025 after sellers began to outnumber buyers, and decided to take their homes off the market to take another bite at the apple this spring. Overall delistings hit a record high of 112,788 in December, while relistings this year represented 3.6% of all homes on the market.

Supply gains have been concentrated in the South and West, particularly among homes priced under $500,000. While the Northeast and Midwest have seen some growth, they are still lagging behind the other regions.

As of February, active listings climbed by 7.9 percent year over year, reaching 914,860 homes across the nation for sale. A little more than 7 percent of those listings resulted in contract cancellations—down slightly from the same time in 2025.

An analysis of the country’s 50 largest markets showed sharp increases in inventory in Seattle, with a 38.5 percent hike, as well as Louisville, Kentucky, 27.3 percent higher, and San Jose, with nearly 25 percent more homes on the market.

On the other side, Hartford, Connecticut, experienced the deepest drop in inventory at over 82 percent, as well as Providence, Rhode Island, at 61.1 percent.

Overall, homes spent a median of 70 days on the market in February, four days longer than a year earlier.

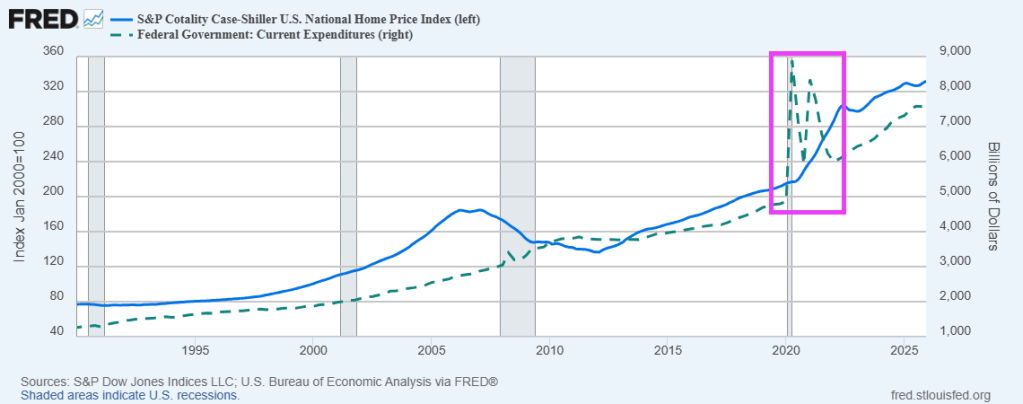

We are seeing the aftermath of the Federal government’s fiscal response to the Covid outbreak of 2020. Home prices exploded following The Federal government’s spending spree. The end result? US housing is simply unaffordable for millions of households.

Not really surprising given the soaring home prices following the Covid Federal spending spree.

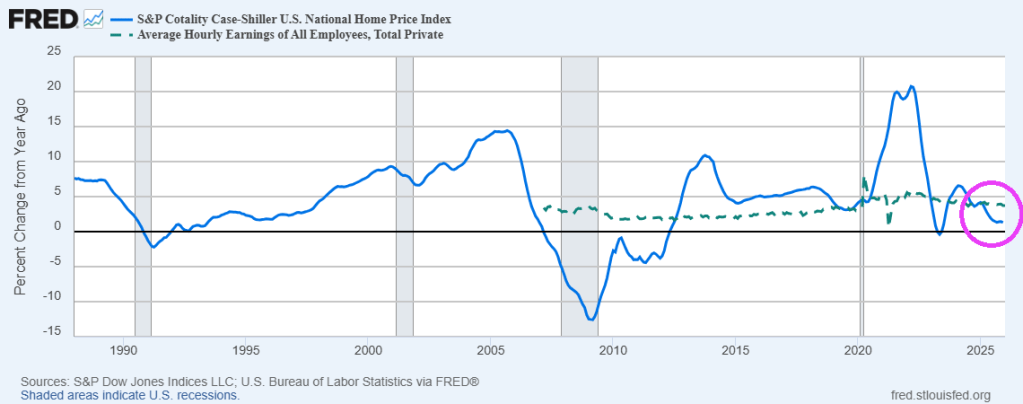

The S&P Cotality Case-Shiller U.S. National Home Price NSA Index posted a 1.3% annual gain (YoY) for December 2025, down from a 1.4% rise in the previous month. Average hourly earnings now at 3.73% YoY, higher than home price growth.

Home price growth exploded following The Federal governments’ Covid-related spending splurge.

Geographic divergence widened sharply: Chicago and New York led all markets with gains above 5%, while Tampa, Phoenix, Dallas, and Miami posted the steepest declines among markets that finished the year in negative territory.

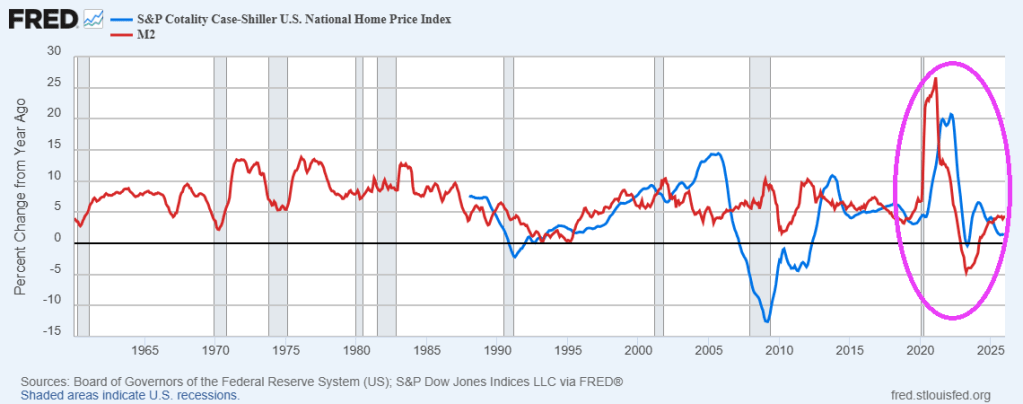

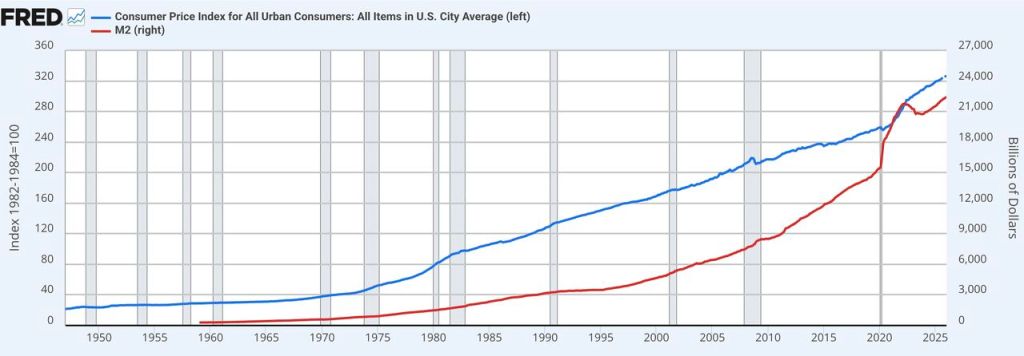

Inflation cooled significantly under Trump, but The Fed keeps printing M2!

{kind=link}

{kind=link}

You must be logged in to post a comment.