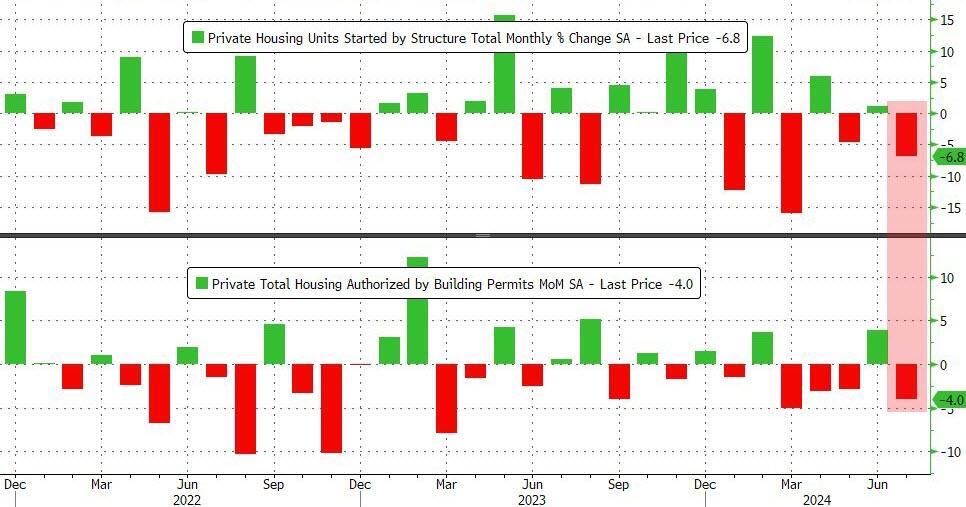

Another bad housing report for July, this time its housing starts.

Housing starts declined in July to the lowest level since the Covid economic lockdowns.

Housing starts fell -6.8% in July.

On a YoY basis, housing starts fell -14.8% YoY.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

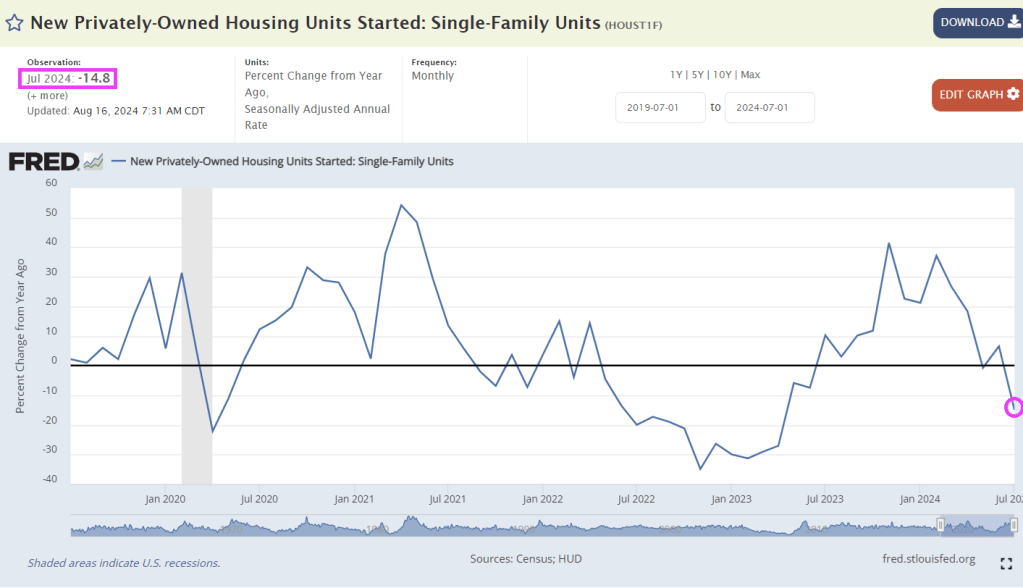

Another bad housing report for July, this time its housing starts.

Housing starts declined in July to the lowest level since the Covid economic lockdowns.

Housing starts fell -6.8% in July.

On a YoY basis, housing starts fell -14.8% YoY.

Is this The Big Short, CMBS style?

The delinquency rate on commercial mortgage-backed securities (CMBS) for offices spiked to 8.1% in July, the highest in 11 years.

The delinquency rate of office CMBS loans has QUADRUPLED in 1.5 years.

Delinquencies are currently rising at a faster pace than during the 2008 Financial Crisis.

A top AAA-rated CMBS experienced a $40 million loss in May for the first time since the 2008 Financial Crisis.

While not an office, Edward Hopper painted some great real estate properties!

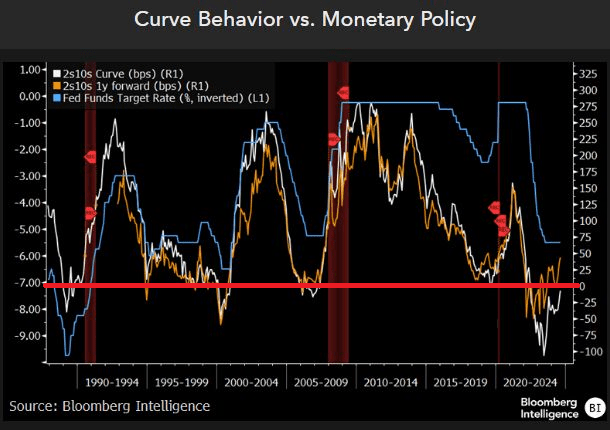

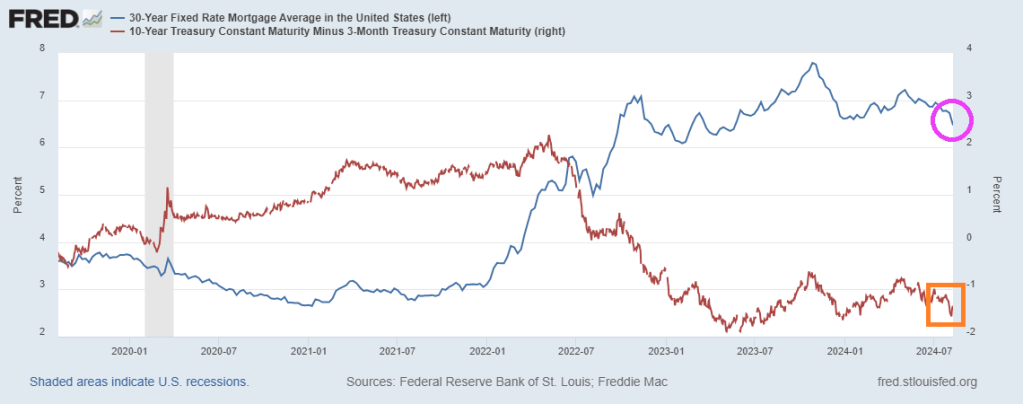

We know several things about the yield curve. First, it goes negative before recessions. Second, it is related to the inverse of The Fed’s target rate (blue line).

How about the US mortgage rate? Generally, US Mortgage rates are inverse to the 10Y-3M yield curve, but lately the US mortgage rate (pink circle) have declined with the 10Y-3M yield curve.

The yield curve does forecast recessions, but is unreliable in forecasting mortgage rate movements.

The slowing US economy has a silver lining: Treasury and mortgage rates are declining. And the is spurring faster mortgage prepayments.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending August 2, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 0.3 percent compared with the previous week and was 11 percent lower than the same week one year ago.

The Refinance Index increased 16 percent from the previous week and was 59 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.55 percent from 6.82 percent, with points decreasing to 0.58 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The deciine in rates led to an increase in MBS convexity.

Watch out! Mortgage convexity continues to rise!

Meanwhile, Kamala “The Kommie” Harris laughs.

The wheels are coming off Bidenomics. Code for corporate welfare and massive government spending. Coupled with misguided and burdensome regulations, we got gut wrenching inflation.

The result? A disastrous stock market showing yesterday.

What has Biden/Harris’ economic agenda wrought? Record high personal debt and record low savings rates.

Mortgage applications decreased 3.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending July 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Note the decline in mortgage purchase demand after Biden/Harris were sworn into office in Janaury 2021.

The Refinance Index decreased 7 percent from the previous week and was 32 percent higher than the same week one year ago. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) remained unchanged at 6.82 percent, with points increasing to 0.62 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Because of rising rates under Biden/Harris economic policies, mortgage refinancing demand has gotten crushed.

We are in the latter half of the year, so seasonalility will kill off purchase mortgage demand compared to the Spring and early Summer.

What’s it going to be? Mortgage rate increases or balance sheet (MBS) reductions?

Since the Covid outbreak in early 2020, The Fed went wild with rate cuts and massive and unpredented balance sheet expansion.

Let’s look at The Fed’s puchase of agency MBS and mortgage rates. From 2020 2022, The Fed continued to buy agency MBS. But in 2022, all hell broke loose as The Fed went crazy RAISING rates, but slowly began unwinding their balance sheet. The result? Mortgage rates began to climb. In fact, the US conforming mortgage rate for 30 years has risen 102% since early 2022. The Fed is only slowing unwinding their MBS holdings.

Despite the struggles in the residential housing market, the COMMERCIAL mortgage market is a trainwreck.

What will The Fed do?? After all, nothing from nothing beats nothing.

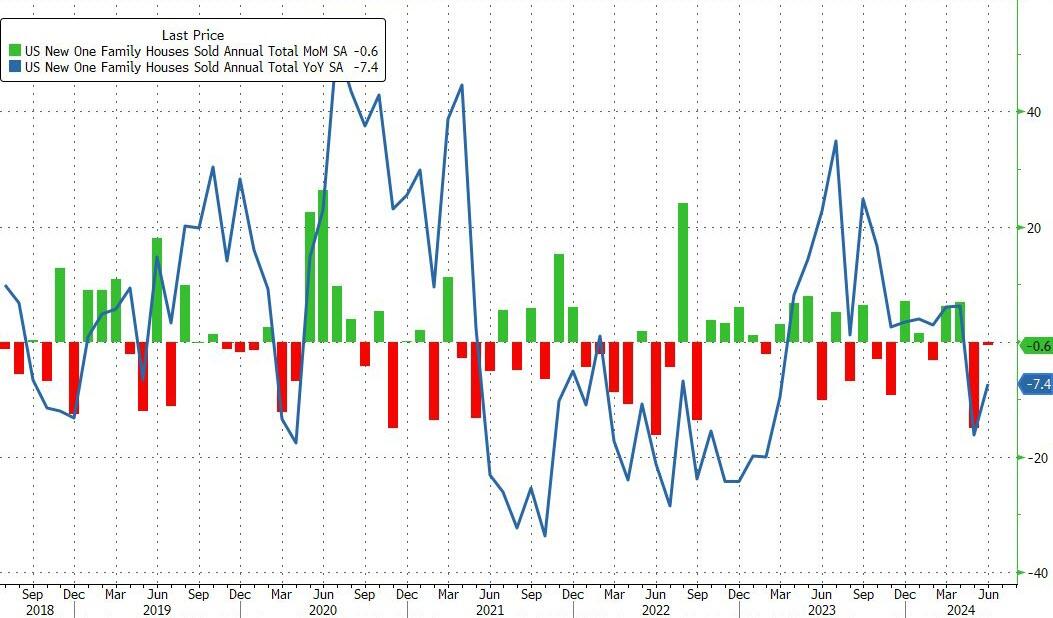

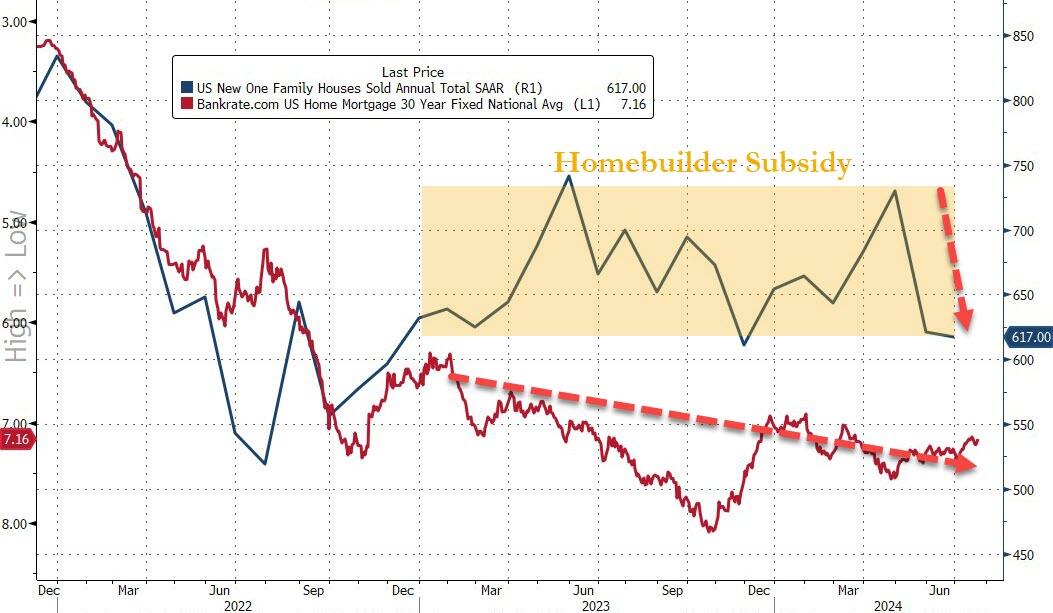

After a disappointing dump in existing home sales in June, new home sales just confirmed the slowdown, dropping 0.6% MoM (notably below the 3.4% MoM expected) and also saw a major downward revision in May from -11.3% MoM to -14.9% MoM. That leaves new home sales down 7.4% YoY…

That shift dragged the new home sales SAAR down to 617k – basically unchanged since 2016…

While the median new home price rose in June, it remains below the median existing home price…

It appears the homebuilder subsidy fad is wearing off as mortgage rates show no signs of easing significantly…

Of course, none of this should be a surprise as homebuyer confidence has collapsed to an all-time record low…

Will cutting rates help?

Probably not. Bidenomics is now called Harrisnomics (or Cacklenomics) since Harris as VP was the tiereaker in the US Senate. So, she holds some responsibility for the outrageous, wasteful spending in Washington DC.

Nothing from nothing should be the slogan of Bidenomics.

Conference board’s leading economic indicators remains negative YoY at -4.8.

Worried? What if I told you that the promises of unfunded entitlements from the Federal government now exceeed the TOTAL national assets of the US??

Way to go, Joe! But he had plenty of help from Congress.

President Biden was expected yesterday to propose a cap of 5% on annual rent increases for tenants of major apartment landlords, and he did. Whether it can happen is something else.

As the White House communicated on Tuesday, the administration is looking for Congress to pass legislation for landlords with more than 50 units in their portfolios, that being the proxy for institutional owners, although it would also affect private investors, family offices, and others that might own at least that many units. According to administration calculations, the total pool would cover 20 million rental units.

The law would then give landlords a choice. They could either restrict annual rent increases to no more than 5% a year or they would forfeit the ability to take fast depreciation of rental housing. There would be an exception for new construction or “substantial renovation or rehabilitation.”

So, Biden is dusting off the old Jane Fonda/Tom Hayden Santa Monica, CA rent control scheme.

I am guesing that this will not pass the House, but will probably pass in the Confederacy of Dunces: the US Senate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.