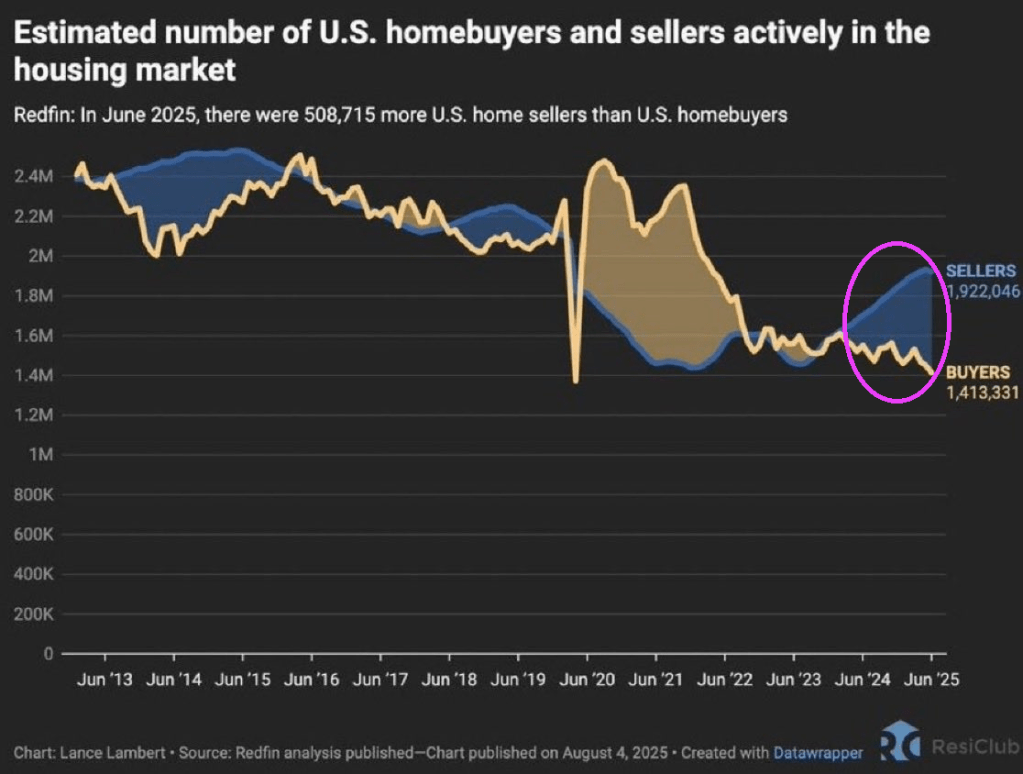

The US housing market is in a pickle. Home sellers now outnumber buyers by more than 500,000, the largest gap ever recorded.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

The US housing market is in a pickle. Home sellers now outnumber buyers by more than 500,000, the largest gap ever recorded.

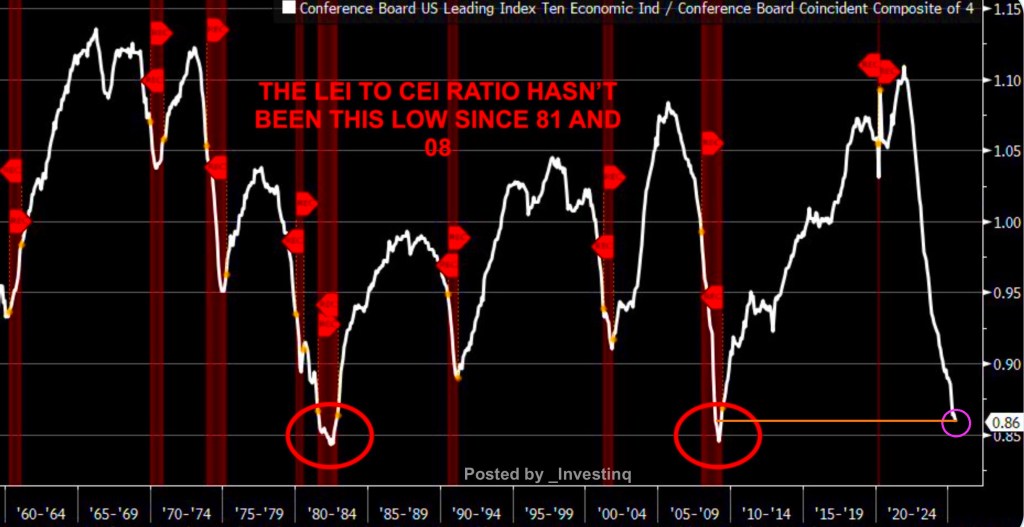

The Fed will have to whip it good with rate cuts if the recession warnings are an indicator of what lies ahead for the US economy.

The ratio of The Conference Board’s Leading Economic Indicators (LEI) vs. The Conference Board’s Coincident Economic Index (CEI) ratio hasn’t been this low since 2008.

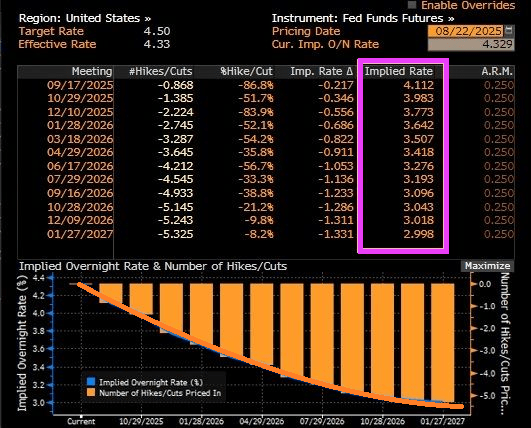

Fed Funds Futures are signalling rate cuts at the September 17th FOMC meeting and December 10th meetings.

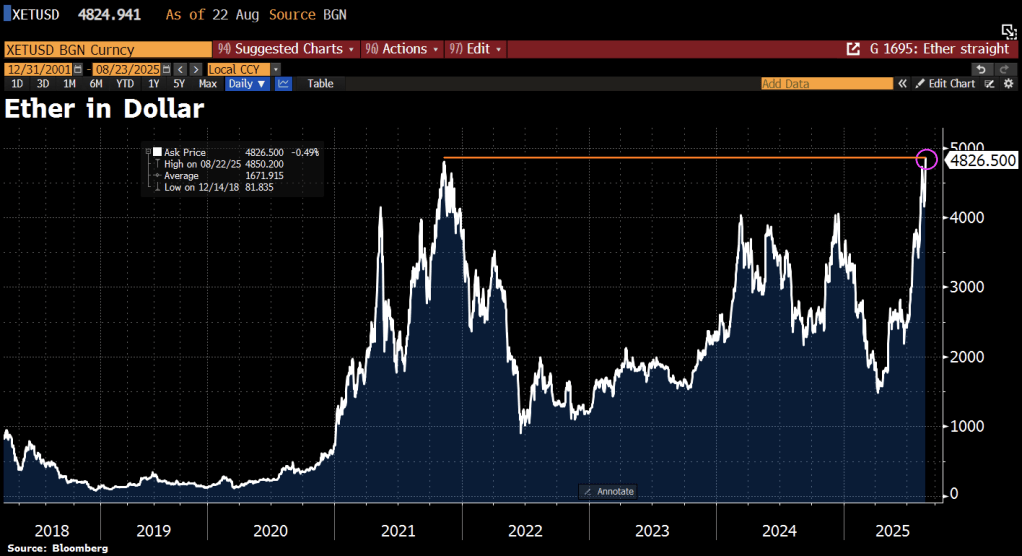

On the crypto front, Ethereum is soaring.

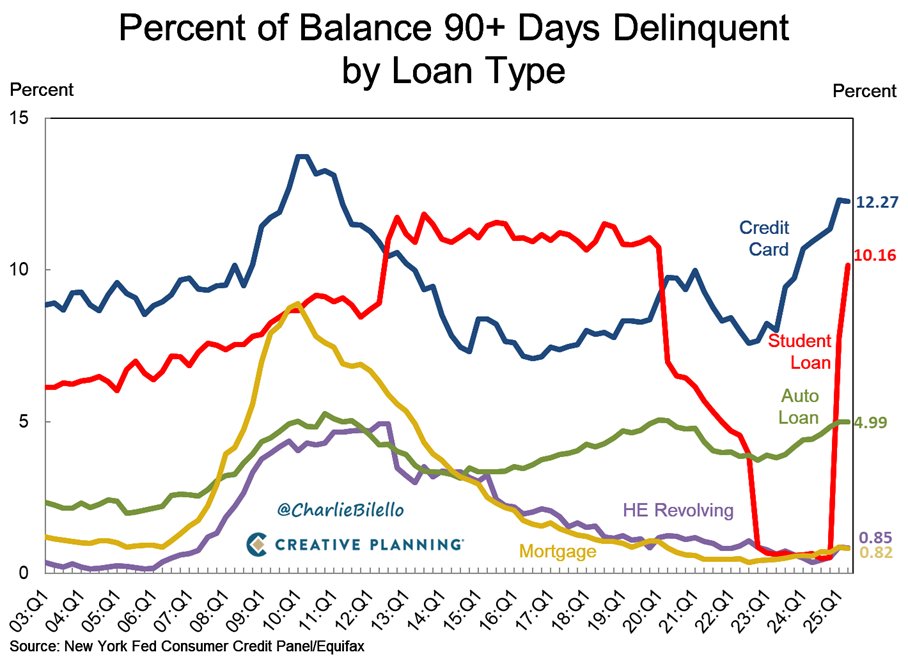

Debt stress is mounting!

Finally, US government debt growth (YoY) was approximately equal to US nominal GDP growth in Q1 2025.

Unfortunately, the BBB (Big Beautiful Bill) is projected to add $3.9 trillion of debt. Unfortunately, there are insufficient spending cuts in the BBB. And the Senate just nixed kicking illegal immigrants off of Federal healthcare programs.

Unfortunately, GDP growth is only expected to be modest with debt growth once again rising faster than GDP growth. As Diane Feinstein once said, politicians are elected to spend money. This, of course, was a ridiculous statement embraced by spend-crazy Democrats and RINOs.

So, Congress has committed American taxpayers to debt slavery.

Should President Trump fire Fed Chair Jerome Powell and replace his with someone else like Treasury Secretary Scott Bessent? The answer is … YES!

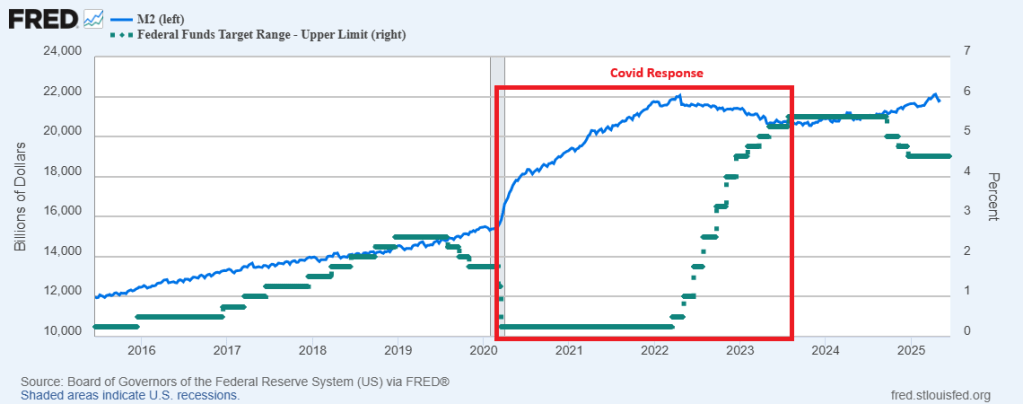

Why? First, there was a massive response to the Covid outbreak in 2020. And the monetary stimulus (aka, stimulypto) has never been removed.

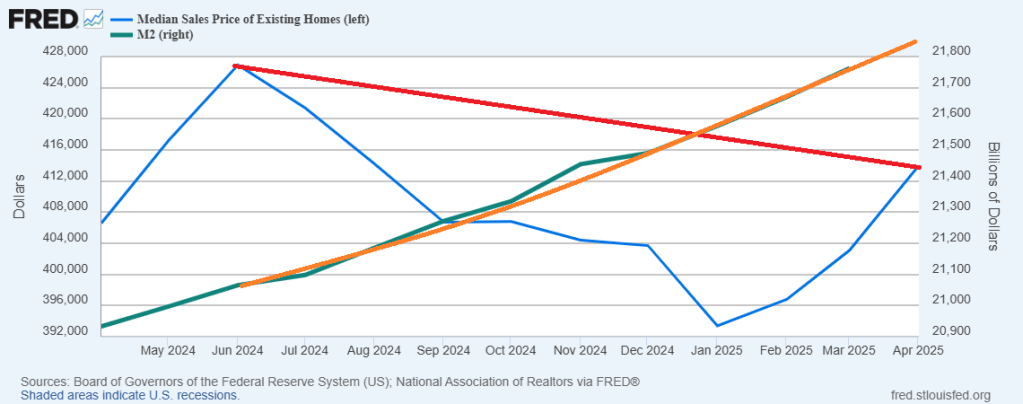

The Fed Funds Target Rate (upper bound) remains high at 4.50% and M2 Money supply is $21.8 TRILLION.

Second, The Fed could help reduce the interest paid on the massive Federal debt load when the debt if refinanced.

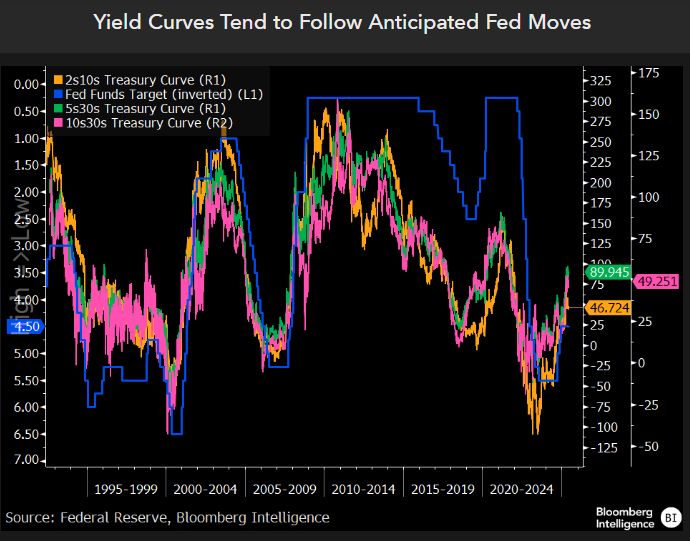

The US Treasury yield curve tends to follow anticipated Fed moves.

Of course, The Fed should be abolished. But a step in the right direction would be to fire “Foul Powell” who is on the prowl.

Fed Chair Jerome Powell.

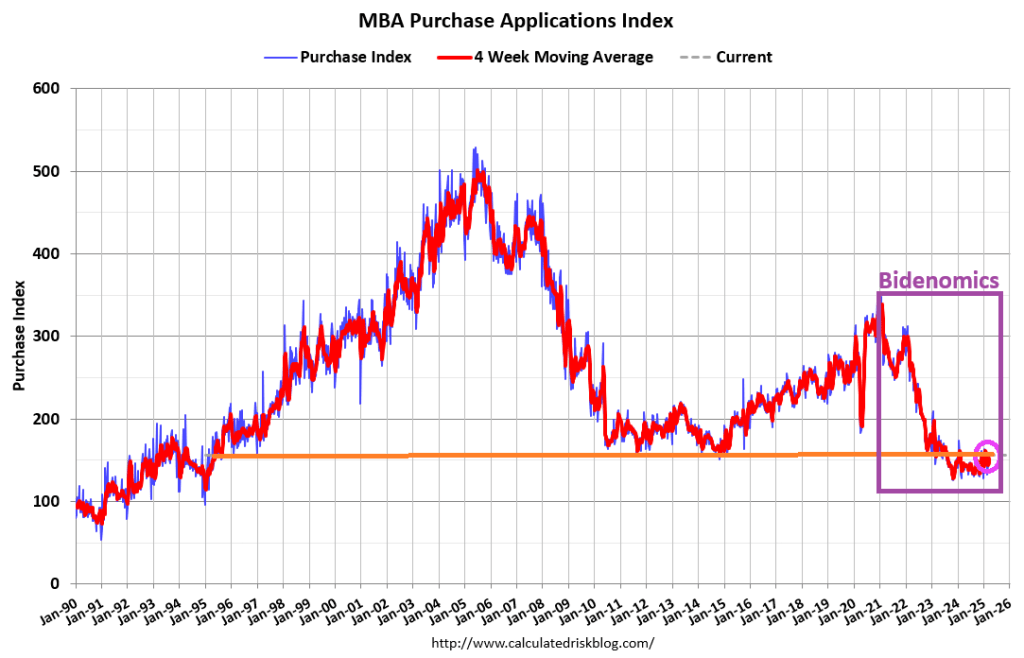

Mortgage applications decreased 3.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 30, 2025. This week’s results included an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 15 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 15 percent compared with the previous week and was 18 percent higher than the same week one year ago.

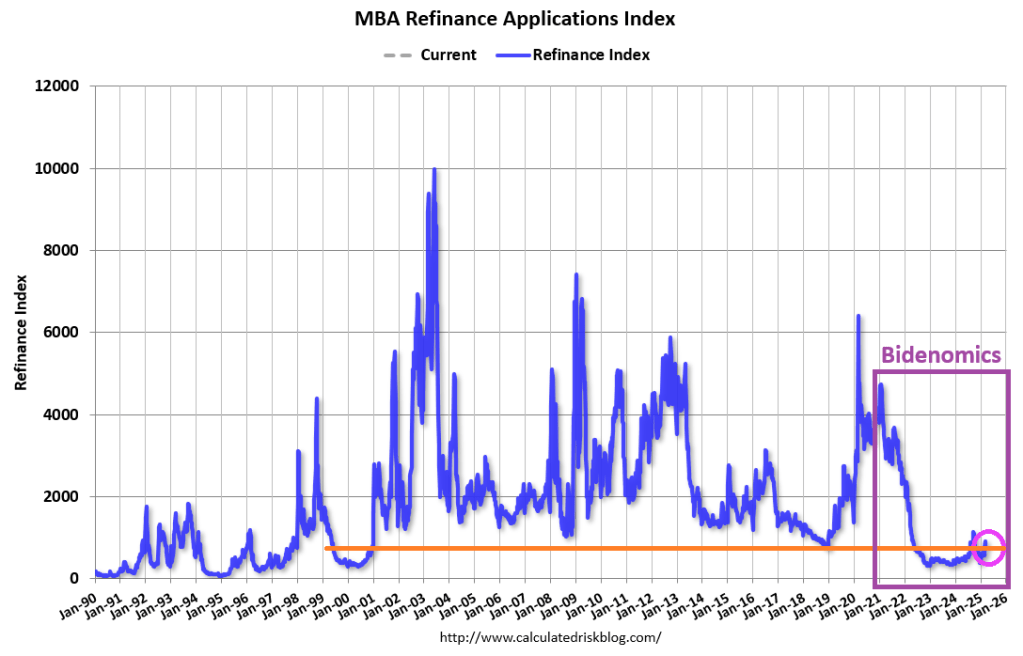

The Refinance Index decreased 4 percent from the previous week and was 42 percent higher than the same week one year ago.

Most mortgage rates moved lower last week, with the 30-year fixed rate declining to 6.92 percent and staying in the 6.8 to 7 percent range since April.

Biden/Harris/Yellen’s gross economic mismanagement reminds me of the song “Into The Mystic.” Because it requires a mystic to determine WHO was running the Biden/Harris adminstration and using the autopen.

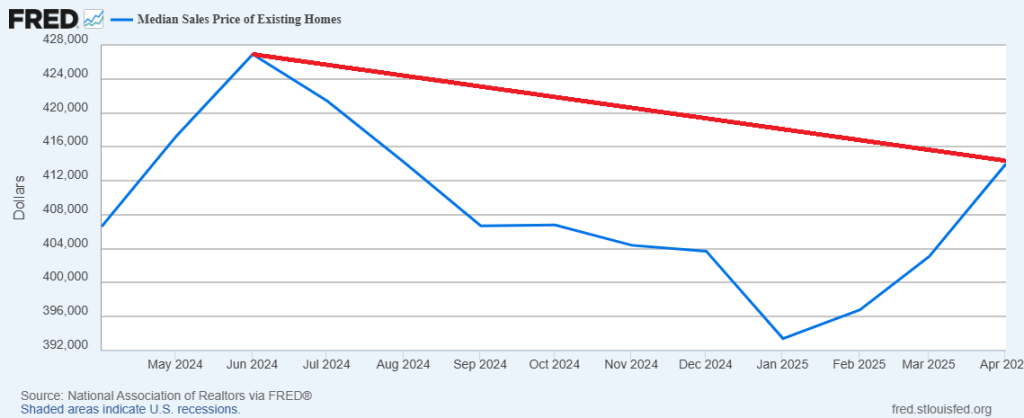

US existing home sales dropped 0.5% MoM in April (considerably worse than the +2.0% MoM rise expected), dropping to just 4.00MM sales SAAR, with sales down 3.1% from a year earlier on an unadjusted basis.

This is the weakest April sales pace since April 2009.

And median price of EHS is rising and is on pace to top 2024’s high.

And with M2 Money printing like a bat out of hell.

Now you know why Trump is so eager to cut wasteful spending! The real mystery is why Democrats and RINOs are so determined to continue wasteful spending and not cut taxes.

Trump inherited a fiscal disaster from Biden and Congress. Not to mention The Federal Reserve. Credit default swaps (CDS) for the USA are near Greece (and China) levels.

Since Covid struck in 2020, US debt is up a staggering 56%!

And M2 Money is up 40% since Covid.

Opa! Our country is on fire!

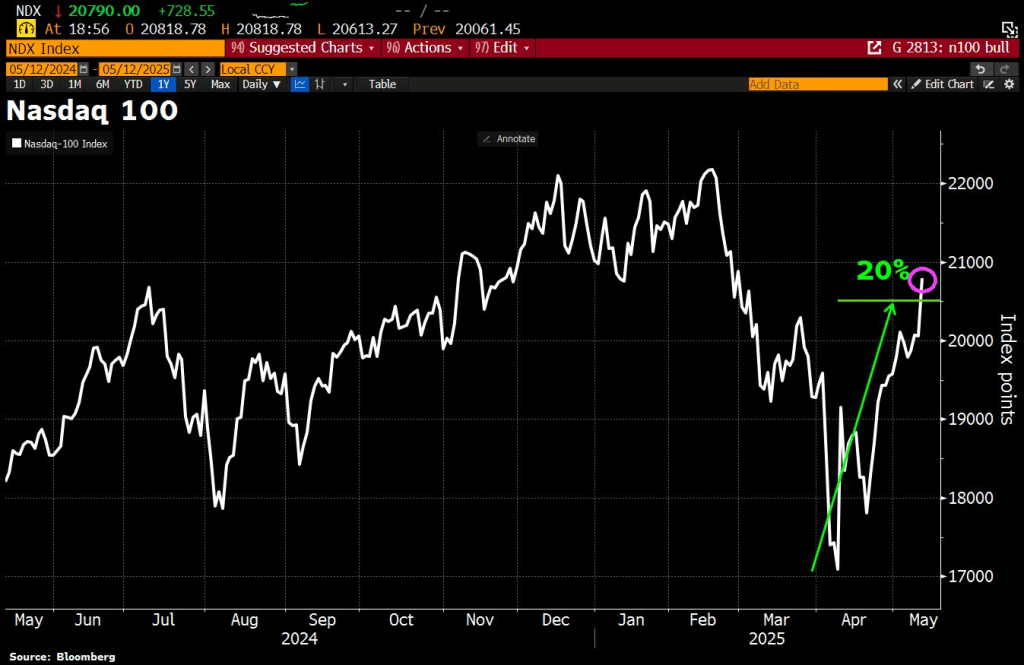

Well, U.S. and China reached an agreement to lower tariffs in a 90-day cool-off period. Despite China claiming they would NEVER agree to tariffs! The result? The NASDAQ 100 rose to its highest level since mid-February.

So much for the MSNBC/CNN doomsayers.

Washington DC is loaded with good ol’ boys. Willing to cut deals with anyone for a slice of financial pie. Like “10% For The Big Guy” Joe Biden.

Money flowing into Treasury funds hit its highest since 2017, by far.

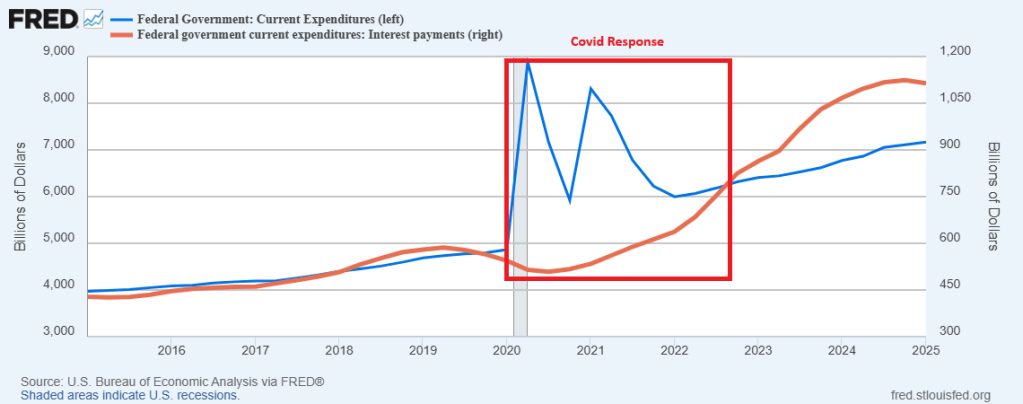

And with the massive expansion of The Fed’s balance sheet with a) the financial crisis and b) Covid crisis, The Fed still has a staggering amount of bonds on its balance sheet, making it vulnerable to interest rate increases.

Like what has happened in 2023 and 2024 under Biden. A fine mess!

Sail away. We are all prisoners of the theft by DC politicians.

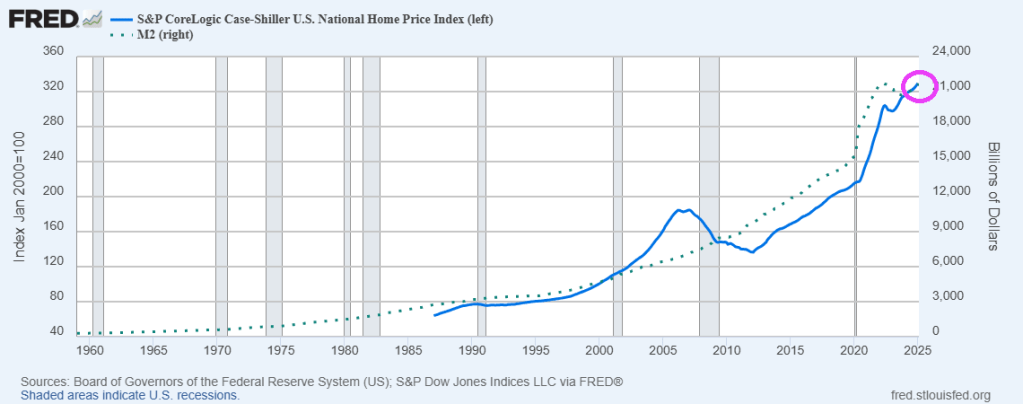

The Fed keeps on printing money M2! The Case-Shiller National home price index is up 4.1% since last year YoY as The Fed continues to print money.

Mortgage applications decreased 2.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 21, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 7 percent higher than the same week one year ago.

The Refinance Index decreased 5 percent from the previous week and was 63 percent higher than the same week one year ago.

You must be logged in to post a comment.