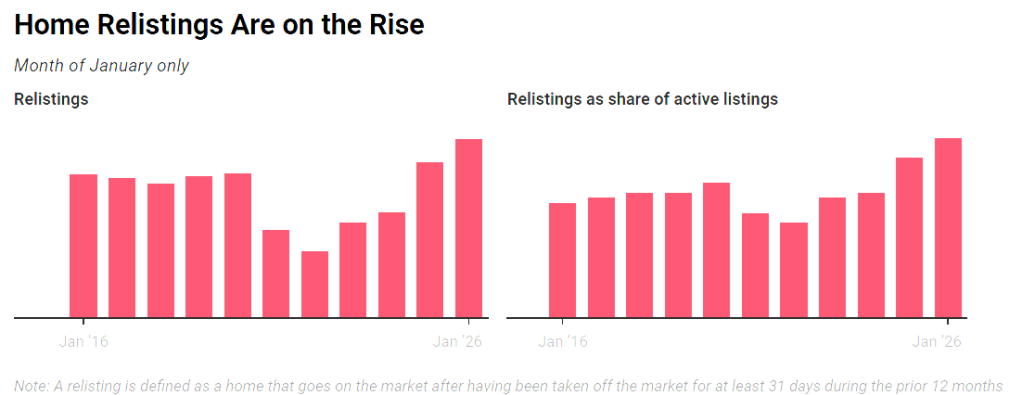

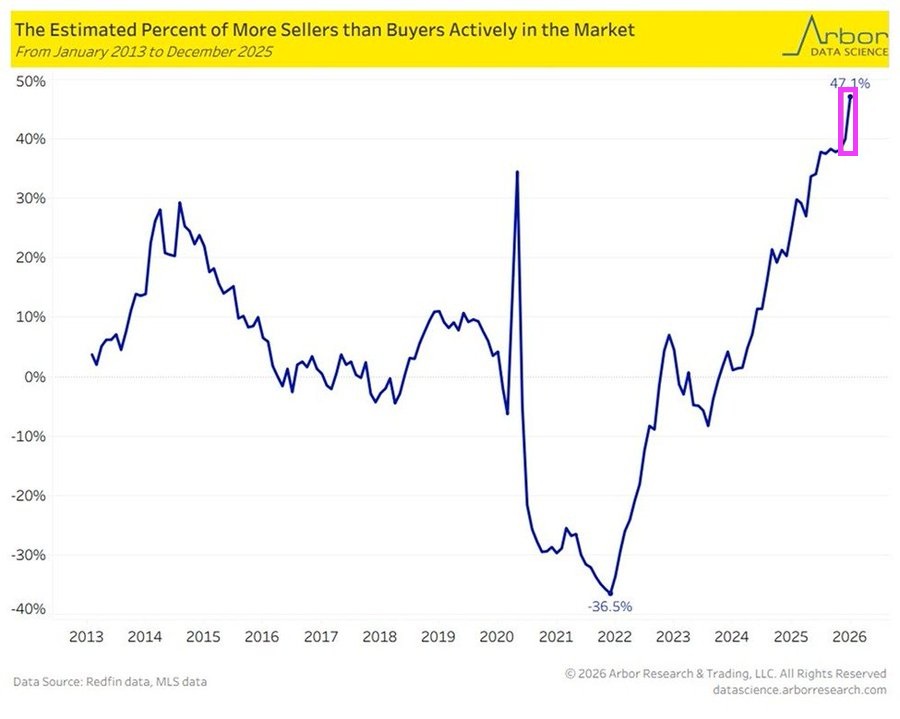

Delistings soared in 2025 after sellers began to outnumber buyers, and decided to take their homes off the market to take another bite at the apple this spring. Overall delistings hit a record high of 112,788 in December, while relistings this year represented 3.6% of all homes on the market.

Supply gains have been concentrated in the South and West, particularly among homes priced under $500,000. While the Northeast and Midwest have seen some growth, they are still lagging behind the other regions.

As of February, active listings climbed by 7.9 percent year over year, reaching 914,860 homes across the nation for sale. A little more than 7 percent of those listings resulted in contract cancellations—down slightly from the same time in 2025.

An analysis of the country’s 50 largest markets showed sharp increases in inventory in Seattle, with a 38.5 percent hike, as well as Louisville, Kentucky, 27.3 percent higher, and San Jose, with nearly 25 percent more homes on the market.

On the other side, Hartford, Connecticut, experienced the deepest drop in inventory at over 82 percent, as well as Providence, Rhode Island, at 61.1 percent.

Overall, homes spent a median of 70 days on the market in February, four days longer than a year earlier.

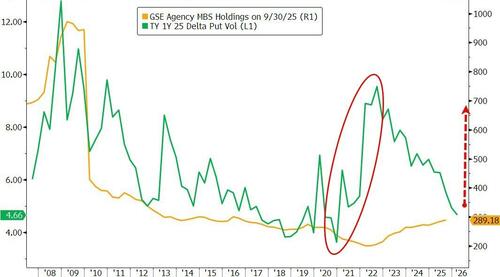

President Trump ordered Fannie Mae and Freddie Mac to operate like The Federal Reserve. Buying assets to manipulate interest rates. In this case, F&F have been ordered to buy $200 billion of agency MBS.

Thursday’s Truth Social post triggered an immediate snap tighter in mortgages, led by the belly and lower coupons. By pulling MBS spreads tighter and crowding out real-money buyers, Fannie and Freddie’s purchases would push incremental demand into Treasuries as the next-best duration substitute, putting a modest bid under the belly of the curve.

However, execution and the ultimate size of purchases is still unclear, as my colleague Alyce Andres noted. If the government-sponsored enterprises GSEs stagger purchases, and signal an ultimate increase above the announces $200 billion, further tightening should occur. They can fund a lot of the buys from existing liquidity portfolios, though there’s a path where they could issue short-term debt to preserve operating buffers and could nudge repo wider at the margin.

The bigger transmission channel is hedging, as highlighted by colleagues Ira Jersey and Will Hoffman. Unlike the Fed, the GSEs actively hedge MBS holdings, shedding duration by paying fixed rates in swaps and using swaptions to manage the negative convexity and vega risks embedded in mortgages. That matters for swap spreads and for volatility, especially in the belly.

That’s why GSE MBS purchases don’t have to be huge to change the feel in rate markets. The post-Global Financial Crisis regime dulled the classic convexity feedback loop because the Fed held such a large amount of agency MBS and didn’t hedge it, while the GSEs shrank their portfolios. Trump’s directive risks bringing more of that regime back.

A recent note out of Goldman Sachs frames it cleanly: A $200 billion build could lift the active convexity-hedger footprint by about 25%. The street then starts front-running the mechanical flows — paying in selloffs, receiving in rallies — which makes breakouts more likely even if day-to-day ranges look calm, Goldman added.

Positioning makes the setup more precarious. JPMorgan already saw mortgage valuations as a “bit snug” before the announcement, while BofA flagged that rates market had recently added fresh belly shorts sitting against a backdrop of benchmark funds still overweight MBS versus IG.

That mix can keep the initial tightening sticky, but it also raises the odds of sharp reversals if the market decides the purchasing flows are slower, smaller, or more heavily hedged than hoped.

Fannie and Freddie’s retained portfolio are soaring along with the duration gap.

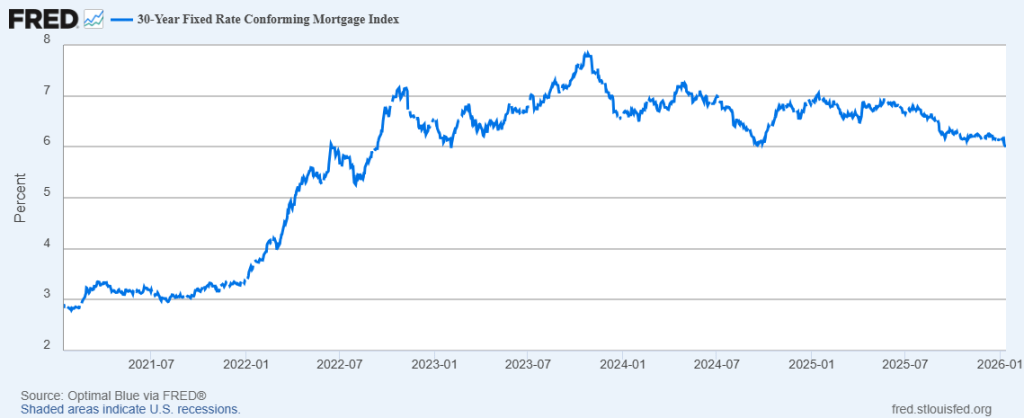

The effect on mortgage rates has so far has been negligible. The 30-year conforming mortgage just fell below 6% at 5.99%.

Mortgage demand is recovering slowly from Biden-era mismanagement. Rising mortgage rates coupled with rising home prices made housing affordability get flushed down the toilet.

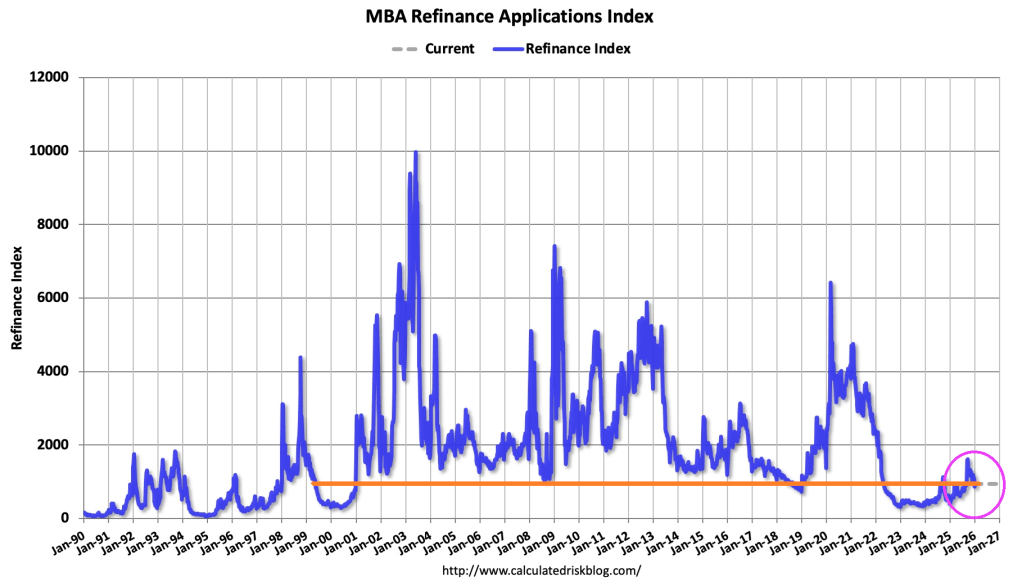

Mortgage applications decreased 9.7 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 2, 2026. The results include an adjustment for the holidays.

The Market Composite Index, a measure of mortgage loan application volume, decreased 9.7 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 28 percent compared with two weeks ago. The unadjusted Refinance Index decreased 31 percent from two weeks ago and was 108 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from two weeks earlier. The unadjusted Purchase Index decreased 23 percent compared with two weeks ago and was 10 percent higher than the same week one year ago.

The holiday adjusted Refinance Index decreased 14 percent from two weeks ago and was 133 percent higher than the same week one year ago.

This is the opposite of the housing bubble from The Big Short where home prices in Phoenix, Las Vegas, Los Angeles and Florida rose then crashed. Instead, the fastest growing cities are in the northeast and midwest.

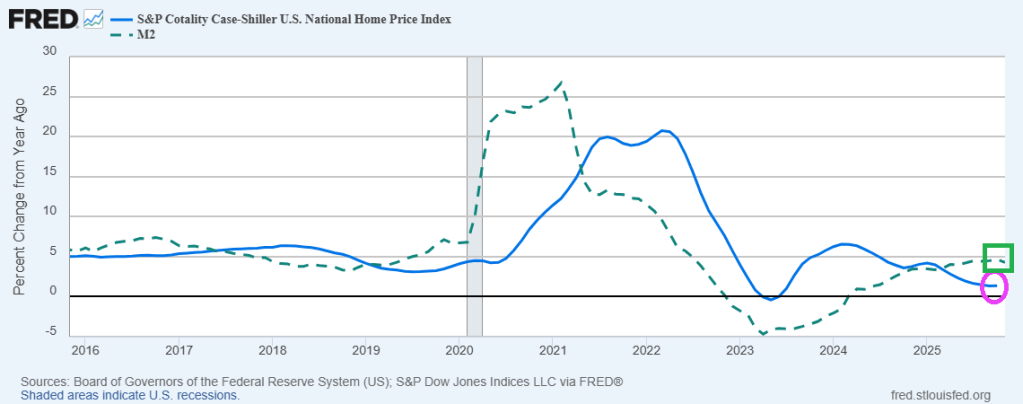

The Case-Shiller 20-City Home Price Index rose 1.3% year over year in October 2025, easing from a 1.4% increase in September and coming in slightly above market expectations of a 1.1% gain. This represents the smallest annual increase since July 2023, reinforcing signs that the US housing market is settling into a much slower growth phase. Home price appreciation continues to trail consumer inflation. With October CPI estimated at around 3.1%, inflation-adjusted home values appear to have edged modestly lower over the past year.

Regional data point to a pronounced geographic rotation. Chicago now leads all major markets with a 5.8% annual gain, followed by New York at 5.0% and Cleveland at 4.1%. In contrast, Tampa recorded a 4.2% decline, the steepest among the 20 cities, and its 12th consecutive month of falling annual prices. Other former pandemic boom markets, especially in the Sun Belt, are seeing the sharpest declines, led by Phoenix (-1.5%), Dallas (-1.5%), and Miami (-1.1%).

Housing price growth has stalled even though M2 money growth is higher YoY.

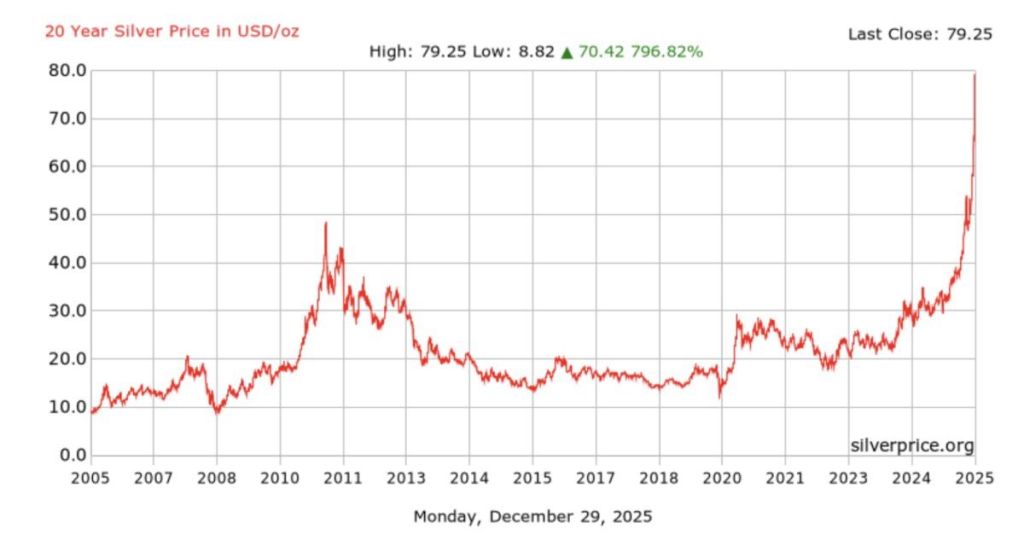

On the silver front, silver regained losses yesterday, but increased margin requirements are causing losses again.

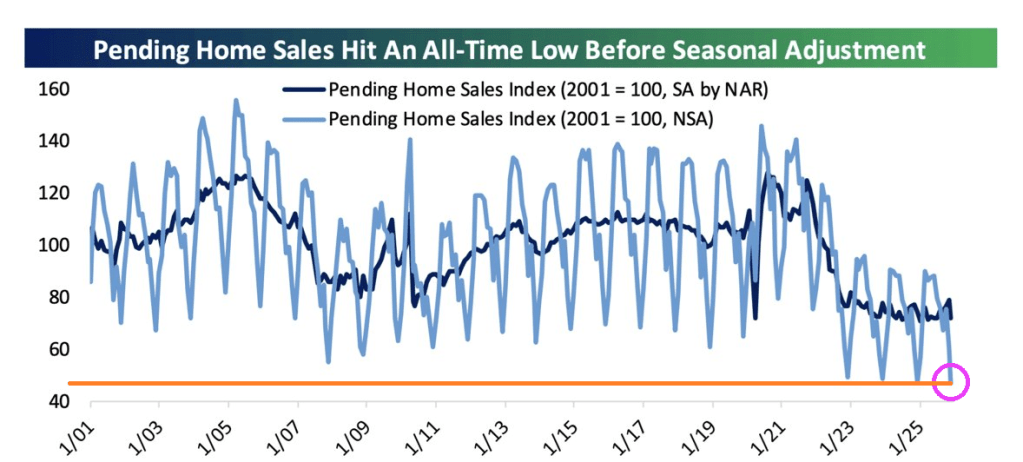

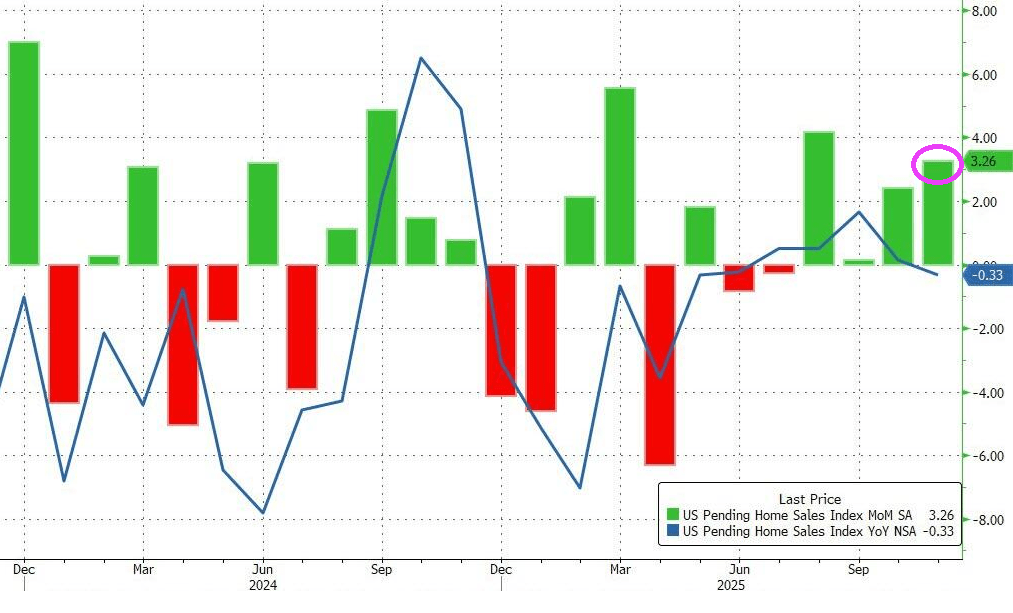

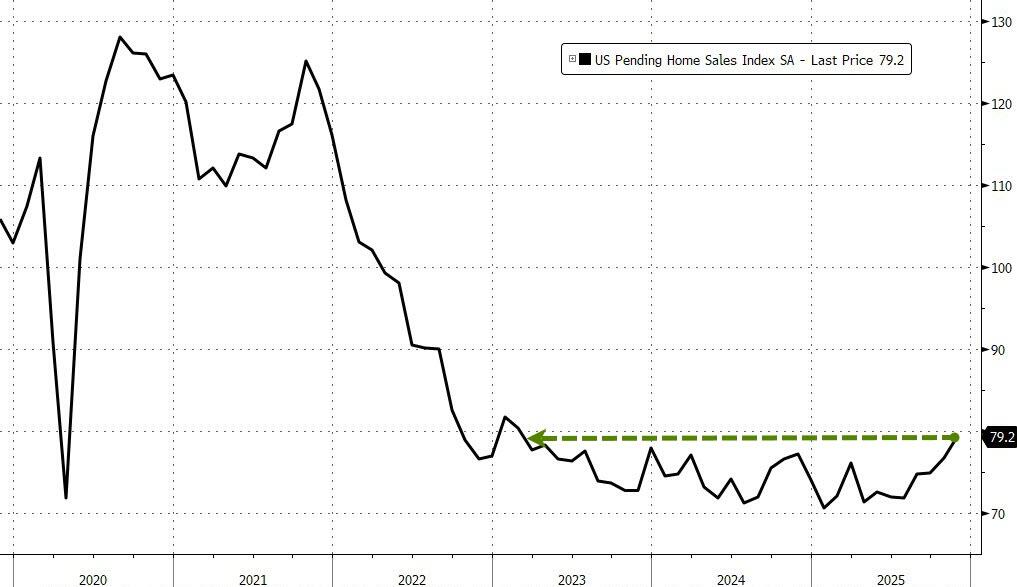

Pending sales of existing homes in the US surged 3.3% MoM (more than the expected 0.9% MoM move) in November as a modest improvement in prices and mortgage rates encouraged buyers.

The gain was broad-based across regions and exceeded all but one estimate in a Bloomberg survey of economists, but left the YoY change in sales somewhat stagnant on an NSA basis.

Signings have now increased for four straight months, matching a streak seen during the frenzied housing market of the pandemic.

The trade association’s report on Monday showed contract signings rose in each US region last month to their highest levels of the year. The West posted the largest increase, followed by the South, the nation’s largest home-selling region.

November’s surge dragged the Pending Home Sales Index to its highest since Feb 2023…

Bloomberg reports that the recent data point to the gradual improvement many economists see for the housing market into 2026.

Mortgage rates that were close to 7% in May have since settled in the 6.3% to 6.4% range, and home prices are growing at a much slower rate compared to last year.

That’s helped fuel small gains in contract closings in recent months. However, economists and industry experts have widely different expectations for next year.

In a recent survey of nine market analysts, estimates for the home resale market ranged from 1.7% to 14% sales growth, with the rosiest projection coming from NAR’s Yun.

Pending-homes sales tend to be a leading indicator for previously owned homes, as houses typically go under contract a month or two before they’re sold.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.