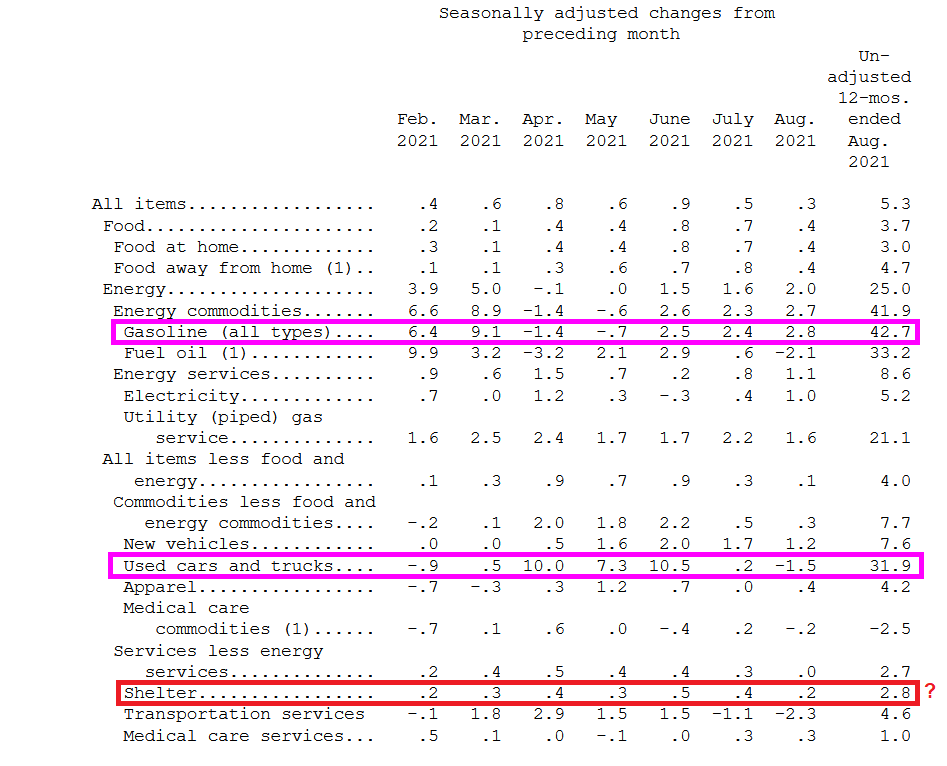

US inflation remained about the same in August as it was in July. CPI YoY fell ever so slightly from 5.4% in July to 5.3% in August. Real hourly earnings remain negative.

The source of consumer inflation? Gasoline prices rose 42.7% YoY while used cars and trucks rose 31.9% YoY.

Shelter rose 2.8% YoY. That is odd since the Case-Shiller national price index is growing at a torrid 18.61% YoY pace and the Zillow Rent Index YoY has recovered to a sizzling 9.24% YoY pace.

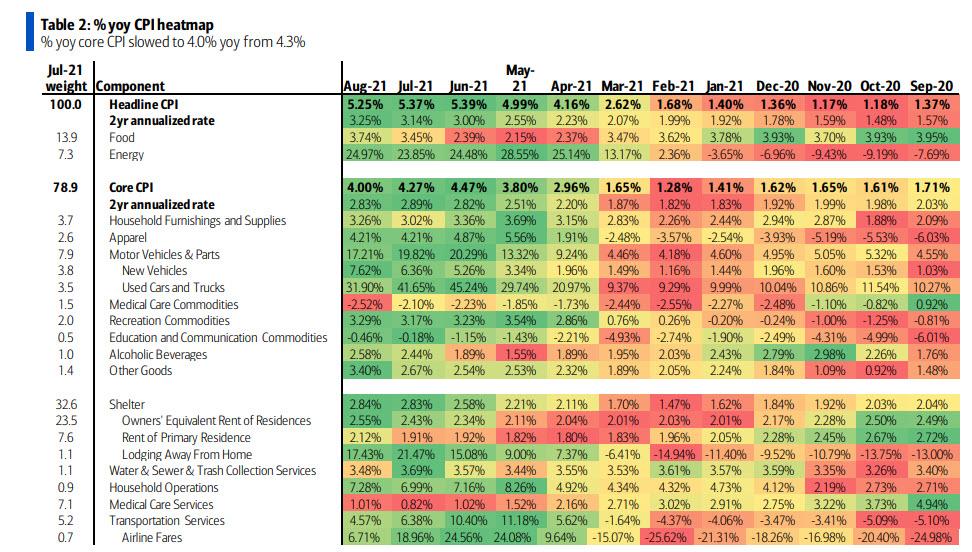

The YoY heatmap of inflation.

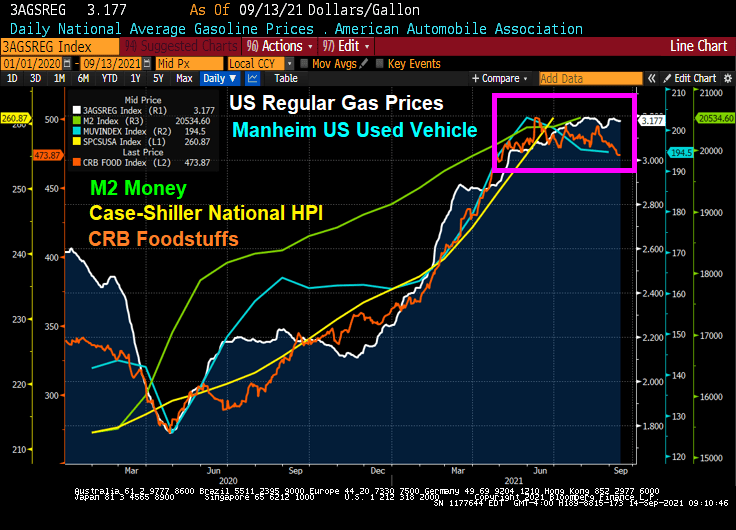

However, with the exception of home prices and rent, we are seeing a slowing of used car, foodstuffs and regular gas prices over the summer.

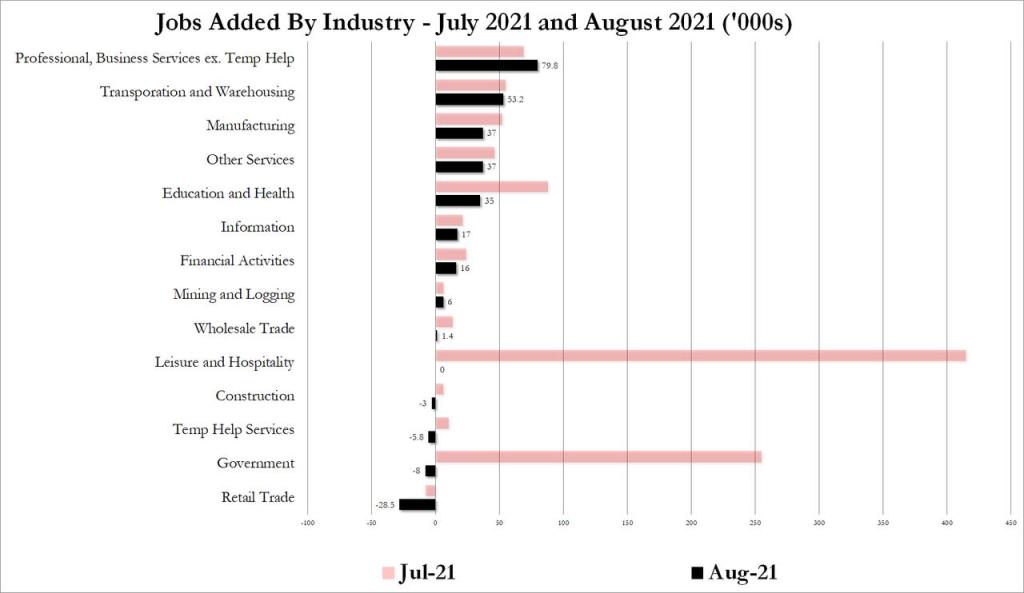

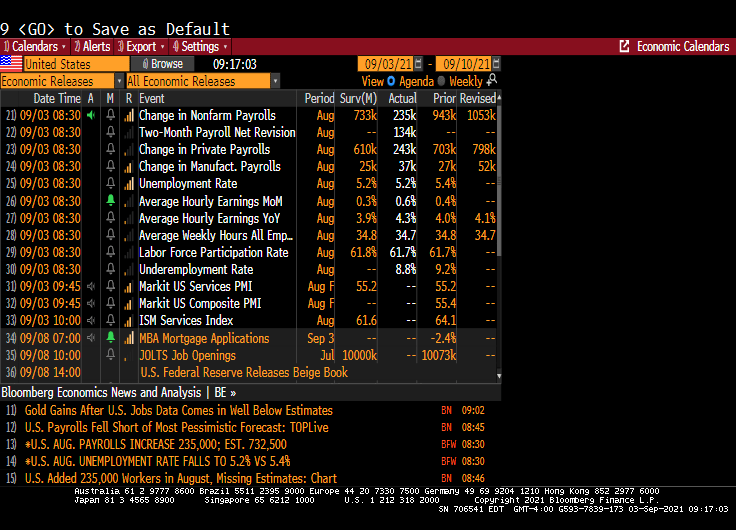

Well, after the dismal ADP print we knew that the August jobs numbers would be worse than imaginable. And they were!

A big miss on the topline job creation number — the establishment survey suggested only 235,000 jobs were created in August, versus expectations for 733,000 — has undercut what little chance there was left of a Fed announcement on tapering later this month. It should make for a very interesting debate among policy makers about forward momentum in the labor market.

The shocker was in the leisure and hospitality sector, which created zero new jobs on net in August after figures of around 400,000 in each of the previous two months. There was a dip in hiring in other service sectors too, but nowhere near as significant. That could perhaps be due to some early impact from the spread of the delta variant in recent weeks.

On the household survey, the numbers looked better. According to those figures, the unemployment rate fell to 5.2%, in line with estimates, thanks to a 509,000 increase in reported employment. That also propelled the prime working-age employment to population ratio to 78%, from 77.8% in July.

Disparities narrowed in August as well, according to prime working-age EPOP ratios by race and ethnicity. Prime working-age Black EPOP, in particular, jumped to 73% from 72.2% the month before — outpacing the rest.

Equity futures pared a modest gain after the release, with contracts on the S&P 500 Index flat as of 9:09 a.m. in New York. With wages climbing, Treasury yields rose, with those on 10-year notes rising 4 basis points to 1.33%. The Bloomberg Dollar Index was down 0.3%.

The unemployment rate dropped which a misleading headline. That simply means that more people dropped out of the labor force than were unemployed. Not a good way to lower the unemployment rate.

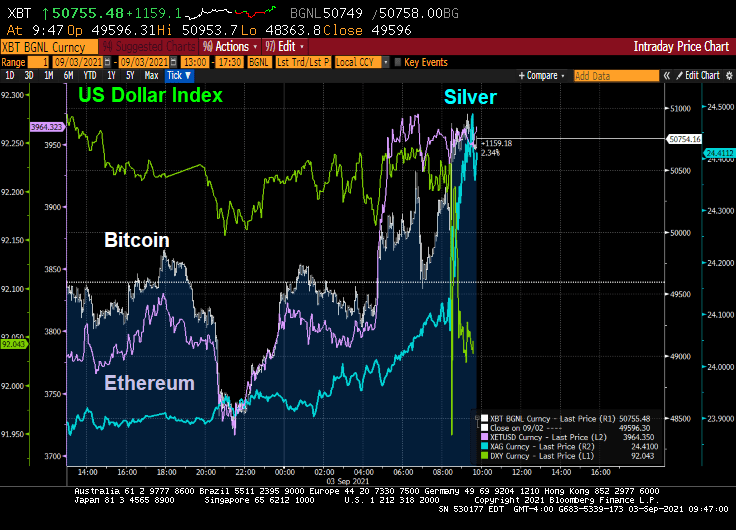

Alternative investments silver, Bitcoin and Ethereum rose on the lousy jobs report as the US Dollar dropped.

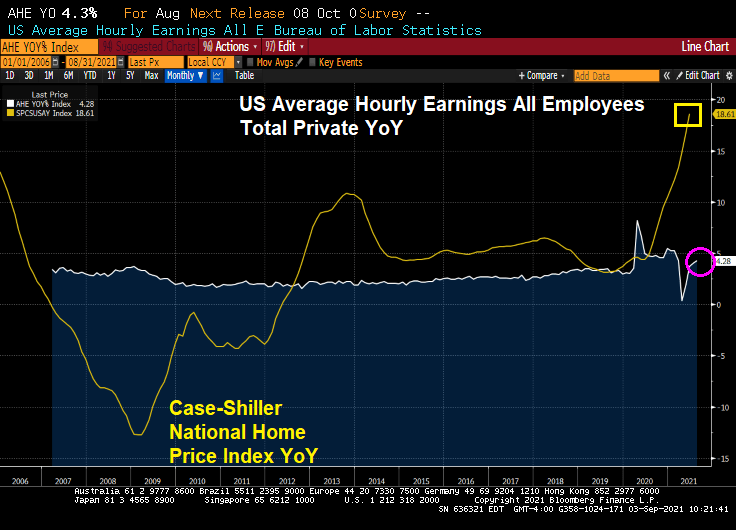

The good news? US Average Hourly Earnings All Employees Total Private YoY rose to 4.28%! The bad news? US home prices are rising at a 18.61% pace.

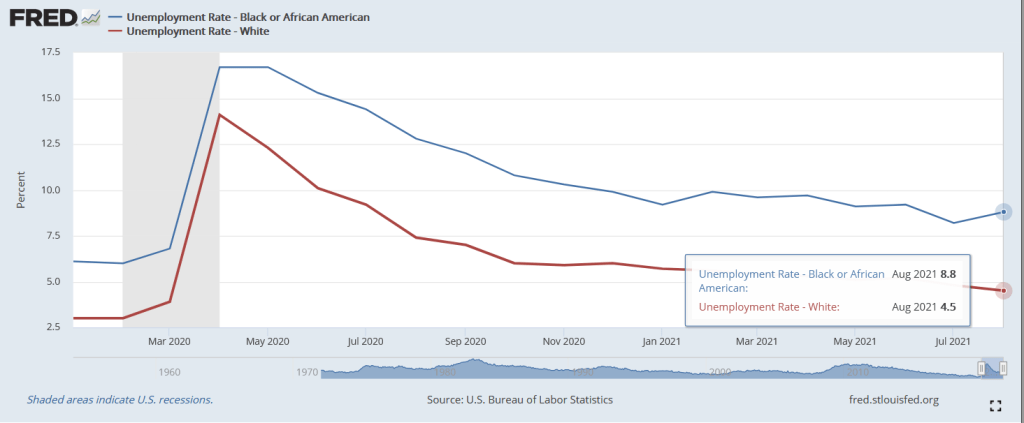

The bad news? Black unemployment rose to 8.8% in August while white unemployment fell to 4.5%. This represents a widening of the employment gap that is higher in August than pre-Covid.

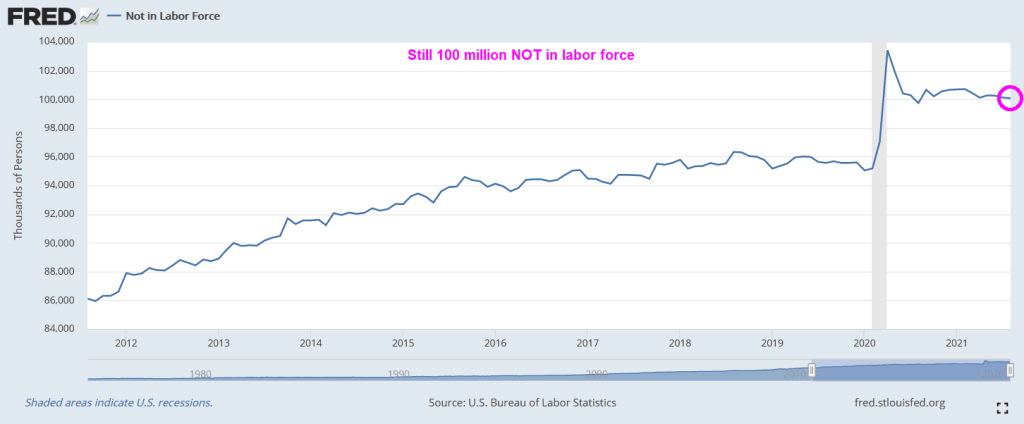

There are still over 100 million NOT in the labor force, higher than pre-Covid.

So, The Fed’s plans to begin tapering have gone up in smoke.

Home prices are now growing at 4.75x hourly earnings growth. And existing home sales inventory remains low by historic standards.

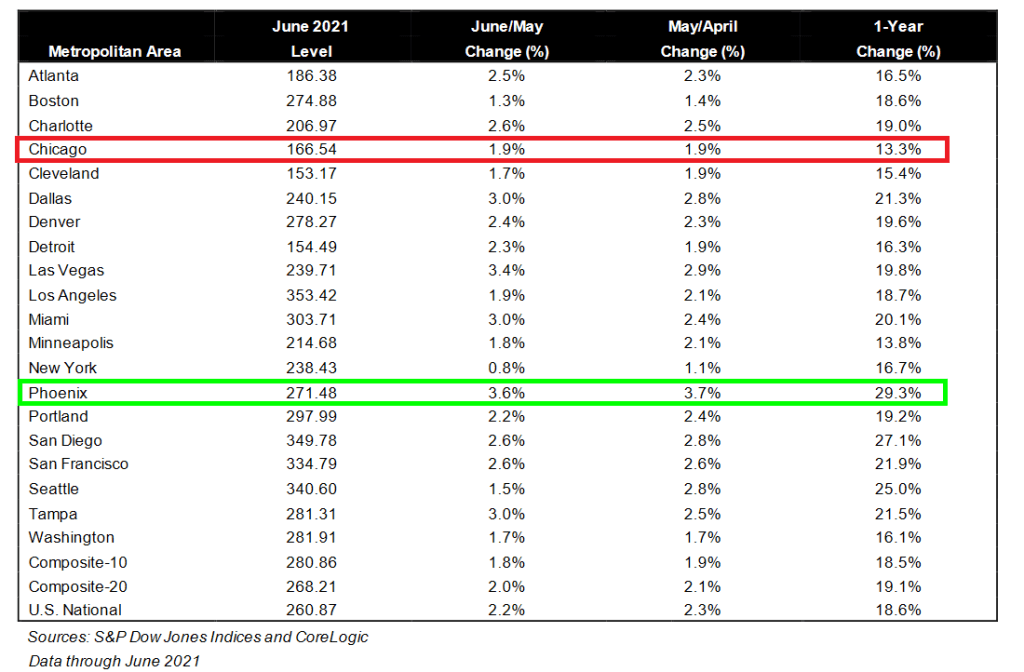

All of the Case-Shiller metro areas were above 13% with Phoenix, AZ leading at 29.3% YoY. The slowest growing metro area is Chicago, IL at 13.3%.

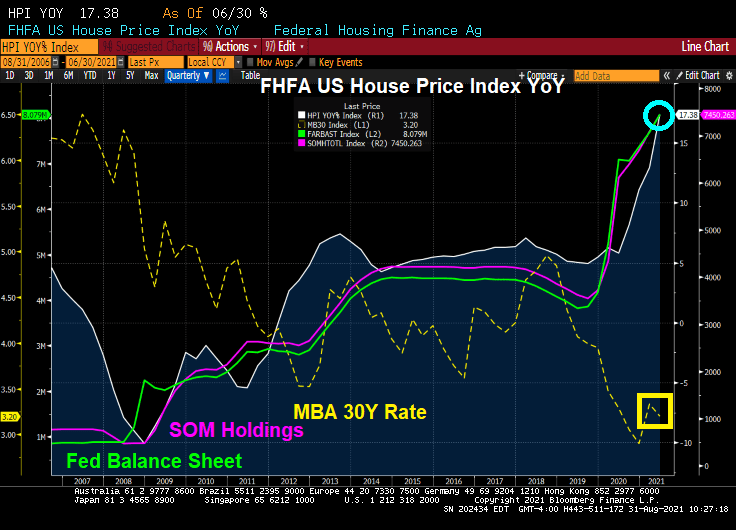

The FHFA’s house price growth hit 17.38% YoY in June. Mortgage rates being low and Fed’s Balance Sheet and The Fed’s System Open Market Holdings sky-high.

Are Fed Chair Jerome Powell and The Fed Board of Governors the Gods of Hellfire?

At the annual Jackson Hole (aka, J-Hole) Economic Symposium, Federal Reserve Chairman Jerome Powell reiterated that the Fed is in no hurry to either taper asset purchases immediately or aggressively. Additionally he made crystal clear that even when the Fed does eventually start tapering asset purchases (likely November or December), it should not be taken as signaling interest rate hikes will follow on some preset course. Indeed, Fed Chairman Powell continues to claim that inflation is transitory. Finally, he said that part of the mandate (employment) is still far from being achieved. So, expect more SNAKE JUICE.

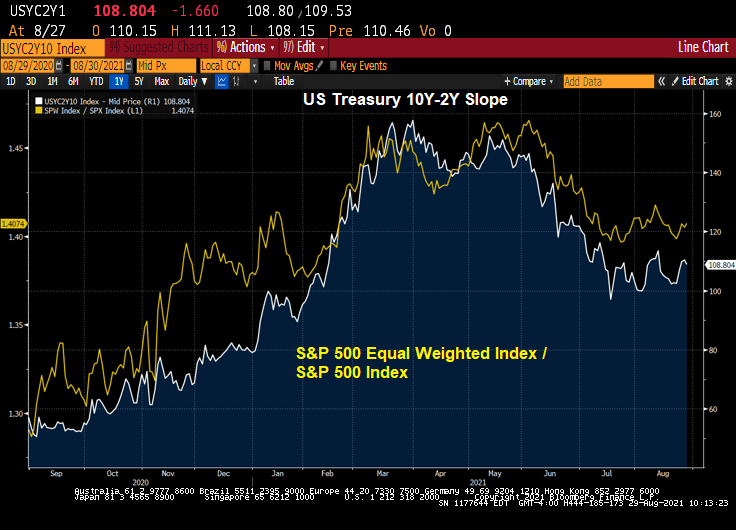

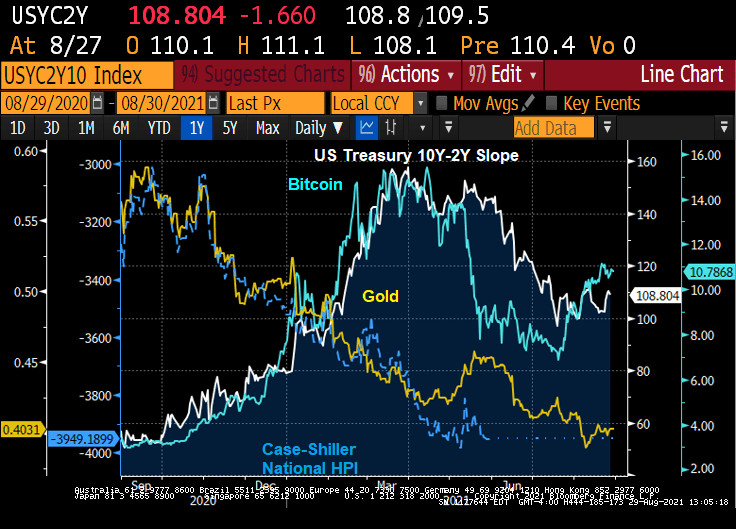

The shape of the yield curve has been highly influential recently in relative performance trends between various areas of the market. From last summer through May of this year, the steepening of the yield curve coincided with healthy outperformance of cyclical stocks. Since May, the flattening of the curve has coincided with more defensive (or at least high quality) leadership out of the tech and health care sectors. The logic goes, therefore, that a re-steepening of the curve should coincide with a shift back to cyclicals. Indeed, that shift may be in the early innings.

Let’s take a look at the US Treasury 10Y-2Y curve slope over the past twelve months against the Citi Economic Surprise Index for the US. You can see curve fatigue starting in April 2021 as the Citi Economic Surprise Index turns negative.

The the more cyclical and smaller skewed S&P 500 equal weight index has started to outperform the S&P 500 again, right on queue with the yield curve re-steepening.

Industrial stocks are under-performing the broader S&P 500 index as the curve flattens.

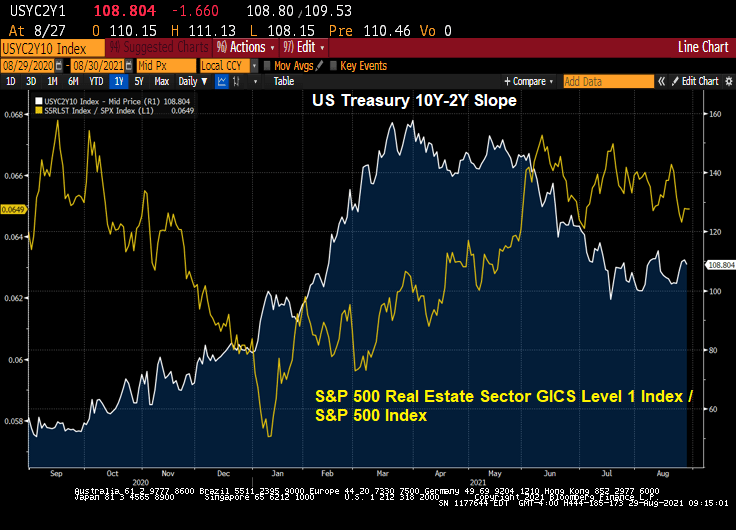

Real estate stocks? They are outperforming the broader S&P 500 index.

Mining stocks like gold mines? They are underperforming the broader S&P 500 index.

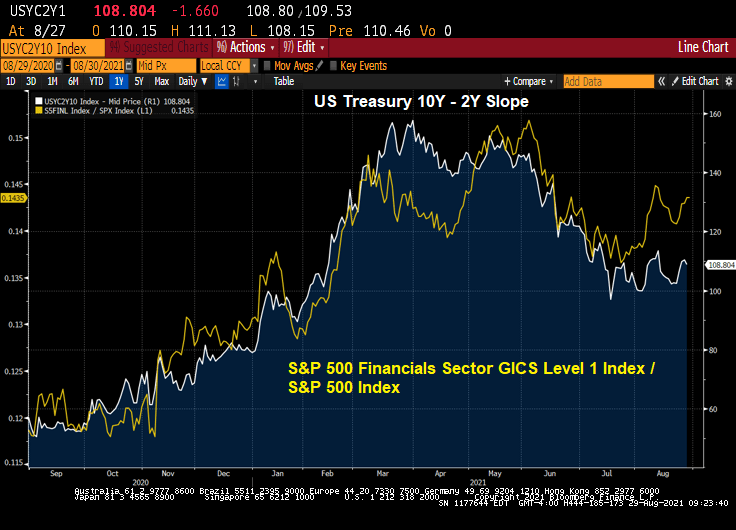

Financial stocks? Not surprisingly, The Fed’s dovish behavior is causing financial stocks to outperform the broader S&P index.

Likewise, information technology stocks are outperforming the broader S&P 500 index.

So, by Powell delaying any balance sheet slowdown and rate increases, we have clear winners (real estate, financials, information tech) and clear losers on a relative basis (industrials, retail, metals and mining).

The Others! Due to volatility differences, I wouldn’t over-interpret this chart. But Bitcoin as a ratio of the S&P 500 index is “kicking ass!” Gold and housing as a ratio of the S&P 500 index seemingly can’t keep up with the S&P 500 index.

W. Scott Frame, Brian Greene, Cindy Hull and Joshua Zorsky August 26, 2021

The Federal Reserve quickly responded to significant financial market disruption at the onset of the COVID-19 pandemic in March 2020, providing stability in a variety of ways. This included large-scale purchases of U.S. Treasuries and agency mortgage-backed securities (MBS).

While market functioning improved in the subsequent months, the central bank has continued purchasing these assets to maintain smooth functioning as well as to help foster accommodative financial conditions. We explore the Federal Reserve’s purchases of agency MBS—mortgage bonds guaranteed by Ginnie Mae, Fannie Mae and Freddie Mac—and related market dynamics during the pandemic, including why mortgage rates fell to historic lows.

Agency MBS and Mortgage Prepayment

The market for agency MBS is among the largest fixed-income markets in the world ($7.6 trillion) and acts as the benchmark for pricing fixed-rate home mortgages eligible for agency guarantees.

These securities distribute monthly principal and interest payments due on underlying mortgages to investors. While agency MBS investors are shielded from credit risk by government guarantees, they do face prepayment risk.

Homeowners with fixed-rate mortgages make principal and interest payments each month based on a predetermined amortization schedule. However, the borrower has the option to pay down additional mortgage principal at any time. (This usually occurs when the borrower refinances the loan or sells the home.) The initial value of this prepayment option is reflected in the borrowers’ mortgage interest rate and is passed through to the agency MBS investor.

Large declines in mortgage rates can result in a sizeable swath of fixed-rate mortgage borrowers with refinancing options “in-the-money.” When this happens, there is an expectation of a rapid decline in existing higher coupon-rate agency MBS balances due to prepayments and a corresponding increase in the issuance of new securities with lower coupon rates.

Evolution of Federal Reserve Policy and Purchases

As the pandemic’s economic impact unfolded, the Federal Open Market Committee (FOMC) announced on March 15, 2020, it would increase agency MBS holdings by at least $200 billion, plus reinvest all principal payments received. This directive was amended a week later to uncap purchases.

The FOMC modified its approach at its June 2020 meeting, increasing agency MBS holdings to around $40 billion per month plus reinvestments, a policy that remains in place. (More information on FOMC directives during 2020 is summarized in the Federal Reserve Bank of New York’s Annual Report on Open Market Operations.) From March 2020 through June 2021, the Federal Reserve increased its agency MBS holdings from $1.4 trillion to $2.3 trillion.

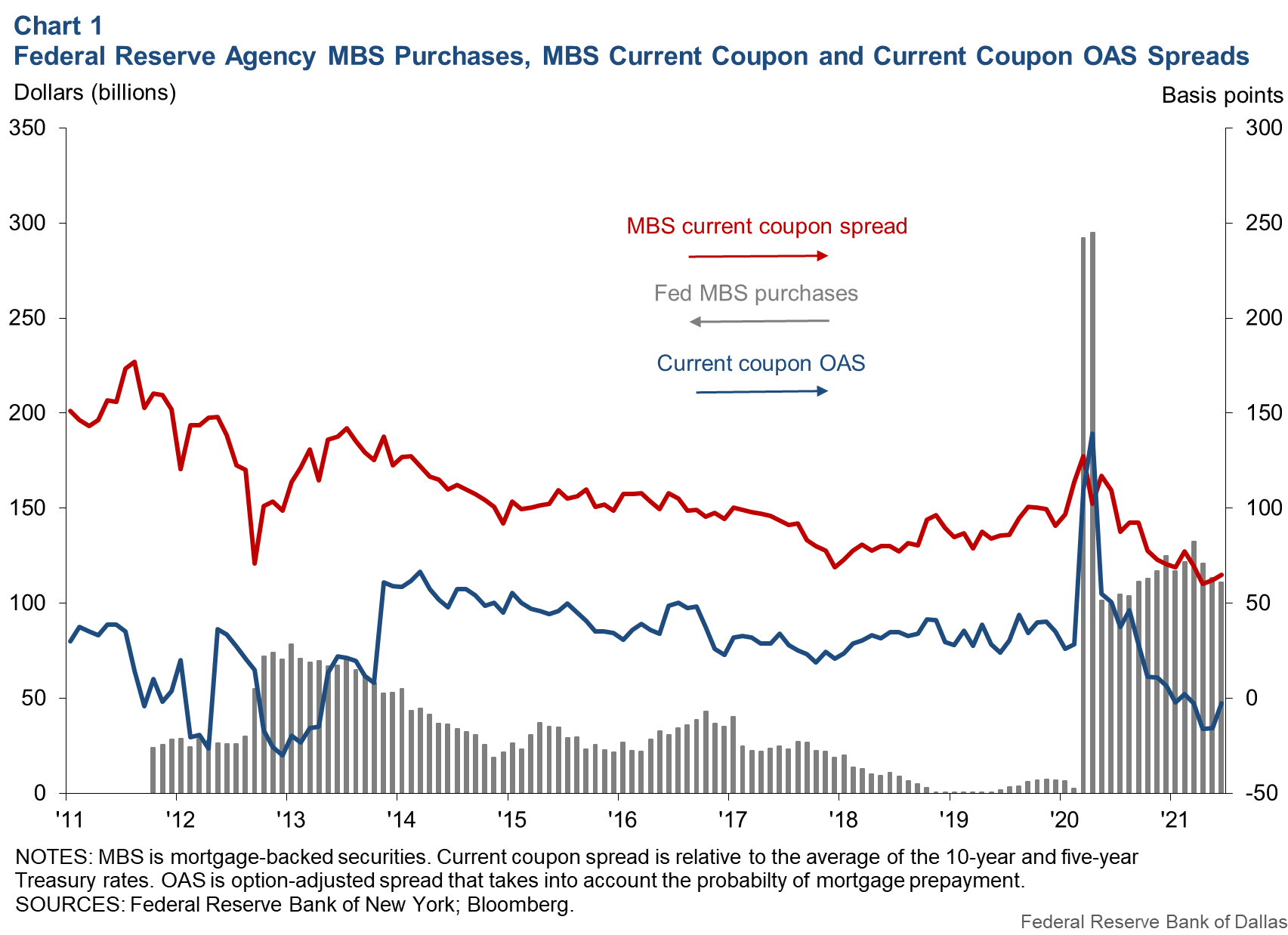

Chart 1 presents the Federal Reserve’s monthly gross purchases of agency MBS over the past decade and the MBS current coupon spread, or the yield consistent with a par value security, less the average of the five-year and 10-year Treasury yields.

The central bank purchased a total $580 billion in agency MBS during the two-month period of March–April 2020, and since has averaged about $114 billion per month including reinvestment of principal payments. During this time, the current coupon spread has steadily narrowed to its tightest levels in almost a decade (62 basis points, or 0.62 percentage points, in May 2021). Primary mortgage rates have similarly fallen during this time, according to Freddie Mac survey data.

Chart 1 also includes a metric known as the current coupon option-adjusted spread (OAS), which includes the likelihood of homeowners prepaying mortgages due to changes in interest rates. The OAS is a derived risk premium that equates model-based agency MBS values (using simulations of future interest rate paths) to prices observed in the market. By accounting for interest rate variability, OAS reflects the residual compensation earned by agency MBS holders arising from noninterest-rate factors, such as the characteristics of the underlying mortgages.

While OAS is typically positive, the measure shown here—produced by Bloomberg for a hypothetical MBS priced at par—has declined steadily since March 2020 and turned negative for the first time since 2013, the only other time in the series history that this has occurred.

Taken together, the data in Chart 1 suggest that the Federal Reserve’s recent large-scale purchases of agency MBS have contributed to historically tight spreads in the secondary market.

Federal Reserve Purchases Agency MBS in Forward Market

The Federal Reserve purchases agency MBS in the to-be-announced (TBA) market, a large and liquid forward market with contracts that settle once per month based on a calendar set by the Securities Industry and Financial Market Association. The central bank typically targets its purchases on the most widely traded coupons for settlement in the following month. This is done through prescheduled auctions conducted throughout the month.

Given the forward-settling nature of the market, the volume of TBA contracts sold for a particular settlement month may not match supply available for delivery when the settlement date arrives.

To manage this mismatch and to avoid delivery failures, market participants engage in “dollar roll” transactions. A dollar roll involves the simultaneous sale (purchase) of a TBA contract for one settlement month and purchase (sale) of a TBA contract for an adjacent month. In this way, a dollar roll allows market participants to delay (bring forward) settlement of TBA contracts. The cost of this trade is reflected by the price difference between TBA contracts settling in adjacent months.

When the price of the front-month TBA becomes greater than the fair value of holding that security over the next month, it is said to be trading “special.” This may be an indication of an expected collateral shortage for the month’s settlement. Dollar roll specialness can subside if the price signal entices market participants to deliver additional collateral into the TBA market for delivery.

Federal Reserve’s Dollar Roll Sales Activity

The Federal Reserve conducts dollar rolls to aid settlement of its TBA purchases if there is a notable level of specialness. The timing and volume of these transactions depend on an internal assessment of market conditions and movements in implied financing rates.

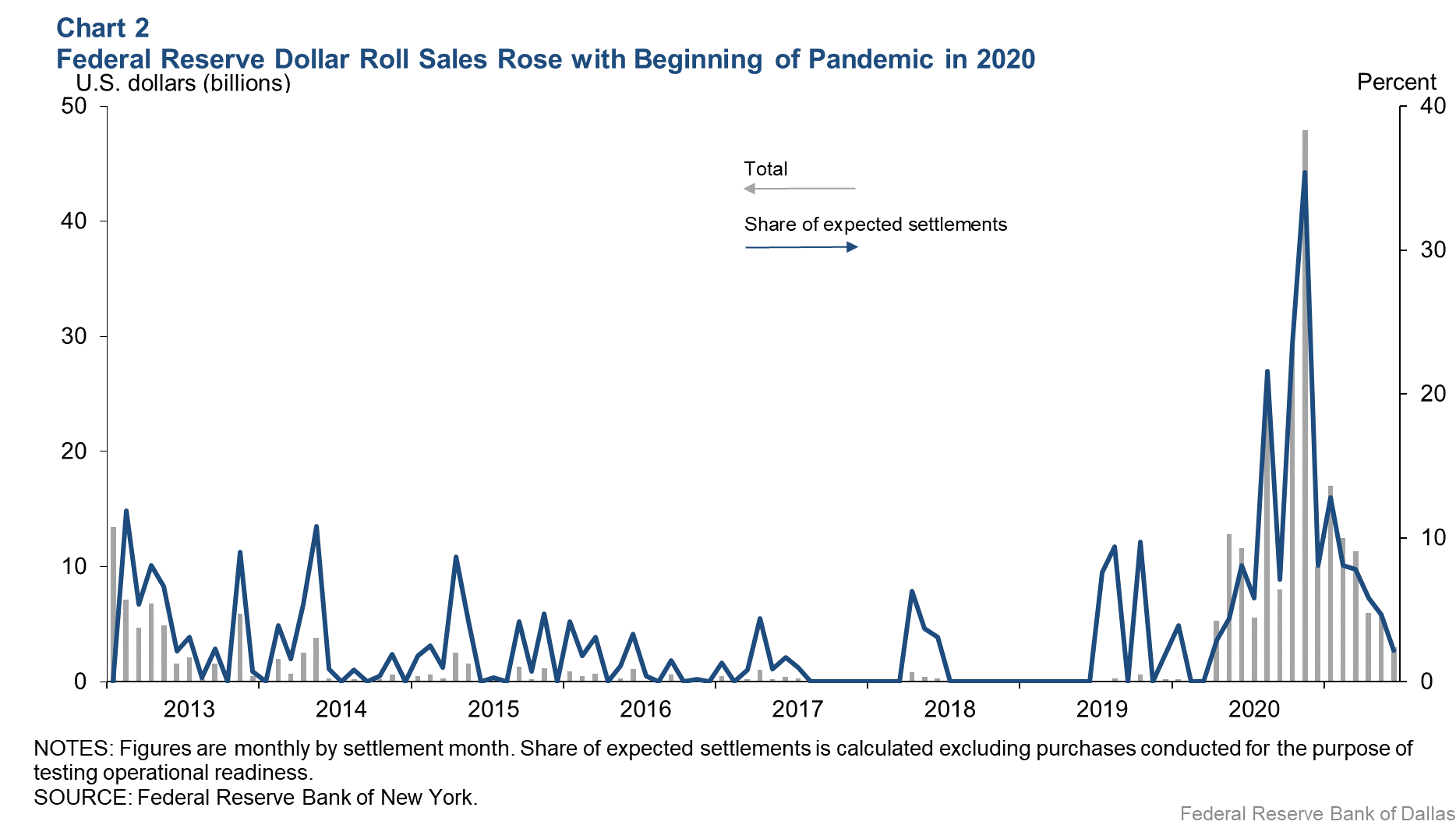

Chart 2 shows the Federal Reserve’s monthly dollar roll sales since the start of 2013 and their share of the month’s expected settlements. Expected settlements are the sum of the regular, planned purchase ($40 billion), principal reinvestments from the prior months’ paydowns and TBA contracts already held for that month’s settlement from previous dollar rolls. The central bank has consistently engaged in dollar roll transactions since April 2020, reaching a peak of $48 billion in November 2020.

The Chart 2 data beg the question of why the Federal Reserve conducted so many dollar roll sales. There are a few explanations.

First, the FOMC’s directive for monthly agency MBS purchases resulted in the central bank acquiring almost 40 percent of newly issued securities since May 2020. Moreover, the Federal Reserve’s TBA purchases were for settlement in the near month, although mortgage originators were often selling TBAs into back months. This created a timing mismatch. In response, the central bank purchased near-month TBAs from dealers, which were then often rolled for back-month settlement.

Second, commercial banks represent the only other investor base that increased its agency MBS holdings during 2020 and through first quarter 2021 ($580 billion). But banks tend not to conduct dollar roll transactions to delay settlement, owing to the nature of their business operations and accounting considerations.

Third, the sharp decline in mortgage rates led to periods of collateral scarcity for lower coupon securities. The Fannie Mae or Freddie Mac Uniform MBS (UMBS) 30-year, 2 percent coupon provides a useful example. During the summer of 2020, mortgage originators sold the majority of TBAs forward into these securities. However, the outstanding stock of UMBS 30-year, 2 percent coupons was modest, thus limiting the ability of existing securities to be delivered for settlement. As the outstanding stock of UMBS 30-year, 2 percent securities increased, the Federal Reserve’s roll activity in the coupon declined commensurately.

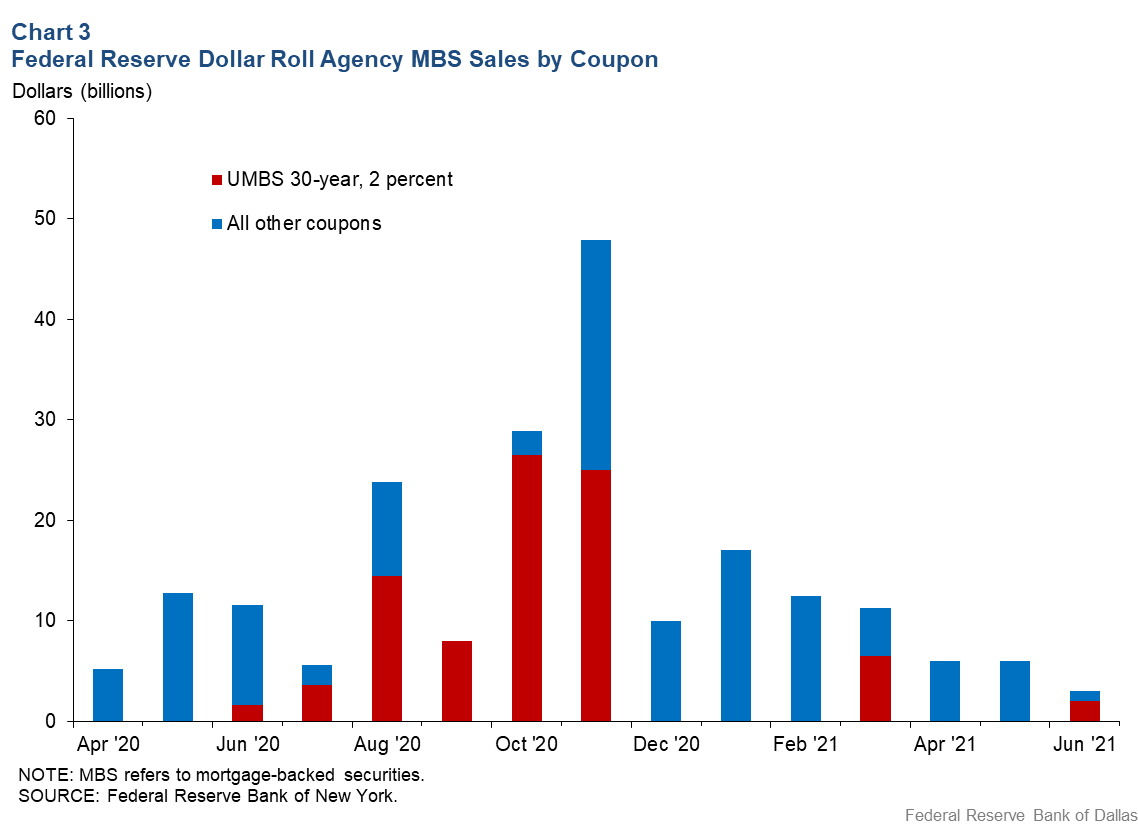

Aside from the UMBS 30-year, 2 percent coupon, the Federal Reserve conducted dollar roll sales in eight other securities. This indicates that specialness was more widespread at times, although the rolling of these other coupons was more sporadic. Chart 3 presents the volume of Federal Reserve dollar roll sales for the UMBS 30-year, 2 percent coupon relative to all other TBA contracts.

The Federal Reserve’s large-scale purchases of agency MBS have likely contributed to dollar roll specialness over the course of the current purchase program. The central bank has responded by using dollar roll sales to extend the settlement of some of its TBA purchases into the future.

Tight Spreads, Low Mortgage Rates

In response to the pandemic, the Federal Reserve restarted its large-scale purchases of agency MBS and now holds more than $2.3 trillion, representing almost 30 percent of outstanding bonds. These purchases have been associated with historically tight spreads in that market, which have translated into historically low mortgage rates.

Because of periodic supply shortages, the Federal Reserve has smoothed purchases using dollar roll sales that extend settlement into the future and aid market functioning.

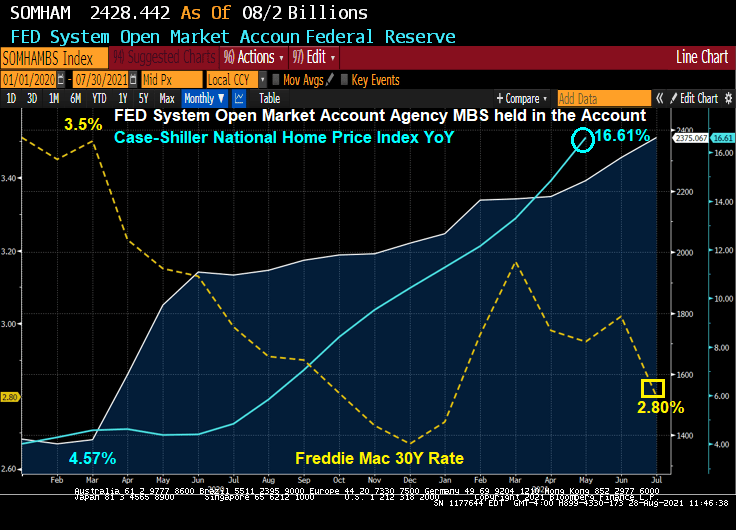

Here is the chart that The Fed Folk left out. Home price growth pre-Covid Fed surge in Agency MBS purchases was 4.57% YoY with a 30-year mortgage rate of 3.5%. The most recent Case-Shiller HPI growth rate was 16.61% and the latest Freddie Mac 30-year mortgage rate is 2.80%.

So while The Federal Reserve calmed the savage beast (mortgage markets), they also contributed to bubble-like growth in home prices.

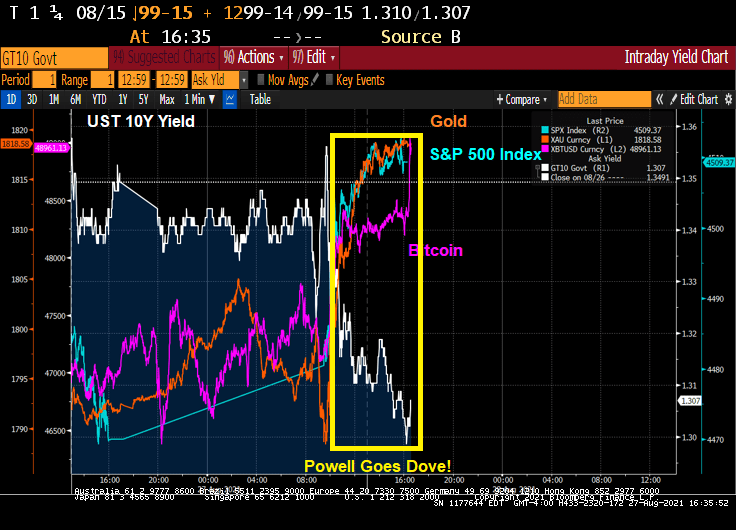

Well, I was expecting a little more guidance than Fed Chair Powell gave today at the J-Hole conference. In fact, failing to give a hard date on paring back the balance sheet and raising rates is downright dovish. A regrettable incident.

As a result of Powell’s dovish talk, GOLD, BITCOIN and the S&P500 index rose.

The S&P 500 index rose almost 1% today while the 10Y Treasury yield dropped 4 bps.

Fed’s Favorite Inflation Measure Surges At Fastest Pace In 30 Years As Spending, Incomes Rise!

Federal Reserve Chairman Mao Powell will be speaking at 10am EST in his virtual Jackson Hole KC Fed Conference speech. He might actually save his blockbuster comments for the next Fed meeting, instead just hinting at what The Fed might do to reduce the behemoth monetary stimulus. After all, The Fed has already slowed the growth rate of M2 Money to 12.1% YoY.

But before Chairman Mao Powell speaks, the PCE deflator numbers were released this AM showing that the PCE Deflator YoY rose to 4.2%. For households for a fixed income, this is bad news unless they receive a COLA (not a Pepsi, but a cost-of-living adjustment).

I would be remiss if I left out the largest assets for most households: housing. The Case-Shiller National Home Price Index is rising at a 16.6% YoY pace, making housing more expensive for those who are currently renting.

Speaking of which, the US Supreme Court overturned the Biden Administrations rent moratorium meaning that renters can be evicted for failure to make rent payments. (This sounds cut and dry, but the ability of landlords to evict non-paying rents varies from state-to-state and county-to-county).

Having said that, we can see that Personal Spending only grew by 0.3% in July while REAL personal spending fell by -0.1%.

Personal income grew by 1.1% in July and 2.7% YoY , which is lower than the PCE Deflator YoY of 4.2%.

University of Michigan sentiment is out at 10AM EST. Stay tuned!

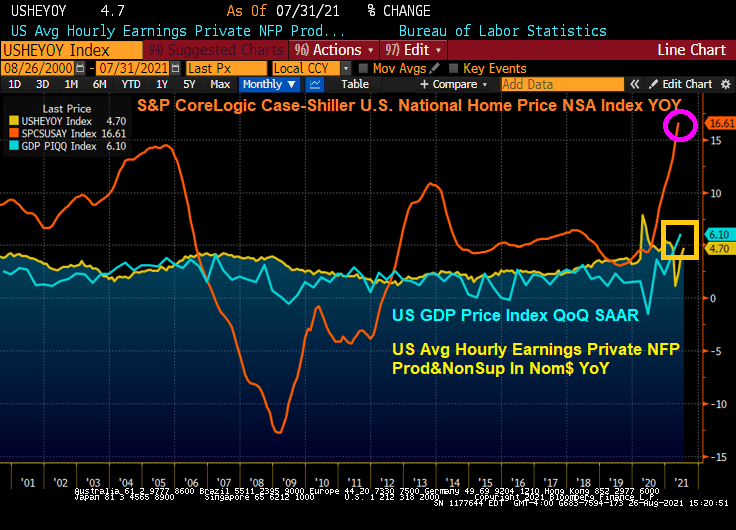

Looks an awful lot like 2005 before the housing price crash, financial crisis and Great Recession. US home prices, HOUSING inflation, is growing at 16.61% YoY, GDP Price index QoQ (annualized) is growing at 6.10%, and average hourly earnings is growing at 4.20% YoY.

Let’s see what happens in Jackson Hole this weekend!

Policy makers should “get started” and begin to slow asset purchases even though the delta variant poses a risk to the U.S. economic outlook and to job growth, Federal Reserve Bank of Kansas City President Esther George said.

“The economy continues to grow at a strong rate,” George said, adding that in terms of the potential risk of the delta variant, “you can imagine that it might slow down some of the returns to the labor market. But I don’t expect at this point that it will derail the economy as we saw last year when we first had to deal with the virus.”

Yes, US GDP QoQ just checked in at a whopping 6.6% with personal consumption growing at 11.9% for Q2.

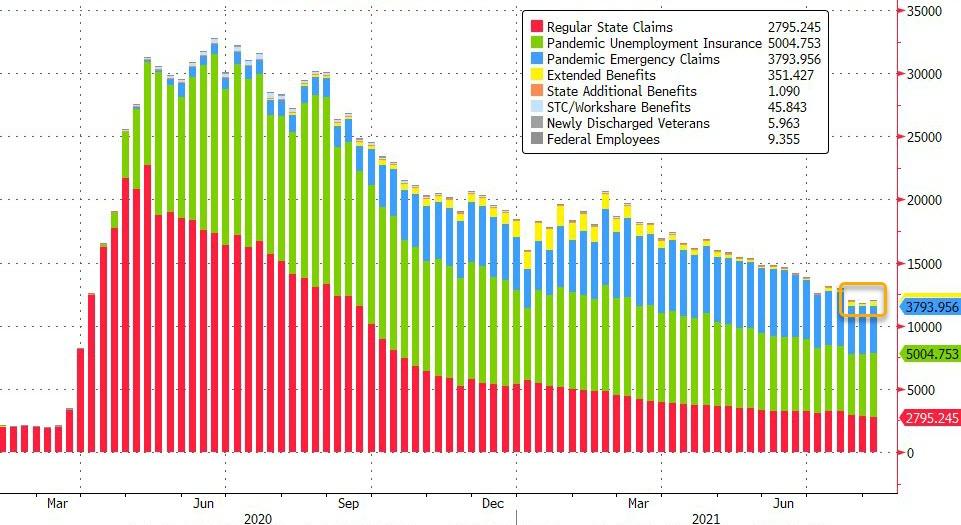

Of course, The Federal government and Federal Reserve have over stimulated the economy and financial markets. Compare the collected benefits (unemployment, pandemic, extended, etc.) compared to before Covid struck in March 2020.

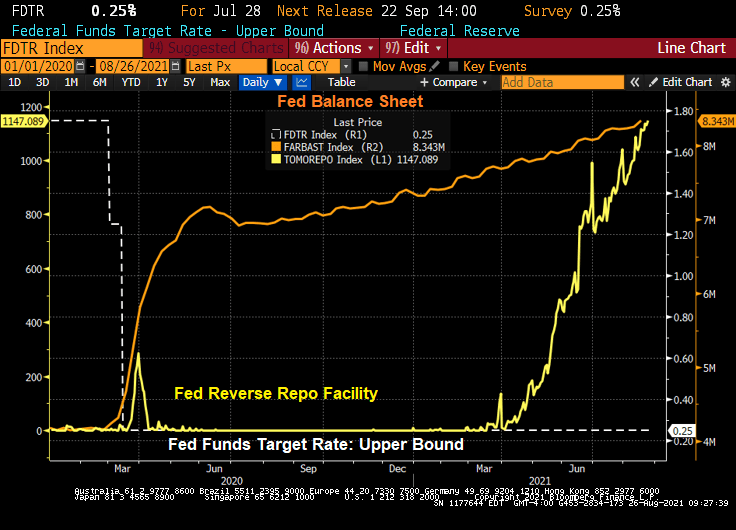

And compare The Fed’s monetary stimulus since Covid struck in March 2020.

Although Esther George is not a voting member of the FOMC, I think she has a good point. There is too much monetary stimulus in the market.

Will the Open Market Committee heed George’s warning? Or will they treat her like Ohio State great Eddie George as just another voice?

Mortgage applications increased 1.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 20, 2021.

The Refinance Index increased 1 percent from the previous week and was 3 percent higher than the same week one year ago. You can clearly see the Refi Wave associated with the Covid outbreak and sudden Fed monetary stimulus resulting in a lowering of 30-year mortgage rates.

The seasonally adjusted Purchase Index increased 3 percent from one week earlier. Notice the general slowdown in purchase applications with soaring home prices.

The unadjusted Purchase Index increased 1 percent compared with the previous week and was 16 percent lower than the same week one year ago.

You must be logged in to post a comment.