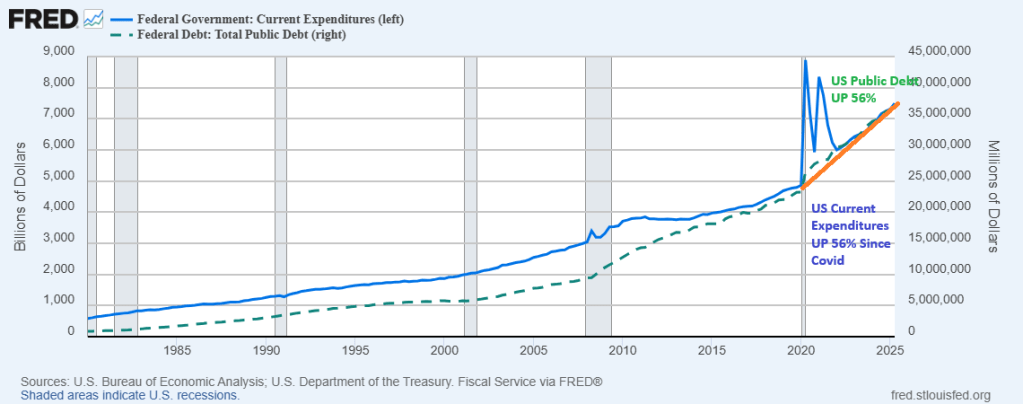

Can we ask the US House and Senate if they will ever return US Federal government spending to pre-Covid levels? Both US Federal government spending and public debt are up 56% since the Covid outbreak in 2020.

The answer is no. Politicians thrive on Federal spending.

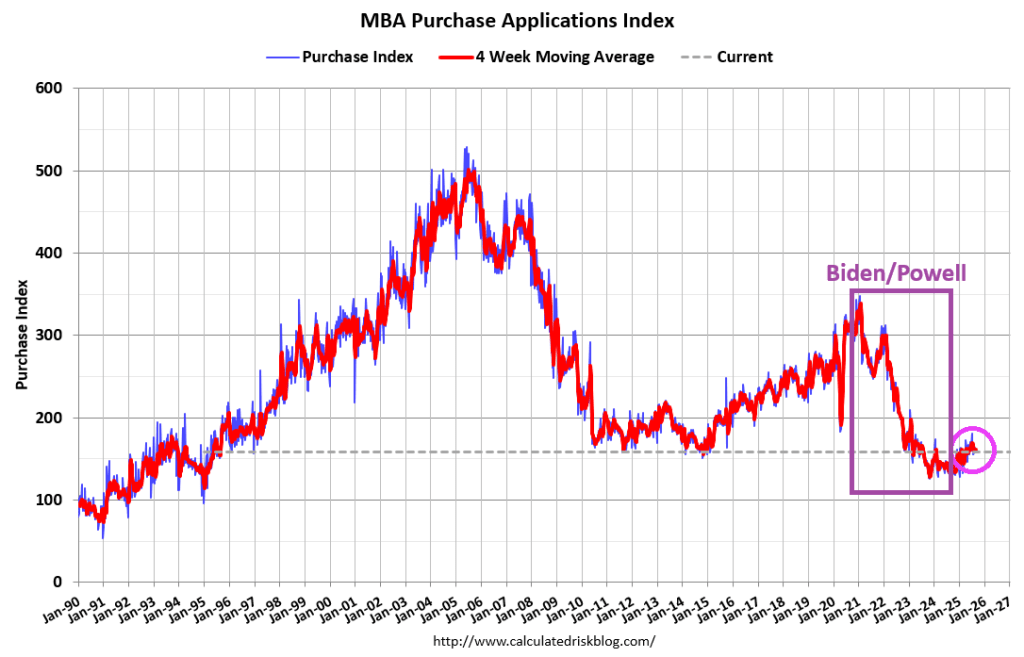

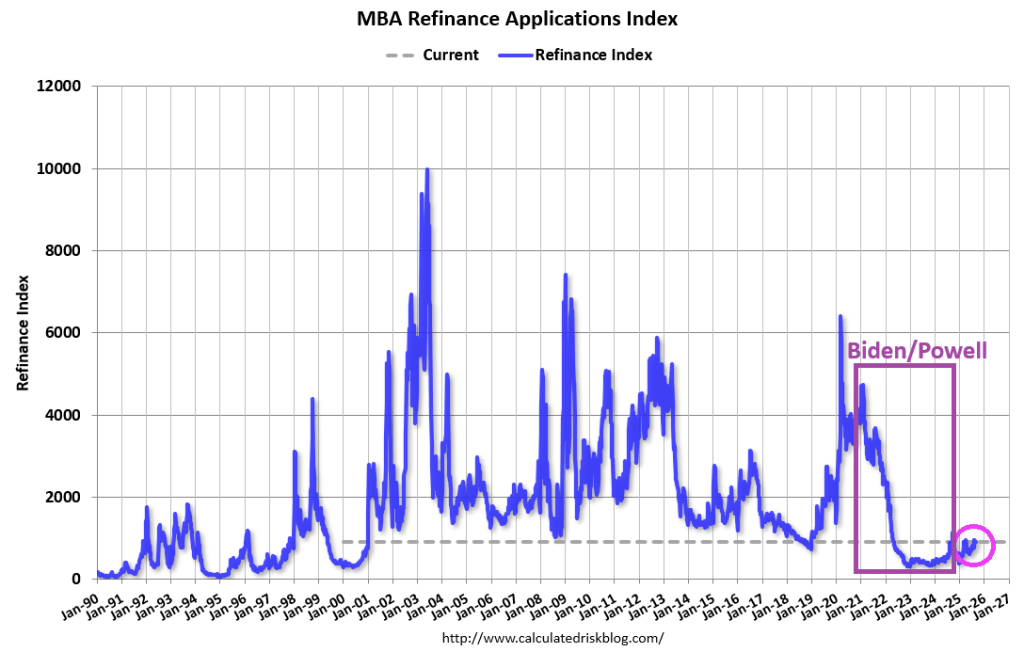

Mortgage applications decreased 12.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 26, 2025.

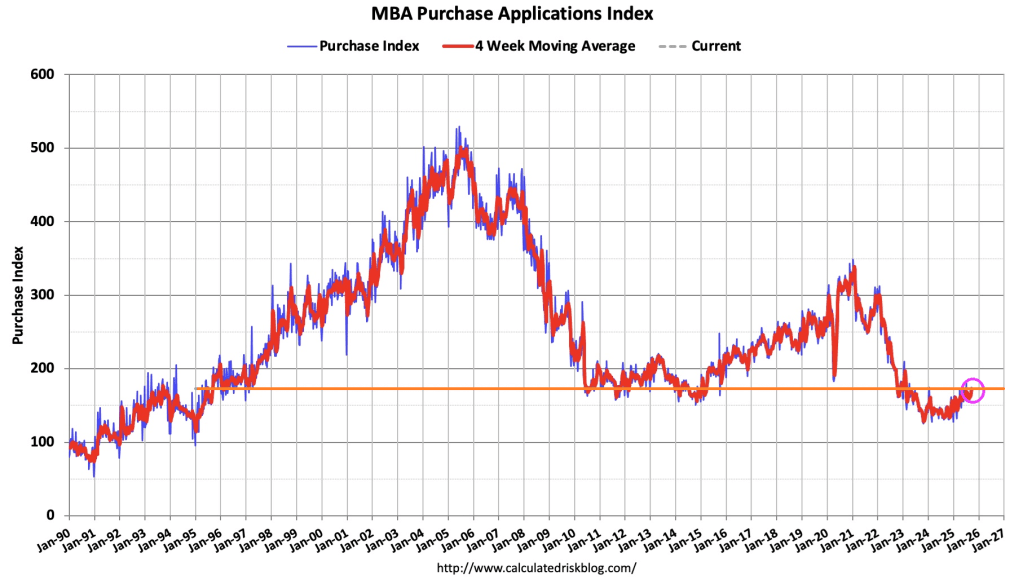

The Market Composite Index, a measure of mortgage loan application volume, decreased 12.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 16 percent higher than the same week one year ago.

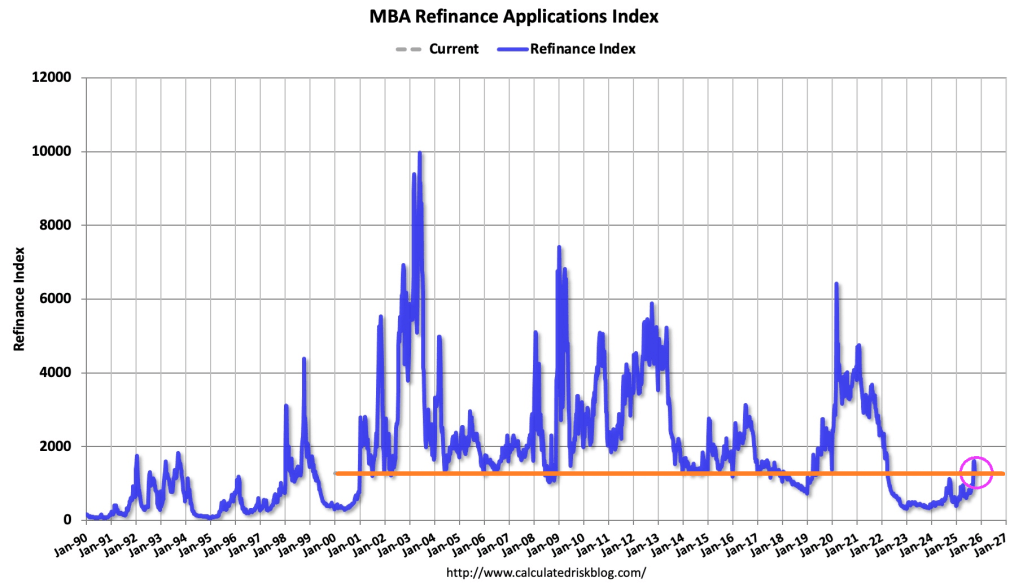

The Refinance Index decreased 21 percent from the previous week and was 16 percent higher than the same week one year ago.

Mortgage rates increased to its highest level in three weeks as Treasury yields pushed higher on recent, stronger than expected economic data. After the burst in refinancing activity over the past month, this reversal in mortgage rates led to a sizeable drop in refinance applications, consistent with the view that refinance opportunities this year will be short-lived.

But for last week, mortgage applications increased 9.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 5, 2025. This week’s results include an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 9.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 23 percent higher than the same week one year ago.

The Refinance Index increased 12 percent from the previous week and was 34 percent higher than the same week one year ago.

The holiday-adjusted refinance index had its strongest week in a year and the average loan size for refinances also increased significantly, since borrowers with large loans are more sensitive to bigger rate moves. Refinance applications accounted for almost 49 percent of all applications last week. … The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.49 percent from 6.64 percent, with points decreasing to 0.56 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

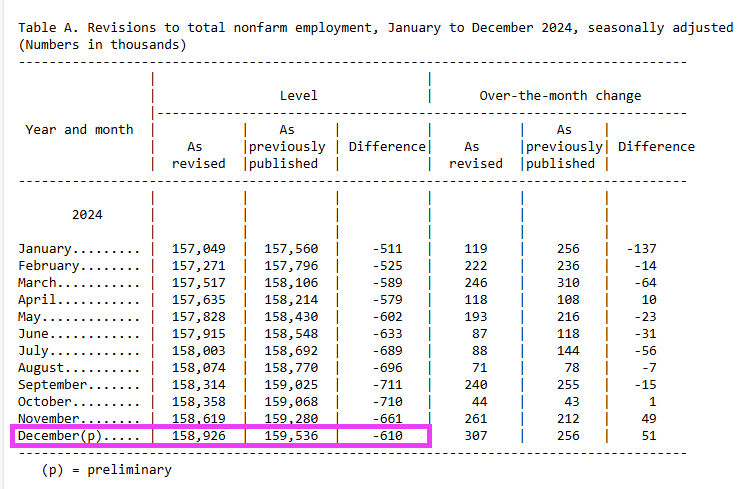

Each year, CES employment estimates are benchmarked to comprehensive counts of employment from the Quarterly Census of Employment and Wages (QCEW). These counts are derived primarily from state unemployment insurance (UI) tax records that nearly all employers are required to file with state workforce agencies.

Here is the breakdown:

Wow. Every month during Biden’s last year in his reign of error was a negative revision.

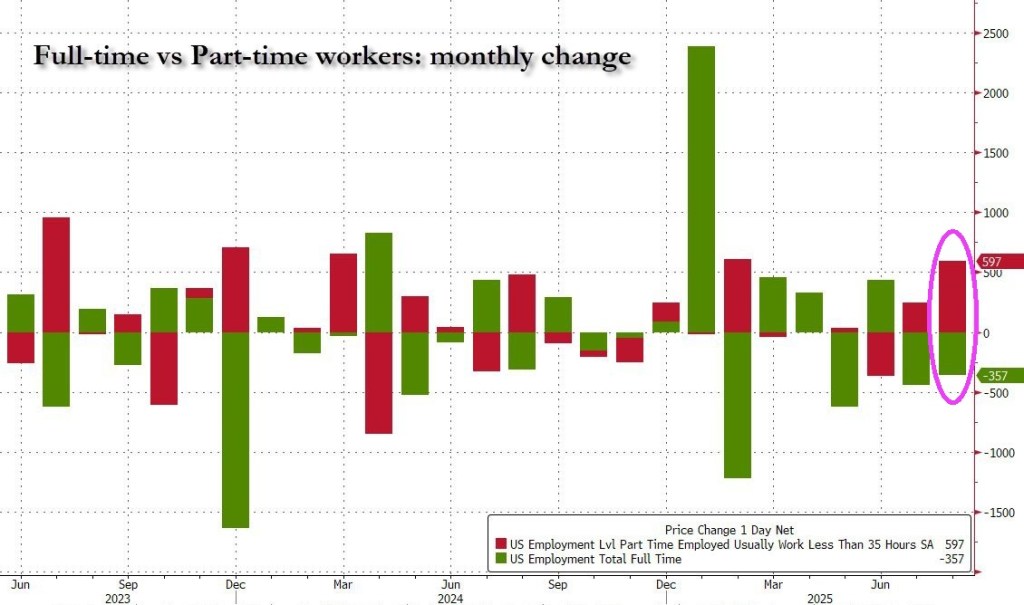

U-3 unemployment rate rose to 4.3%. U-6 unemployment and part-time rose to 8.1%.

Total private jobs added was 38k while manufacturing jobs added was down -12k.

Government jobs dropped -16k.

It gets worse! All of the jobs added were PART-TIME!

It gets even worse: native-born workers plunged by 561K, the biggest one month drop since August 2024. Foreign-born workers increased by 50K, the first increase since March.

Let’s see if The Fed drops the hammer on rates by 50 basis points.

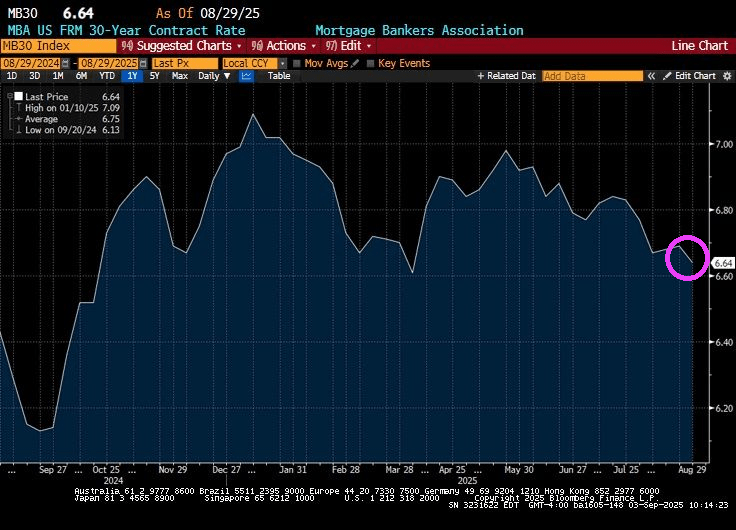

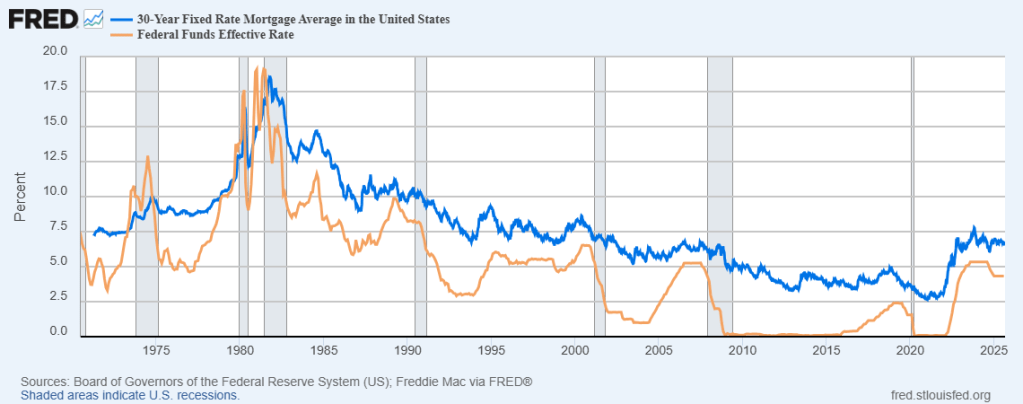

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

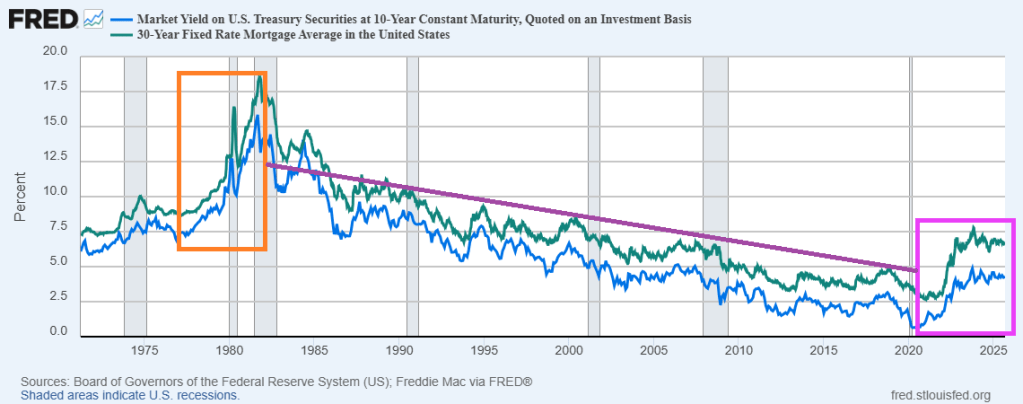

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 29, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was17 percent higher than the same week one year ago.

The Refinance Index increased 1 percent from the previous week and was 20 percent higher than the same week one year ago.

Mortgage rates declined last week, with the 30-year fixed rate decreasing to its lowest level since April to 6.64 percent. However, that was not enough to spark more application activity. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.64 percent from 6.69 percent, with points decreasing to 0.59 from 0.60 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

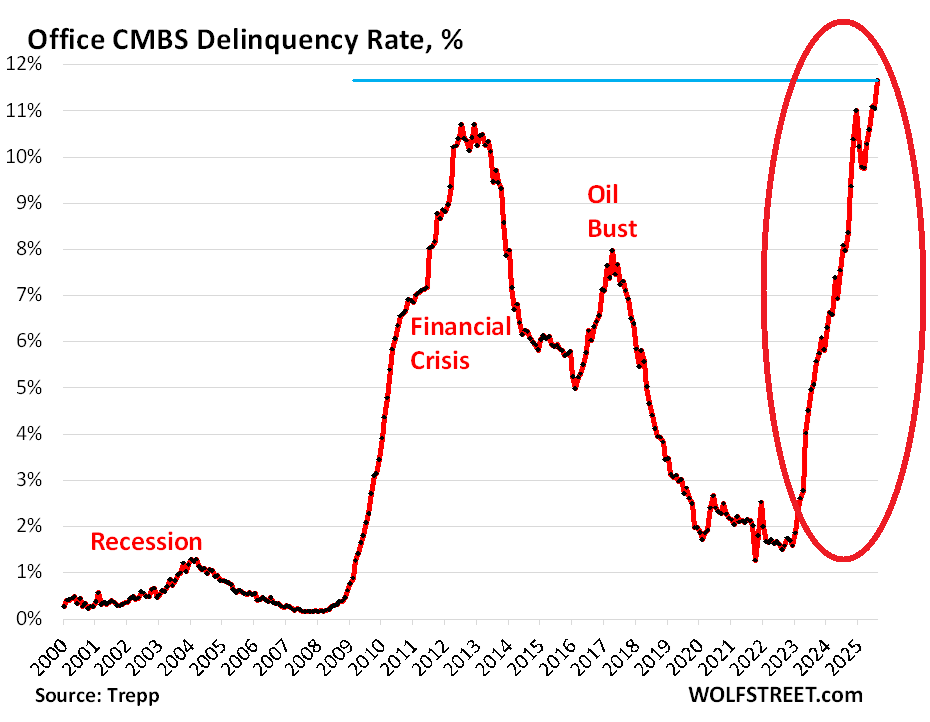

But don’t get your hopes up about The Fed saving the housing market.

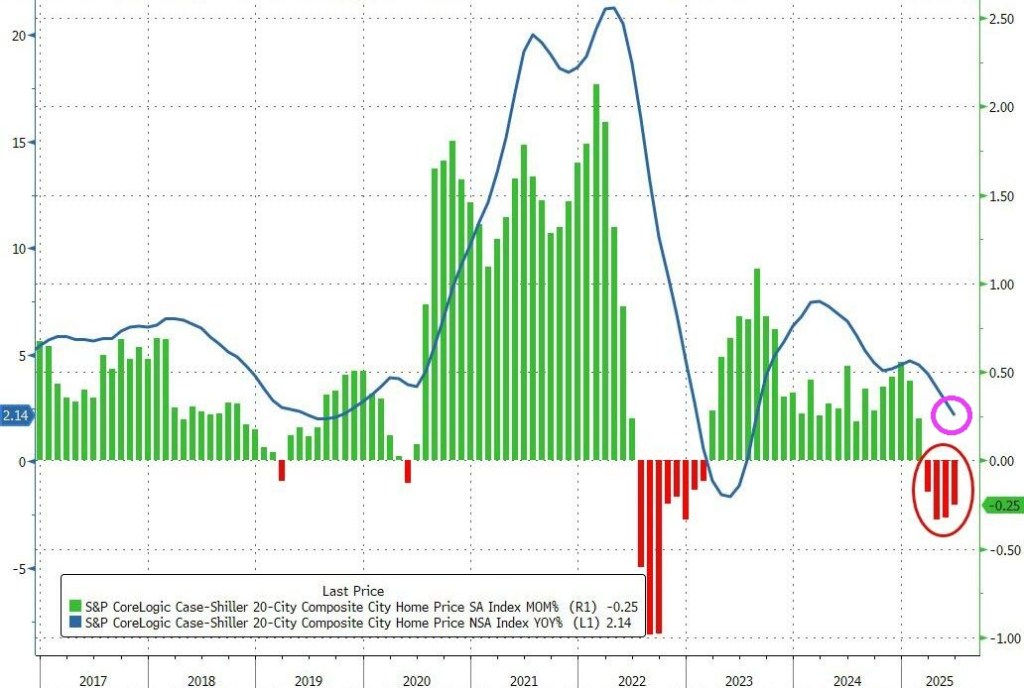

Home prices in America’s 20 largest cities fell for the 4th straight month in June (the latest data available from S&P CoreLogic’s Case-Shiller data released this morning).

The -0.25% MoM drop was larger than expected and dragged the YoY price growth down to +2.15% – the weakest since July 2023.

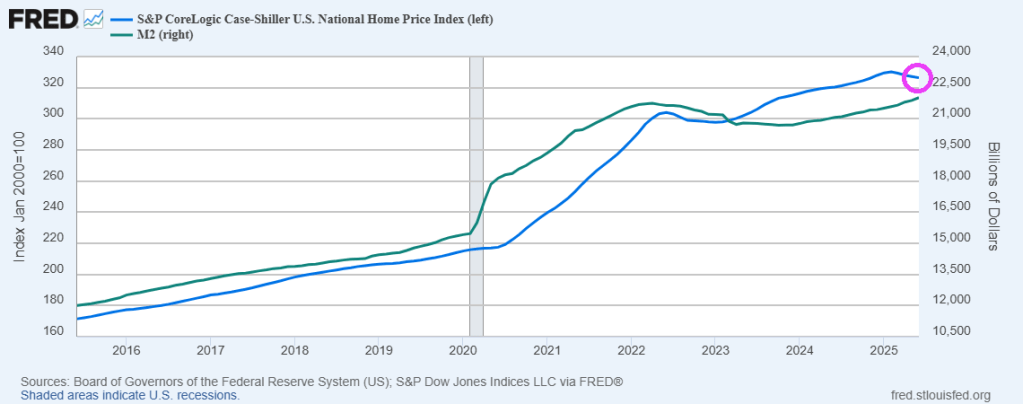

Meanwhile The Federal Reserve keeps on printing money, helping to drive up home prices.

,Metro level? New York and Chicago lead, with Phoenix, Miami, Denver, San Diego, Dallas, San Francisco and Tampa all experiencing price declines.

On a side note, Chicago is even more unaffordable than last year. So much for Mayor Brandon Johnson saying there would be no crime if everyone could afford housing (one of the stupidest comments I have ever heard).

You must be logged in to post a comment.