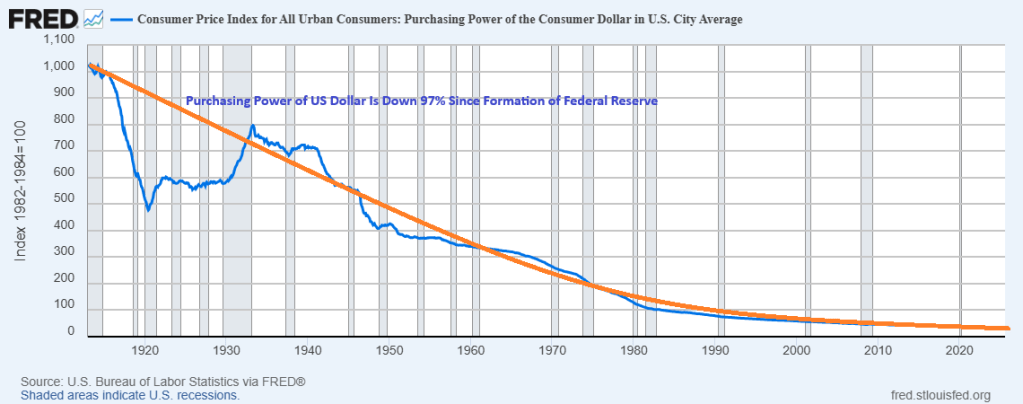

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913. It is the House of the Dying Dollar.

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913.

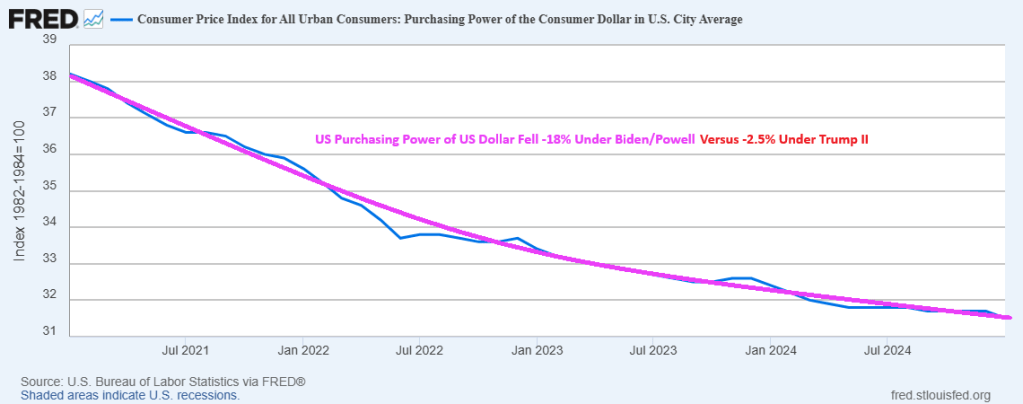

Of course, Trump II is only 9 months old and Biden had 4 long years to destroy the dollar.

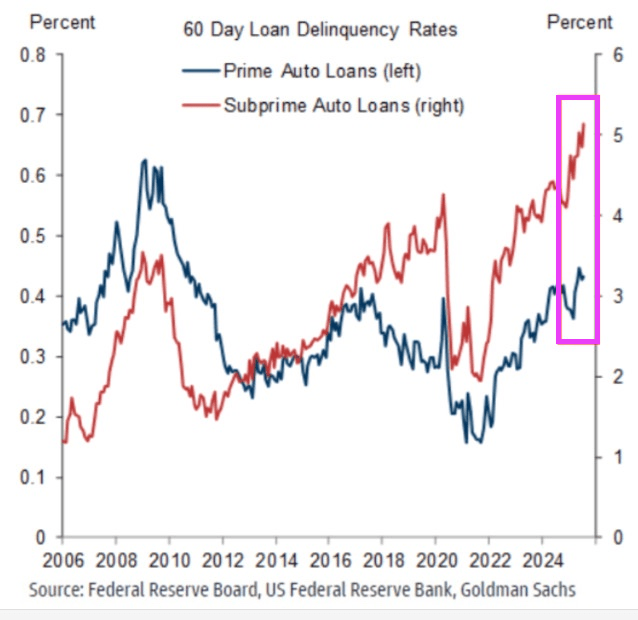

The car market bubble is bursting! Subprime auto loan delinquency rates have now surpassed 5% for the first time in history. The 60-day delinquency rate for subprime auto loans has more than DOUBLED over the last 3 years. Delinquency rates are now ~1.5 percentage points above the 2008 Financial Crisis peak. At the same time, prime auto loan delinquencies rose to their highest in 15 years. Meanwhile, the total value of auto loans in the US jumped $13 billion, to a record $1.66 trillion in Q2 2025. An auto debt crisis is brewing.

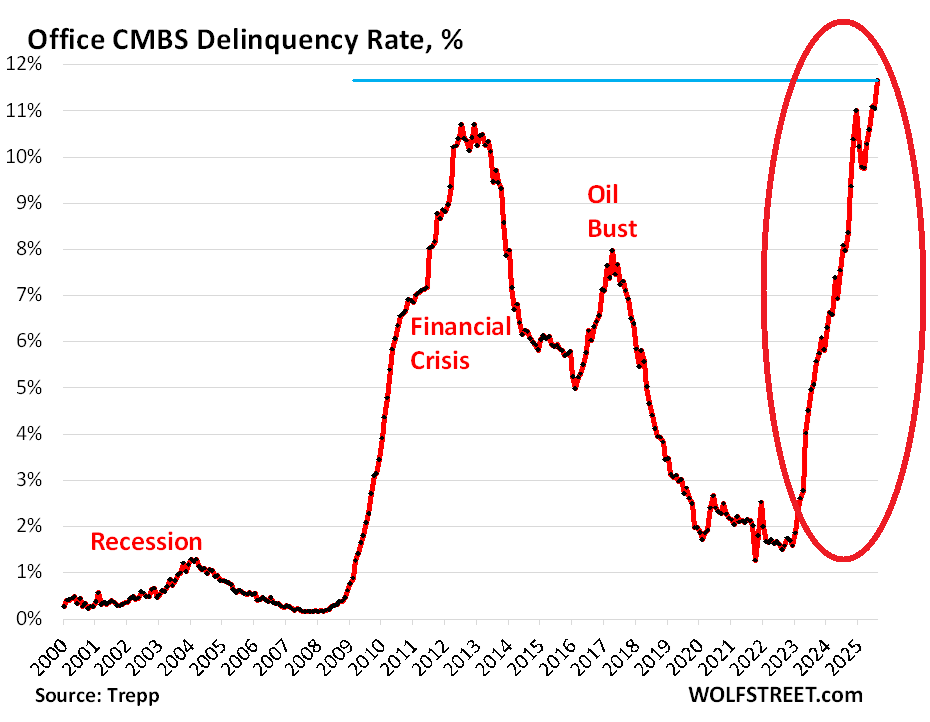

The office CMBS delinquency rate is at an all-time high.

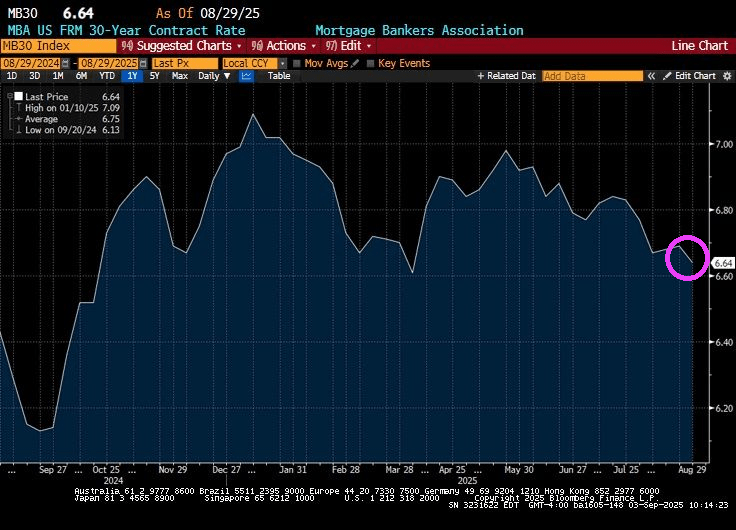

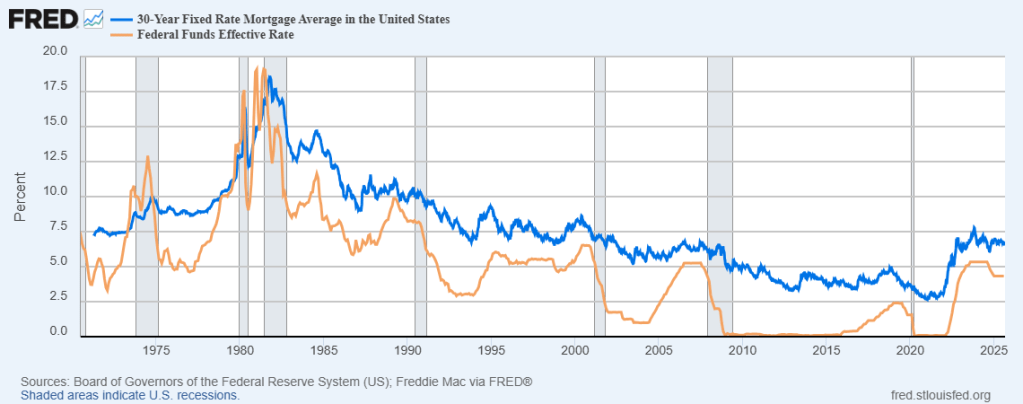

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

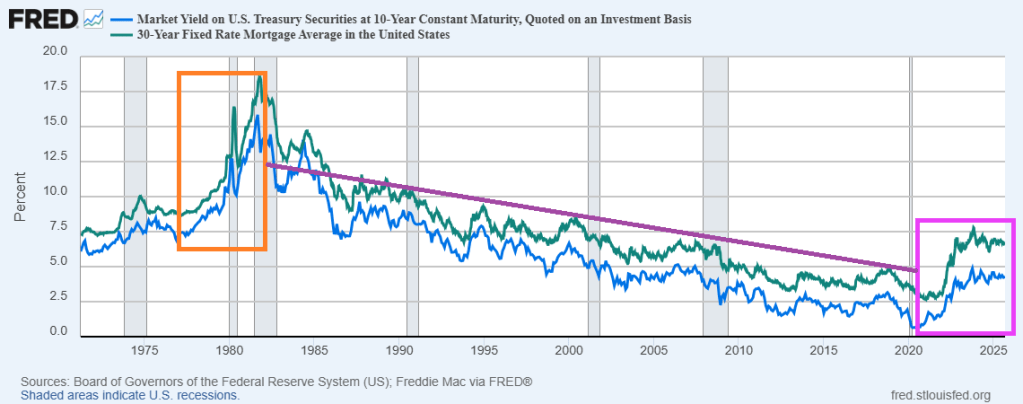

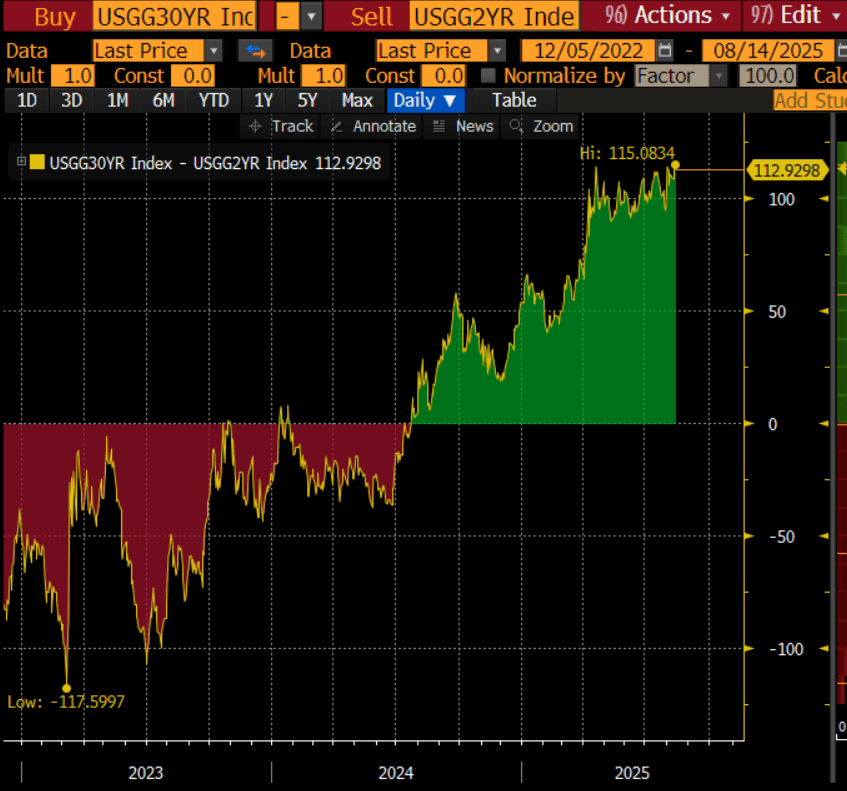

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

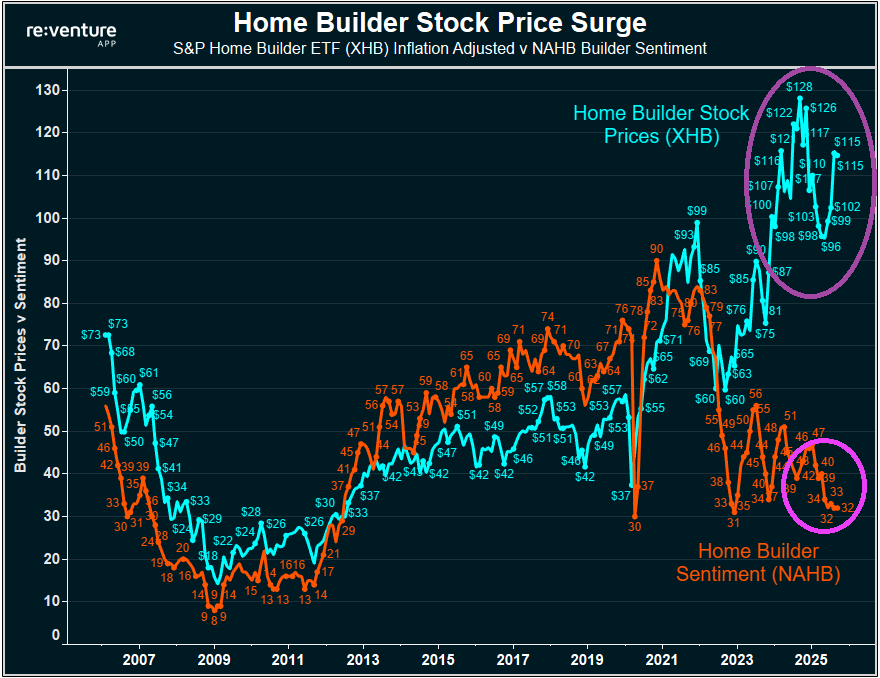

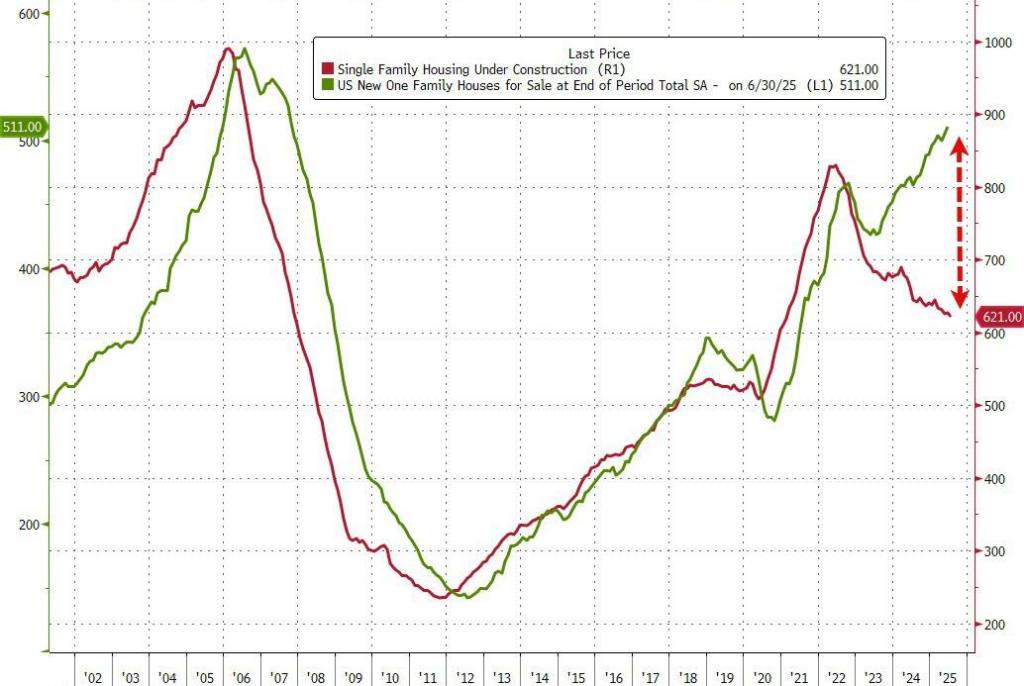

Home builder stock prices have surged, while home builder sentiment has plunged.

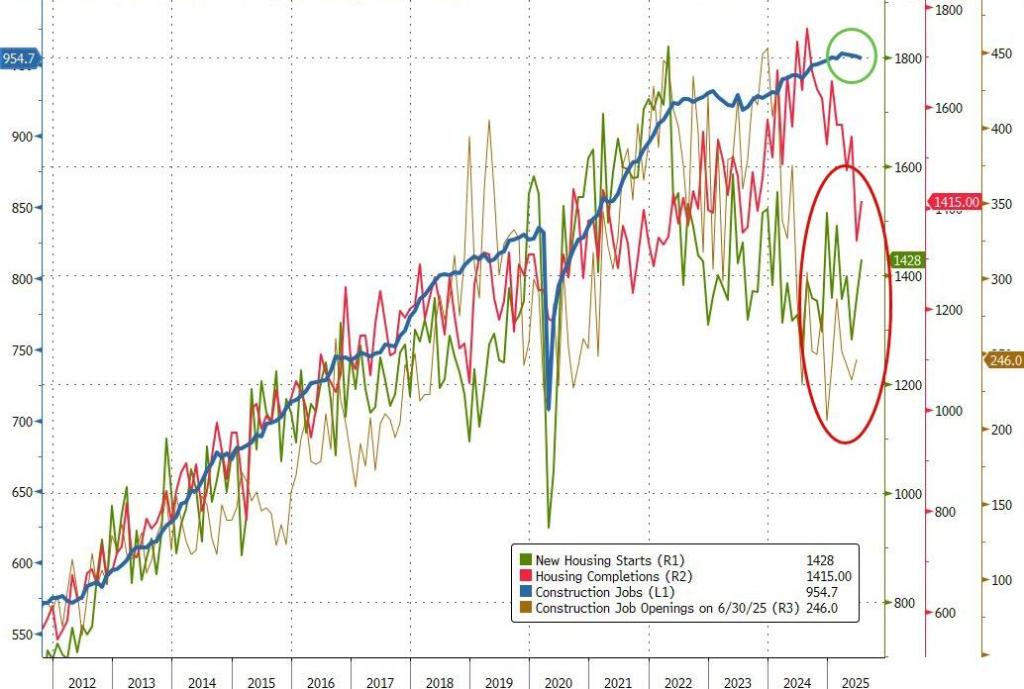

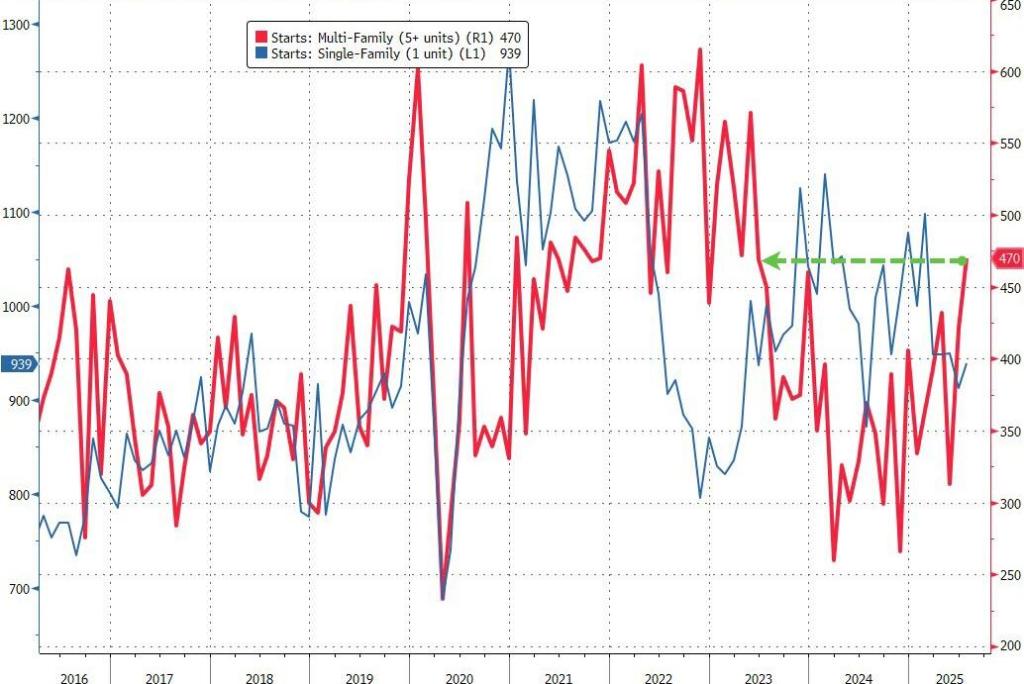

Of course, The Fed’s endless money printing isn’t helping the supply side of home building.

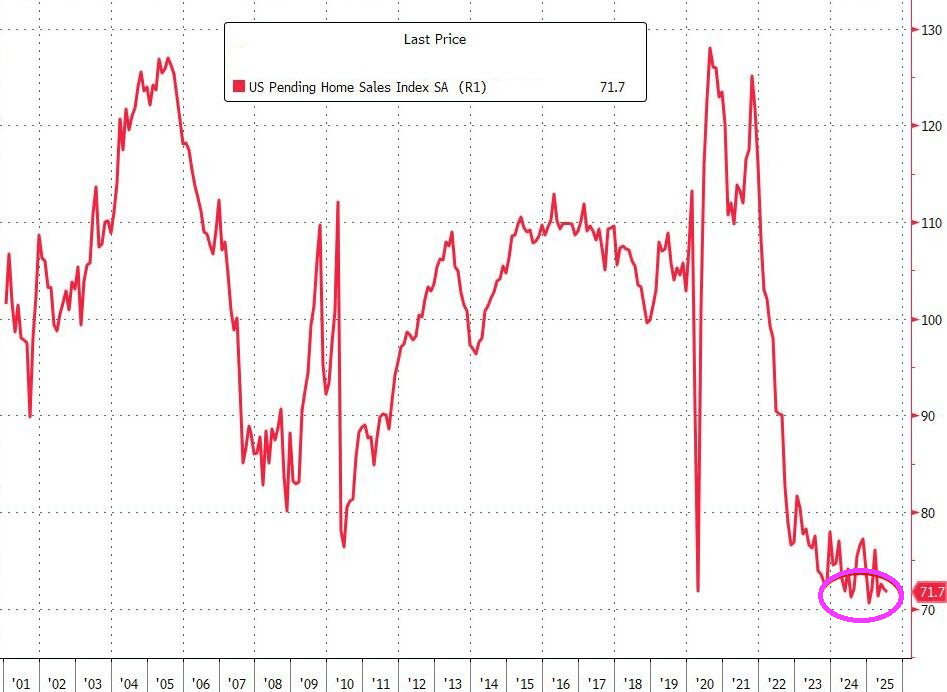

To make matters worse, pending home sales remain in the doldrums.

Federal Reserve Board member Lisa Cook is an embarrasment for committing mortgage fraud, then refusing to step down. And now she has filed a lawsuit against the Trump Administration for wrongful termination. Typical of an Obama appointee!

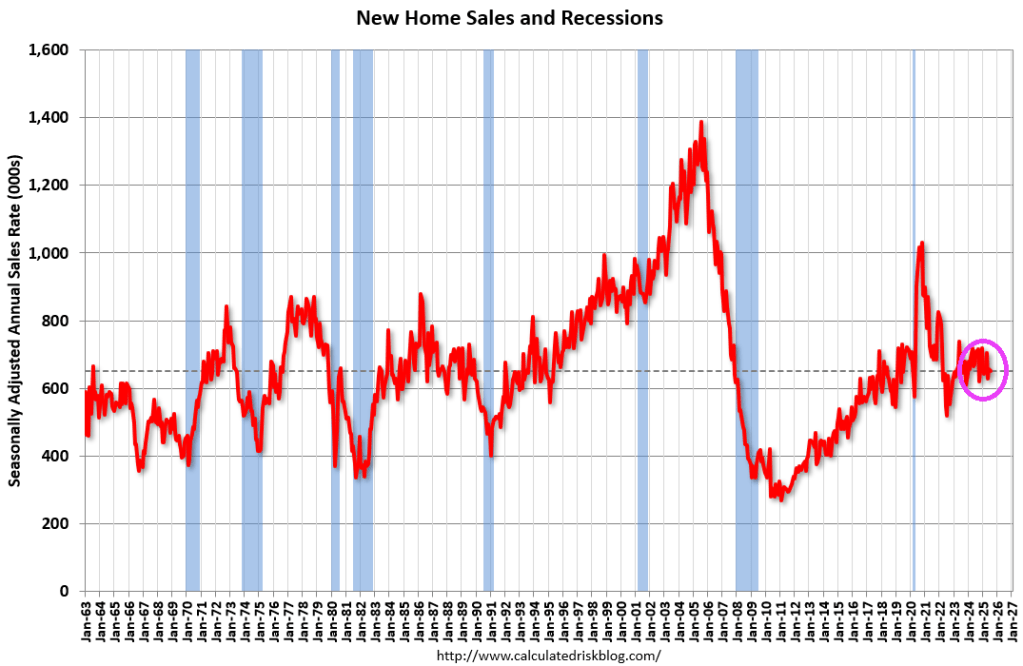

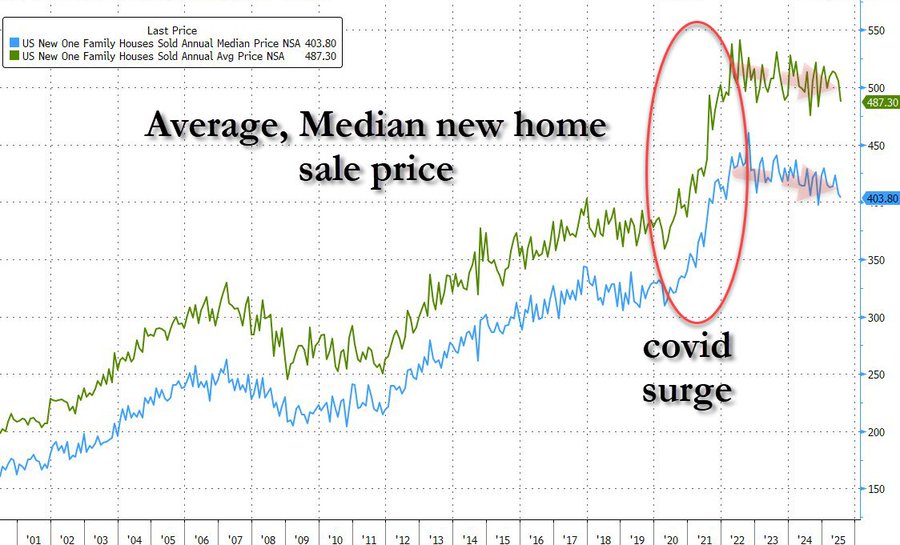

According to the US Census Bureau, New Home Sales of new single-family houses in July 2025 were at a seasonally-adjusted annual rate of 652,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 0.6 percent (±15.5 percent)* below the June 2025 rate of 656,000, and is 8.2 percent (±14.0 percent)* below the July 2024 rate of 710,000.

Median and Average Sales Price

The median sales price of new houses sold in July 2025 was $403,800. This is 0.8 percent (±5.9 percent)* below the June 2025 price of $407,200, and is 5.9 percent (±8.5 percent)* below the July 2024 price of $429,000. The average sales price of new houses sold in July 2025 was $487,300. This is 3.6 percent (±8.0 percent)* below the June 2025 price of $505,300, and is 5.0 percent (±8.6 percent)* below the July 2024 price of $513,200.

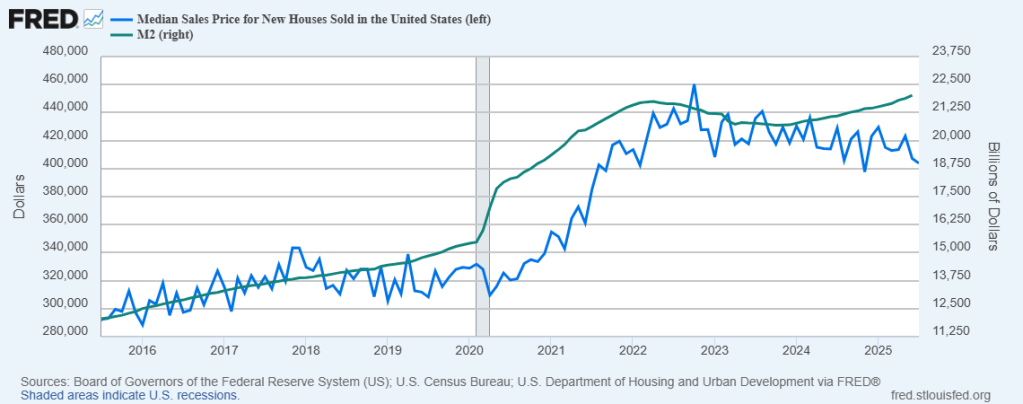

Here is a chart of median sales price of new homes against Fed money printing (M2).

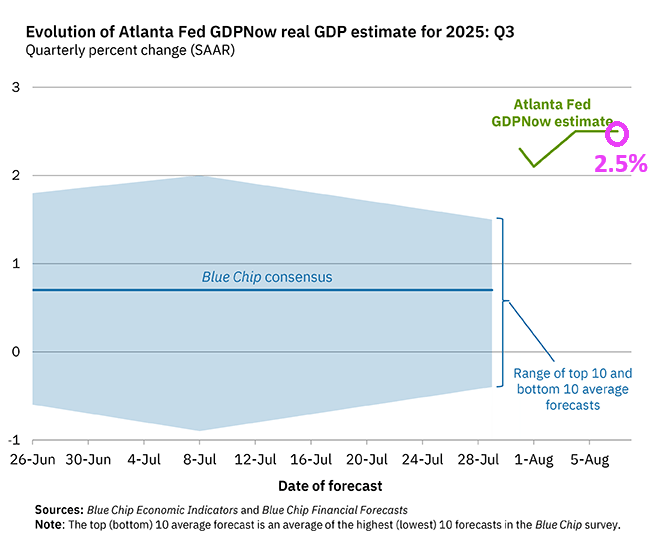

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 2.5 percent on August 7, unchanged from August 5 after rounding. After this morning’s wholesale trade report from the US Census Bureau, the nowcast of the contribution of inventory investment to third-quarter real GDP growth increased from 0.76 percentage points to 0.82 percentage points.

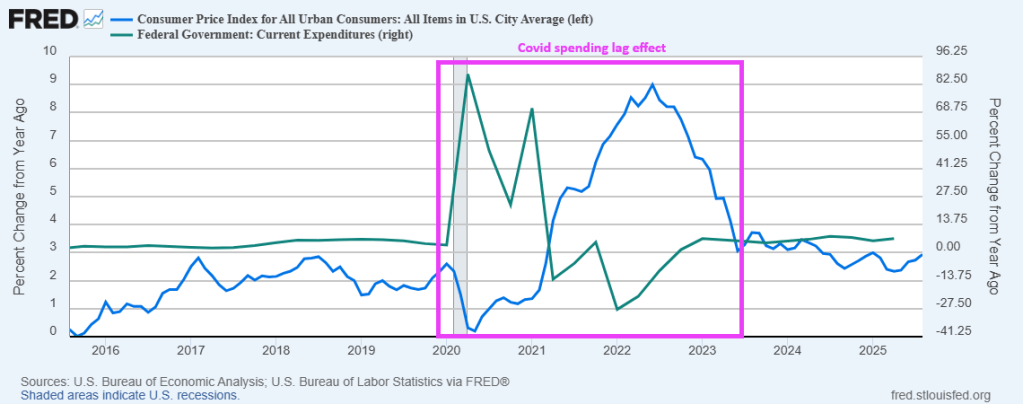

Federal spending, elevated with the outbreak of Covid in 2020 remains higher than pre-Covid levels as does M2 Money printing.

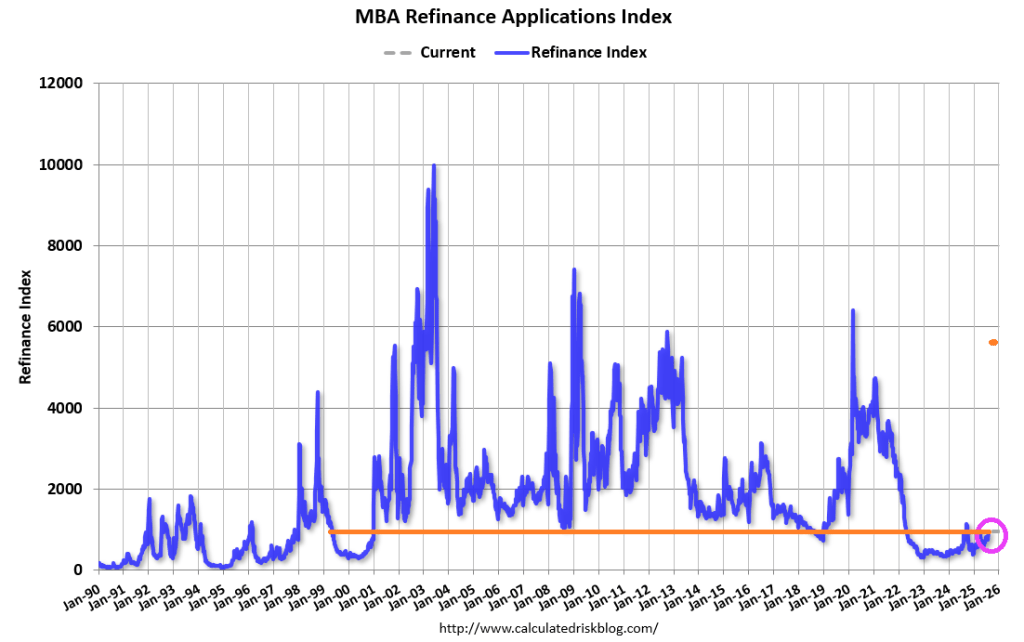

The Fed didn’t try, but mortgage rates fell and mortgage applications rose 10.9% week-over-week.

Mortgage applications increased 10.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 8, 2025.

The Market Composite Index, a measure of mortgage loan application volume, increased 10.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 10 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 17 percent higher than the same week one year ago.

The Refinance Index increased 23 percent from the previous week and was 8 percent higher than the same week one year ago.

The 30-year fixed mortgage rate declined to 6.67 percent last week,which spurred the strongest week for refinance activity since April. Borrowers responded favorably, as refinance applications increased 23 percent, driven mostly by conventional and VA applications. Refinances accounted for 46.5 percent of applications and as seen in other recent refinance bursts, the average loan size grew significantly to $366,400. Borrowers with larger loan sizes continue to be more sensitive to rate movements.

You must be logged in to post a comment.