The delinquency rate on commercial mortgage-backed securities (CMBS) for offices spiked to 8.1% in July, the highest in 11 years.

The delinquency rate of office CMBS loans has QUADRUPLED in 1.5 years.

Delinquencies are currently rising at a faster pace than during the 2008 Financial Crisis. A top AAA-rated CMBS experienced a $40 million loss in May for the first time since the 2008 Financial Crisis.

While not an office, Edward Hopper painted some great real estate properties!

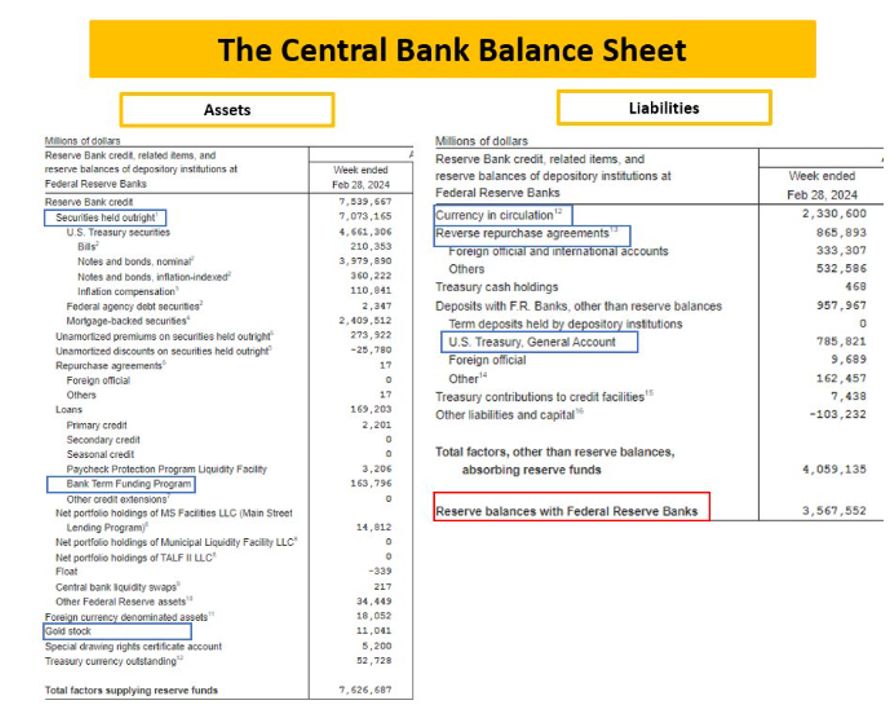

Kamala Harris, despite being VP for almost 4 years, is going to annouce her plans for taming inflation. Why doesn’t she do it now?? What Harris can’t control is The Federal Reserve that is losing money at breakneck speed.

Here is The Fed’s balance sheet.

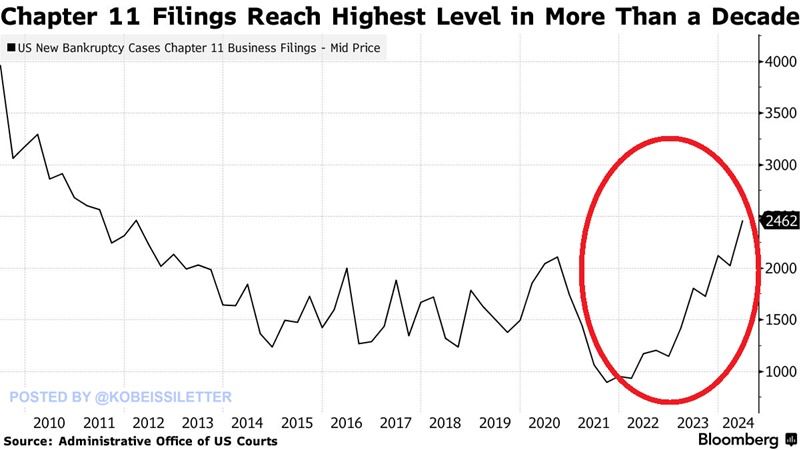

I shudder to think what Harris will propose to solve the highest bankrupty (Chap 11) rate in 13 years. Probably more Bidenomics (big wealth transfers to large corporations/donors).

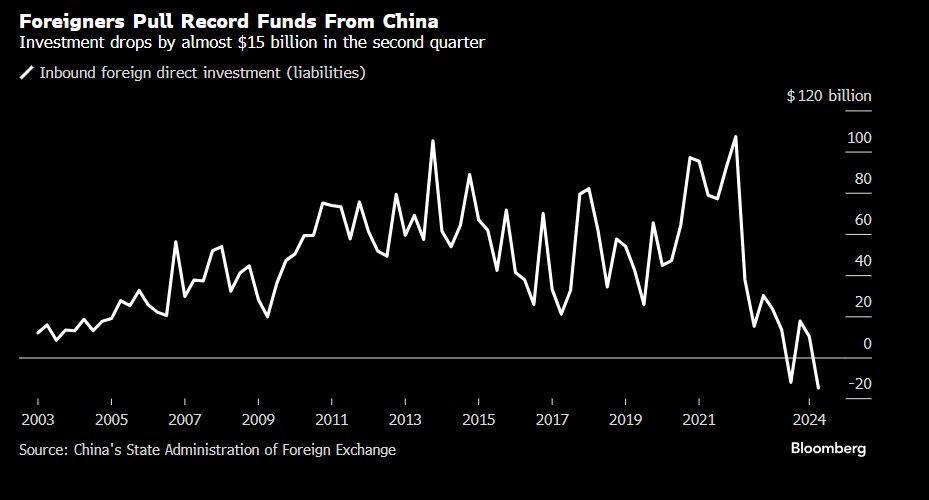

Meanwhile, foreigns pulled a record amount of funds from ailing China.

Kamala Harris will say anything to get elected, then fall back on her Communist agenda.

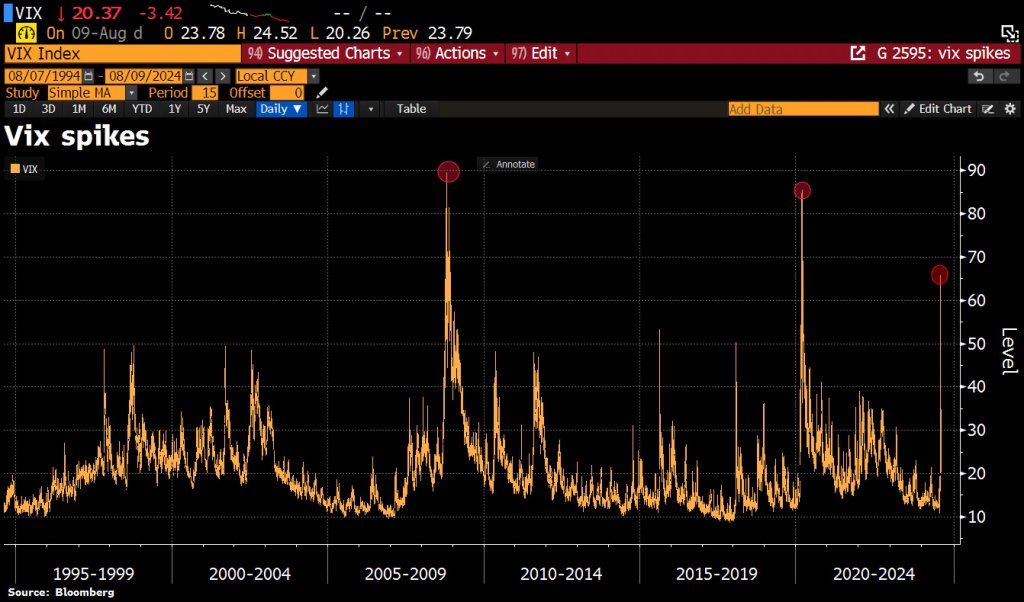

I have another use for VIX … to wipe out stock market gains. VIX is the S&P 500 volatility index, also known as “The Fear Index.”

Over the last 35yrs, the whole life of VIX history, there have only been 2 prior episodes of VIX trading >60: The 1st was during GFC, the collapse of Lehman, the 2nd episode occurred during Covid and we had a 3rd occurrence: that was last Monday.

The slowing US economy has a silver lining: Treasury and mortgage rates are declining. And the is spurring faster mortgage prepayments.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending August 2, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 0.3 percent compared with the previous week and was 11 percent lower than the same week one year ago.

The Refinance Index increased 16 percent from the previous week and was 59 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.55 percent from 6.82 percent, with points decreasing to 0.58 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The deciine in rates led to an increase in MBS convexity.

Remember the TV show “The Biggest :Loser”? That show was about weight loss.

Now The Federal Reserve has posted a record loss of $114 BILLION IN 2023.

The cause of the loss? Massive expansion of The Fed’s balance sheet coupled with rising interest rates. The two year track record of The Fed is truly appaling. With a bloated balance sheet, rising interest rates have caused staggering losses.

Mortgage applications decreased 3.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending July 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Note the decline in mortgage purchase demand after Biden/Harris were sworn into office in Janaury 2021.

The Refinance Index decreased 7 percent from the previous week and was 32 percent higher than the same week one year ago. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) remained unchanged at 6.82 percent, with points increasing to 0.62 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Because of rising rates under Biden/Harris economic policies, mortgage refinancing demand has gotten crushed.

We are in the latter half of the year, so seasonalility will kill off purchase mortgage demand compared to the Spring and early Summer.

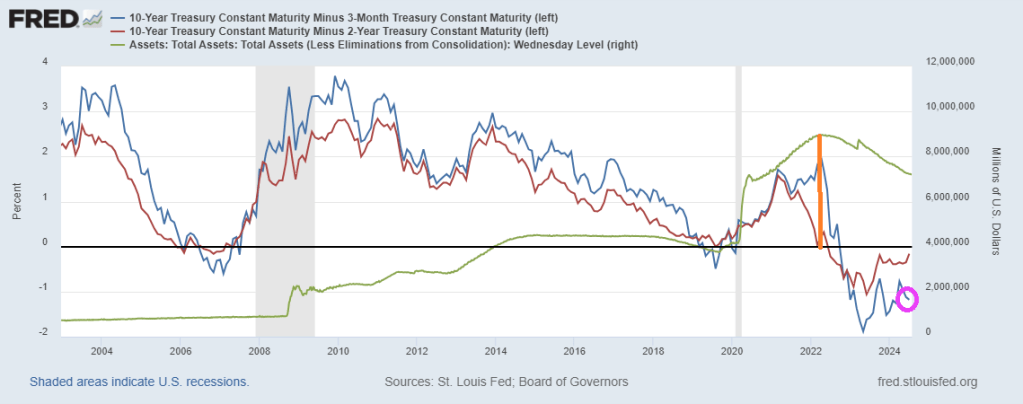

Up until 2022, the US Treasury yield curve behaved normally. In fact, as late as May 6th, 2022, the US Treasury 10Y-3M yield curve was at +227 basis points. Denote by the orange line in the following chart. That date corresponded with peak Fed balance sheet.

Then the massive spending by Biden/Harris/Congress hit the fan and inflation soared. The Fed counter attacked by raising rates and began scaling back their balance sheet. The 10Y-3M yield curve has been negative ever since.

Since the Covid outbreak in early 2020, The Fed went wild with rate cuts and massive and unpredented balance sheet expansion.

Let’s look at The Fed’s puchase of agency MBS and mortgage rates. From 2020 2022, The Fed continued to buy agency MBS. But in 2022, all hell broke loose as The Fed went crazy RAISING rates, but slowly began unwinding their balance sheet. The result? Mortgage rates began to climb. In fact, the US conforming mortgage rate for 30 years has risen 102% since early 2022. The Fed is only slowing unwinding their MBS holdings.

Despite the struggles in the residential housing market, the COMMERCIAL mortgage market is a trainwreck.

You must be logged in to post a comment.