Politicians love to scream about housing being simply unaffordable. Like mayor-elected Mandami in New York City. But the reality is that housing prices vary by city and there are more affordable cities than New York City to choose from. Federal policies should not be focused on letting people staying a particular city.

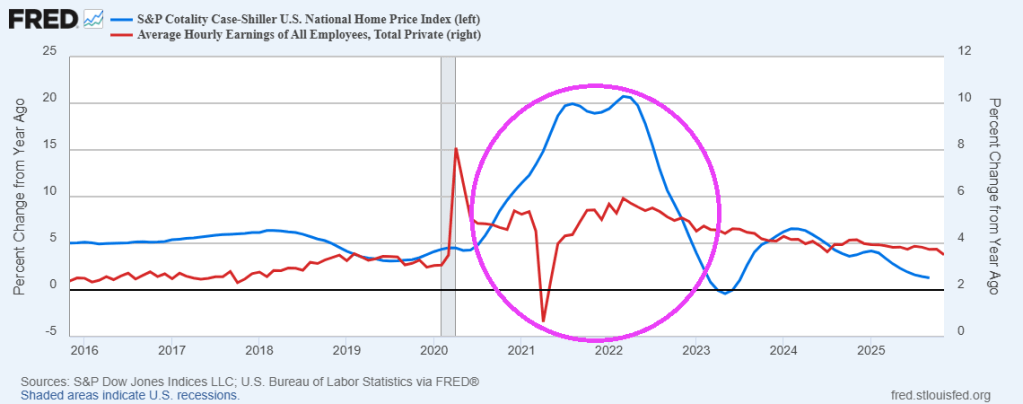

When we look at housing prices compared to average hourly earnings, we see housing prices rising with average hourly earnings … as expected.

If we look at year-over-year changes, we see the Covid bump in housing prices corresponding with the surge in Federal spending. But things have simmered down since the bump in 2020-2023.

My suggestion is for the Federal government to stop interfering in the housing market.

Hallelujah, I love this economy so! Of course, former First Lady Jill Biden is on the national tour trashing the economy saying it was “perfect” under Joe Biden.

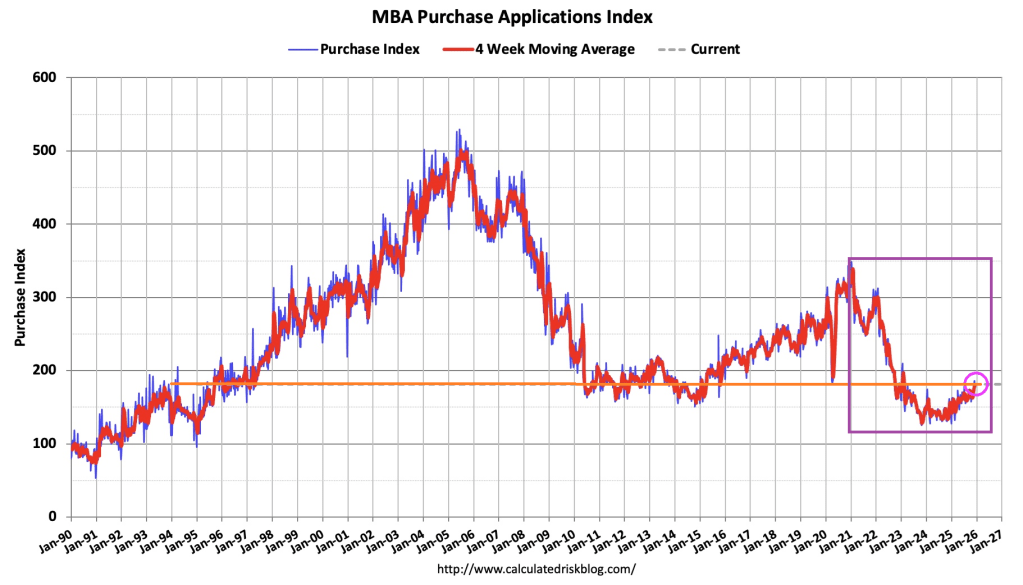

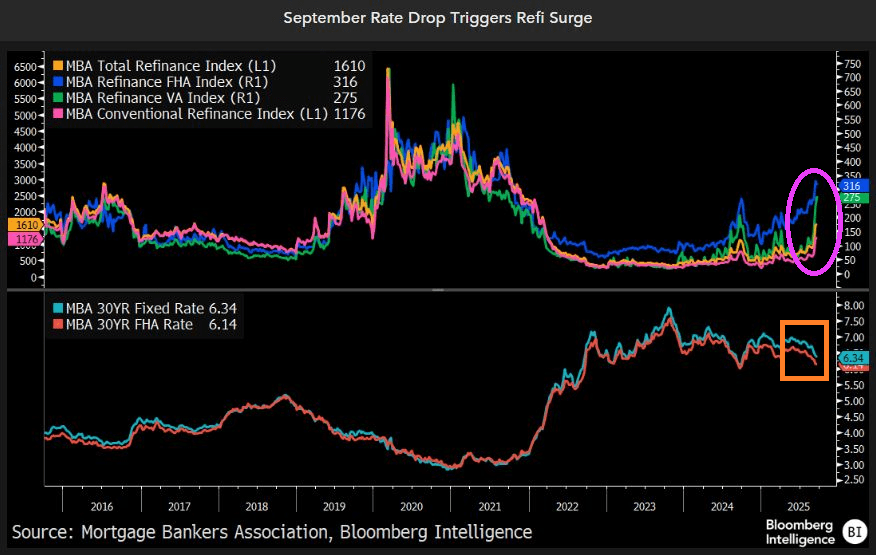

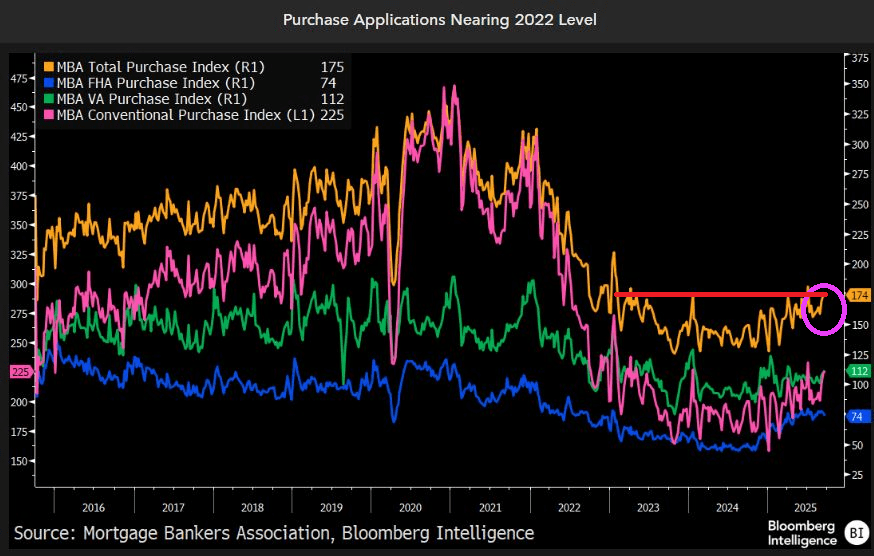

The Market Composite Index, a measure of mortgage loan application volume, increased 4.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 49 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index increased 32 percent compared with the previous week and was 19 percent higher than the same week one year ago.

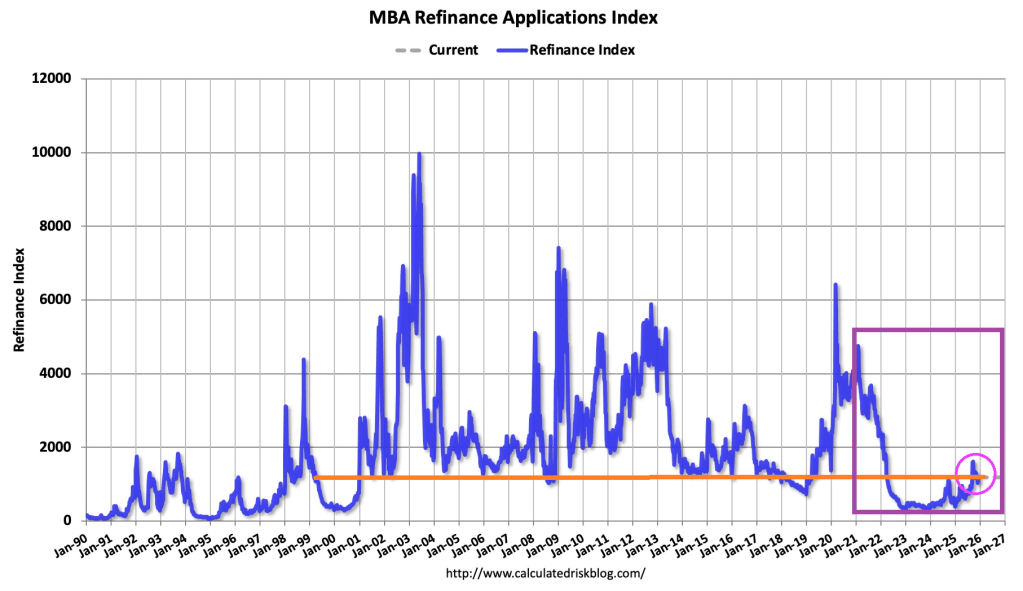

The Refinance Index increased 14 percent from the previous week and was 88 percent higher than the same week one year ago.

Compared to the prior week’s data, which included an adjustment for the Thanksgiving holiday, mortgage application activity increased last week, driven by an uptick in refinance applications,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Conventional refinance applications were up almost 8 percent and government refinances were up 24 percent as the FHA rate dipped to its lowest level since September 2024. Conventional purchase applications were down for the week, but there was a 5 percent increase in FHA purchase applications as prospective homebuyers continue to seek lower downpayment loans. Overall purchase applications continued to run ahead of 2024’s pace as broader housing inventory and affordability conditions improve gradually.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.33 percent from 6.32 percent, with points increasing to 0.60 from 0.58 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The good news / bad news for immigration enforcement is that home prices are declining as immigration enforcement keeps rolling. Good news for new homebuyers. Bad news for recent homeowners.

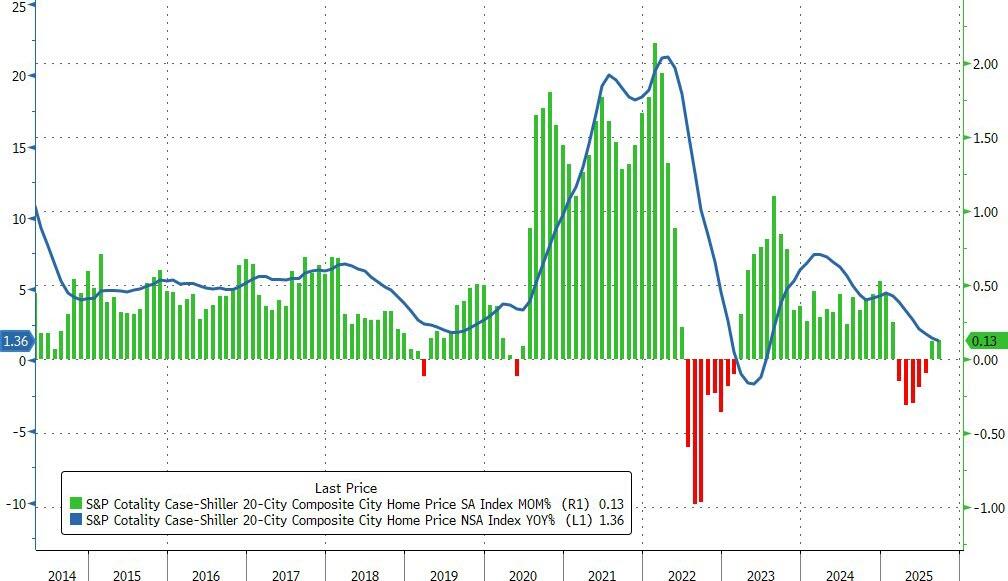

US home prices in the 20 largest cities rose 0.13% MoM in September (very slightly better than the 0.1% rise expected) and up for the second month in a row (after falling for five straight months before). This MoM rise left the average priers up just 1.36% YoY – the lowest since July 2023.

Source: Bloomberg

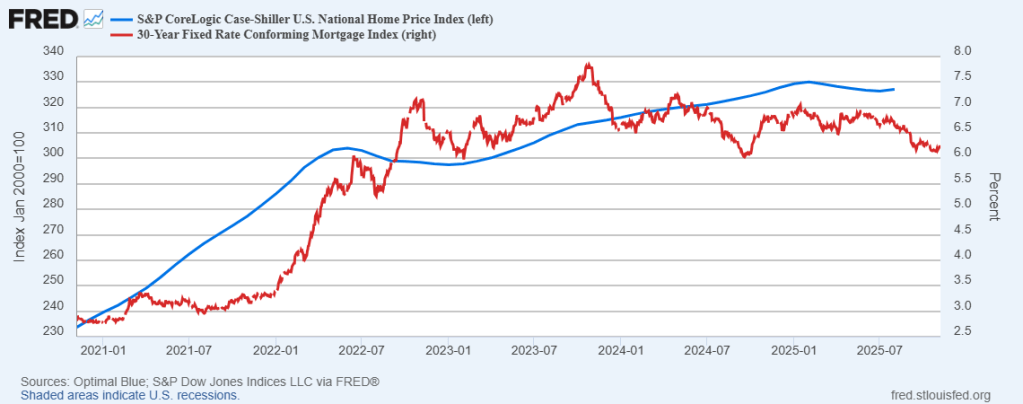

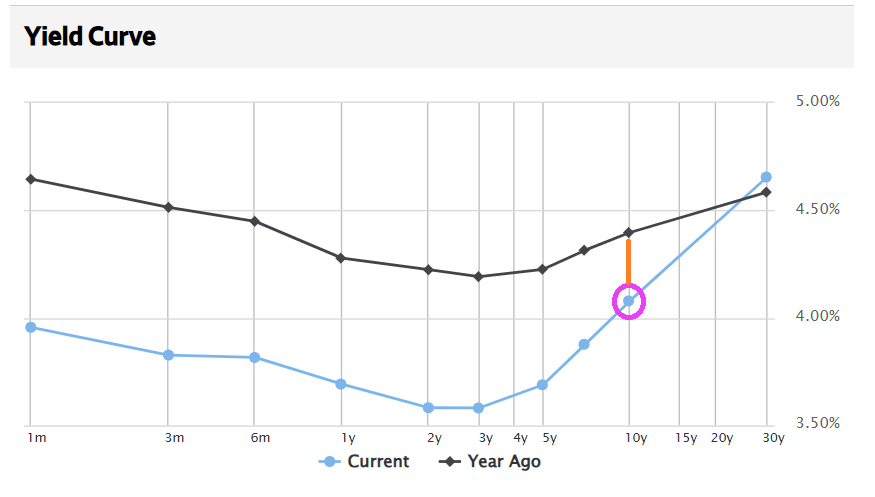

Declining mortgage rates suggest a rebound in aggregate prices could be looming…

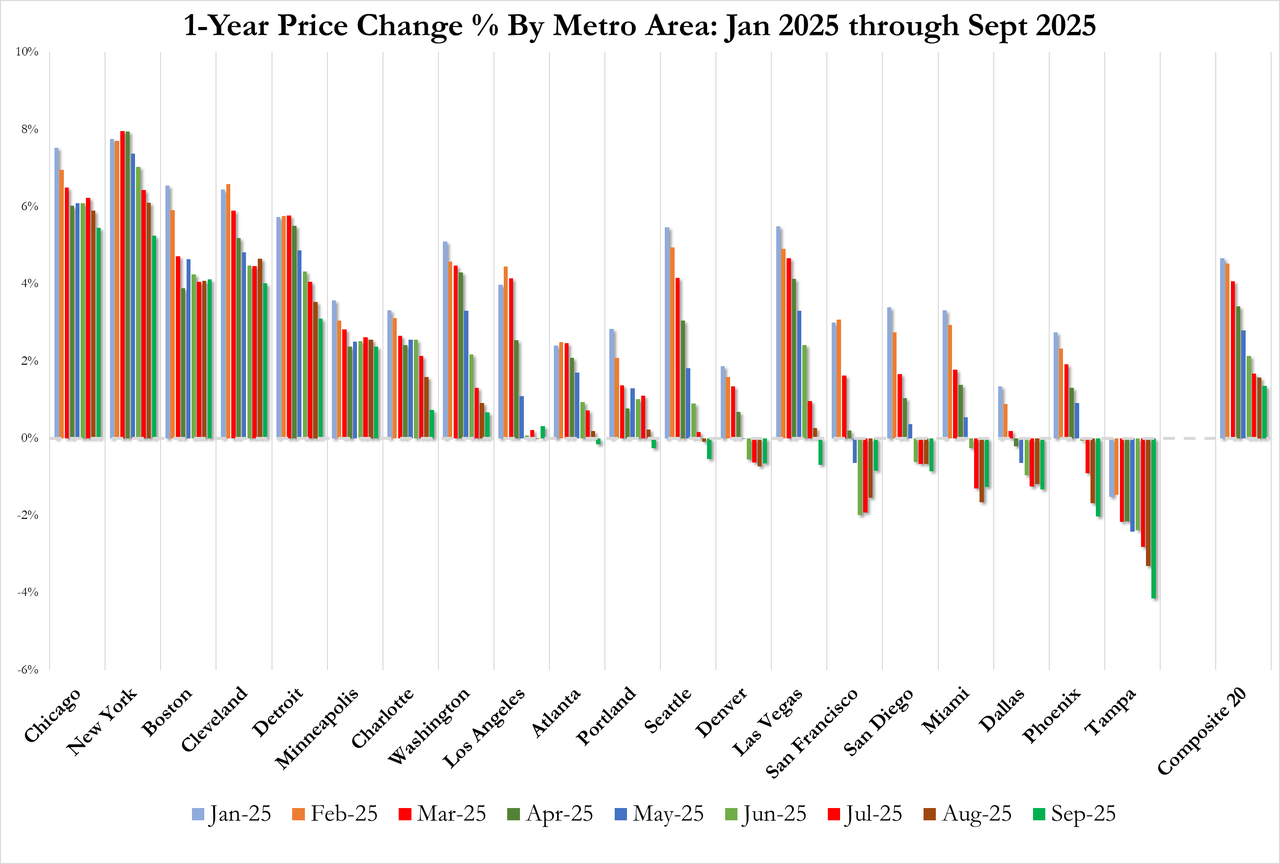

Regional performance reveals a tale of two markets.

Chicago continues to lead with a 5.5% annual gain, followed by New York at 5.2% and Boston at 4.1%. These Northeastern and Midwestern metros have sustained momentum even as broader market conditions soften.

At the opposite extreme, Tampa posted a 4.1% annual decline – the sharpest drop among tracked metros and its 11th consecutive month of negative annual returns. Phoenix (-2.0%), Dallas (-1.3%), and Miami (-1.3%) likewise remained in negative territory, highlighting particular weakness in Sun Belt markets that experienced the most dramatic pandemic-era price surges.

Home Prices are now falling (YoY) in a majority (11/20) of America’s largest cities…

“The geographic rotation is striking,” said Nicholas Godec, CFA, CAIA, CIPM, Head of Fixed Income Tradables & Commodities at S&P Dow Jones Indices.

Meanwhile, traditionally stable metros in the Northeast and Midwest continue to post solid gains, suggesting a reversion to prepandemic patterns where job markets and urban fundamentals drive appreciation rather than migration trends and remote-work dynamics.”

“Markets that were pandemic darlings—particularly in Florida, Arizona, and Texas—are now experiencing outright price declines.

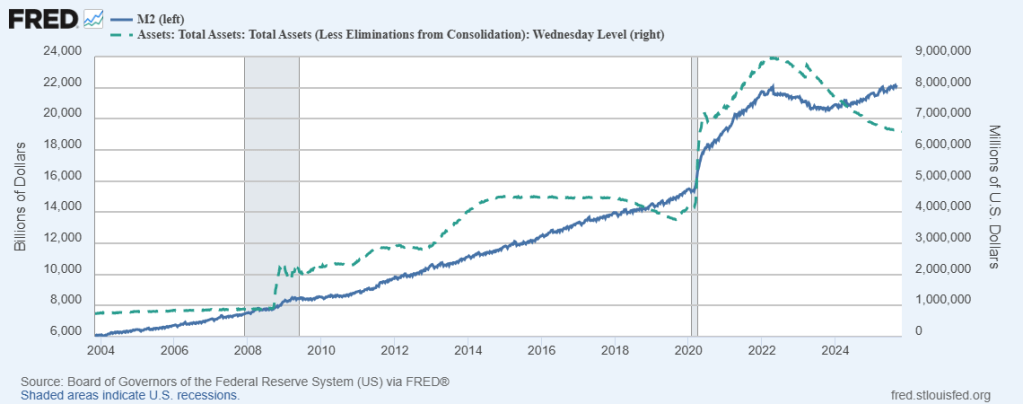

And don’t forget the surge in home prices associated with increased M2 money printing around Covid.

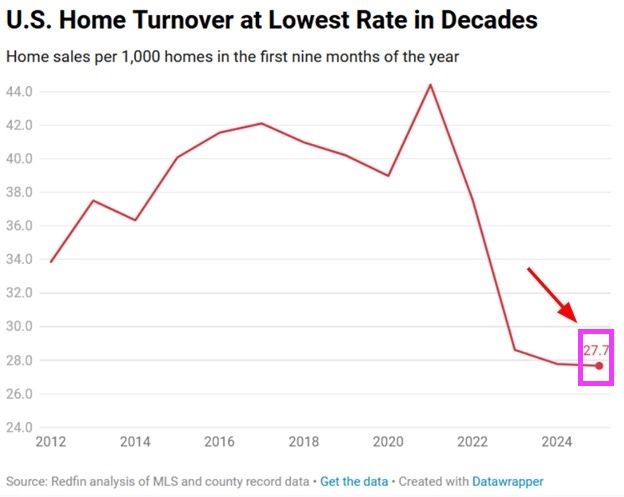

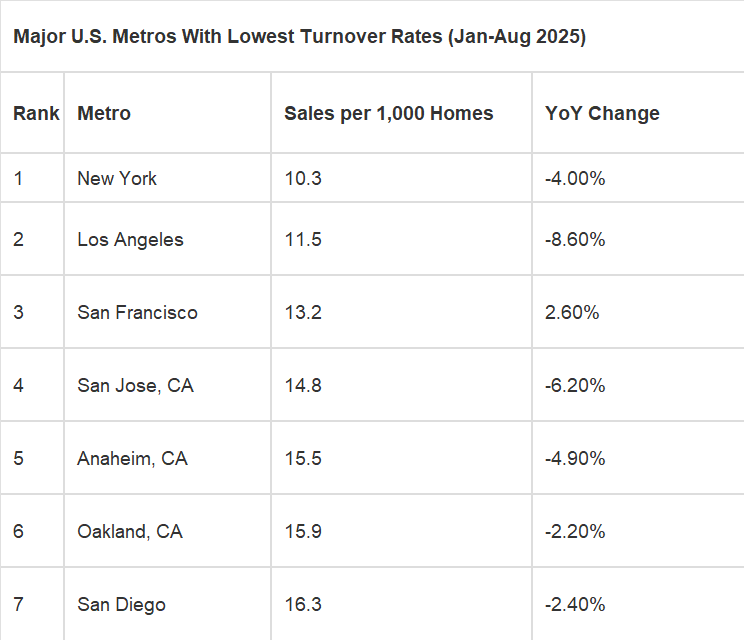

Just 2.8 homes out of every 1,000 changed owners in the first nine months of 2025—the lowest turnover rate in at least three decades. This marks a 38% plunge from the 2021 frenzy, when 44 per 1,000 homes sold, and is 44% below the pre-pandemic 2019 pace of 40 per 1,000.

Why the freeze? – Rate lock-in: Over 70% of homeowners are sitting on sub-5% mortgages and are reluctant to trade them for today’s rates exceeding 6%.

Sticker shock: Record prices combined with high borrowing costs have left many potential buyers on the sidelines. The result is a housing market that remains stagnant.

*Home prices are relatively high as are mortgage rates.

Someone will undoubtedly write me to look at Singapore. Yes, I know. Been there, done that. Or London.

In the US, the lowest turnover rates are in Democrat strongholds New York and California.

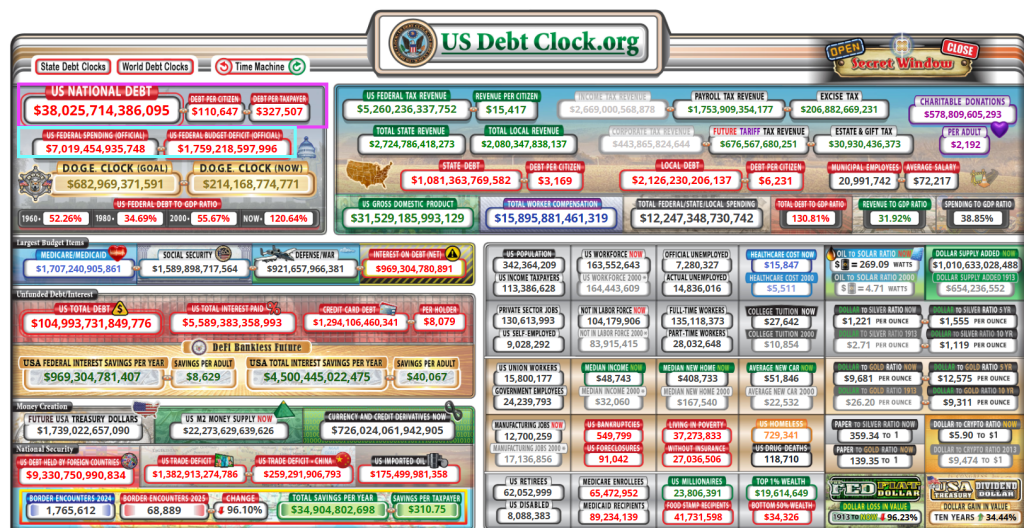

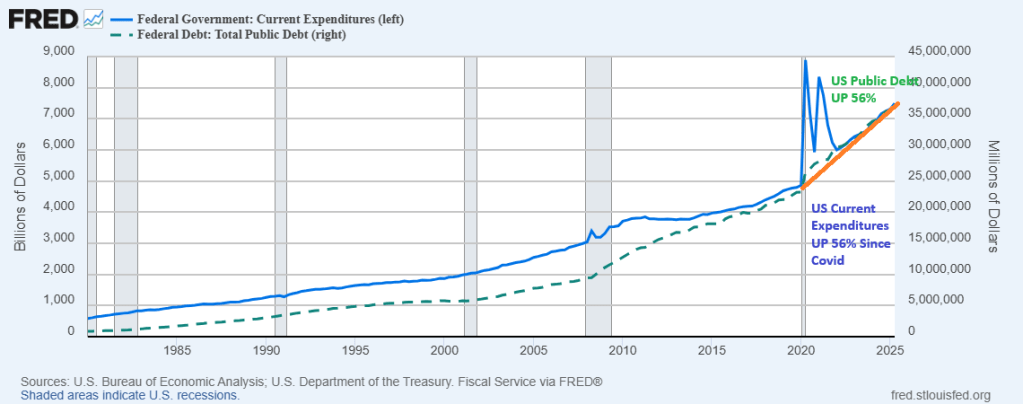

Of course, CPI data release has been delayed thanks to the US Federal government shutdown (aka, the Schumer Shutdown). But never fear, the Federal government is continuing to spending like the proverbial drunken sailors in port. The Federal debt just breached the $38 trillion mark.

And the Federal budget deficit just breached the $7 trillion mark. Why? Too much Federal spending! The Federal government COULD raises taxes, but that would strangle the economy. But politicians in DC are terrified of not being re-elected, so they are terrified of cutting spending.

The September drop in mortgage rates is sparking the biggest boom in refinancings since the pandemic. Mortgage-refinancing applications have surged above the decade average, despite that period including the record-breaking refi boom of 2020-21 when rates fell to all-time lows. Purchase-loan demand has also rebounded to its best for this time of year since 2022, yet remains well below pre-pandemic levels.

Can we ask the US House and Senate if they will ever return US Federal government spending to pre-Covid levels? Both US Federal government spending and public debt are up 56% since the Covid outbreak in 2020.

The answer is no. Politicians thrive on Federal spending.

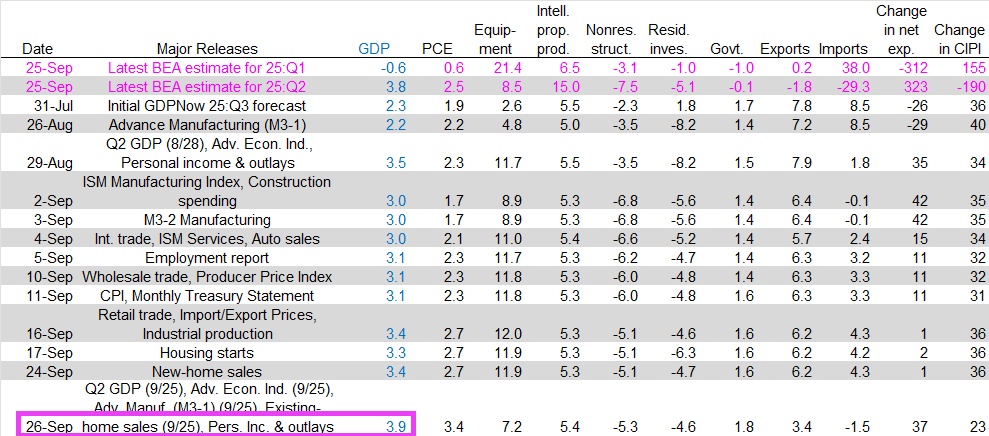

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.9 percent on September 26, up from 3.3 percent on September 17. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the National Association of Realtors, a decrease in the nowcast of third-quarter real gross private domestic investment growth from 6.4 percent to 4.1 percent was more than offset by increases in the nowcast of third-quarter real personal consumption expenditures growth from 2.7 percent to 3.4 percent and the nowcast of the contribution of net exports to third-quarter real GDP growth from 0.08 percentage points to 0.58 percentage points.

Existing home sales helped drive higher GDP growth.

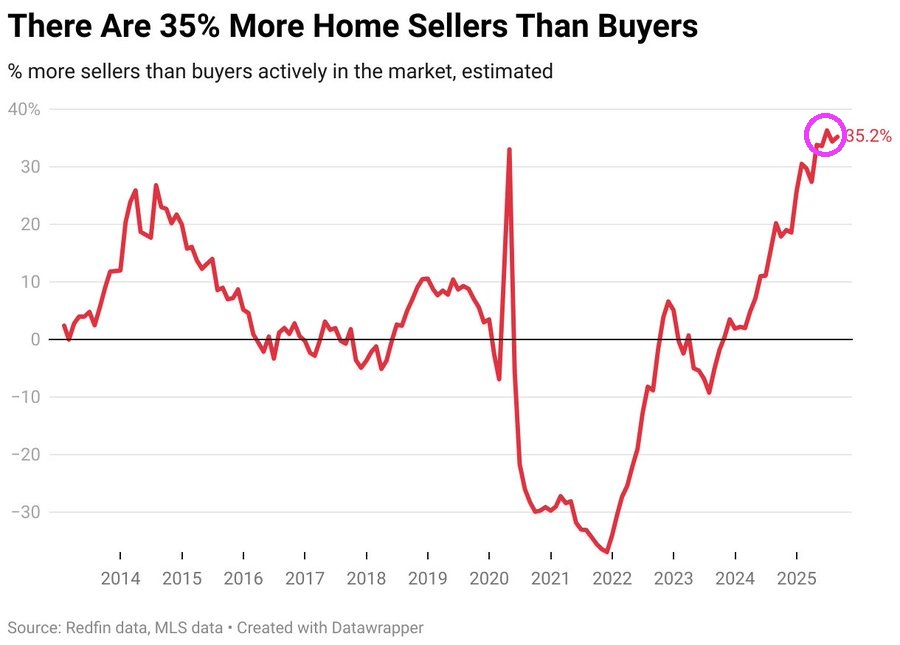

August represents a massive switch from 3 years ago when there were nearly 40% more home buyers and sellers in the US housing market. There are now 35.2% MORE home sellers than buyers!

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.