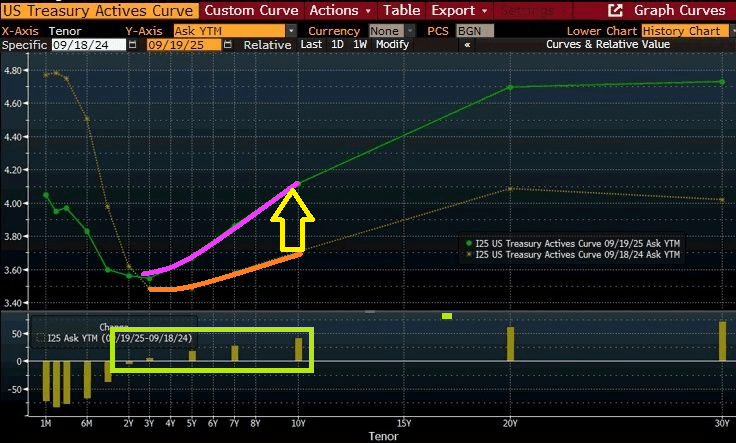

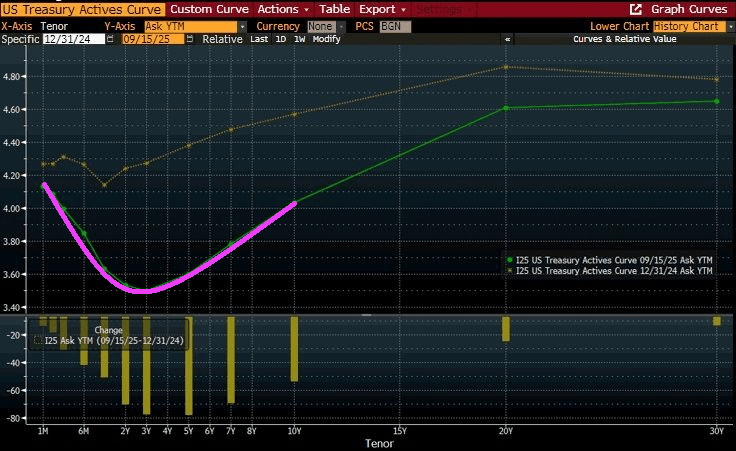

It’s Friday and the US Treasury yield curve is rising/steepening at the 10-year tenor.

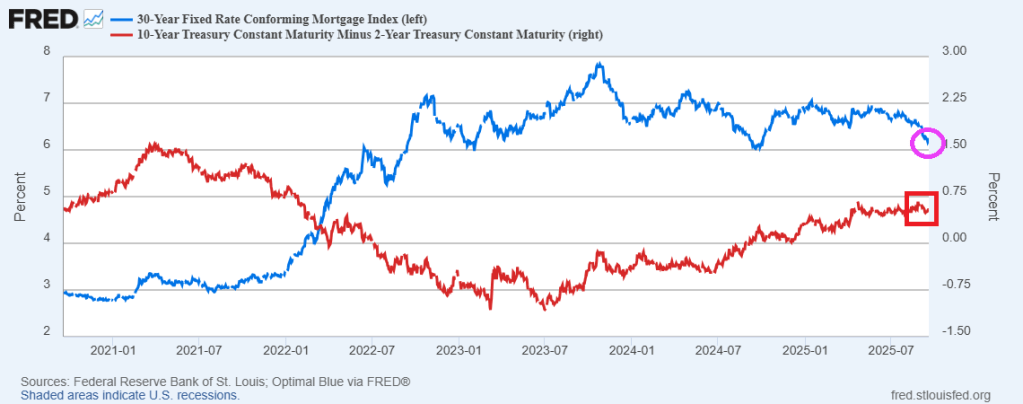

As of yesterday, the 30-year mortgage rate fell to 6.17%

Thanks in part to Funky Cold Jerome!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

It’s Friday and the US Treasury yield curve is rising/steepening at the 10-year tenor.

As of yesterday, the 30-year mortgage rate fell to 6.17%

Thanks in part to Funky Cold Jerome!

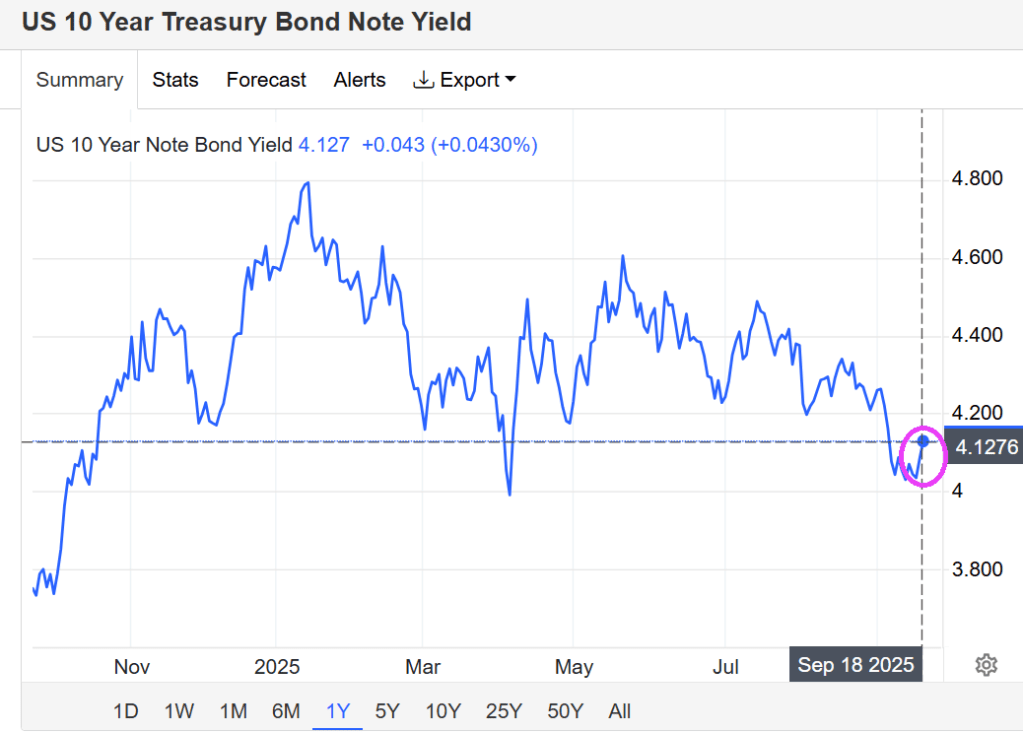

Fed Chair Jerome Powell is the God of Hellfire! We should always wait a day to digest Fed’s annoucements since they often make little sense. For example, yesterday the 10Y yield fell below 4% after The Fed’s announcement … then promplty rose above 4% again. And today, the US Treasury 10Y yield rose to 4.1276%

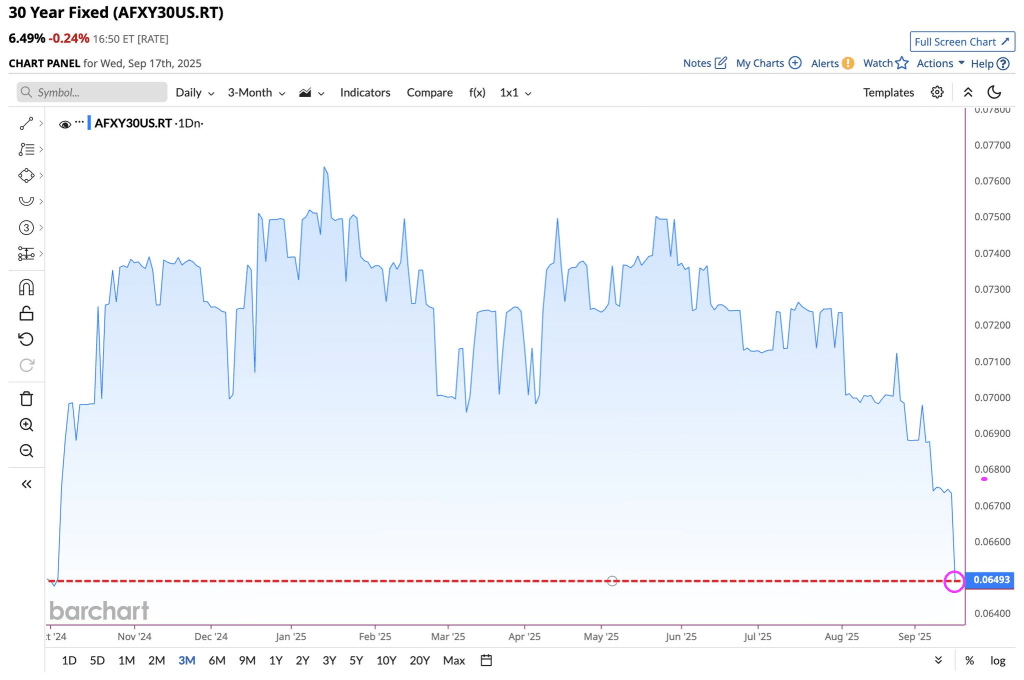

The 30Y US mortgage rate fell to 6.493%.

How about the US Dollar? Similar to the US 10Y yield, volatility reigned following Powell’s muddled message.

Powell rarely is straightforward and never puts cash on the barrelhead.

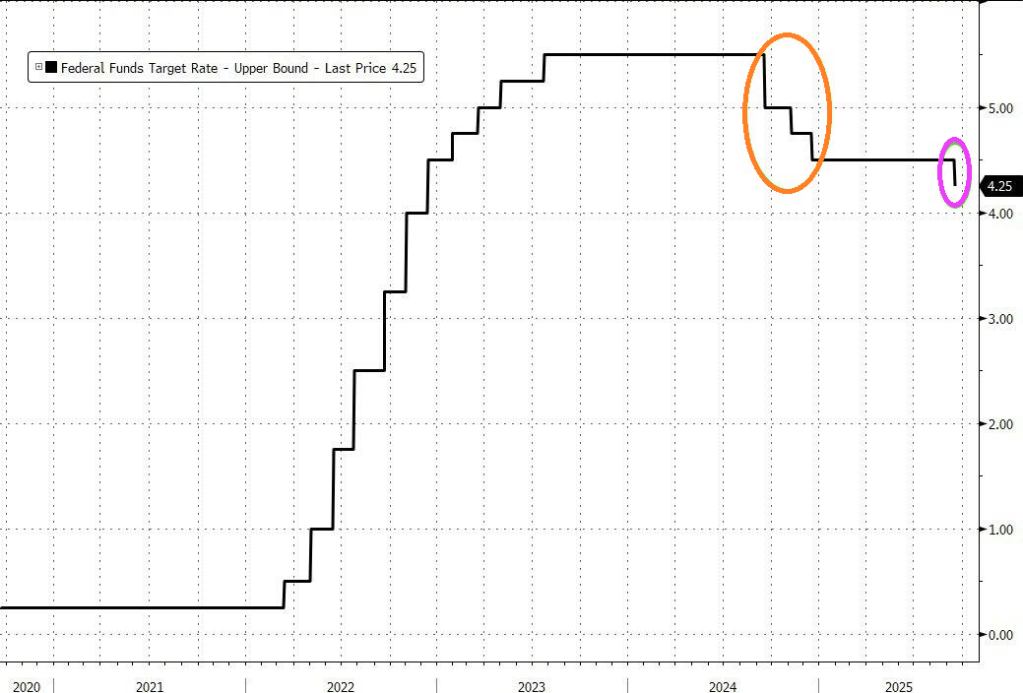

Well, The Fed cut their target rate by 25 basis points.

Following The Fed’s 25 bp cuts, the 10Y yield fell below 4% to 3.9879%.

The Fed Dots??

We shall see tomorrow if mortgage rates fall.

Of course, as soon as I posted this, US Treasury 10Y yields surged. This often happens with The Fed’s incompetent messaging.

Participants in the mortgage market are hoping for relief in the mortgage market when The Fed lowers rates tomorrow.

But the reality is the the bond market is expecting declining short-term rates, but not much change at the 10-year tenor.

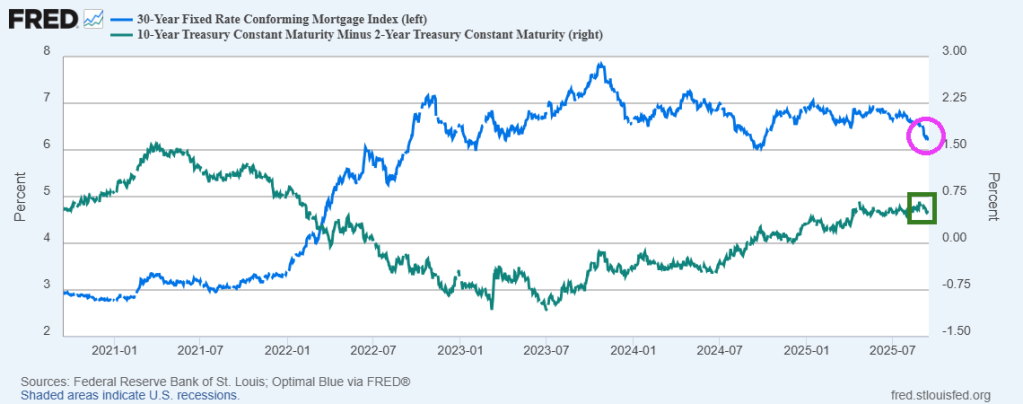

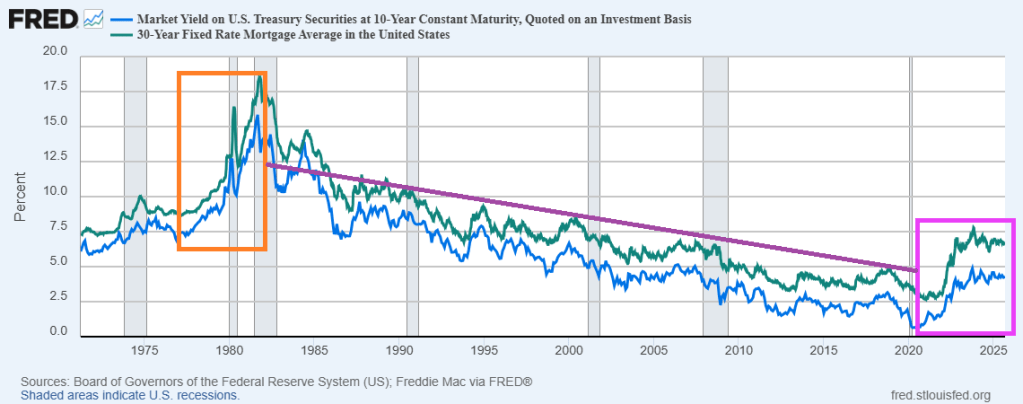

Mortgage rates have fallen since October 23, 2023 as the yield curve has gradually steepened.

So don’t be surprised if The Fed cuts rates tomorrow and there is little or no reaction in mortgage rates.

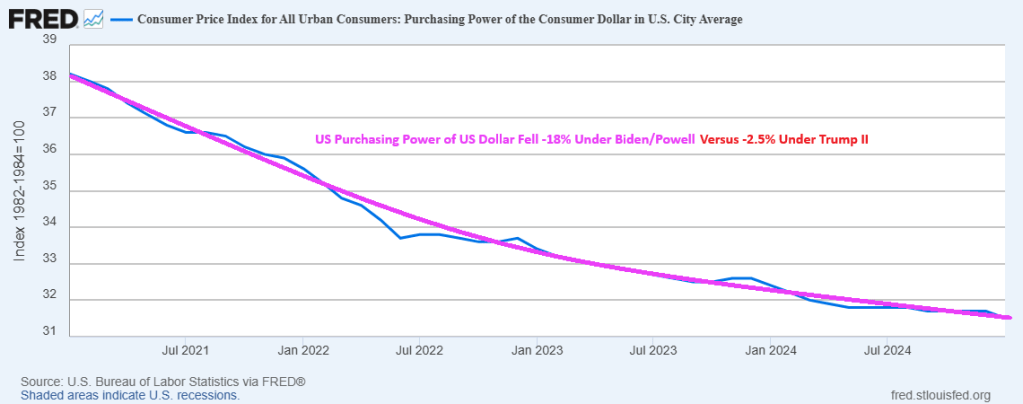

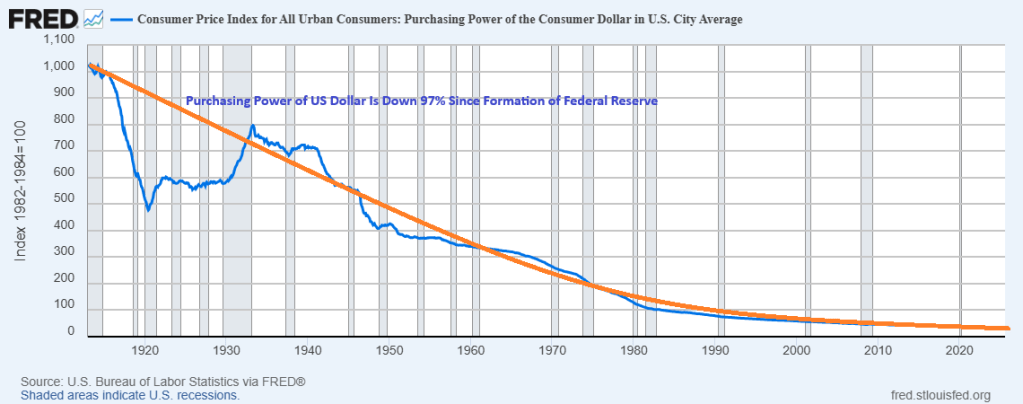

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913. It is the House of the Dying Dollar.

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913.

Of course, Trump II is only 9 months old and Biden had 4 long years to destroy the dollar.

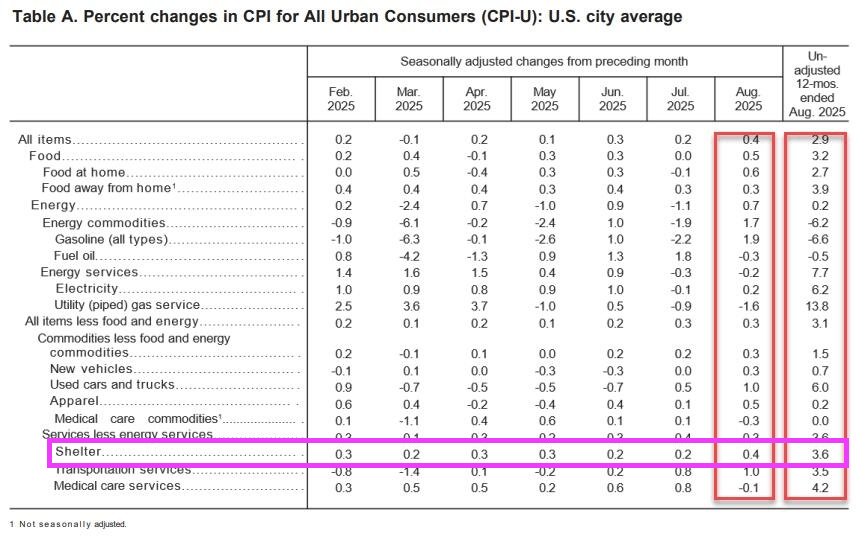

According to the Bureau of Labor Statistics (BLS), headline inflation rose 0.4% MoM and 2.9% YoY in August.

Shelter (housing) is up 3.6% YoY. Gimme (expensive) shelter!

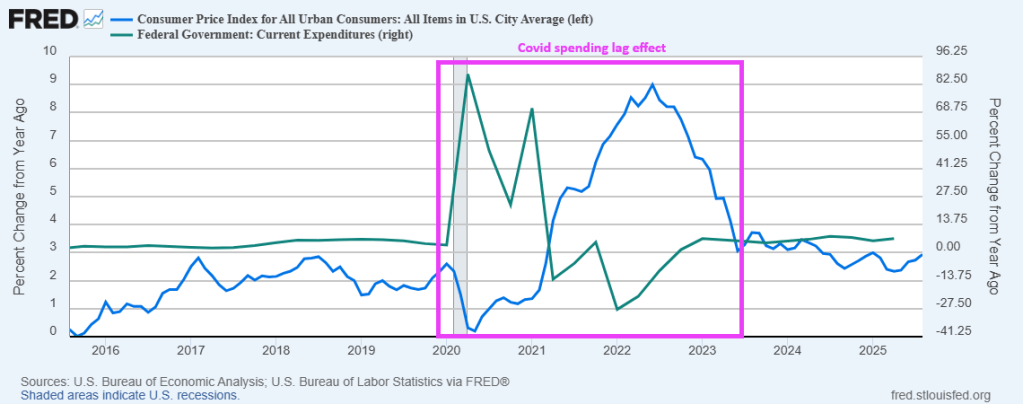

Of course, Federal government spending is the source of inflation. Notice the lag between Covid spending and resulting inflation.

So much for Trump Tariffs causing runaway inflation.

Prayers for Charlie Kirk and his family. I hope they catch the sick SOB that assassinated Charlie.

Stay with the mortgage market! It is improving under Trump after a disastrous run under Biden.

But for last week, mortgage applications increased 9.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 5, 2025. This week’s results include an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 9.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 23 percent higher than the same week one year ago.

The Refinance Index increased 12 percent from the previous week and was 34 percent higher than the same week one year ago.

The holiday-adjusted refinance index had its strongest week in a year and the average loan size for refinances also increased significantly, since borrowers with large loans are more sensitive to bigger rate moves. Refinance applications accounted for almost 49 percent of all applications last week.

…

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.49 percent from 6.64 percent, with points decreasing to 0.56 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

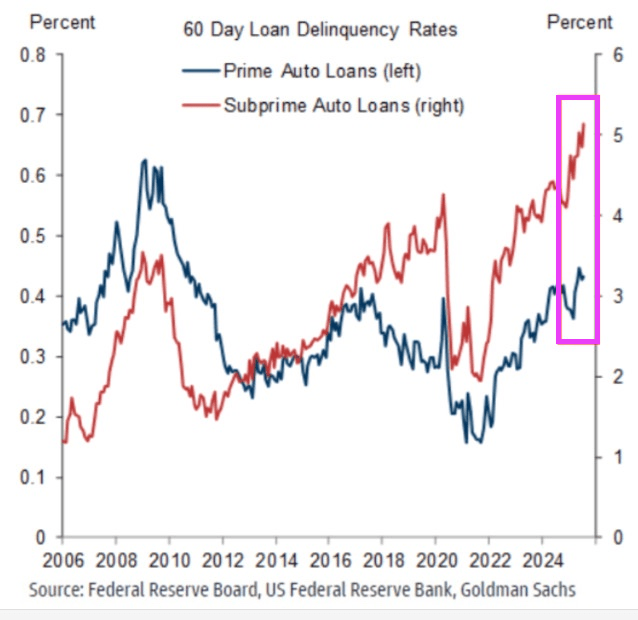

The car market bubble is bursting! Subprime auto loan delinquency rates have now surpassed 5% for the first time in history. The 60-day delinquency rate for subprime auto loans has more than DOUBLED over the last 3 years. Delinquency rates are now ~1.5 percentage points above the 2008 Financial Crisis peak. At the same time, prime auto loan delinquencies rose to their highest in 15 years. Meanwhile, the total value of auto loans in the US jumped $13 billion, to a record $1.66 trillion in Q2 2025. An auto debt crisis is brewing.

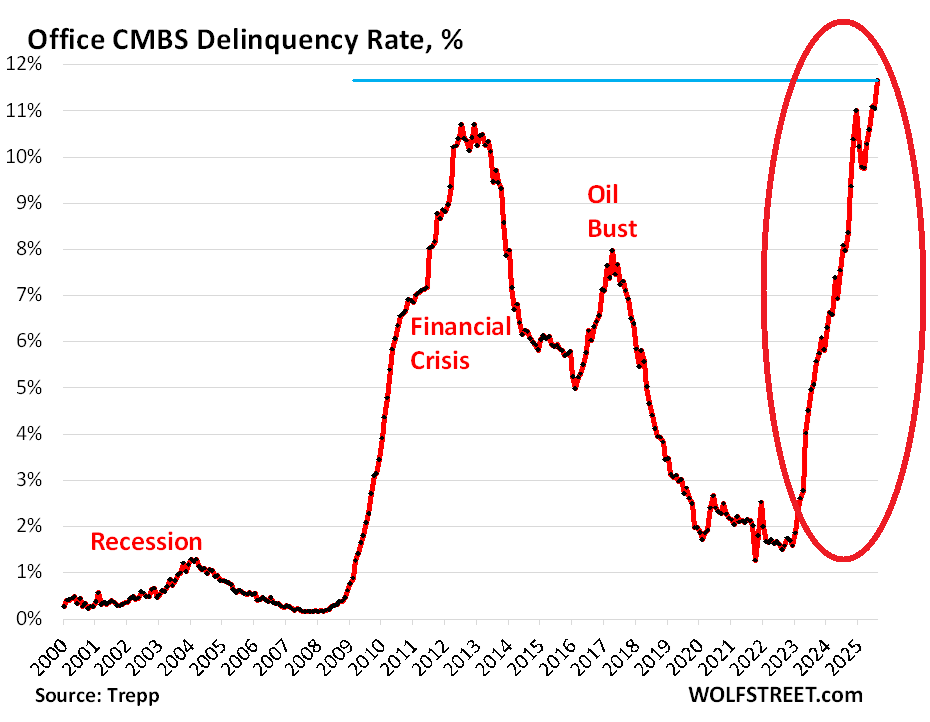

The office CMBS delinquency rate is at an all-time high.

Not exactly the Guns Of August. More like a wet cap gun firing.

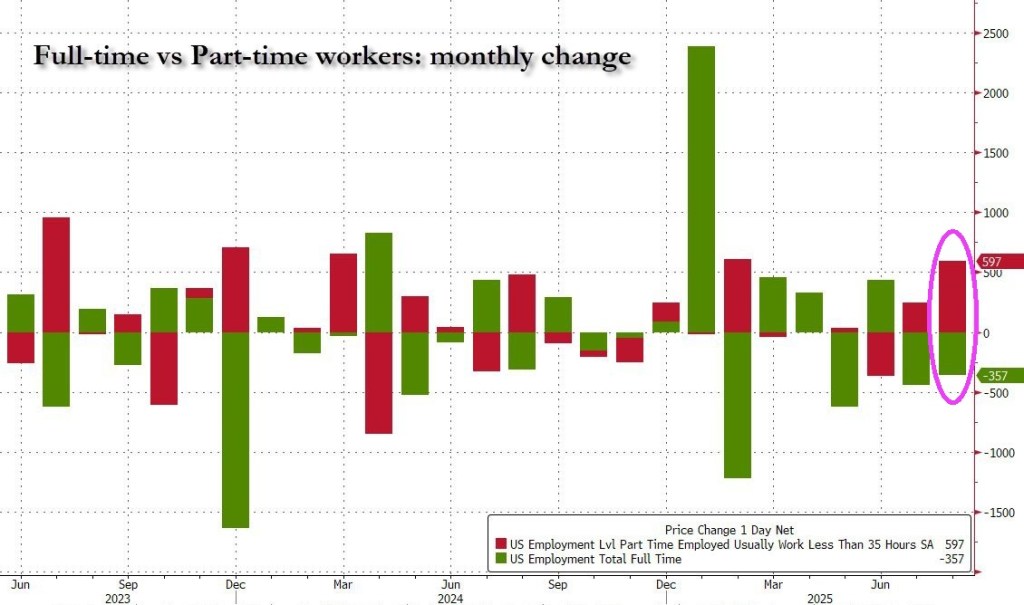

The jobs report for August showed only 22k jobs added.

U-3 unemployment rate rose to 4.3%. U-6 unemployment and part-time rose to 8.1%.

Total private jobs added was 38k while manufacturing jobs added was down -12k.

Government jobs dropped -16k.

It gets worse! All of the jobs added were PART-TIME!

It gets even worse: native-born workers plunged by 561K, the biggest one month drop since August 2024. Foreign-born workers increased by 50K, the first increase since March.

Let’s see if The Fed drops the hammer on rates by 50 basis points.

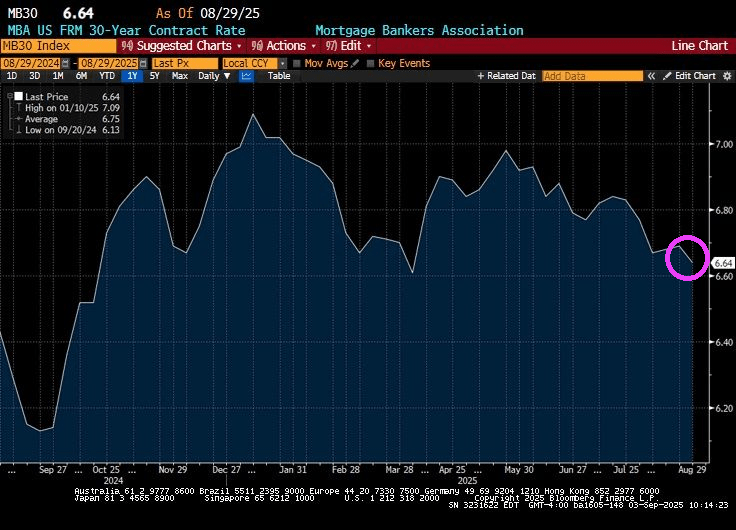

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

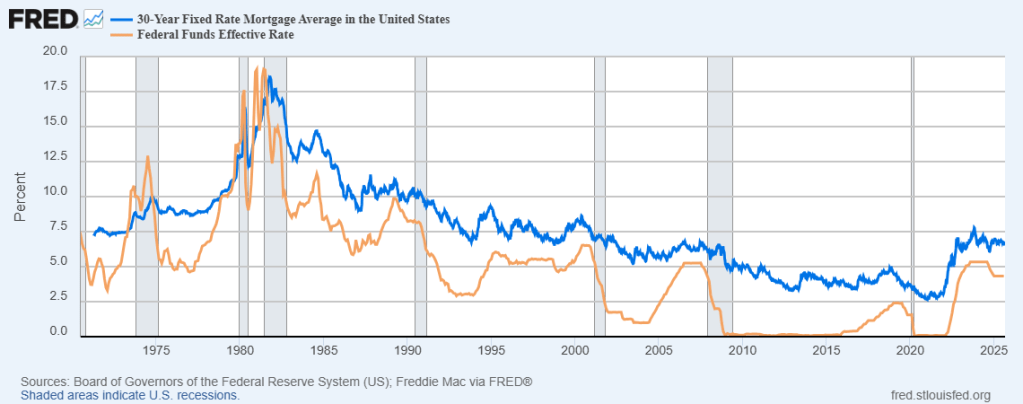

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

Here is a video of Fed Chair Jerome Powell trying to lower mortgage rates.

What about the mortgage rates, Fawlty?

You must be logged in to post a comment.