But for last week, mortgage applications increased 9.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 5, 2025. This week’s results include an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 9.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 23 percent higher than the same week one year ago.

The Refinance Index increased 12 percent from the previous week and was 34 percent higher than the same week one year ago.

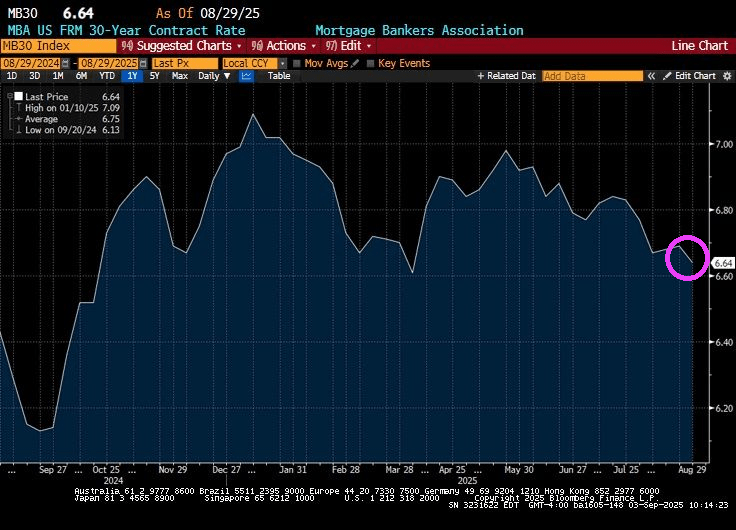

The holiday-adjusted refinance index had its strongest week in a year and the average loan size for refinances also increased significantly, since borrowers with large loans are more sensitive to bigger rate moves. Refinance applications accounted for almost 49 percent of all applications last week. … The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.49 percent from 6.64 percent, with points decreasing to 0.56 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

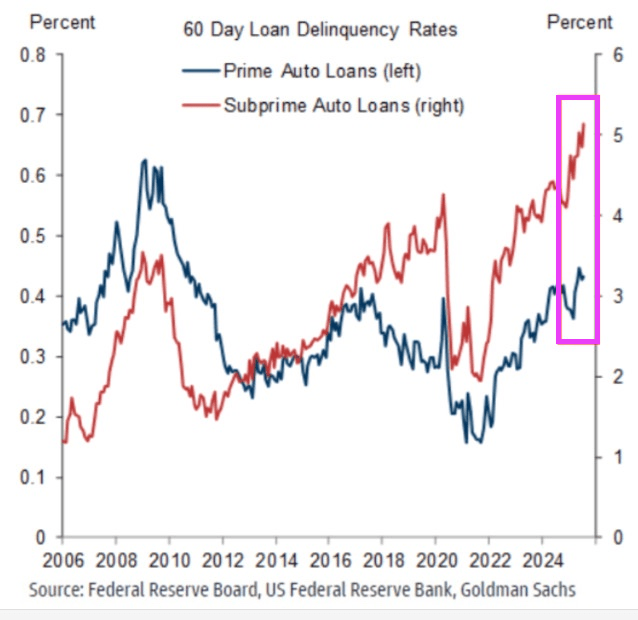

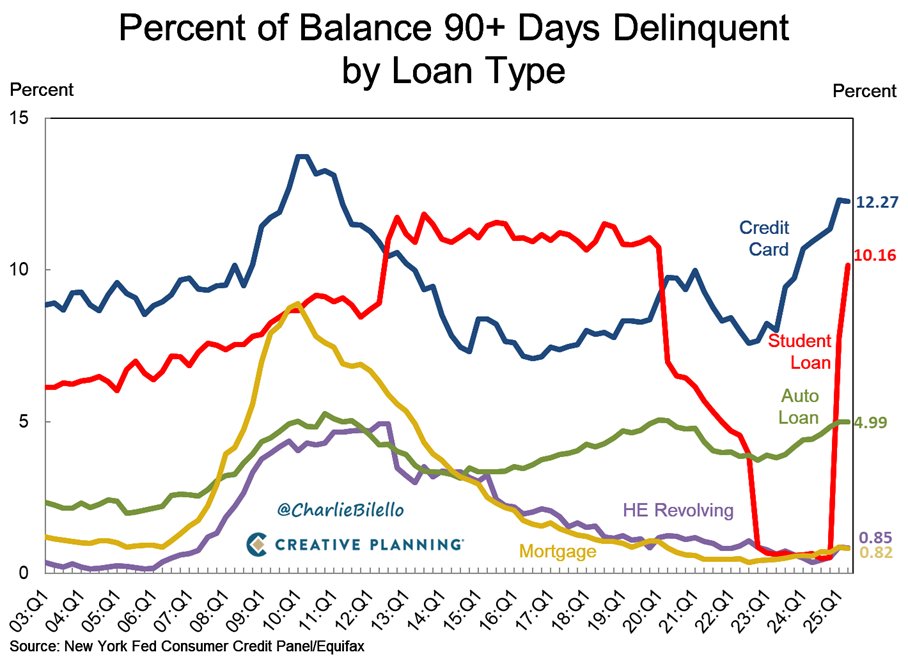

The car market bubble is bursting! Subprime auto loan delinquency rates have now surpassed 5% for the first time in history. The 60-day delinquency rate for subprime auto loans has more than DOUBLED over the last 3 years. Delinquency rates are now ~1.5 percentage points above the 2008 Financial Crisis peak. At the same time, prime auto loan delinquencies rose to their highest in 15 years. Meanwhile, the total value of auto loans in the US jumped $13 billion, to a record $1.66 trillion in Q2 2025. An auto debt crisis is brewing.

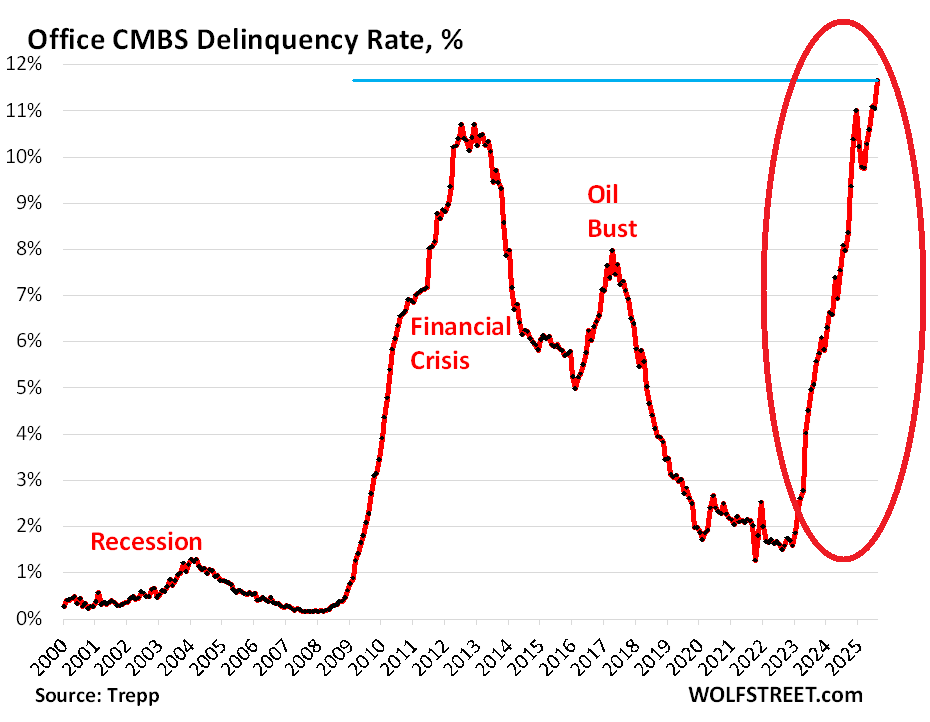

The office CMBS delinquency rate is at an all-time high.

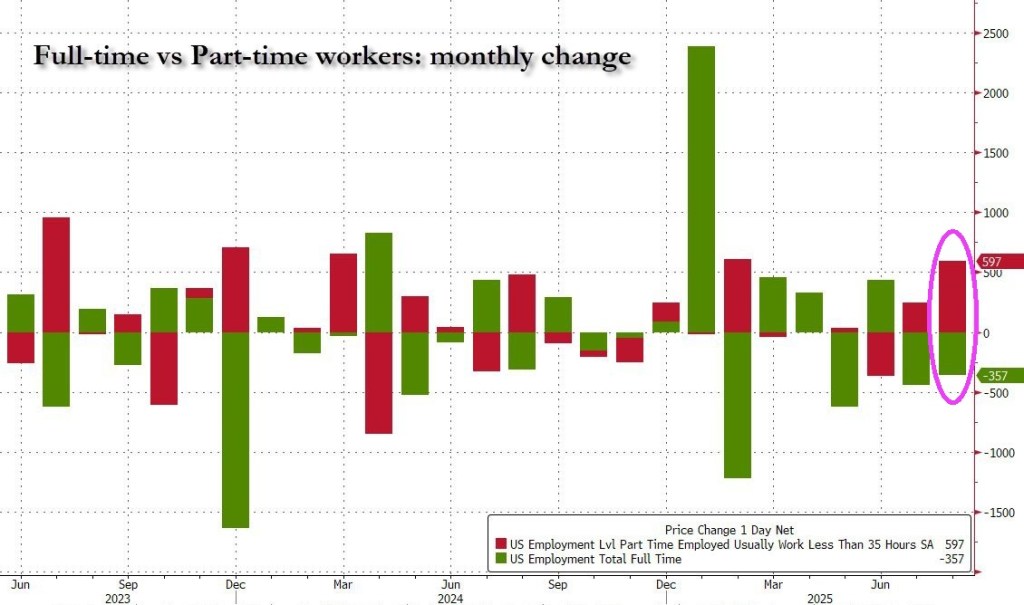

U-3 unemployment rate rose to 4.3%. U-6 unemployment and part-time rose to 8.1%.

Total private jobs added was 38k while manufacturing jobs added was down -12k.

Government jobs dropped -16k.

It gets worse! All of the jobs added were PART-TIME!

It gets even worse: native-born workers plunged by 561K, the biggest one month drop since August 2024. Foreign-born workers increased by 50K, the first increase since March.

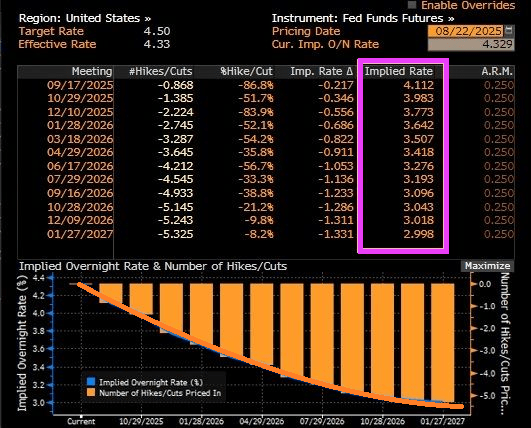

Let’s see if The Fed drops the hammer on rates by 50 basis points.

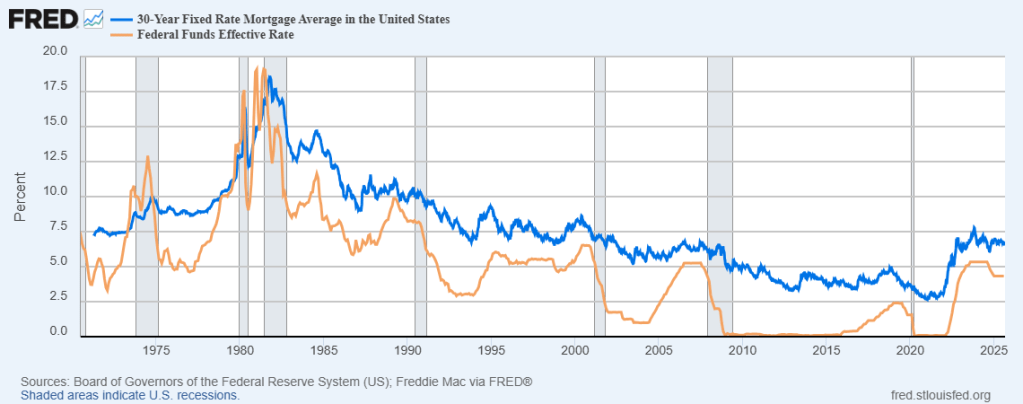

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

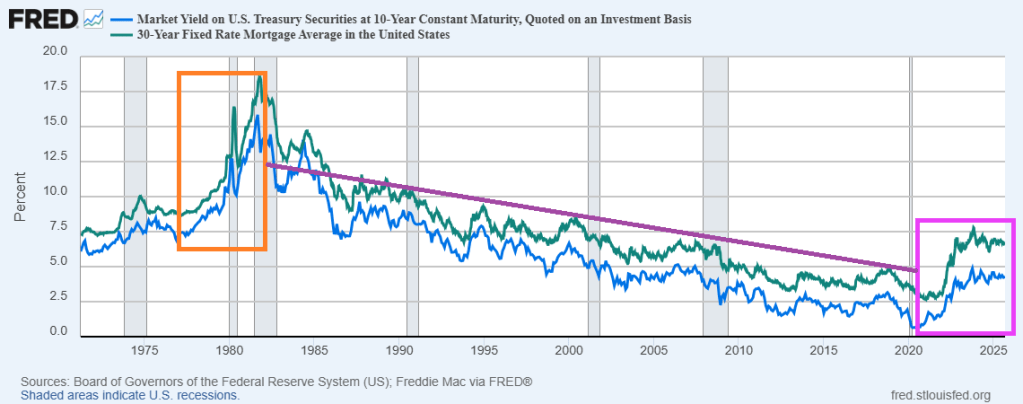

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

S&P Global’s US Manufacturing PMI rose dramatically from 49.8 in July to 53.0 in August (down very marginally from its preliminary print of 53.3) – the strongest in over three years.

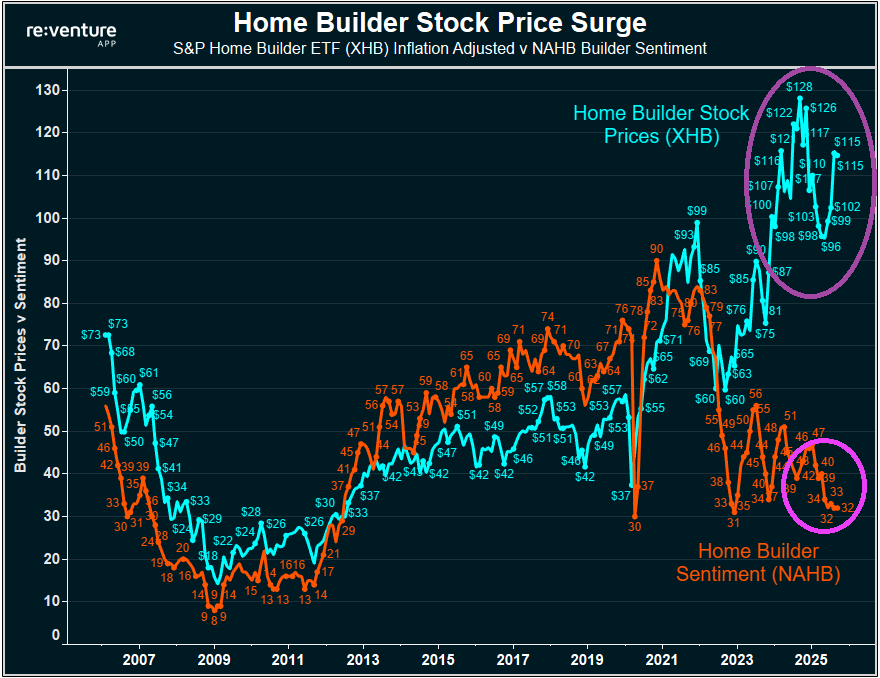

Home builder stock prices have surged, while home builder sentiment has plunged.

Of course, The Fed’s endless money printing isn’t helping the supply side of home building.

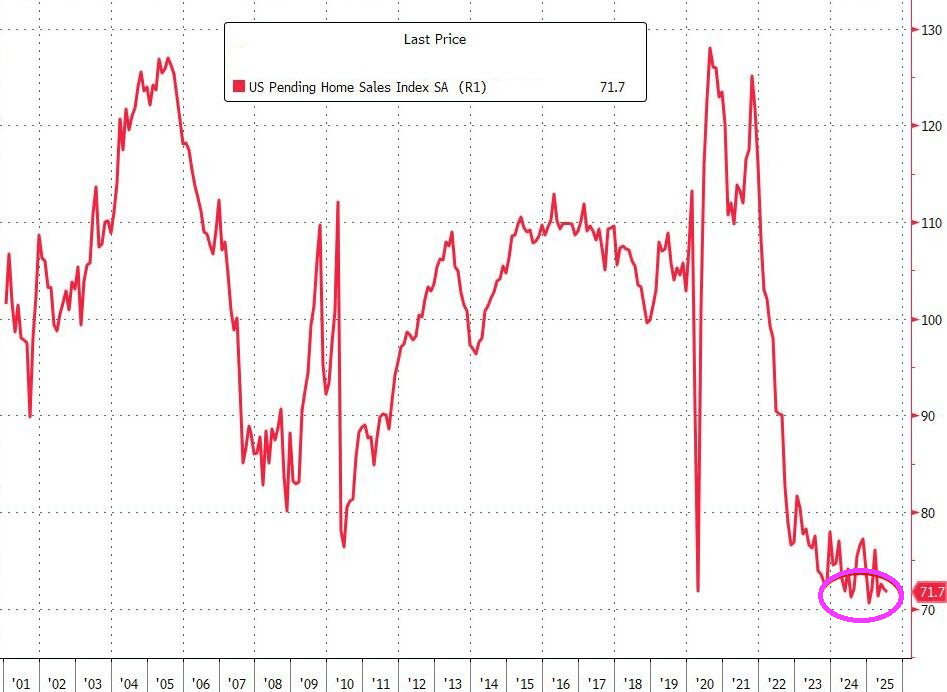

To make matters worse, pending home sales remain in the doldrums.

Federal Reserve Board member Lisa Cook is an embarrasment for committing mortgage fraud, then refusing to step down. And now she has filed a lawsuit against the Trump Administration for wrongful termination. Typical of an Obama appointee!

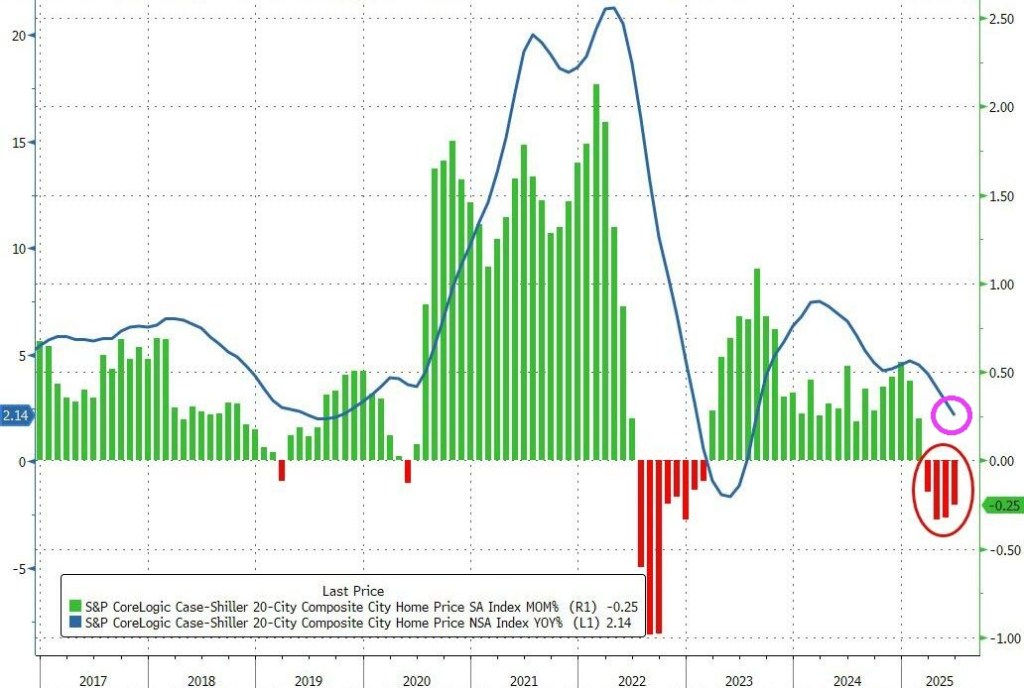

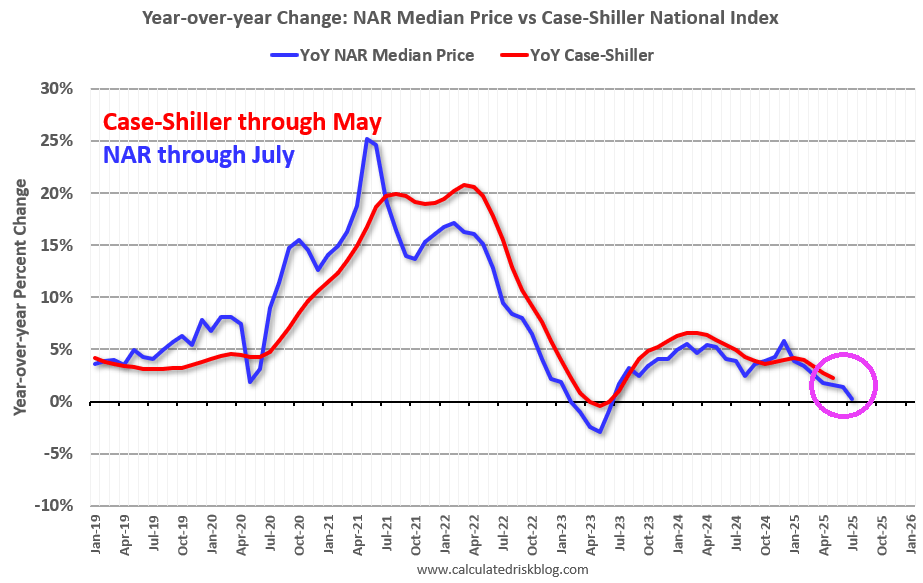

Home prices in America’s 20 largest cities fell for the 4th straight month in June (the latest data available from S&P CoreLogic’s Case-Shiller data released this morning).

The -0.25% MoM drop was larger than expected and dragged the YoY price growth down to +2.15% – the weakest since July 2023.

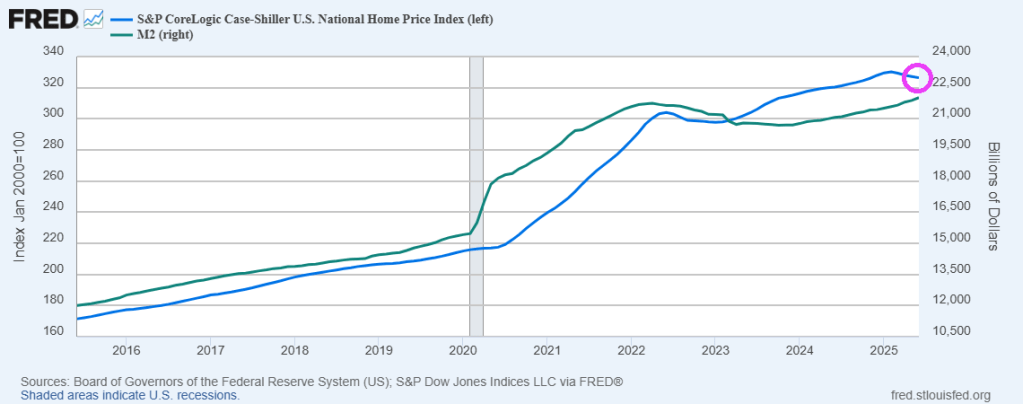

Meanwhile The Federal Reserve keeps on printing money, helping to drive up home prices.

,Metro level? New York and Chicago lead, with Phoenix, Miami, Denver, San Diego, Dallas, San Francisco and Tampa all experiencing price declines.

On a side note, Chicago is even more unaffordable than last year. So much for Mayor Brandon Johnson saying there would be no crime if everyone could afford housing (one of the stupidest comments I have ever heard).

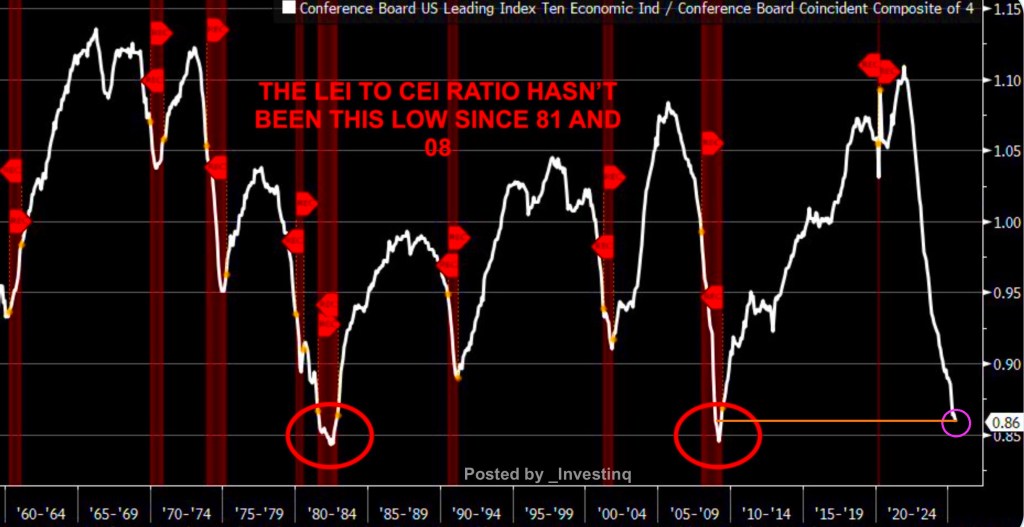

The Fed will have to whip it good with rate cuts if the recession warnings are an indicator of what lies ahead for the US economy.

The ratio of The Conference Board’s Leading Economic Indicators (LEI) vs. The Conference Board’s Coincident Economic Index (CEI) ratio hasn’t been this low since 2008.

Fed Funds Futures are signalling rate cuts at the September 17th FOMC meeting and December 10th meetings.

Month-over-month sales increased in the Northeast, South, and West, and fell in the Midwest. Year-over-year, sales rose in the South, Northeast, and Midwest, and fell in the West.

• 2.0% increase in existing-home sales – seasonally adjusted annual rate of 4.01 million in July.

• Year-over-year: 0.8% increase in existing-home sales

Median existing-home price for all housing types, up 0.2% from one year ago ($421,400) – the 25th consecutive month of year-over-year price increases.

It will be hard to make housing more affordable as long as The Fed keeps printing money.

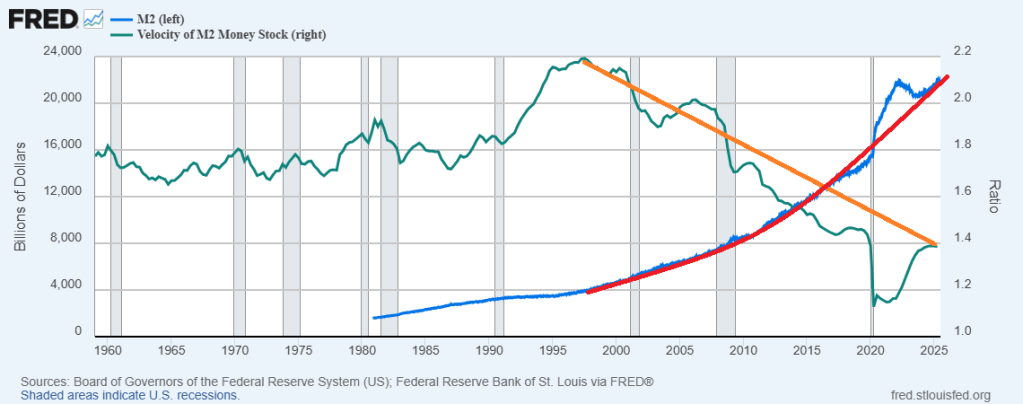

Powell et al cutting rates 25 basis points won’t really matter as long as they continue to print money. Unfortunately, M2 VELOCITY peaked under the Clinton Administration and has declined since despite frantic money printing.

What happended in 1995? Clinton’s National Homeownership Strategy that mandated HUD partners (GNMA, FHA, Fannie Mae, Freddie Mac, banks, etc.) to lower credit standards to encourage homeownership.

We need FHFA Director Bill Pulte to avoid doing what Democrats love (everything free or cheap).

You must be logged in to post a comment.