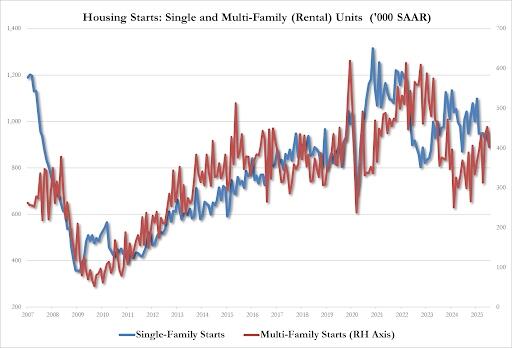

It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

Housing starts:

Single-family 890K SAAR, down 7.0% from 957K in July and the lowest since July 2024

Multi-family 403K SAAR, down 11% from 453K in July and the lowest since May.

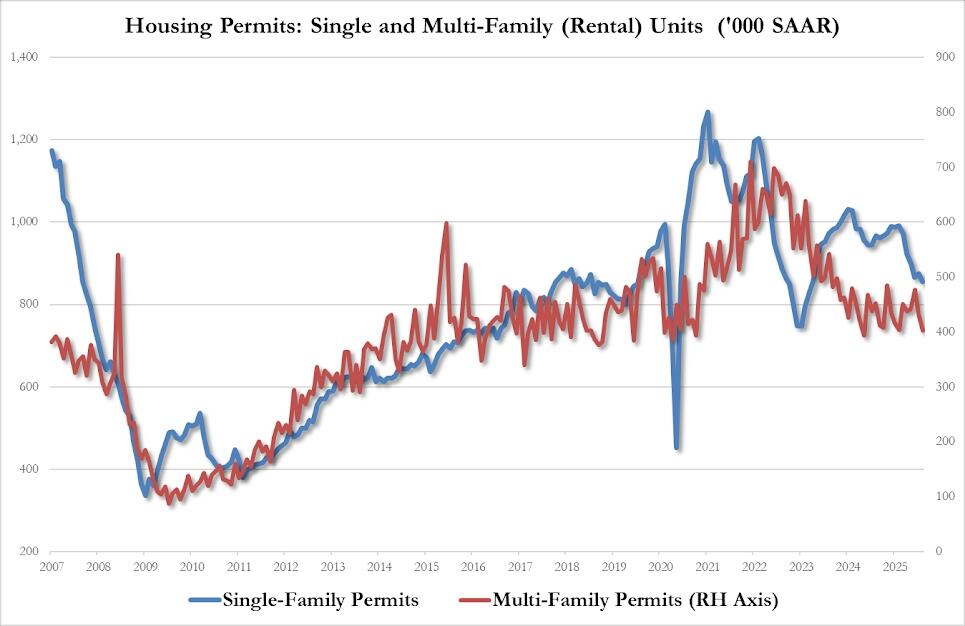

Housing permits?

Single-family 856K SAAR, down 2.2% from 875K in July and the lowest since March 2023

Multi-family 403K SAAR, down 6.7% from 432K in July and the lowest since May 2024

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

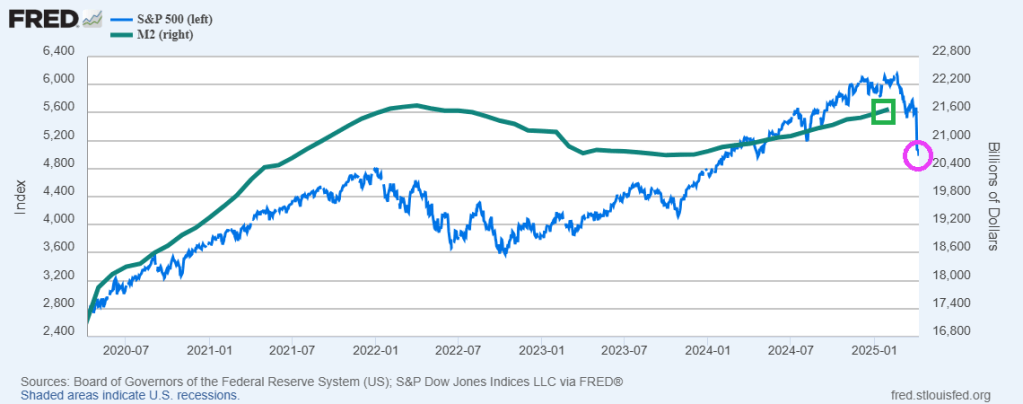

The Federal Reserve has created massive asset bubbles in financial markets. And the “tariff war” between the US and China. Since April 8, 2020, the S&P 500 index is up 81% while The Federal Reserve has printed a staggering amount of money as M2 Money is up 27.4% over the same period.

So, it is not surprising (except to Barstool Sports’ Dave Portnoy) that the stock market has declined with China’s childish petulance over Trump’s tariffs. While Trump levied a 104% tariff on Chinese goods, China counterattacked with a 84% tariff on US goods.

Freddie Mac Serious Delinquency Rate on Multifamily (Apartment) loans soared to highest rate since 2000. Since it is as of January 31, 2025, you can’t blame this on Donald Trump (although I am sure they will try).

Of course, home prices and rents soared under Biden. Home prices rose 37% under Biden and rents rose 25%. Simply unaffordable.

The US economy is gradually recovering from Bidenomics (government/donor dictated spending). Mortgage applications increased 11.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 7, 2025.

The Market Composite Index, a measure of mortgage loan application volume, increased 11.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 12 percent compared with the previous week. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index increased 8 percent compared with the previous week and was 4 percent higher than the same week one year ago.

The Refinance Index increased 16 percent from the previous week and was 90 percent higher than the same week one year ago.

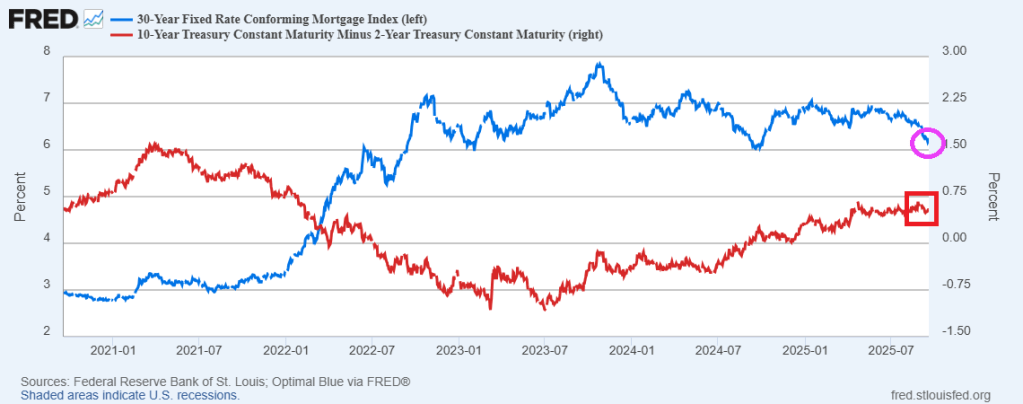

Mortgage rates declined for the sixth consecutive week, with the 30-year fixed rate dropping to 6.67 percent, the lowest level since October 2024. As a result, applications increased over the week and were up 31 percent from a year ago.

The US housing market is still suffering a hangover from Biden’s Presidency (high housing prices, high food prices, high inflation, high oil/gas prices, etc.) Housing prices are the highest in history, now we have FHA delinquencies at almost 15%.

The last gasp of the Biden/Harris reign of (economic) error!

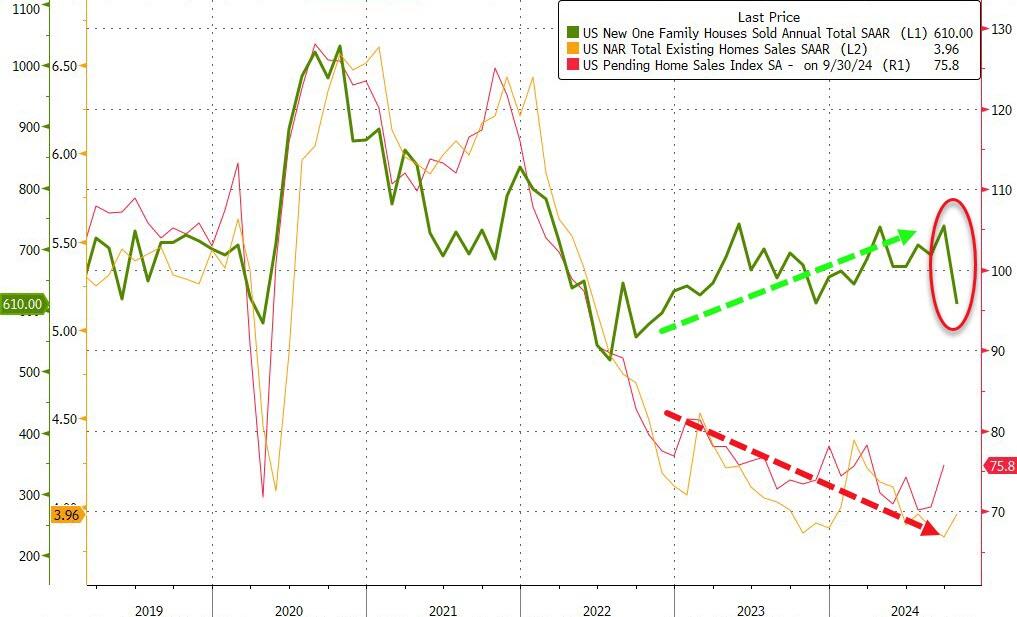

After existing home sales unexpectedly ticked up in October, analysts expected new home sales to slow after their recent resurgence (-1.8% MoM). They were right… BUT… the magnitude is mind-boggling!

New Home Sales collapsed 17.3% MoM in October. That is the largest MoM drop since July 2013.

Source: Bloomberg

That MoM plunge dragged sales down 9.4% YoY to 610k SAAR – the lowest since Nov 2022

Source: Bloomberg

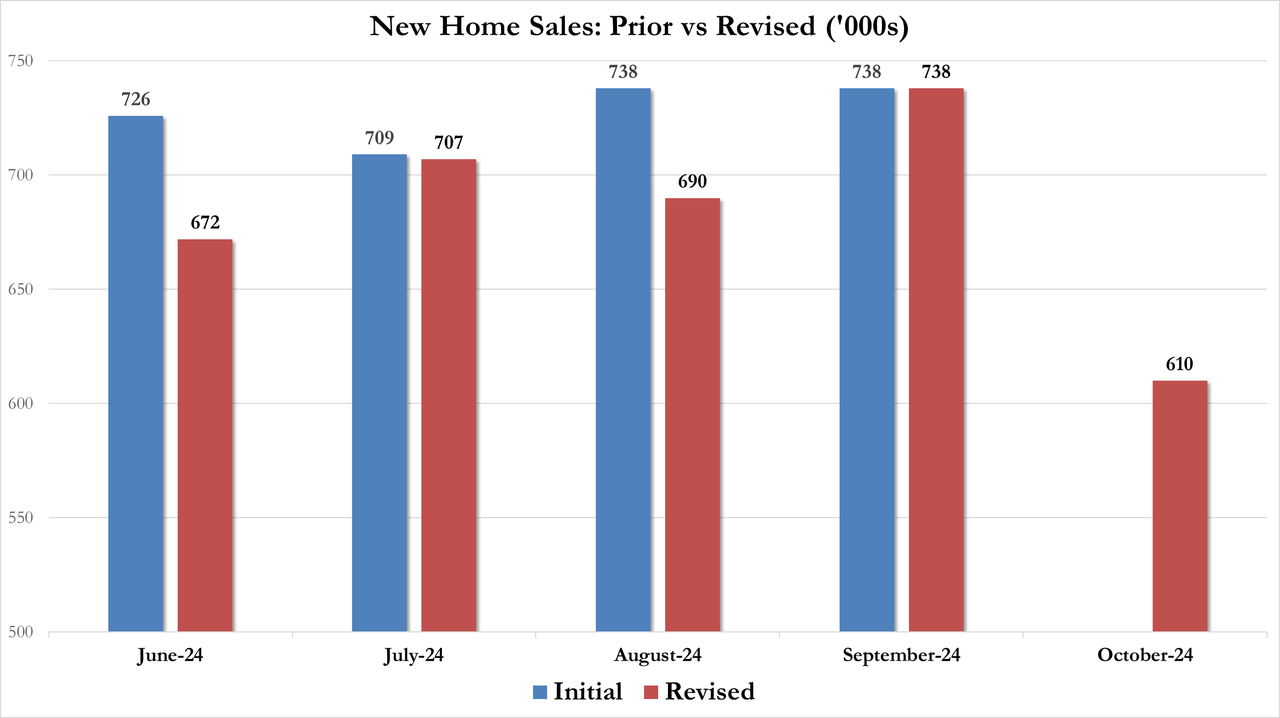

Of course, all the revisions are lower…

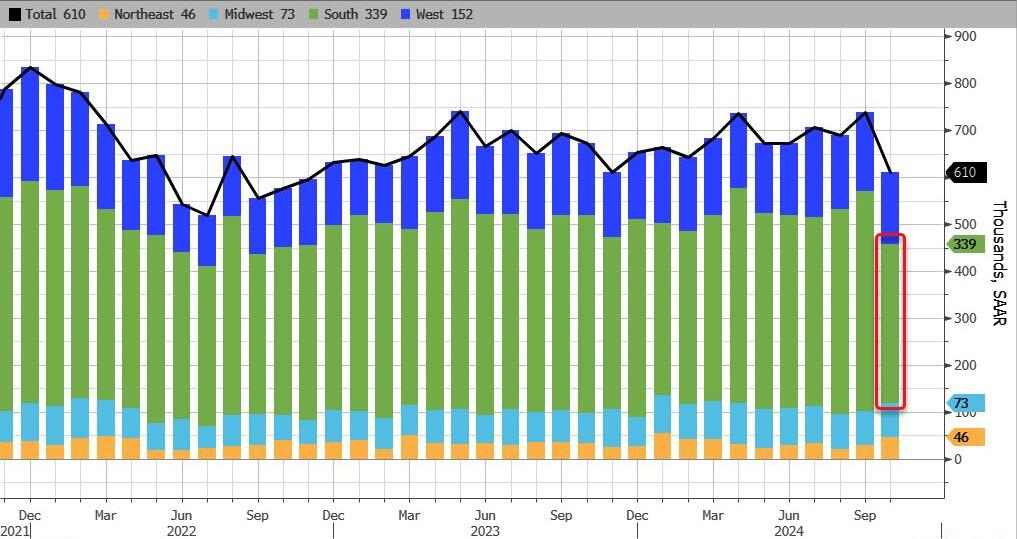

Hurricanes Helene and Milton, which tore through parts of the Southeast, delayed sales in the nation’s biggest housing region and dragged down sales overall.

Sales in the South decreased 28% to 339,000, the slowest pace since April 2020. Sales also fell in the West, but rose in the Northeast and the Midwest.

Source: Bloomberg

Finally, we note that the median sale price of a new home increased to $437,300 in October, the highest in 14 months.

Does this mean November’s data will see a massive surge in new home sales? …even as rates have increased significantly?

Fortunately, the Biden/Harris administration is winding down. On the mortgage side, the mortgage market is already gone under Biden/Harris where mortgage purchase applications are down a whopping 60%.

Mortgage applications increased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 15, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 1.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 1 percent lower than the same week one year ago. And down -60% under Biden/Harris.

The Refinance Index increased 2 percent from the previous week and was 43 percent higher than the same week one year ago.

Slowing economy, rising rates, too expensive housing. Not a good sign for the mortgage market.

The slowing US economy has a silver lining: Treasury and mortgage rates are declining. And the is spurring faster mortgage prepayments.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending August 2, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 0.3 percent compared with the previous week and was 11 percent lower than the same week one year ago.

The Refinance Index increased 16 percent from the previous week and was 59 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.55 percent from 6.82 percent, with points decreasing to 0.58 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The deciine in rates led to an increase in MBS convexity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.