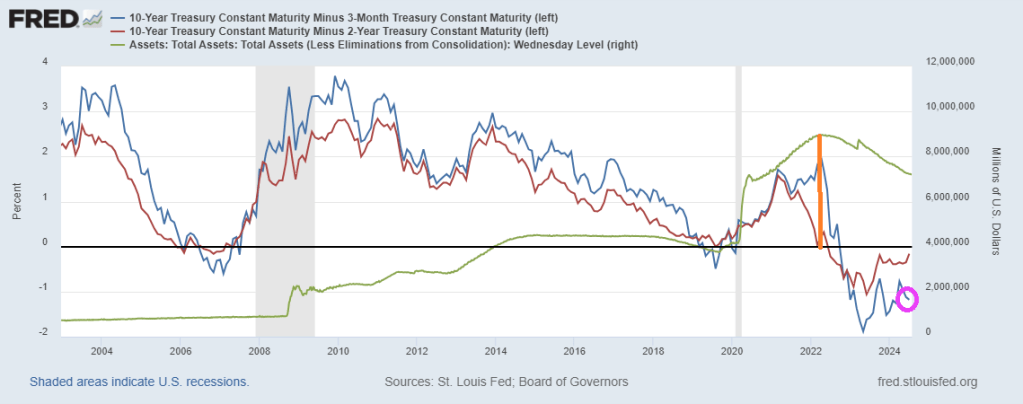

Up until 2022, the US Treasury yield curve behaved normally. In fact, as late as May 6th, 2022, the US Treasury 10Y-3M yield curve was at +227 basis points. Denote by the orange line in the following chart. That date corresponded with peak Fed balance sheet.

Then the massive spending by Biden/Harris/Congress hit the fan and inflation soared. The Fed counter attacked by raising rates and began scaling back their balance sheet. The 10Y-3M yield curve has been negative ever since.

Since the Covid outbreak in early 2020, The Fed went wild with rate cuts and massive and unpredented balance sheet expansion.

Let’s look at The Fed’s puchase of agency MBS and mortgage rates. From 2020 2022, The Fed continued to buy agency MBS. But in 2022, all hell broke loose as The Fed went crazy RAISING rates, but slowly began unwinding their balance sheet. The result? Mortgage rates began to climb. In fact, the US conforming mortgage rate for 30 years has risen 102% since early 2022. The Fed is only slowing unwinding their MBS holdings.

Despite the struggles in the residential housing market, the COMMERCIAL mortgage market is a trainwreck.

President Biden was expected yesterday to propose a cap of 5% on annual rent increases for tenants of major apartment landlords, and he did. Whether it can happen is something else.

As the White House communicatedon Tuesday, the administration is looking for Congress to pass legislation for landlords with more than 50 units in their portfolios, that being the proxy for institutional owners, although it would also affect private investors, family offices, and others that might own at least that many units. According to administration calculations, the total pool would cover 20 million rental units.

The law would then give landlords a choice. They could either restrict annual rent increases to no more than 5% a year or they would forfeit the ability to take fast depreciation of rental housing. There would be an exception for new construction or “substantial renovation or rehabilitation.”

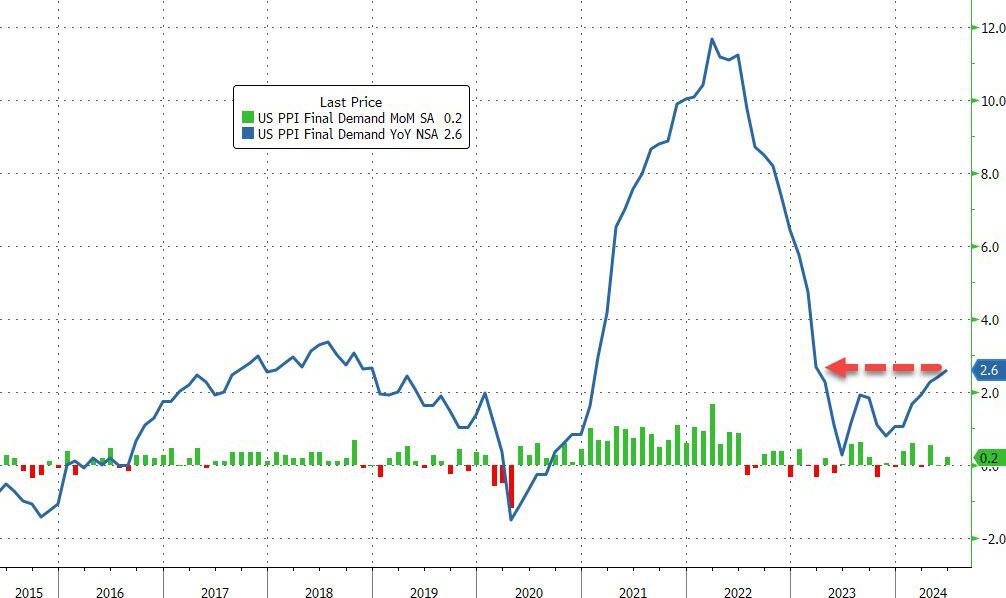

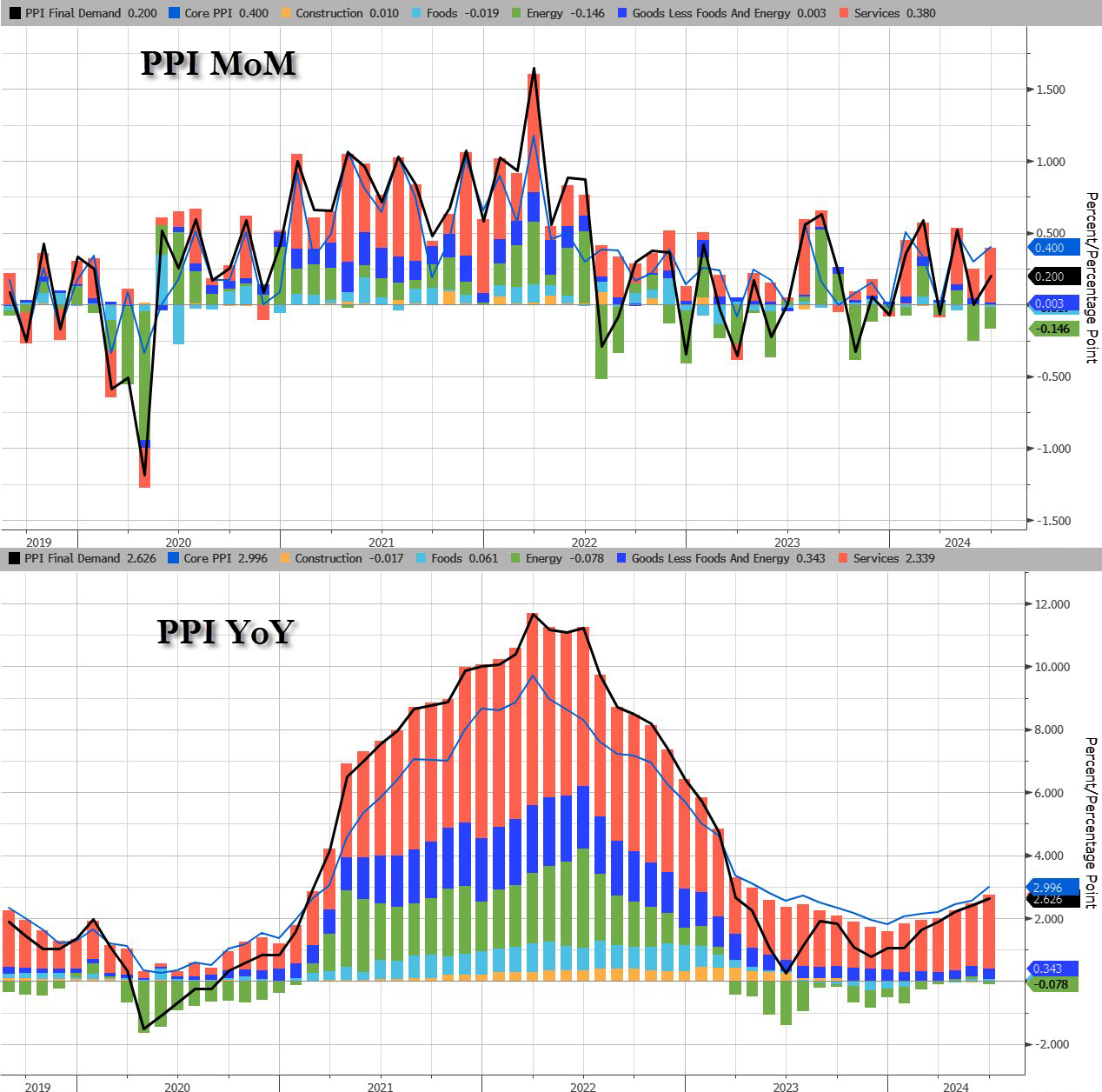

Core PPI rose by 0.4% MoM (double the 0.2% exp), sending the YoY price rise up by 3.0% (also the hottest since March 2023)…

Source: Bloomberg

The jump in PPI was driven by a resurgence in Services costs as Energy remains deflationary (for now)…

Source: Bloomberg

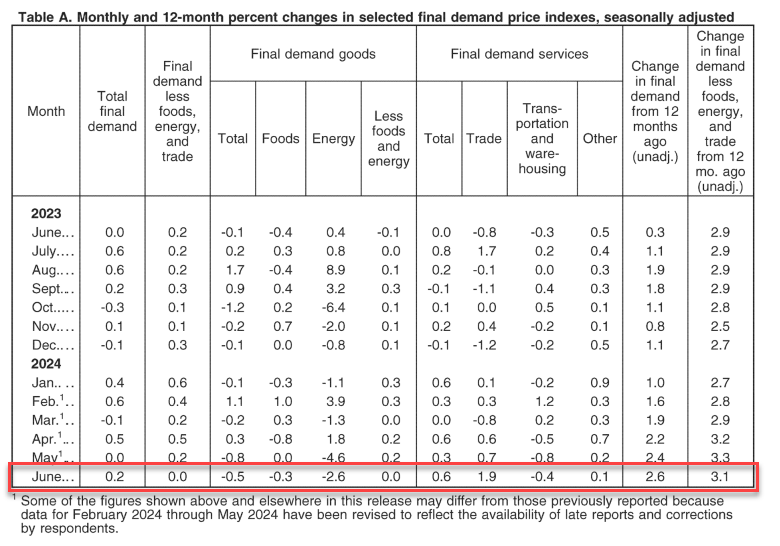

The June rise in the index for final demand can be traced to a 0.6-percent increase in prices for final demand services. In contrast, the index for final demand goods decreased 0.5 percent

Perhaps worse still, the pipeline for PPI (intermediate demand) is accelerating…

Source: Bloomberg

On the housing side, buying conditions for housing tanks to all-time low.

Are you ready? You can tell an election is on the radar since inflation numbers are settling down for the most part. According to the BLS, overall inflation fell slightly in June to 3.0%.

Shelter CPI is up 5.14% YoY as M2 Money growth has been rising slowly … again.

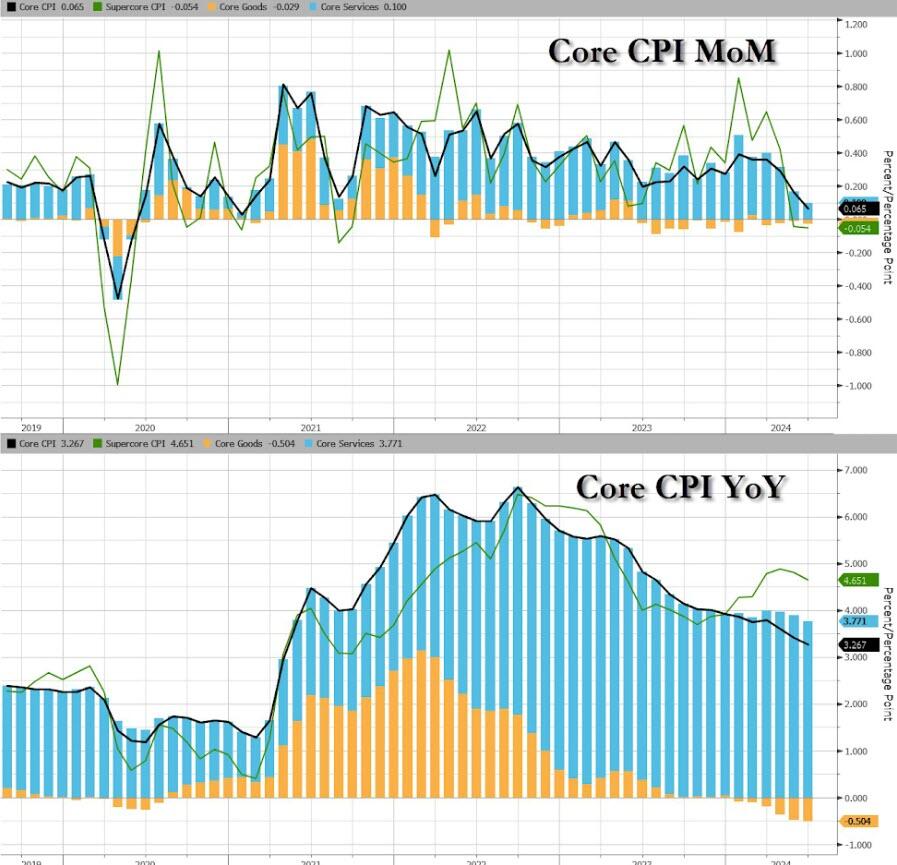

Core CPI also ‘missed’, rising just 0.1% MoM (vs +0.2% exp), dragging the YoY Core CPI down to +3.27% – its lowest since April 2021…

Source: Bloomberg

Goods deflation also dominates core prices disinflationary trend…

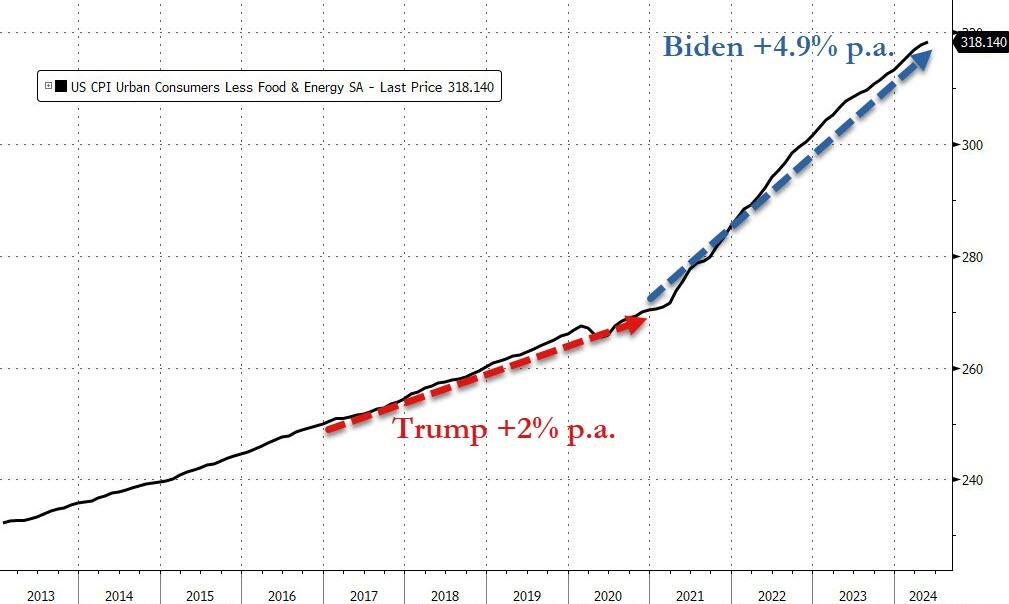

We do note that Core consumer prices have still not seen a single monthly decline since Bidenomics began.

Core consumer prices are up just under 18% since Bidenomics began (+4.9% per annum) – that is dramatically higher than the 2.0% per annum Americans experienced under Trump…

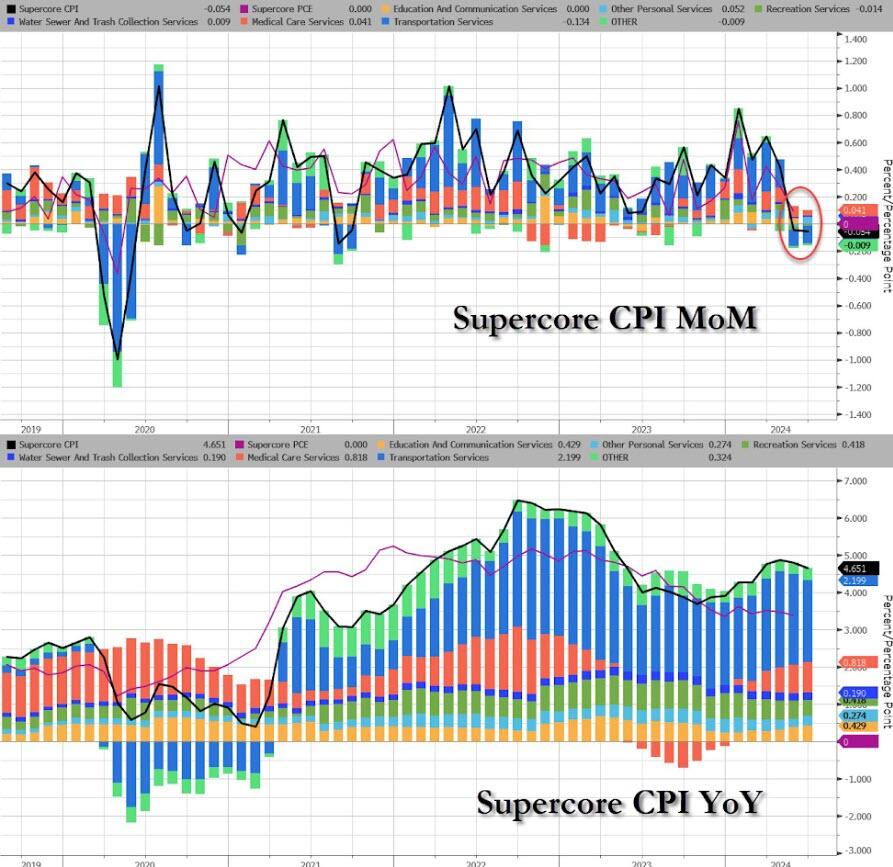

The much-watched SuperCore CPI rose on a MoM basis but declined (back below 5.0%) on a YoY basis (but obviously remains extremely elevated)…

Source: Bloomberg

Transportation Services are seeing prices fall…

Finally, we can’t help but get a sense of deja vu all over again here. What if… The Fed cuts (because bad – recession – data), Biden loses (because dementia), and inflation re-accelerates (just like in the 80s)…

Source: Bloomberg

Challenger job cuts in construction we the highest since 2008 putting downward pressure on wages.

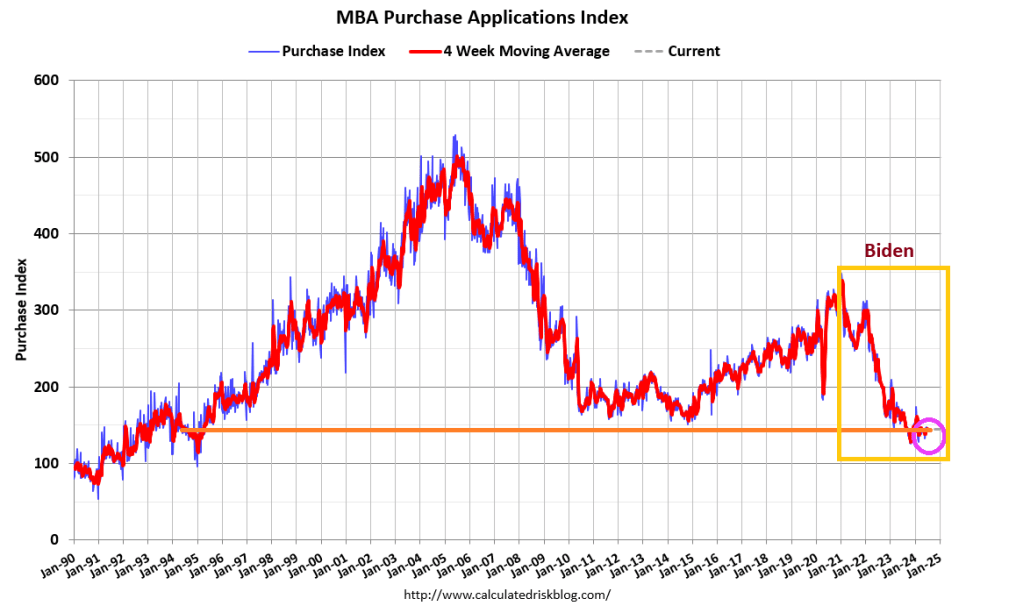

Mortgage applications decreased 0.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending July 5, 2024. Last week’s results included an adjustment for the July 4th holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 20 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index decreased 19 percent compared with the previous week and was 13 percent lower than the same week one year ago.

The Refinance Index decreased 2 percent from the previous week and was 28 percent higher than the same week one year ago.

Mprtgage prepays fell less than daycoiunt.

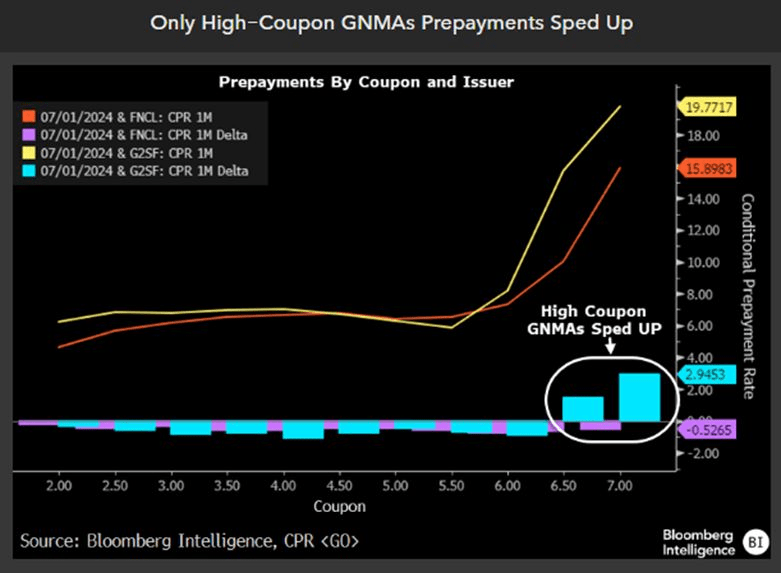

But on;y high-coupn GNMAs prepayments sped up.

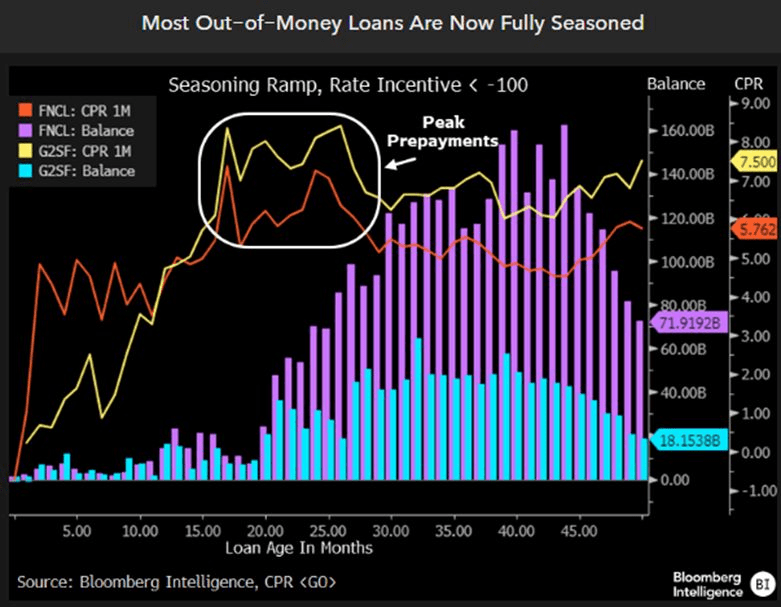

Finally, most out-of-the-money loans are now fully seasoned.

Yes. everyone can see the mental decline in President Biden and he should be in a nursing home. While he vows to run for President against Donald Trump, can you imagine what he will be like in 2 years? Let alone another 4 years??

This estimate is down from 4.2% seen in mid-May and from 2.2% seen on June 28th. If this estimate turns out to be correct it will be the 2nd consecutive quarter of GDP growth below 2.0% after Q1 2024 GDP of 1.4%.

Housing hasn’t slowed across the board … yet. But with mortgage payments as % of income near the highest since the early 1980’s, it will eventually slow down.

There is only one way out. CEASE Bidenomics and the crazy spending and debt and deficits!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.