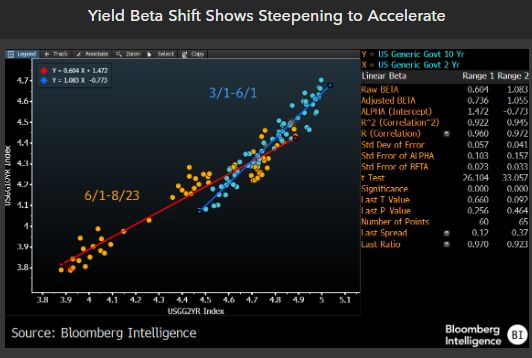

US 2y yields plunge to 3.95% as Fed’s Powell says ‘time has come’ to cut interest rates. Says Fed doesn’t seek, welcome further cooling in labor market.

Of course, there is a Presidential election in 60 days and The Fed doesn’t want the Orange Man to win. Instead, they want the Green Gal to win (Kamala Harris). Here is Green Gal (Harris) with Green Porker (Walz).

First, market participants are pricing in nearly 250 basis points (or 2.5%) in rate cuts by Jan 2026. Down to 3% from the cuurent rate of 5.50.

Why? The economy is a shambles due to bad economic policies by Harris/Biden and their Congressional stooges, especially Schumer in the Senate and Pelosi in the House. Hence, The Fed will feel pressure to lower rates. Although I don’t think that it will happen.

Of course, the Philly Fed disclosed that the Biden/Harris administration overstated jobs added by almost 1 million jobs in Q2. I would love to see Harris interviewed about that and watch her deflect and break into gales of laughter. How do American workers feel about Biden/Harris overstating jobs gains by almost 1 million jobs?? Isn’t that fraud?

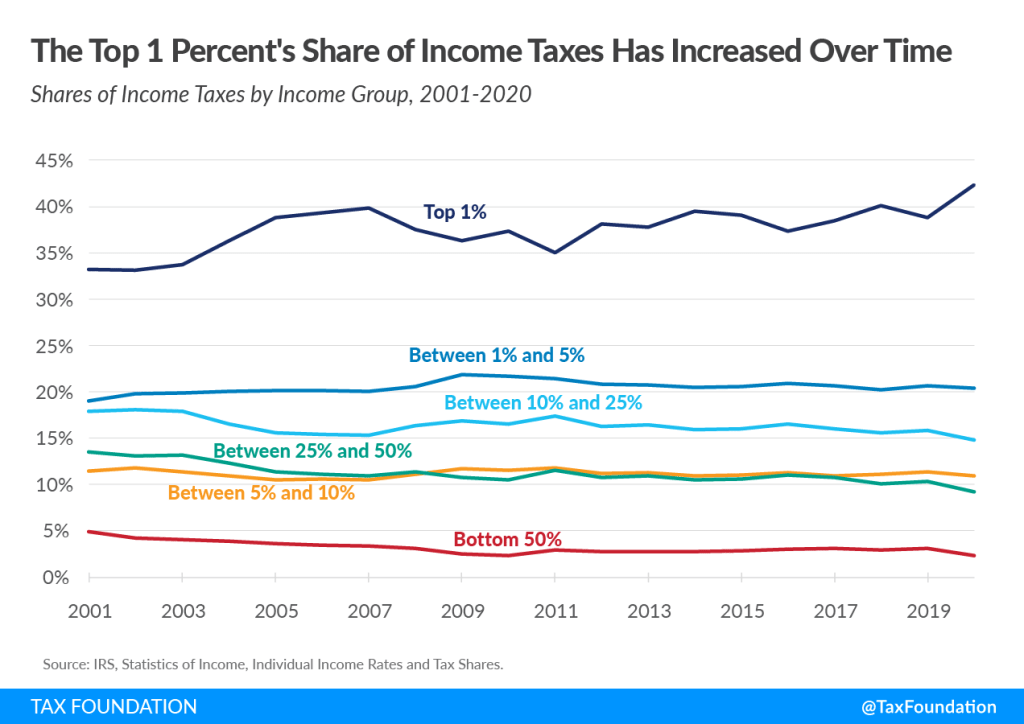

Harris and the DNC gave us an Orwellian picture of the future at the Democrat National Convention. Massive taxation ($5 TRILLION in crippling wealth transfers aka taxes). Of course, the top 1% will bear the brunt of the new taxes.

Small business owners pay business taxes on their individual tax return. The Harris endorsed budget raises the top marginal income tax rate to 39.6% from the current 37%.

Corporate tax rate higher than the EU and communist China.

Kamala Harris wants to hike the current 21% federal corporate income tax rate to 28%, higher than communist China’s 25% and the EU average of 21%, her campaign said Monday.

The Kamala Harris federal 28% rate is higher than the Asia average corporate tax rate of 19.8%, the EU average of 21%, the world average of 23.5%, and the OECD average of 23.7%. (See the Tax Foundation’s comprehensive listing here.)

The Harris federal 28% rate is also higher than Canada (26.2%), the UK (25%) Sweden (20.6%), and even Russia (20%), Afghanistan (20%), and Iraq (15%).

After adding state corporate income taxes, the combined federal-state tax burden in most states will easily exceed 30% under the Harris plan.

The Harris rate hurts the USA vs. China with its 25% rate. And note: Industry sectors of strategic use to the Chinese government pay an even lower rate of 15%.

American workers will bear the brunt of Harris’s corporate tax increase.

The non-partisan Joint Committee on Taxation affirmed in congressional testimony that corporate tax rate hikes hit “labor, laborers.” A study compiled by the Tax Foundation found that “labor bears between 50 percent and 100 percent of the burden of the corporate income tax, with 70 percent or higher the most likely outcome.”

Capital gains and dividends tax more than twice as high as communist China

Here is a direct quote from the Biden-Harris budget: “Together, the proposals would increase the top marginal rate on long-term capital gains and qualified dividends to 44.6 percent.“

Yes, you read that correctly: A Kamala Harris capital gains and dividends tax rate of 44.6%

China’s capital gains tax rate is 20%. Is it wise to have higher taxes than China?

Under the Harris plan, the combined federal-state capital gains tax exceeds 50% in many states. California will face a combined federal-state rate of 57.8%, New Jersey 55.3%, Oregon at 54.5%, Minnesota at 54.4%, and New York state at 53.4%.

Unconstitutionalwealth tax on unrealized gains

The Harris-endorsed budget calls for an annual 25 percent minimum tax on the unrealized gains of individuals with income and assets exceeding $100 million. Once in place, it won’t be long before the threshold is lowered to hit more and more Americans.

Americans overwhelmingly oppose taxes on unrealized gains, by a factor of three to one, including 76% of independents. Americans know that a “gain” isn’t “real” until it is actually realized, in hand.

This Harris tax is similar to the wealth taxes pushed by radical progressives such as Sens. Elizabeth Warren (D-Mass.) and Bernie Sanders (I-Vt.).

Capital gains taxes should only be paid when a gain is realized. Harris’s wealth tax would break with current tax policy and impose tax Americans based on the value of an asset on a particular arbitrary date.

This unprecedented tax would give even more power to the IRS, encourage taxpayers to move assets overseas, and will only expand to hit millions of Americans over time.

A second Death Tax by taking away stepped-up basis when parents die

Harris wants to impose a second Death Tax by taking away stepped-up basis when parents die. This would result in a mandatory capital gains tax at death — separate from, and in addition to — the current Death Tax.

This will impose a steep tax increase and paperwork nightmare for small businesses, farms, and families.

Under current tax law, assets that pass directly to your heirs get a step-up in basis for income tax purposes. It doesn’t matter if you pay estate tax when you die or not. For generations, assets held at death get a stepped-up basis—to market value—when you die. Small businesses count on this.

Wood notes the “proposalwould tax an asset’s unrealized appreciation at transfer. You mean Junior gets taxed whether or not he sells the business? Essentially, yes. The idea that you could build up your small business and escape death tax and income tax to pass it to your kids is on the chopping block.”

“When someone dies and the asset transfers to an heir, that transfer itself will be a taxable event, and the estate is required to pay taxes on the gains as if they sold the asset,” said Howard Gleckman, senior fellow in the Urban-Brookings Tax Policy Center.

Harris’s proposal to take away stepped-up basis has already been tried, and it failed: In 1976 congress eliminated stepped-up basis but it was so complicated and unworkable it was repealed before it took effect.

As noted in a July 3, 1979 New York Times article, it was “impossibly unworkable.”

NYT wrote:

“Almost immediately, however, the new law touched off a flood of complaints as unfair and impossibly unworkable. So many, in fact, that last year Congress retroactively delayed the law’s effective date until 1980 while it struggled again with the issue.“

As noted by the NYT, intense voter blowback ensued:

“Not only were there protests from people who expected the tax to fall on them — family businesses and farms, in particular — bankers and estate lawyers also complained that the rule was a nightmare of paperwork.“

Global tax cartel with 21% minimum tax rate

Harris wants to yoke the U.S. to an international tax cartel and impose a 21% global minimum tax on American businesses. This would be a devastating blow to U.S. competitiveness and sovereignty and eliminate healthy tax competition between countries.

The Biden-Harris administration has for years pursued a misguided international tax regime under the control of the Paris-based Organisation for Economic Co-Operation and Development (OECD). The OECD wants to stamp out tax competition.

Harris’s plan would go well beyond the OECD’s framework for a 15% global minimum tax and instead increase the rate to 21%. And the tax rate will only go up from there since bloated governments won’t have to compete.

Donald Trump had wisely kept the U.S. away from the tax cartel.

Quadrupled tax on stock buybacks — a Harris tax that will hit every American with a 401K or IRAor union pension

Democrats imposed a 1% stock buyback tax in the misnamed Inflation Reduction Act. Now, the Harris endorsed budget calls for quadrupling the tax, the burden of which hits every American with a 401k, IRA, or union pension.

A record share of 401(k) account holders took early withdrawals from their accounts last year for financial emergencies including preventing foreclosures, evictions and paying medical and tuition bills, according to the Wall Street Journal.

Raising taxes and restricting buybacks would further harm the 58 percent of Americans who own stock and more than 60 million workers invested in a 401(k). An additional 16.14 million Americans are invested in 529 education savings accounts.

Quadrupling the buyback tax, would stifle U.S. employers and put Americans at a competitive disadvantage vs. China, which does not have a buyback tax.

30% federal excise tax on electricity used in cryptocurrency mining

The Harris-backed budget imposes a 30% excise tax on the cost of electricity used to mine digital assets. The Treasury Department’s claims that mining has “negative environmental effects and can have environmental justice implications as well as increase energy prices.” Another excuse to raise taxes. It also neglects the fact that private sector innovation is already reducing any preexisting de minimis emissions by switching to “proof of stake” instead of “proof of work” consensus mechanisms.

Applies the wash sale rules to digital assets

The Harris-backed budget would apply the wash sale rule to digital assets. Under current IRS rules, a wash sale occurs when an investor sells “stock or securities” at a loss, and either 30 days before or after the sale, purchases a “substantially identical” stock or security. The IRS prohibits the deduction of losses when a wash sale occurs. The Joint Committee on Taxation (JCT) estimates that this change would increase the tax burden on digital asset transactions by roughly $17 billion.

$37 billion tax on American energy

The Harris-endorsed budget calls for a host of new taxes on oil and gas companies totaling $37 billion. This includes the repealing of expensing for intangible drilling costs (IDC), the use of percent depletion for oil and gas well and additional excise taxes on crude oil production. These tax hikes will be passed on to consumers in the former higher gas prices and energy bills. This tax hike on American energy comes on the heels of Democrats passing roughly $20 billion worth of new energy taxes included in the Inflation Reduction Act.

32% increase to Medicare taxes

Harris endorsed raising Medicare taxes from the current rate of 3.8 percent to 5 percent for individuals making over $400,000 per year, roughly a 32 percent tax hike. The plan reportedly broadens the Net Investment Income Tax (NIIT) to apply to non-passive business income and Harris would also increase the hospital insurance (HI) payroll tax from 0.9 percent to 2.1 percent for individuals earning over $400,000.

Carried interest tax on capital gains

Harris would tax carried interest as ordinary income for individuals earning over $400,000. While the Left labels carried interest as a “loophole” it is actually based on longstanding tax principles. Raising taxes on carried interest capital gains should be rejected. It is a terrible tax policy that would harm economic growth, reduce jobs, and reduce the returns of public pension funds across the country.

Even Sen. Kyrsten Sinema (I-Ariz.) rejected Democrats’ attempt to raise taxes on income from carried interest by blocking this proposal from being included in the Inflation and Reduction Act.

This tax hike would hit private equity, venture capital, real estate partnerships, and their portfolio companies which together account for over 25 million American jobs. In response, firms would downsize and decrease investment, causing both a loss of jobs and a reduction in the returns investors see.

$24 billionretirement tax

The Harris proposal calls for capping the retirement plan benefits of certain individuals. The White House projects this limitation on retirement benefits will raise $24 billion in taxes from individuals with retirement account balances above $10 million and earnings above $400,000.

Real estate tax hike on Like-Kind exchanges

Harris backs raising taxes on capital gains from real estate transaction by limiting what are knows as 1031 Like-Kind Exchanges to $500,000 in gains.

Under current tax rules, real estate investors can exchange real property used for business for similar real property and defer capital gains tax. Harris’s proposed changes to this tax treatment will hurt individuals and farmers.

An even further-supersized IRS

If you thought Harris and congressional Democrats had already supersized the IRS enough, think again. The Harris budget plan shovels another $104.3 billion to the agency.

Erodes taxpayer rights by making it easier for IRS agents to stack up questionable penalties against taxpayers

Last year the Biden-Harris IRS got caught illegally backdating penalty documents and signatures in U.S. Tax Court in order to run up the bills on taxpayers. The court caught the IRS lying. U.S. Tax Court is generally very deferential to IRS neglect but in this case the court was rightly furious.

While testifying to congress in late 2023, IRS Commissioner Werfel declined to say whether anyone has been fired for this practice. It is suspected the backdating incident was not an isolated occurrence within the IRS. Another indication that the IRS has a severe accountability problem that is only going to get worse.

Due to reforms enacted by Republicans in 1998, IRS agents are currently required to get written approval from their immediate supervisor before imposing penalties on taxpayers. This is designed to protect taxpayers from agent chicanery.

Congressional investigators discovered years of abuse by IRS agents running up the penalty score as an intimidation tactic against taxpayers. Agents would use the threat of penalties as a bargaining chip. The IRS has a history of targeting people who do not have the means to fight back, and unethical agents at employee review time could point to all the penalties they imposed on people who perhaps did not deserve it. So, in 1998 congressional Republicans enacted a taxpayer protection (Section 6751) which requires agents to get personal written approval from their immediate supervisor before sending written penalty letters to taxpayers.

But the Biden-Harris budget allows IRS agents to shop around for sympathetic supervisors anywhere in the building. Harris also wants to scrap the written approval requirement altogether for many penalty scenarios. Agents will abuse this and taxpayers will be the victim.

From the Biden-Harris budget: “In addition, the proposal would expand approval authority from an ‘immediate supervisor’ to any supervisory official, including those that are at higher levels in the management chain or others responsible for review of a potential penalty.”

Won’t be long before agents just go directly to the taxpayer-hostile supervisor on, say, the fourth floor who will sign off on anything. Good luck to taxpayers without the resources to defend themselves in court against an agency with a near-unlimited budget.

Of course, what will the new taxes be spent on? That is REALLY scary. Healthcare for illegal immigrants? Wealth transfer to large donors??

Well, it is already getting nasty on the employment front with jobs transitioning to unemployment at a rapid rate.

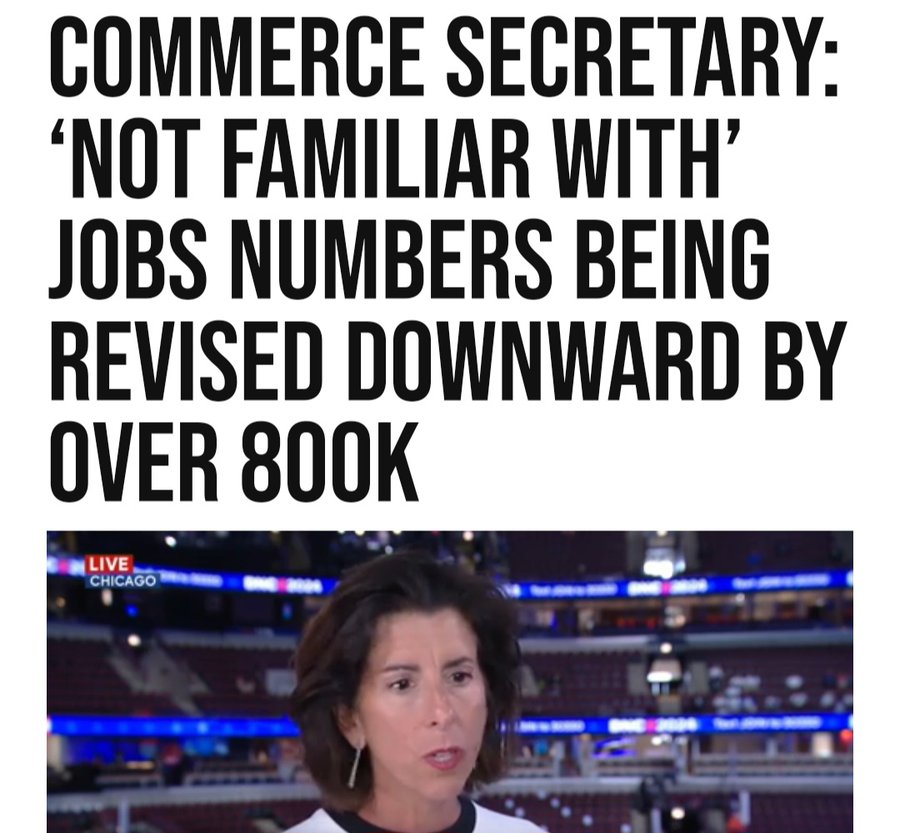

The scary thing about the BLS overstating job gains by Biden/Harris by almost 1 million jobs is that US Commerce Secretary Gina “The Goofball” Raimondo didn’t even know about the Philly Fed report.

Back in March, when most of Wall Street and economists still believed the lies spewed forth by the Biden Bureau of Labor Statistics, which intentionally uses inaccurate, rushed “data” from the Establishment survey which is meant to pad sentiment and make the economy appear far stronger than it is for propaganda purposes (as one can see by the constant monthly downward revisions), we did an in-depth analysis looking at the actual, “uncooked” numbers published by the Philadelphia Fed preview of the annual Quarterly Census of Employment and Wages employment revision, and warned our readers that actual US payrolls are overstated by at least 800,000.

Specifically, we concluded that “the BLS had overstated payrolls by 800,000 through Dec 2023 (and more if one were to extend the data series into 2024)” and added that “it’s truly statistically remarkable how every time the data error is in favor of a stronger, if fake, economy.”

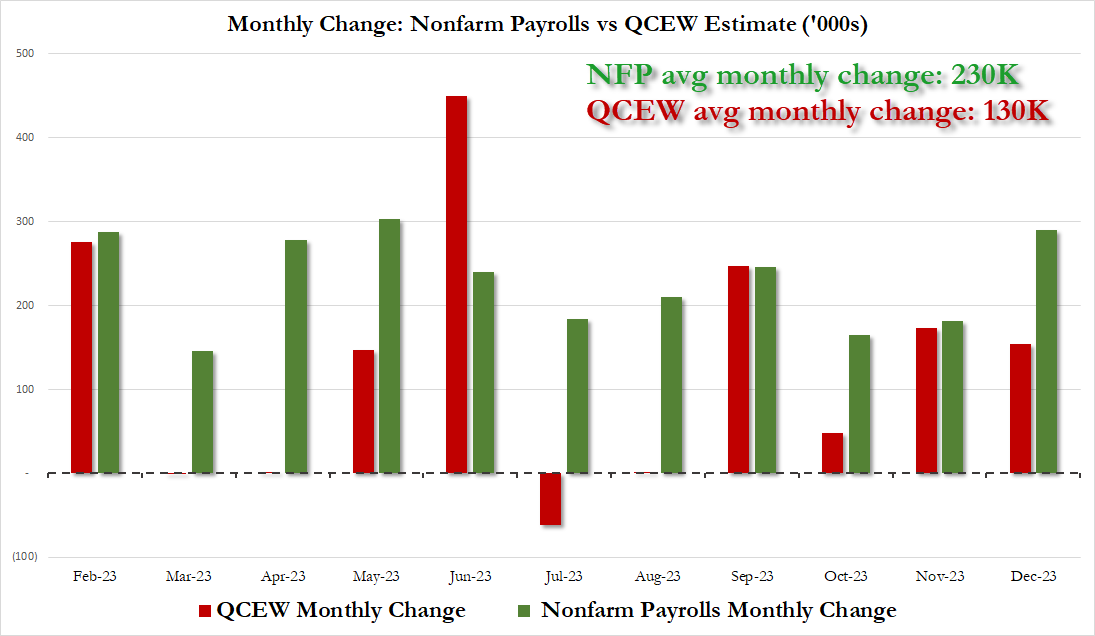

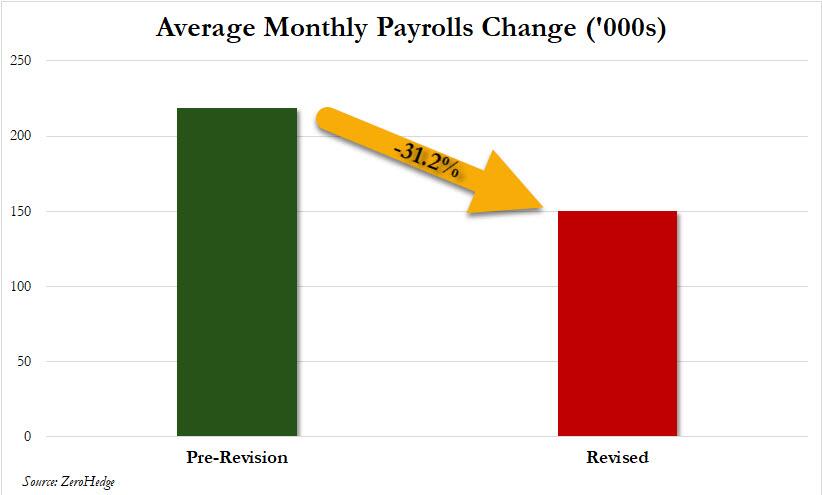

Furthermore, we also noted that the revision “also means that far from the stellar 230K average monthly increase in payrolls in 2023, which the White House would spin time and again as direct evidence of the benefits of Bidenomics, the true average monthly payroll increase in 2023 was only 130K! The full monthly change in payrolls as originally reported by the BLS (in green) and the actual monthly number, as per the QCEW (in red) is shown below.”

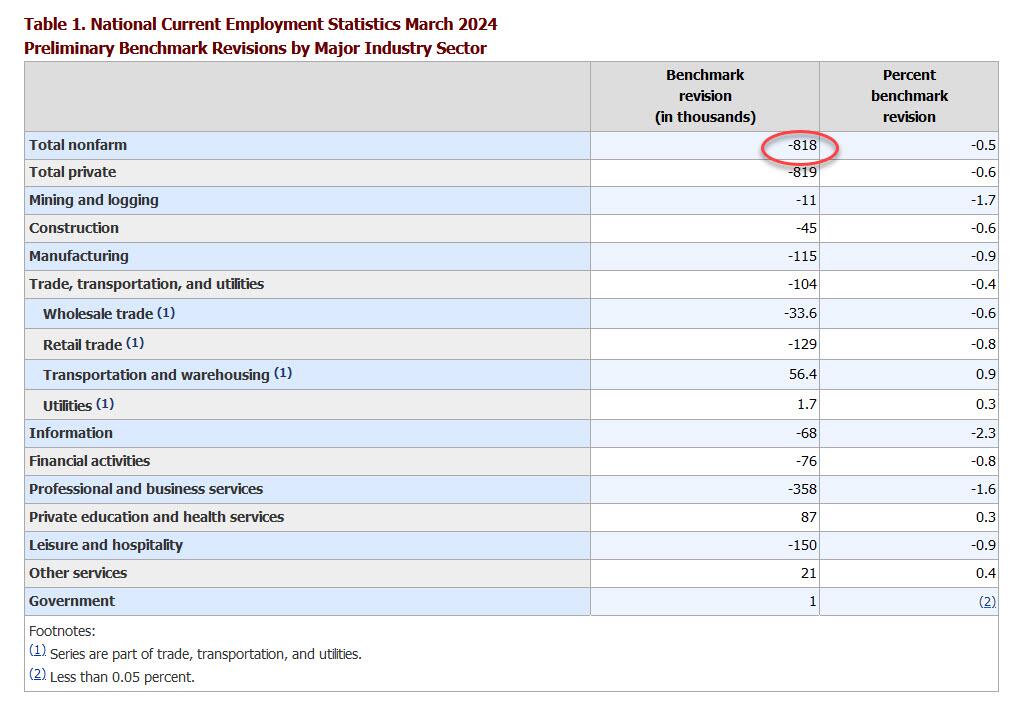

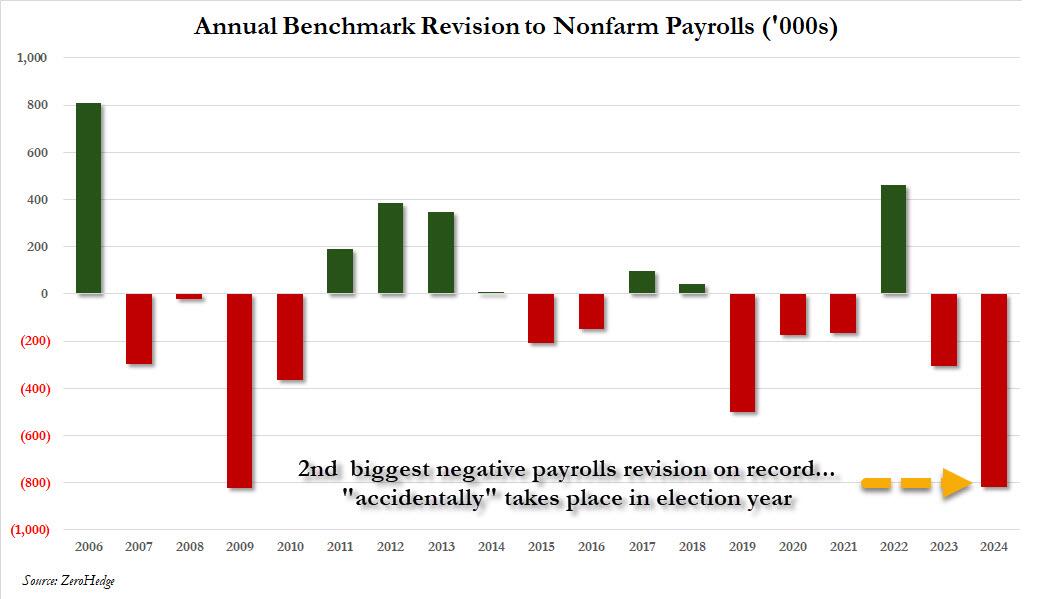

This matters because as we reminded our followers this weekend, today at 10am, the BLS would publish its annual nonfarm payrolls benchmark revision where it would unveil as , which it did (with the usual 35 minute delay because that’s the kind of service $35 trillion in debt buys you), and it confirmed that we were right almost to the dot, because as the BLS unveiled in its CES Preliminary Benchmark Announcement, “the preliminary estimate of the benchmark revision indicates an adjustment to March 2024 total nonfarm employment of -818,000 (-0.5 percent)” or just above the 800,000 was said to expect back in March.

The revision is mainly due to the highest-paying sectors: i.e., professional services -358k, leisure -150k, and manufacturing -115k. Not at all surprising: government was revised +1,000.

As an aside, while the data were scheduled to be released at 10 a.m. in Washington but didn’t appear on the BLS’s website for more than a half hour later. A spokesperson for the agency didn’t answer Bloomberg’s questions as to why the figures were delayed, but we have some pretty good guesses about the panic that gripped the BLS as they realized they needed a green lights from the propaganda ministry before going live with this number.

How big is the 818,000 revision in context? As the chart below shows, the 2024 revision was the biggest in the past decade, and the second biggest on record, with just the 824K downward revision in 2009 just (barely) greater.

The revisions confirm that – as we had been warning for much of the past year – the labor market started moderating much sooner than flawed conventional wisdom thought. It wasn’t until earlier this month that markets and economists grew concerned with the release of the July jobs report. That set off alarm bells with a weak pace of hiring and a fourth month of rising unemployment, but other metrics like jobless claims and vacancies have suggested a more moderate slowdown.

Putting it all together, we now know – as we reported first back in March – that the labor market is, and was, far weaker than conventionally believed. In fact, no less than 800,000 payrolls would end up “missing” when one uses the far more accurate Quarterly Census of Employment and Wages data rather than the BLS’ woefully inaccurate and politically mandated payrolls “data”, and if one looks back the the monthly gains across most of 2023, one gets not 218K jobs added on average every month but rather 150K, a 31% decline. Needless to say, the market would look very different if it had known that effectively all the payroll “beats” of the past year would be deleted!

Of course, none of that paints Bidenomics, or Kamalanomics, or whatever it is now, in a flattering picture, because while one can at least pretend that issuing $1 trillion in debt every 100 days to add 3 million jos per year is somewhat acceptable, learning that that ridiculous amount buys 800,000 jobs less is hardly the endorsement that the White House needs. On the flip side, pretending that the US had added an additional 800,000 jobs in the past year is precisely what Biden, and now, Kamala would have wanted to generate the kind of buzz and momentum that somehow translates into the “greatest economy ever”… at least until it is all revised away as the admin’s lies finally wash away.

What is the implication for the market? Well, as UBS trader Leo He correctly notes, “the Fed is well aware of nonfarm payrolls (establishment survey) overstating the job market, but unemployment rate (household survey) underestimating the job market” and he goes on to quote Governor Bowman’s speech on Tuesday:

“There are also risks that the labor market has not been as strong as the payroll data have been indicating, and it appears that the recent rise in unemployment may be exaggerating the degree of cooling in labor markets. The Q4 Quarterly Census of Employment and Wages (QCEW) report suggests that job gains have been consistently overstated in the establishment survey since March of last year, while the household survey unemployment data have become less accurate as response rates have appreciably declined since the pandemic. The rise in the unemployment rate this year largely reflects weaker hiring, as job searchers entering the labor force are taking longer to find work, and layoffs remain low. It is also likely that some temporary factors contributed to the soft July employment report. The rise in the unemployment rate in July was largely accounted for by workers who are experiencing a temporary layoff and are more likely to be rehired in coming months. Hurricane Beryl also likely contributed to weaker job gains, as the number of workers not working due to bad weather increased significantly last month.”

At the end of the day, all this does is cement the Fed’s 25bps rate cut next month.

As for broader socio-political implications, the reactions are already pouring in with those on the blue side of the spectrum pretending nothing happened, while those on the other side of the aisle raging at what has now become clear propaganda by the highly politicized Department of Labor. To wit, here is RFK, Jr., proposed VP candidate Nicole Shanahan slamming the BLS, and using our data to do so:

The Bureau of Labor Statistics (BLS) has long been used as a tool of propaganda by the executive branch. Here’s how: they distort definitions, manipulate data, exclude discouraged workers, and revise past reports to create narratives that fit the agenda of whichever administration is in power. This skews the actual economic picture and misleads citizens about the true state of our economy. It’s like a game of musical chairs, and neither side wants to be caught standing when the music stops. The Constitution doesn’t grant the government the authority to track unemployment statistics, so why do we even have this agency? Perhaps it’s time to get rid of it. Their $750M budget could surely be put to better use, and private companies already track U.S. unemployment for free. Win-win.

We agree: back in March we concluded our article, which predicted today’s revision with near 100% accuracy, by warning that the staggering size of the revised data “is also why nobody in the mainstream media – which is now nothing more than the PR smokescreen for the Biden puppetmasters, the government and the deep state – will ever mention this report.”

Today it will be more difficult for the propaganda press to ignore it.

At least she should speak in front of a Communist Chinese flag! Her true master.

The wheels are coming off Bidenomics. Code for corporate welfare and massive government spending. Coupled with misguided and burdensome regulations, we got gut wrenching inflation.

The result? A disastrous stock market showing yesterday.

What has Biden/Harris’ economic agenda wrought? Record high personal debt and record low savings rates.

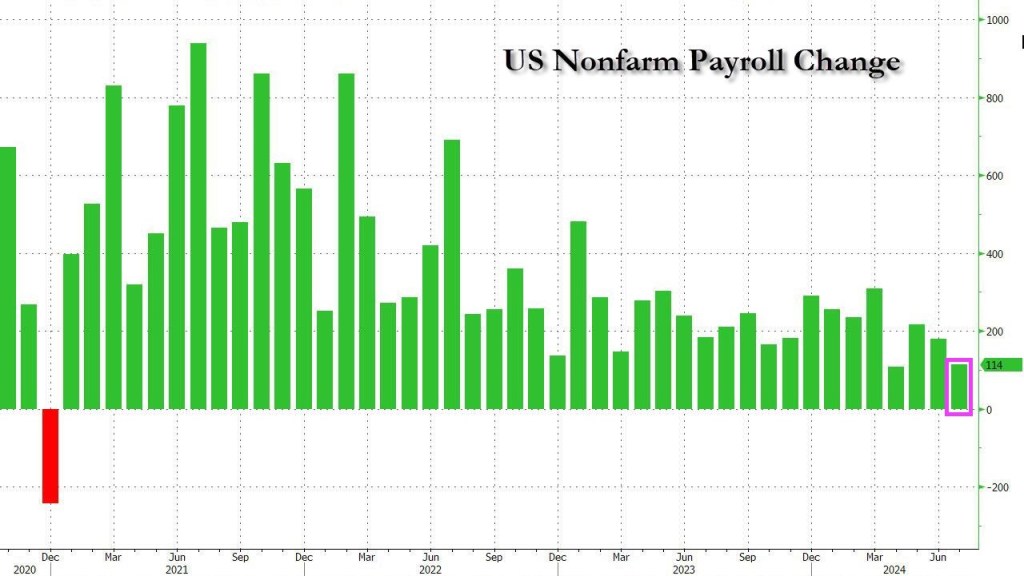

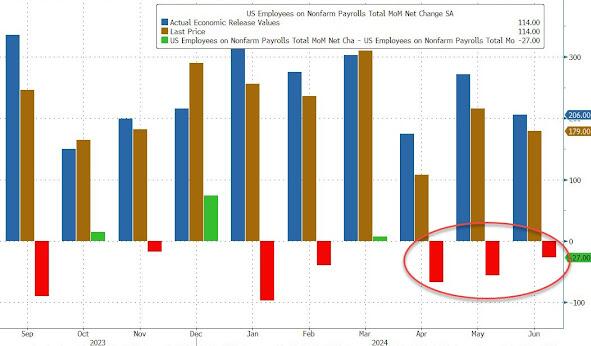

Qhat a terrible jobs report! The number of unemployed rose by 352k and only 114k jobs added.

It was a 3 sigma miss to the median estimate of 175K.

May revised down by 2,000, from +218,000 to +216,000, and the change for June was revised down by 27,000, from +206,000 to +179,000. With these revisions, employment in May and June combined is 29,000 lower than previously reported. It gets better because as shown in the next chart shows, 5 of the past 6 months have now been revised lower.

And the US yield curve is screaming recession ahead!

Over the last year, native-born Americans have LOST 1.2 million jobs while foreign-born employment has increased 1.3 million; we’re just swapping out American workers at this point.

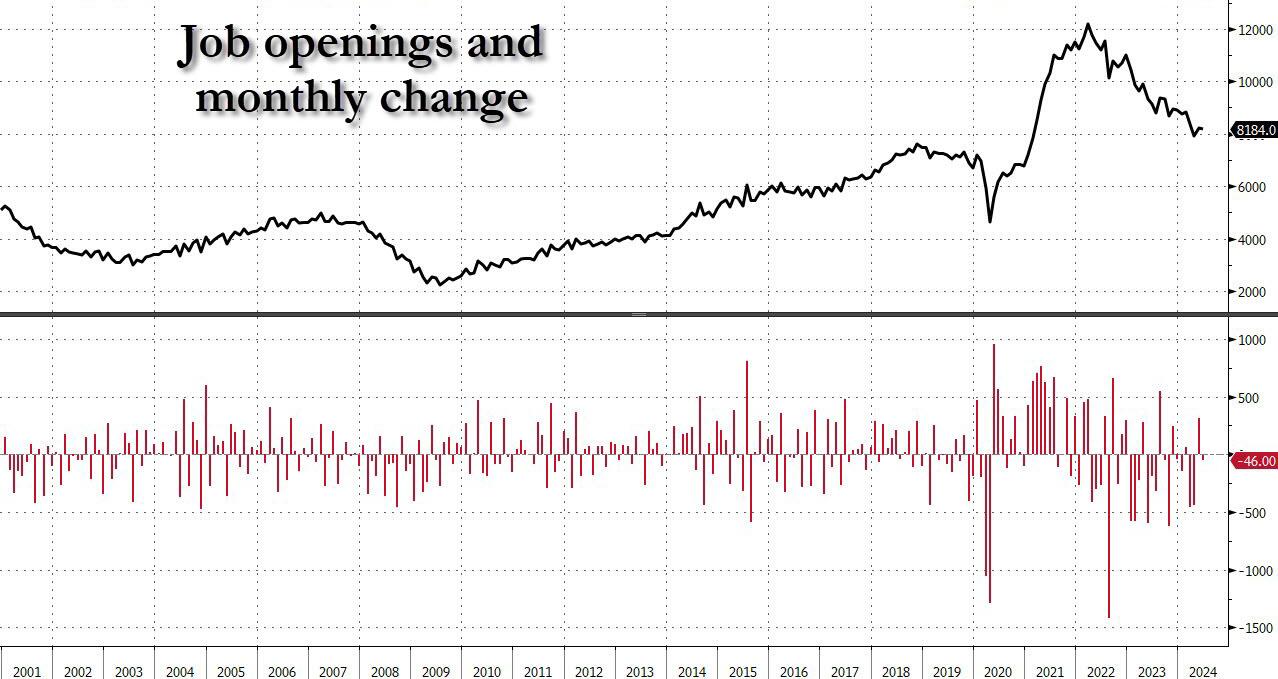

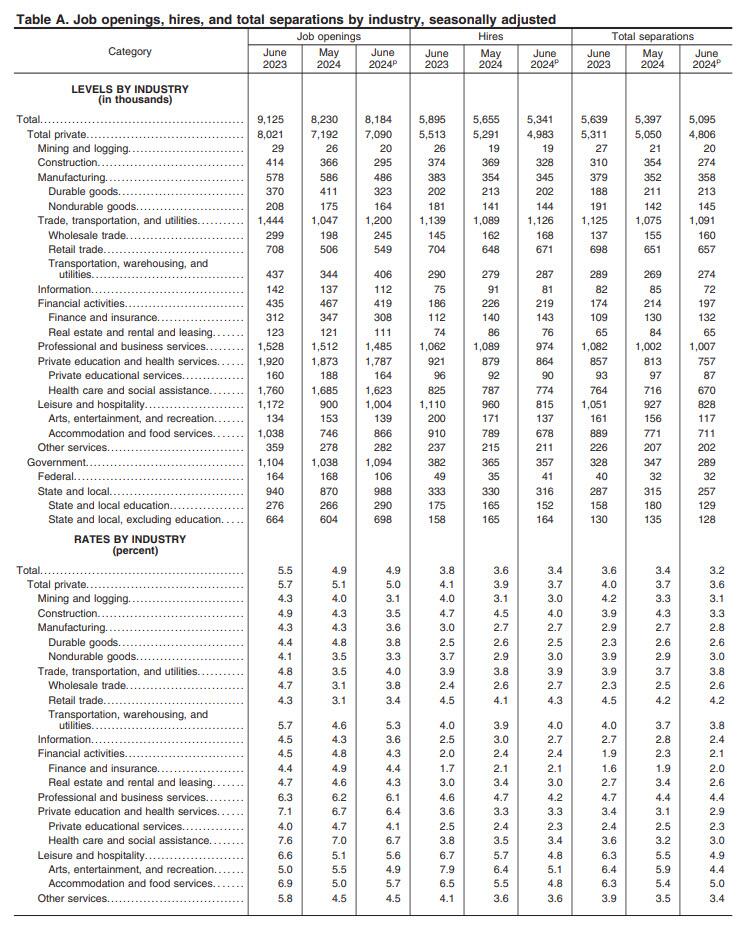

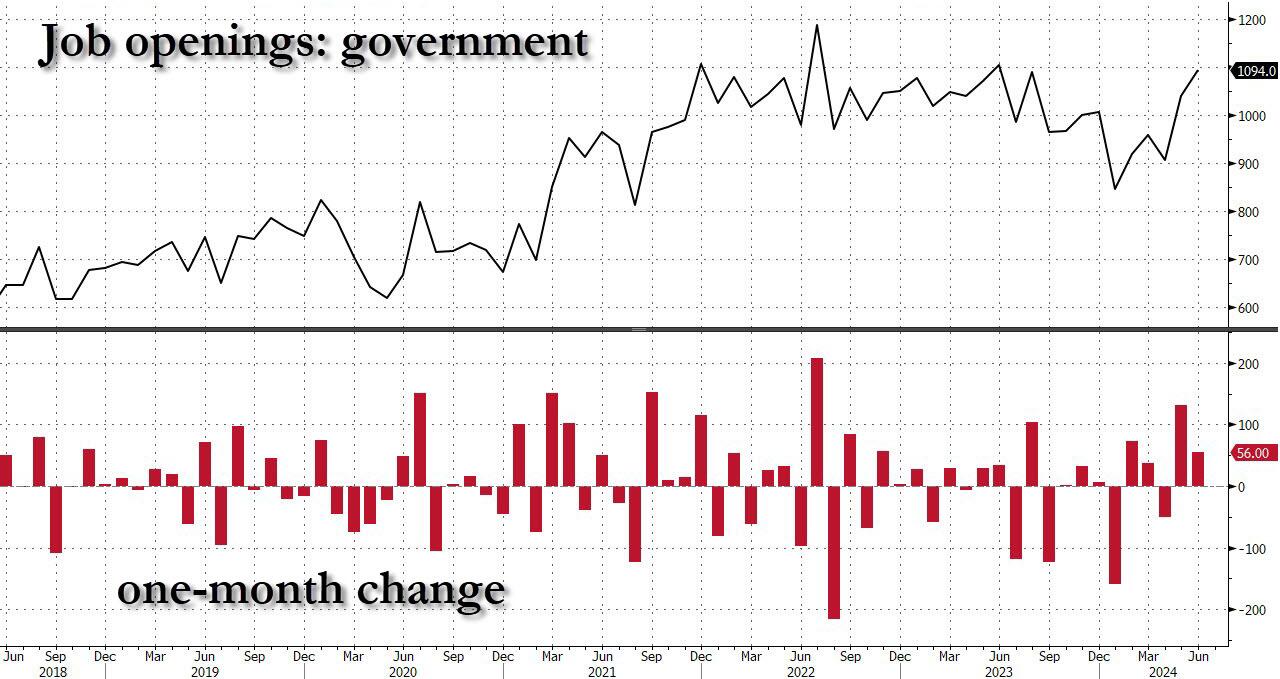

And yet, the same data rigging observed last month took place once again, because a quick look at the breakdown shows that while private jobs saw another broad drop in openings across private sectors…

… this was almost fully offset by the relentless surge in government job openings.

Yes, while May was indeed revised lower, June saw another bizarre jump in government job openings, surging to a near record 1.094 million, driven by a 118K spike in State and Local job openings.

Putting it all together, while private sector job openings plunged to a level seen back in late 2018, government job openings are just shy of a record high!

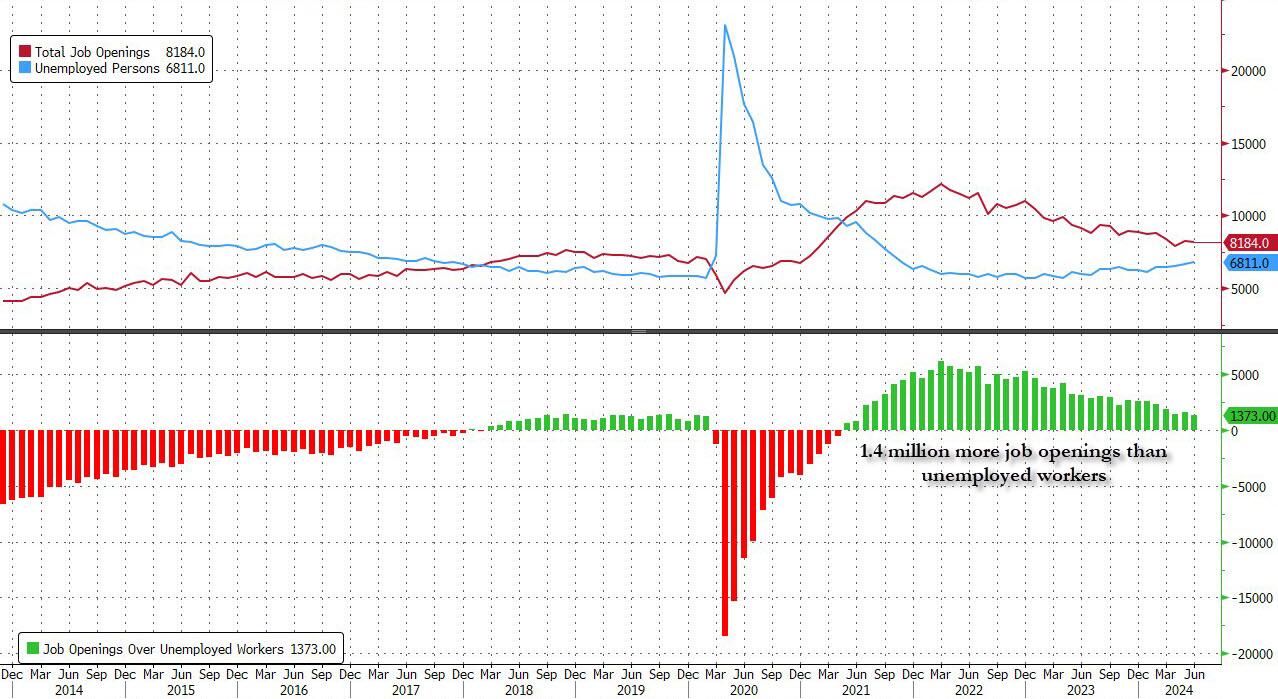

Ignoring the data manipulation, in the context of the broader jobs report, in June the number of job openings was 1.373 million more than the number of unemployed workers (which the BLS reported was 6.811 million), down from last month’s 1.581 million and the lowest since the summer of 2021.

Said otherwise, in April the number of job openings to unemployed dropped to just 1.24, a sharp slide from the March print of 1.30, the lowest level since June 2021 and now officially back to pre-covid levels.

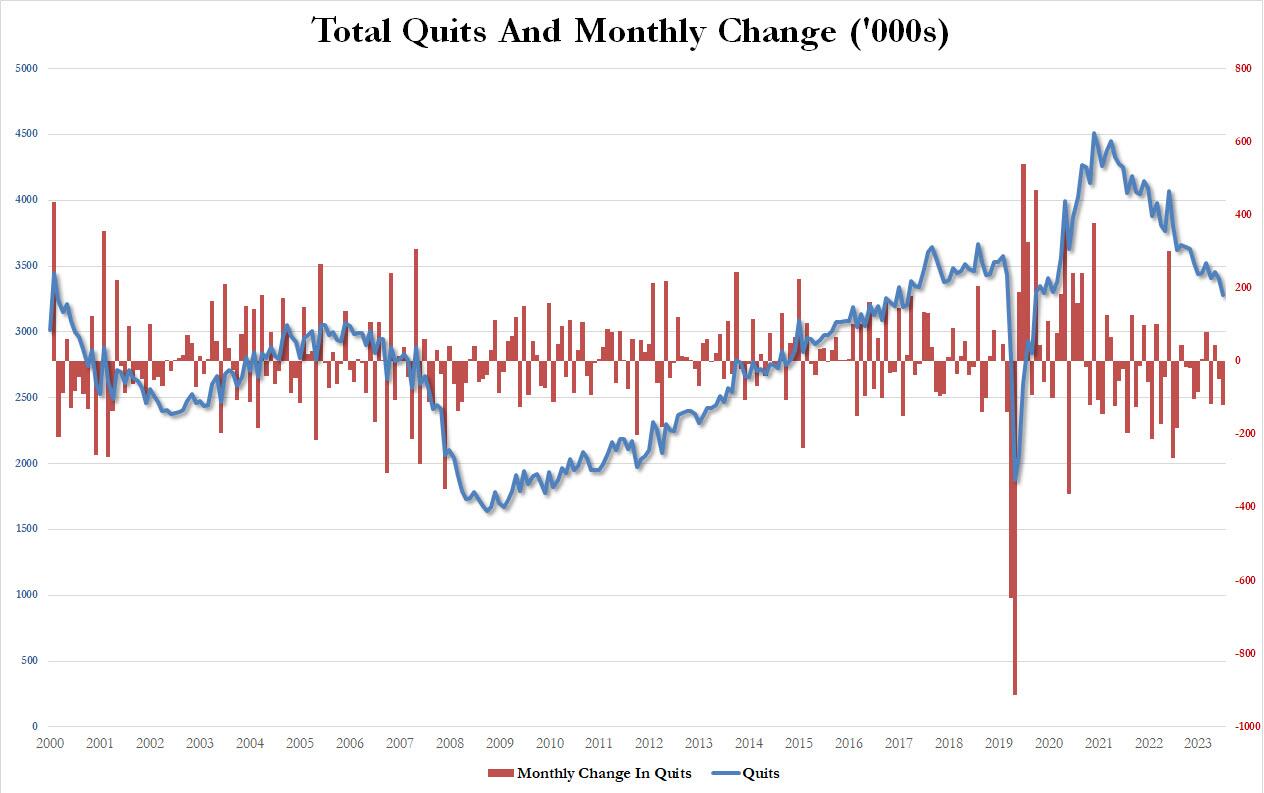

But wait there’s more: confirming that if one ignores the clearly manipulated jump in government job openings (“quick, let’s hire a ton more TSA agents and deep state apparatchiks to make it seems that Kamalanomics is working”), a quick look at the number of quits – an indicator closely associated with labor market strength as it shows workers are confident they can find a better wage elsewhere – showed a plunge in June, dropping by 121K, the most since July 2023, to just 3.282 million, the lowest since August 2020!

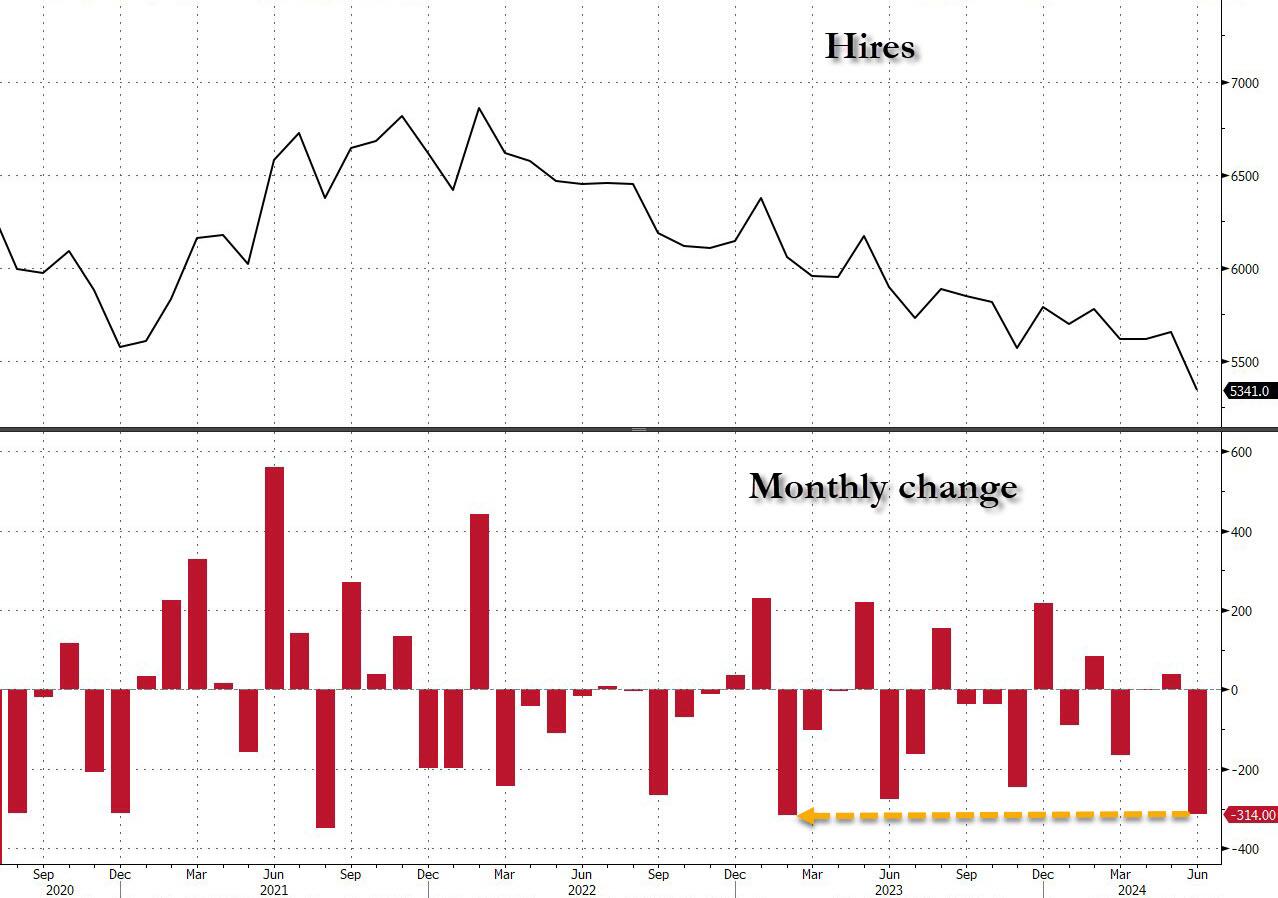

Finally, the piece de resistance was the number of actual hires, which in June also tumbled to just 5341, down a massive 314K in one month, the biggest monthly drop since February 2023…

… dragging the total to just 5.3 million, the lowest level since the depts of the covid lockdowns.

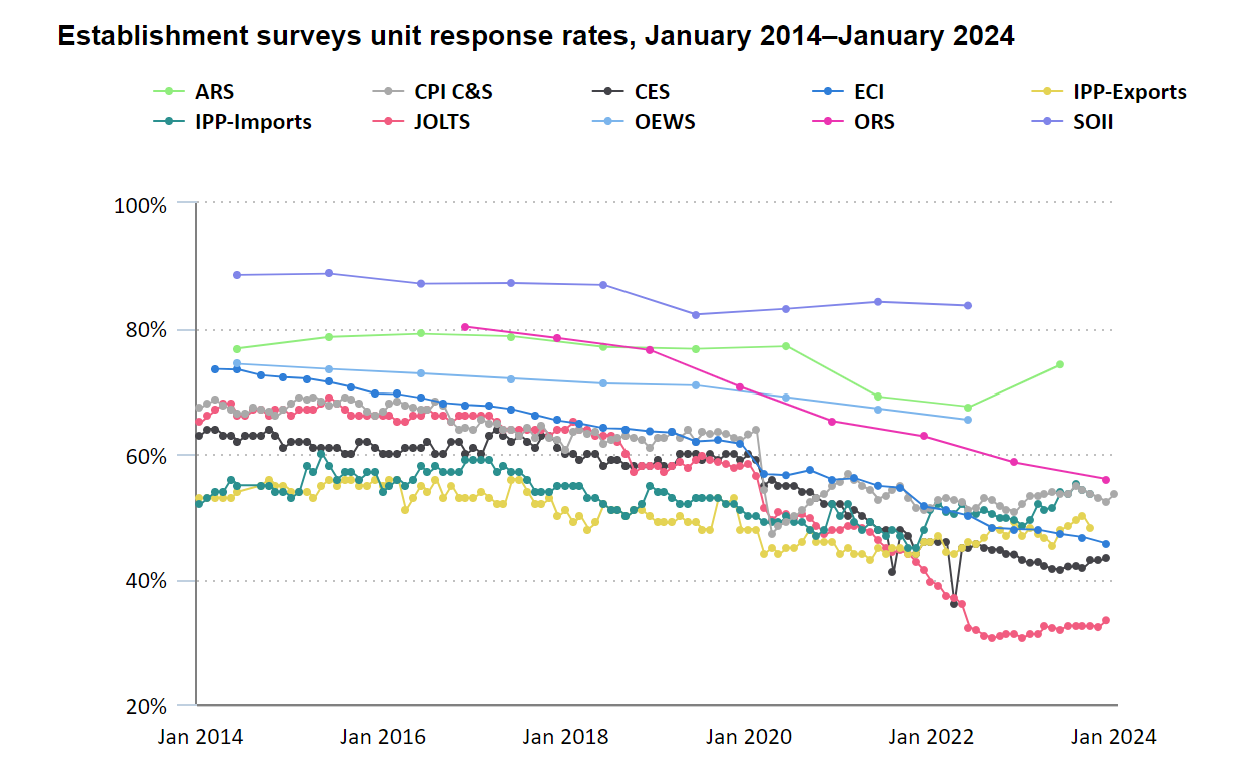

Finally, no matter what the “data” shows, let’s not forget that it is all just estimated, and it is safe to say that the real number of job openings remains still far lower since half of it – or some 70% to be specific – is guesswork. As the BLS itself admits, while the response rate to most of its various labor (and other) surveys has collapsed in recent years, nothing is as bad as the JOLTS report where the actual response rate remains near a record low 33%

In other words, more than two thirds, or 70% of the final number of job openings, is estimated!

And at a time when it is critical for Biden, pardon Kamala, to still maintain the illusion that at least the labor market remains strong when everything else in the economy is crashing and burning, we’ll let readers decide if the near record number of government job openings at a time when hiring and quitting are both crashing, is an accurate reflection of a strong labor market, or is merely a reflection of a debt-funded deep state gone full tilt. We’ll know the answer on Friday.

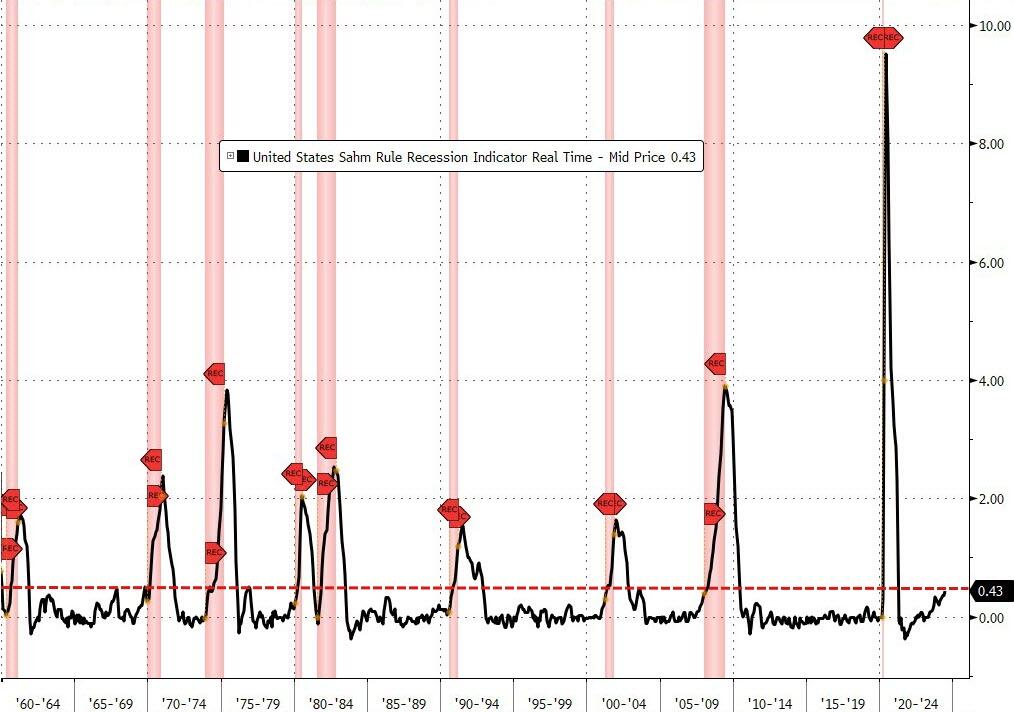

This isn’t the Sahm’s Club that is good fpr consumers. This is the club which crushes consumers. Better to be called Joe’s Club after our demented President Joe Biden.

This uptick triggers the Sahm Rule, a real-time recession indicator, suggesting that the US economy is in, or is nearing, a recession. The Sahm Rule, developed by former Fed economist Claudia Sahm, is designed to identify the start of a recession using changes in the total unemployment rate.

According to the rule, a recession is underway if the three-month moving average of the national unemployment rate rises by 0.50 percentage points or more, relative to its low during the previous 12 months. With the June 2024 U-3 rate of 4.1 percent, the average of the last three months being 4.0 and the lowest 12-month rate of 3.5 percent in July 2023, this criterion has been met.

Sahm Rule indications (1960 – 2024)

Source: Bloomberg

Surveys had forecast the U-3 rate to hold steady at 4.0 percent in June, unchanged from May 2024. The seemingly small 0.1 percent uptick, however, carries substantial implications for the broader economy. One possible confounding effect of the signal is growth in the labor force: If the labor force grows rapidly and the economy does not generate enough jobs to match the increase, the unemployment rate might rise and the Sahm Rule may be triggered, even if overall employment is increasing.

The rise of initial claims over the past few weeks, and nine consecutive increases in continuing claims, support the June 2024 Sahm indication.

Source: Bloomberg

Equity futures were flat just after the release, while Treasuries rallied across all maturities.

In recent months, Fed Chairman Jerome Powell has indicated that “unexpected weakness” may prompt a start to an accommodative policy stance without the additional data sought regarding the pace of disinflation. Historically, an increase in unemployment rates and the onset of a recession have led to policy adjustments aimed at stimulating economic growth and mitigating job losses, and the reversal of the rate hikes which began in 2022 to mitigate the highest inflation in four decades has been widely anticipated.

While more data will be required to confirm the Sahm Rule indication, the impact of accelerating prices, interest rates at their highest levels since 2007, and commercially suppressive pandemic policies have probably caught up with US producers and consumers.

Biden’s version of Sahm’s Club. Where the economy tanks and all he and his wife Jill care about is staying in Power. Perhaps we should call the sagging US economy “Joe’s Club.”

Like a bad “good news, bad news” joke,. June employment numbers are out from the Feral governement. The good news? Jobs added increased by 206k, more than expected.

The bad news? The unemployment rate hit 4.1%, the highest in 3 years.

Meanwhile, 1/3rd of jobs created were NON-PRODUCTIVE government jobs.

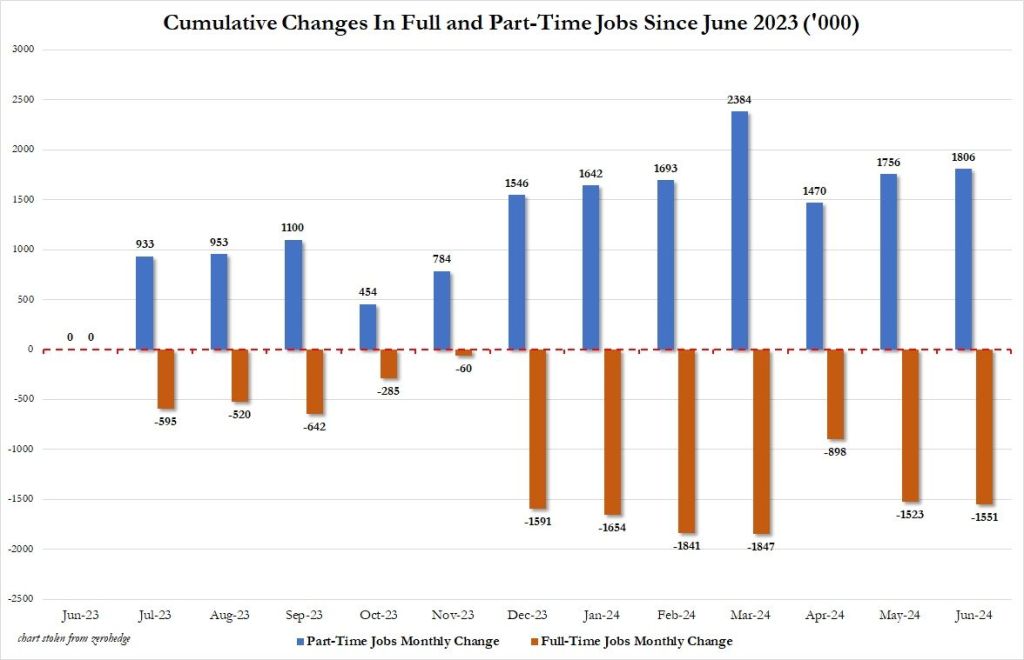

Since June 2023, the US has added 1.8 million part-time jobs and lost 1.6 million full time jobs.

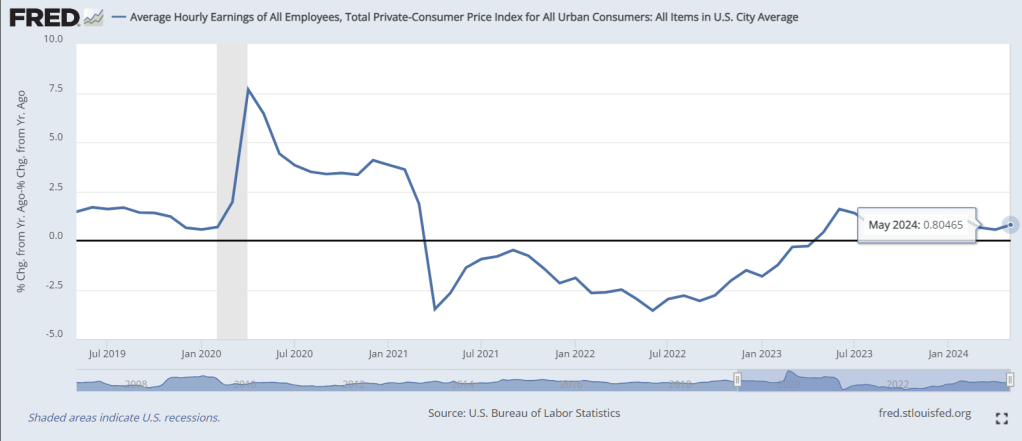

While nominal wage growth grew, REAL wage growth rose a measly 0.8% YoY.

The share of total new worth held by the top 1% is 30.4% while the total net worth held by the bottom 50% is a measly 2.5%.

So much for politicians’ promises to make everyone equal in wealth! Oddly, they keep getting wealthier and the bottom 50% keep losing ground.

No, Joe Biden isn’t Joltin’ Joe Di Maggio (the Yankee Clipper). Joe Biden is a Socialist who loves government and hates free markets. I feel like Biden and his junta are emuilating the old Soviet Union and Communism. Those of us who still love free markets are back on the chain gang.

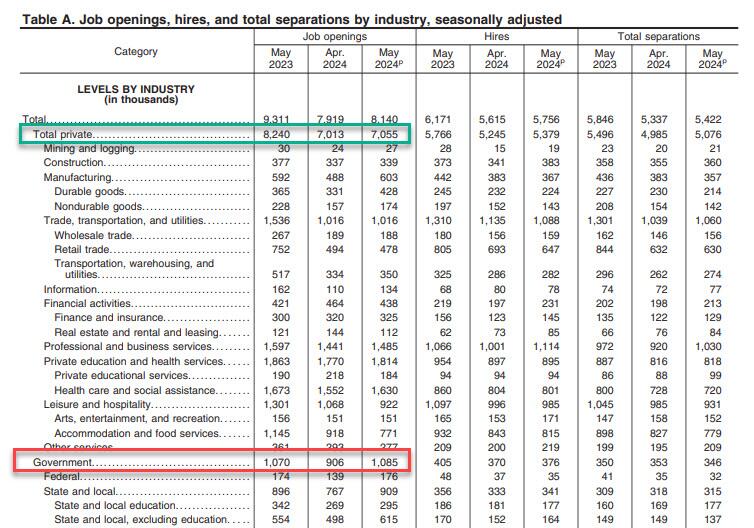

After two months of sharp declines in the number of job openings, moments ago Biden’s highly politicized Department of Labor reported that in May, the number of job openings unexpectedly spiked by a whopping 221K, to 8.140 million – far above the 7.950 million estimate – from a downward revised April print of 7.919 million, down 140K from the original print of 8.059 million.

Job revisions aside, there was only a 2.8% increase in private sector job openings in May. On the other hand, nonproductive job openings (aka, government) were up a staggering 20% in May.

C’mon man, hiring government workers doesn’t grow the economy in an organic way. Just a Soviet way.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.