2022 should be an interesting year as the wheels come off The Fed’s constant stimulation of markets.

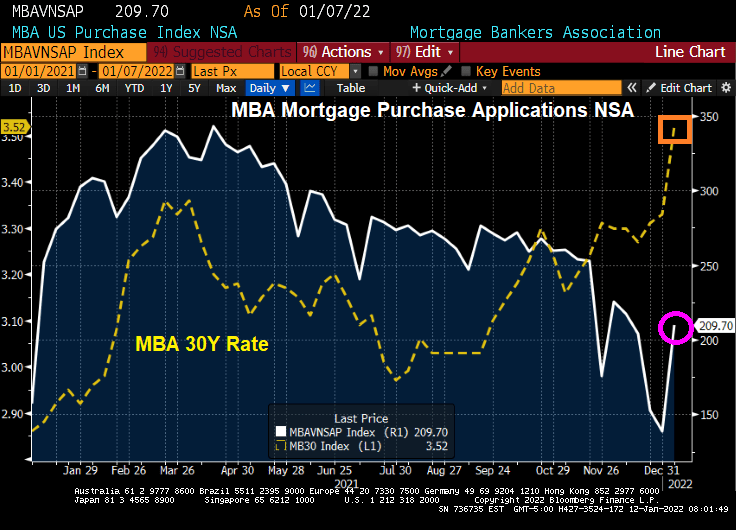

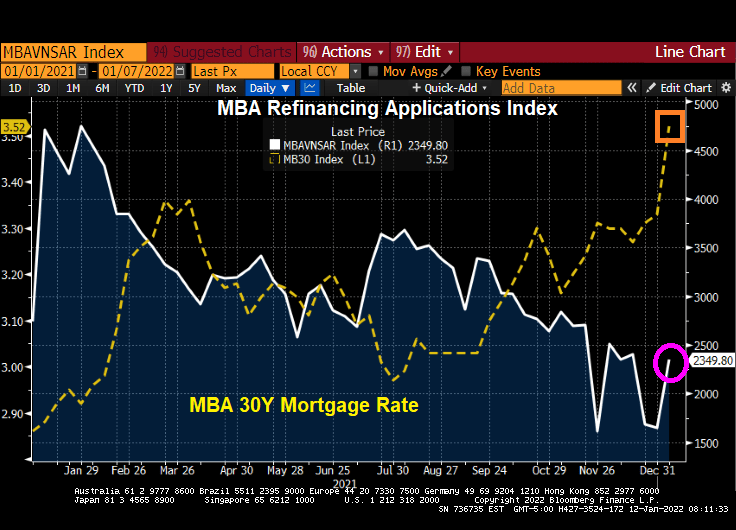

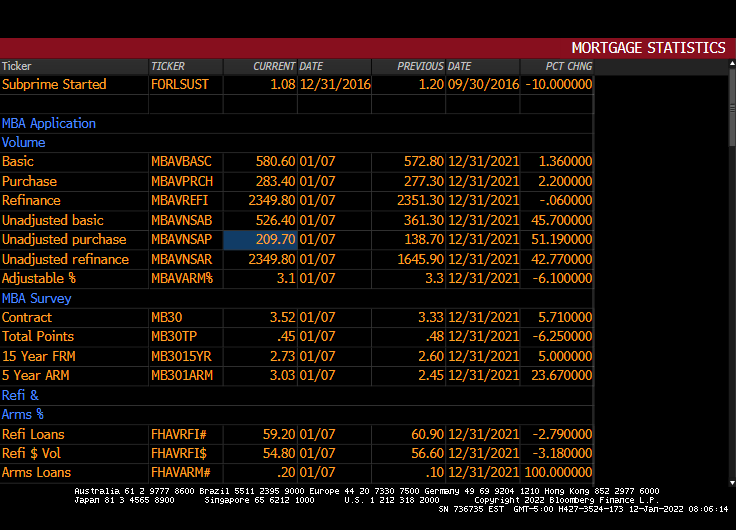

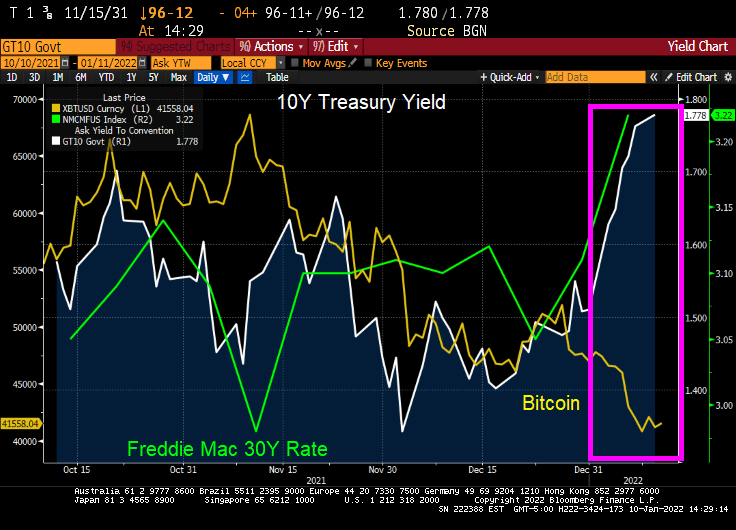

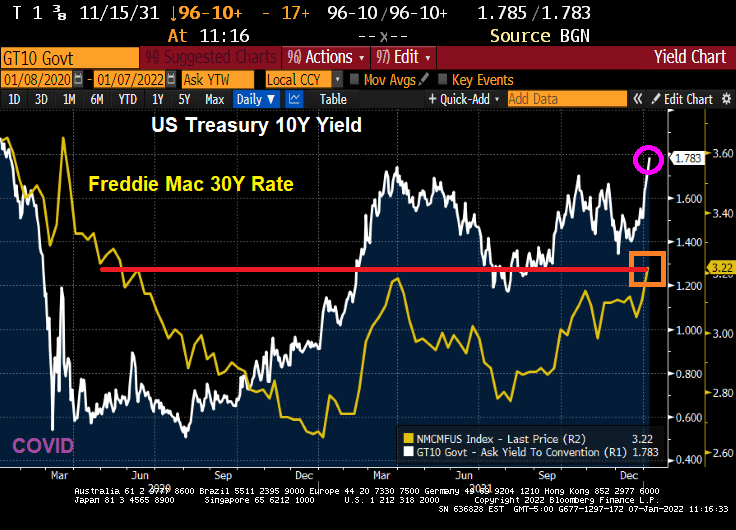

Today, we saw the 10-year Treasury Note yield almost hit 1.8% as mortgage rates rose to 3.22%.

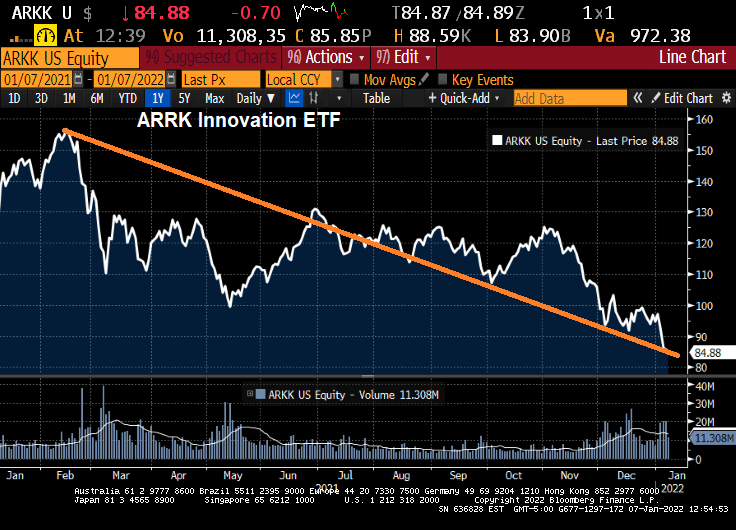

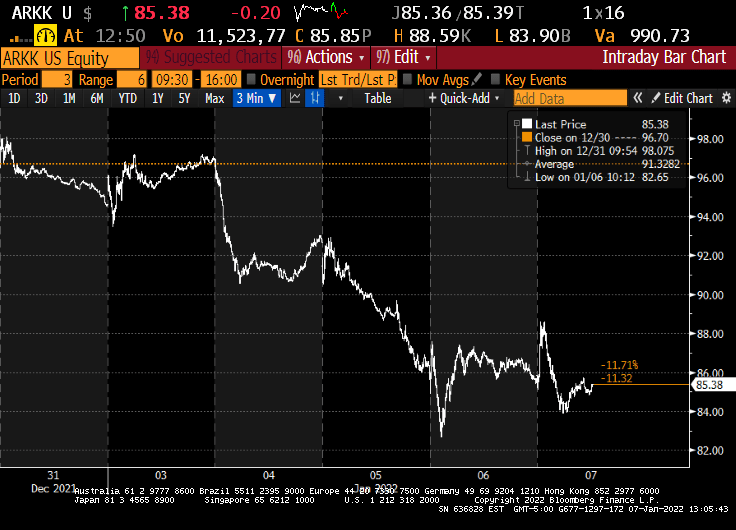

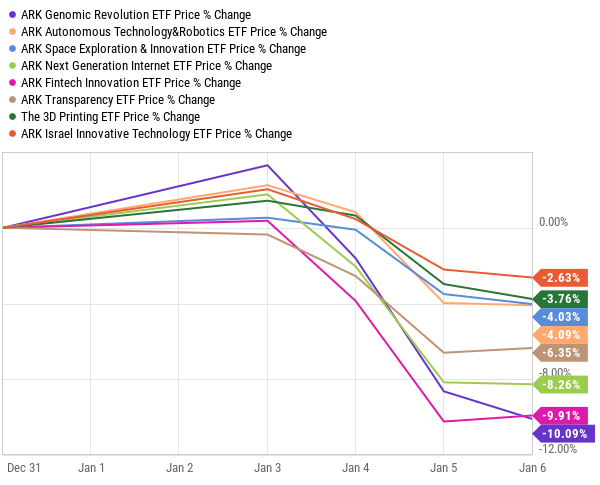

Unfortunately for crypto investors, bitcoin is having a bad 2022. And ethereum is feeling some pain as well.

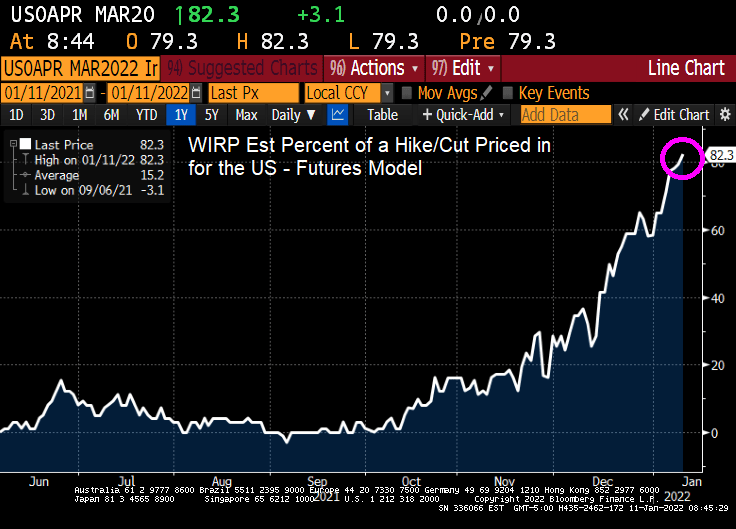

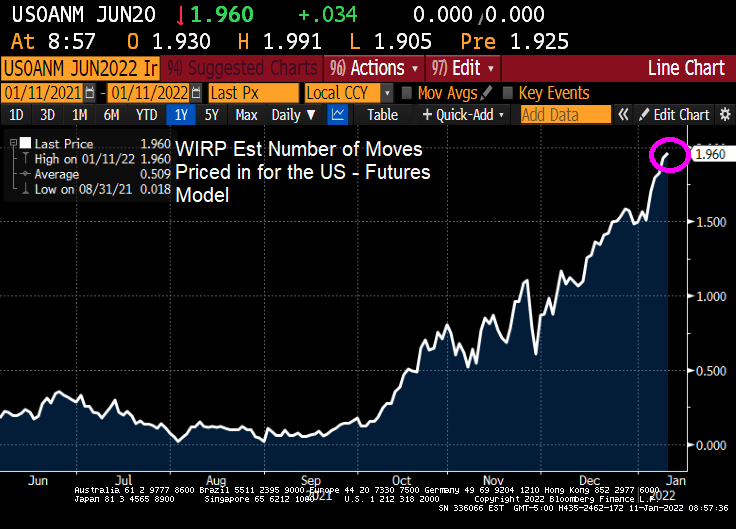

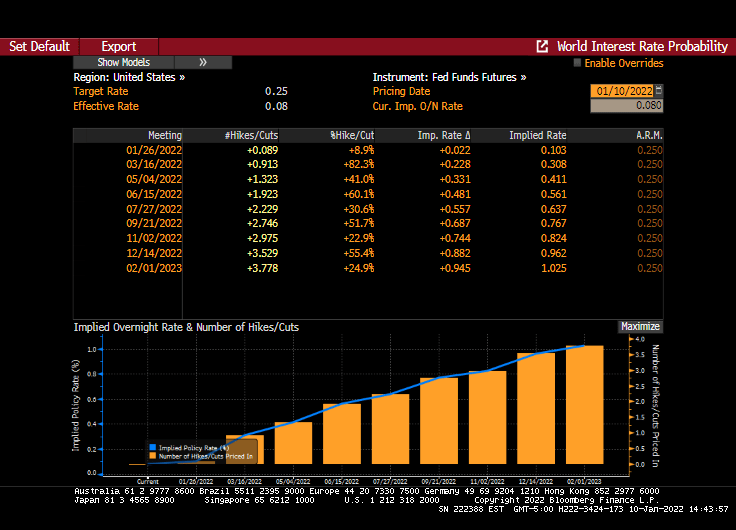

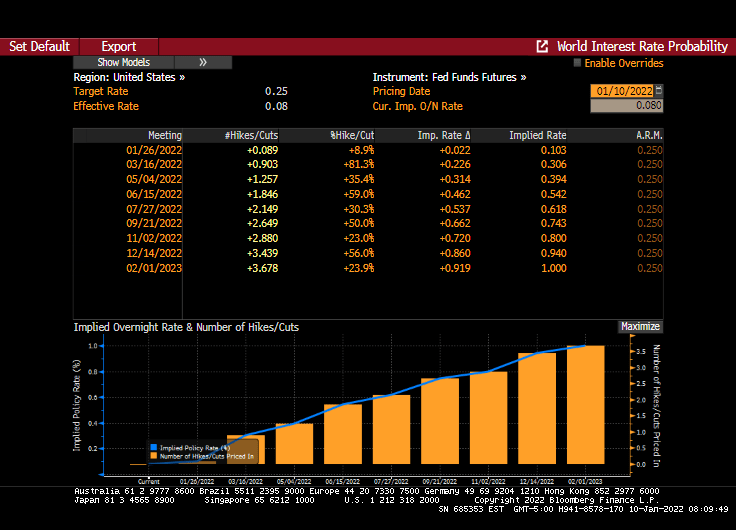

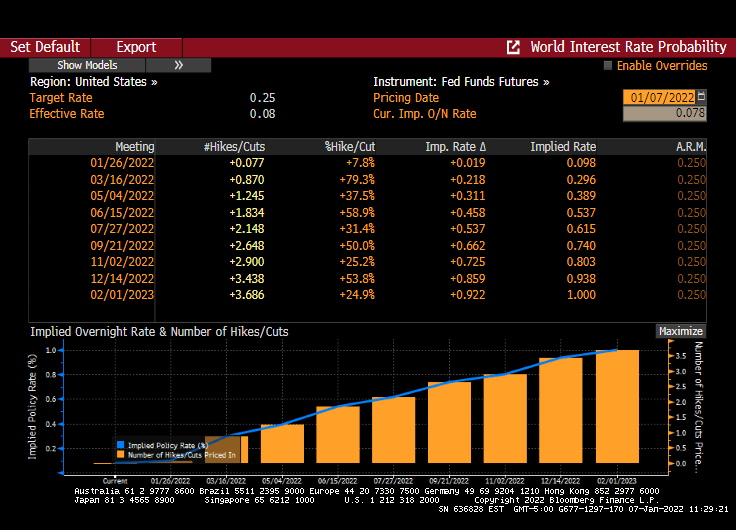

While Goldman Snakes predicted 4 rates increases in 2022, Fed Funds Futures are predicting almost 4 rates increases (3 in 2022 and 1 in Jan 2023 … almost).

So whatever is giving markets the jitters, I would follow the advice of Samuel L. Jackson from Jurassic Park: “Hold on to your butts.”

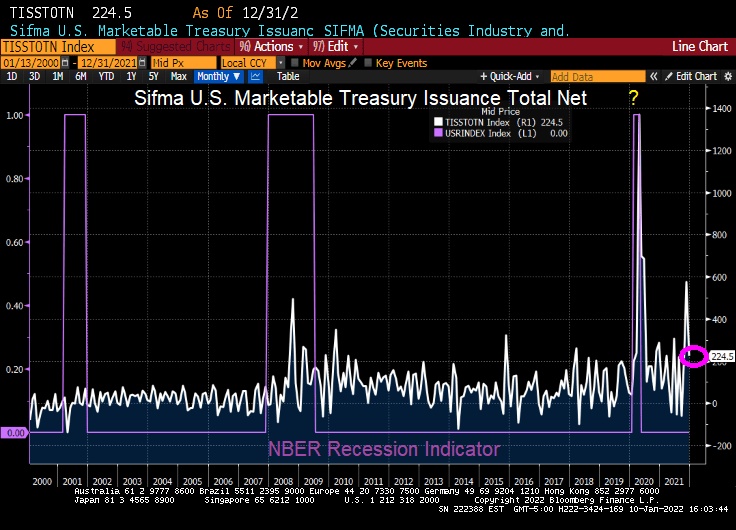

UPDATE: Did The Fed/Treasury seriously overreact due to COVID? Lool at Treasury issuance related to COVID recession versus the financial crisis (Great Recession) and the 2001 recession.

(Bloomberg) — The Federal Reserve will likely raise interest rates four times this year and will start its balance sheet runoff process in July, if not earlier, according to Goldman Sachs Group Inc.

Rapid progress in the U.S. labor market and hawkish signals in minutes from the Dec. 14-15 Federal Open Market Committee suggest faster normalization, Goldman’s Jan Hatzius said in a research note.

“We are therefore pulling forward our runoff forecast from December to July, with risks tilted to the even earlier side,” Hatzius said. “With inflation probably still far above target at that point, we no longer think that the start to runoff will substitute for a quarterly rate hike. We continue to see hikes in March, June, and September, and have now added a hike in December.”

In its December meeting minutes, Fed officials signaled they are preparing to move quicker than the last time they tightened monetary policy in a bid to keep the U.S. economy from overheating amid high inflation and near-full employment. These conditions — along with a larger balance sheet that’s suppressing longer-term borrowing costs — “could warrant a potentially faster pace of policy rate normalization,” the minutes said.

Officials also saw the timing of reducing the $8.8 trillion balance sheet as likely “closer to that of policy-rate liftoff than in the committee’s previous experience,” according to the minutes.

While Goldman sees 4 rate hikes in 2022, The Fed Funds Futures market only sees 3 rate hikes and the Fed Funds target rates hitting 1% by Feb 2023.

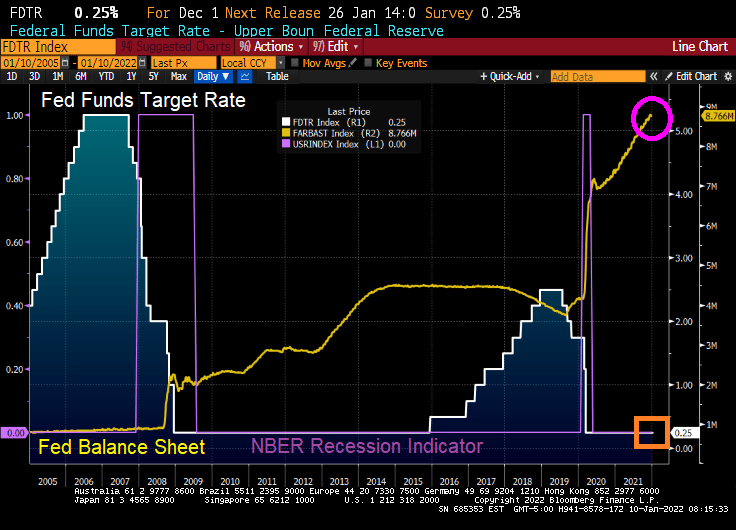

An increase to 1%? The Fed Funds target rate hit 5.25% during the housing bubble in 2006/2007 and markets are worried about an increase to 1%??

So, Goldman thinks that there will be faster “run-off” than expected. This simply means that The Fed will allow Treasuries and Agency MBS to mature rather than actually sell securities.

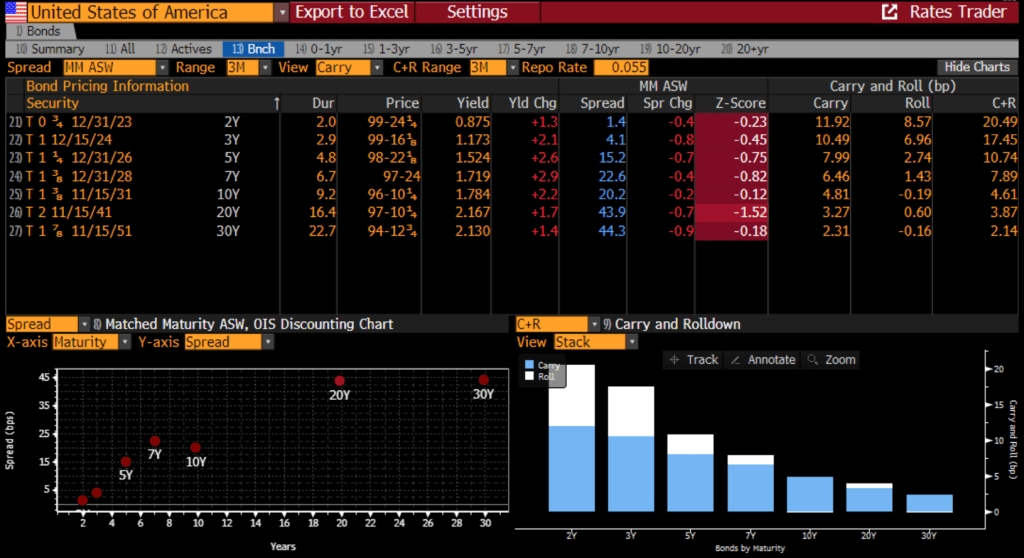

With the expectation of Fed activity, z-scores for Treasuries are negative across the board.

So we shall see if The Fed Open Market Committee are hawks, doves or “birds of war.”

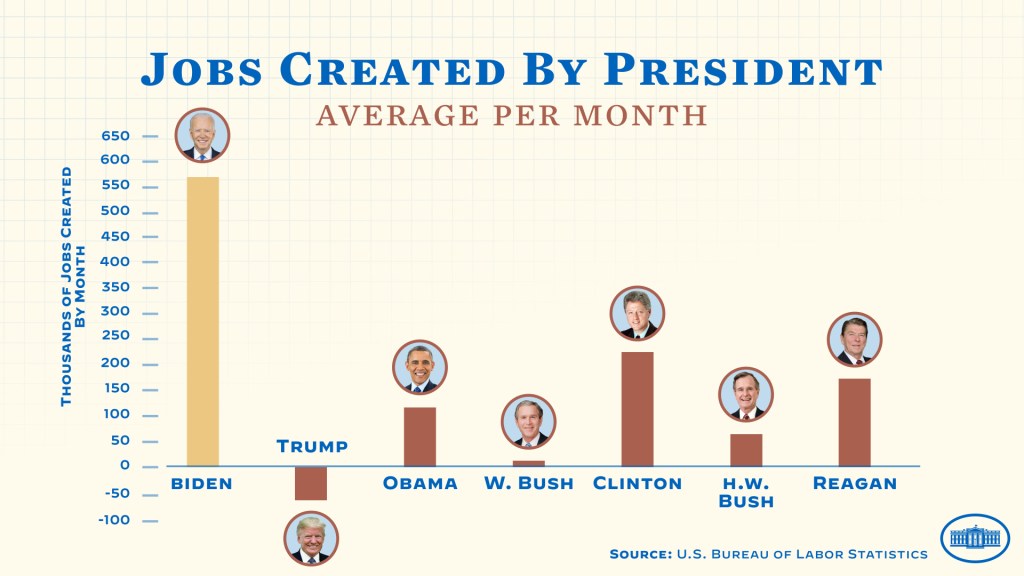

Recently, the White House claimed that the Biden Administration created more jobs (per month) than Trump, Obama, George W Bush, George HW Bush, Clinton and Reagan.

It always helps to be elected President after a recession when the economy naturally snaps back from the economic doldrums (like Obama after the financial crisis, Clinton after the first Gulf War, Reagan after Carter).

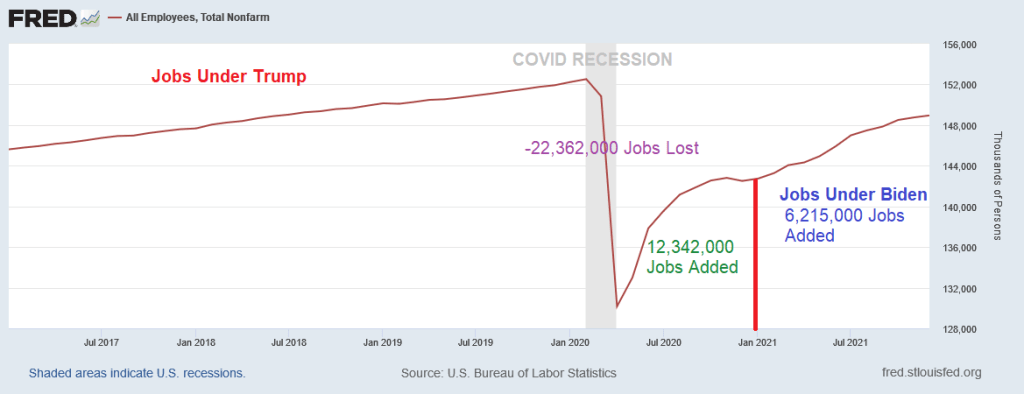

So let’s look at job totals under Trump, the COVID lockdowns, the ensuing economic damage, and the Biden “rebound.” In a brief two months in early 2020 thanks to COVID and lockdowns, the US economy lost 22.362 MILLION jobs. But the snap-back effect under Trump was 12.342 MILLION jobs added back by the time Biden was sworn-in as President.

Under his term as President, Biden has benefited from “Snap-back inertia” and saw 6.215 MILLION jobs added in just a year. Pretty impressive, except that it is about half the snap-back effect experienced under Trump.

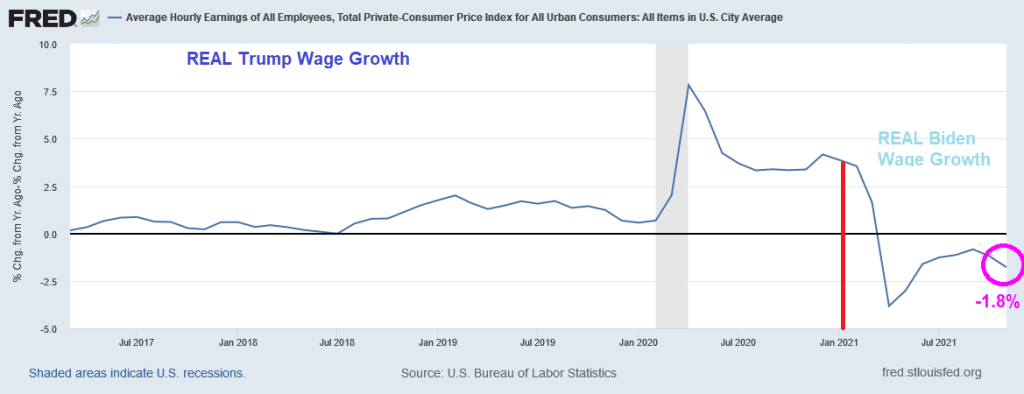

How about REAL wage growth (nominal wage growth less inflation)? Real wage growth was higher under Trump and has been declining under Biden. Strange that the White House isn’t bragging about declining real wage growth under Biden.

Let’s see how Omicron impacts the labor market and whether Biden/Psaki will take credit for the snap-back from Omicron.

Call this the Biden malaise (or Ka-malaise) for wage growth. Where inflation nukes positive wage gains.

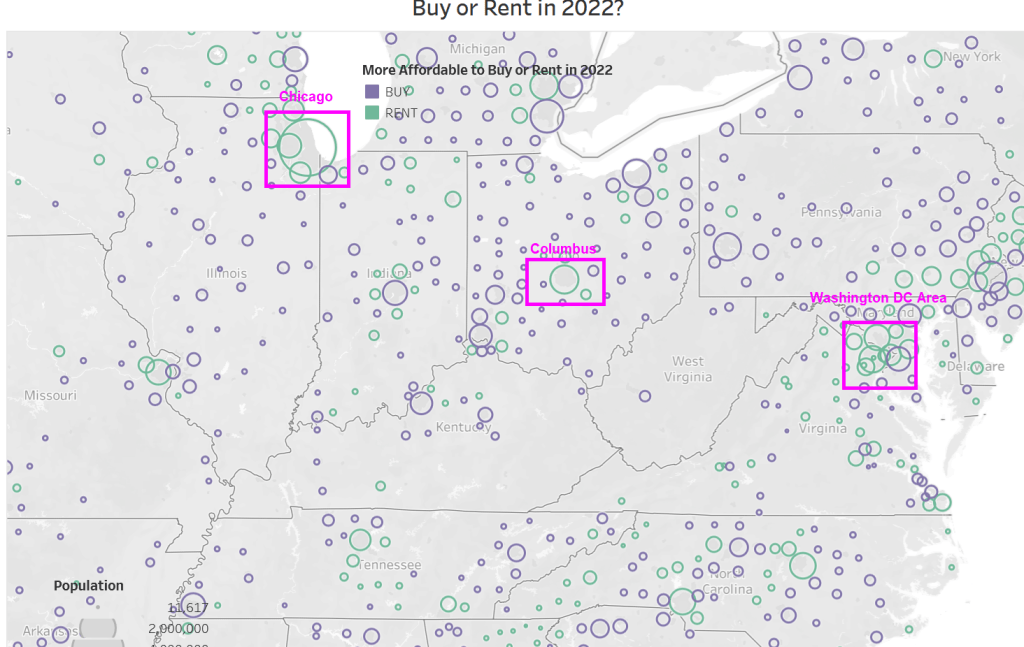

According to Attom, US home prices are growing faster than rents in nearly 90 percent of the nation; but prices are still more affordable in almost 60 percent of U.S. markets; Renting remains more financially viable in most-populous urban areas.

If we look at Attom’s map of affordability, you can see that in western states, it is more affordable to rent. And in megalopolis (Boston, New York, Philadelphia, Washington DC). And Miami. But elsewhere in the eastern states, it is more affordable to buy than to rent.

Of course, any where I live like Phoenix, Fairfax VA, Chicago IL, and Columbus OH it is more affordable to rent than to own.

You will notice that the areas where buying is more affordable than renting tend to be smaller towns with slower growth, while larger cities tend to be more affordable to rent.

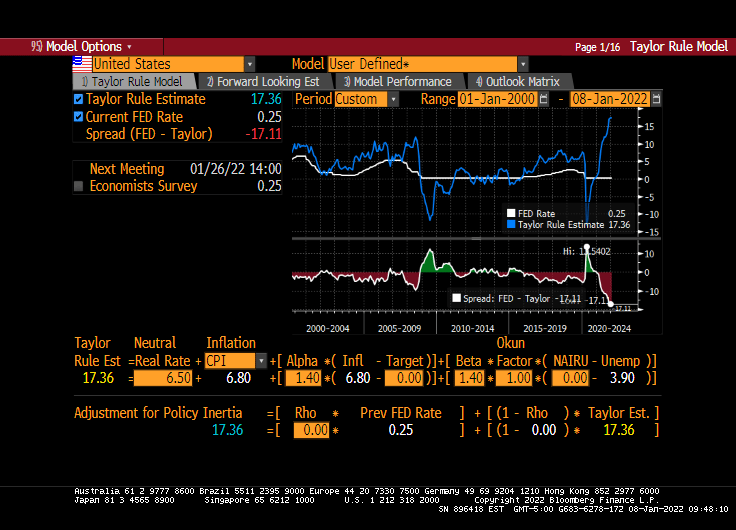

It is somewhat mystifying that markets would be soooooo sensitive to 3 rate increases from The Fed, particularly since the Taylor Rule suggests that The Fed’s target rate should be 17.36%. Even if you don’t like the Taylor Rule or disagree with its inputs, you must admit that the gap between where The Fed is (0.25%) and where they should be (17.36%) is … k-razy.

It looks like markets are buying into the prospect of The Federal Reserve raising rates three times (Bob) in 2022. And ceasing COVID monetary stimulus.

Today, the 10-year Treasury yield rose to PRE-COVID levels of 1.783%. And the Freddie Mac 30-year mortgage commitment rate rose to 3.22%, the highest since May 2020.

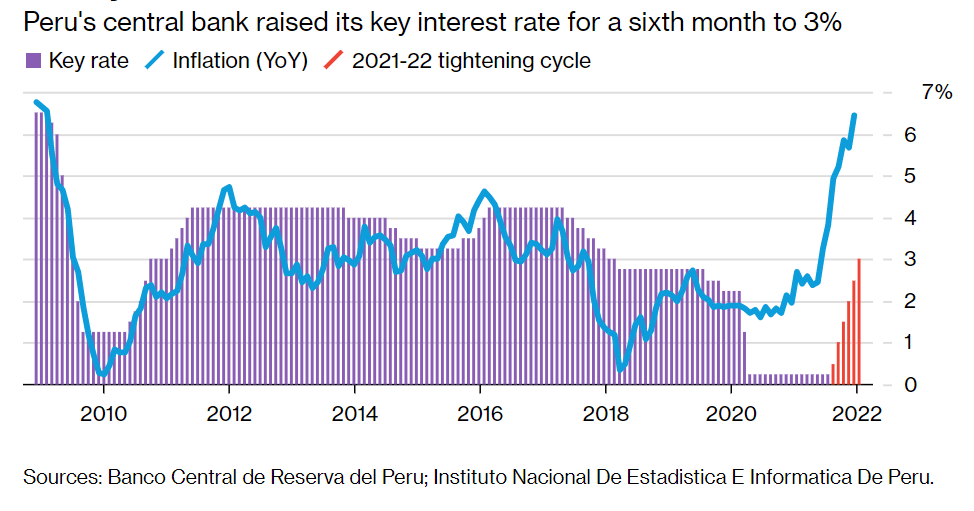

Today’s rising wage rates (although negative in terms of REAL wage rates) will likely put a Peruvian fire under The Fed’s behind. As of this morning, Fed Funds Futures are still pointing to three rate increases in 2022 (May, July and December).

And The Fed is supposed to be winding down the COVID monetary stimulus.

Why a Peruvian fire? Even Peru’s central bank is raising its key interest rate to 3% after soaring inflation.

Let’s see if Powell and The Gang follow through … or reveal themselves to be Peruvian Chickens.

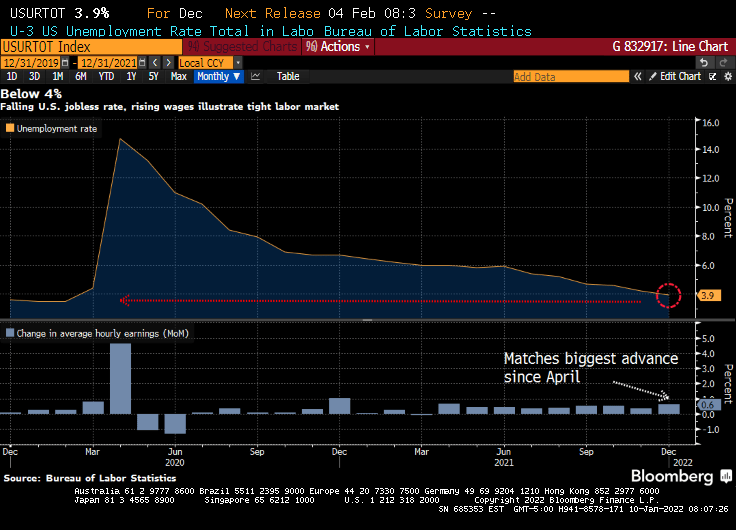

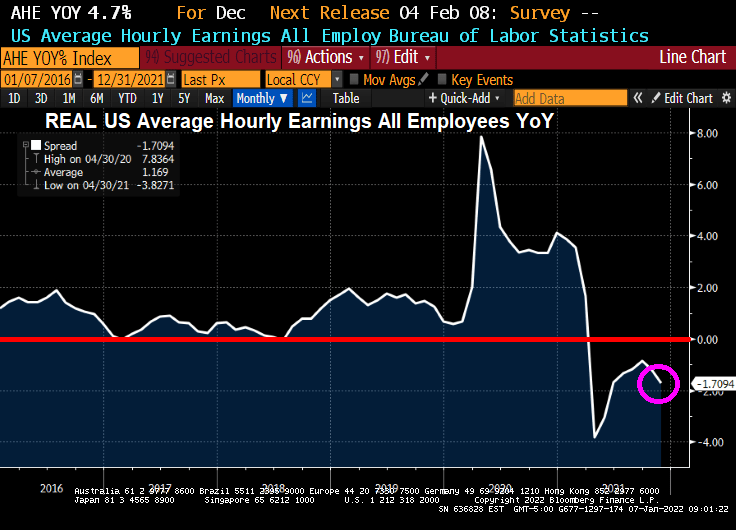

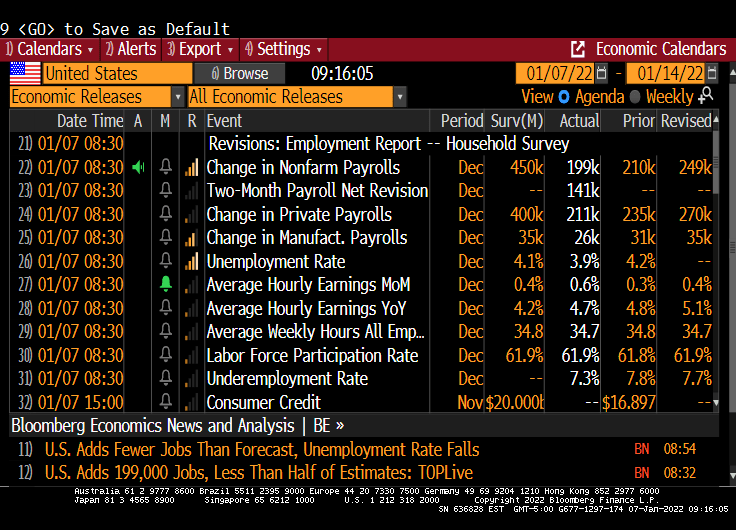

The November jobs report is out and the highlight is that US Average Hourly Earnings GREW at a rate of 4.7% YoY. Unfortunately, inflation is still raging resulting in REAL US Average Hourly Earnings DECLINING at a rate of -1.71% YoY.

REAL US home price growth is slowing and is at 12.856% YoY as REAL average hourly earnings slowed to -1.7094% YoY.

The lowlight of the November jobs report is that only 199K jobs were added versus the 450K jobs expected to be added. At least the unemployment rate fell to 3.9%.

WHERE we the jobs added? Leisure and hospitality led the way! Hey bartender.

Yes, REAL wage growth and REAL home price growth are slowing.

You must be logged in to post a comment.