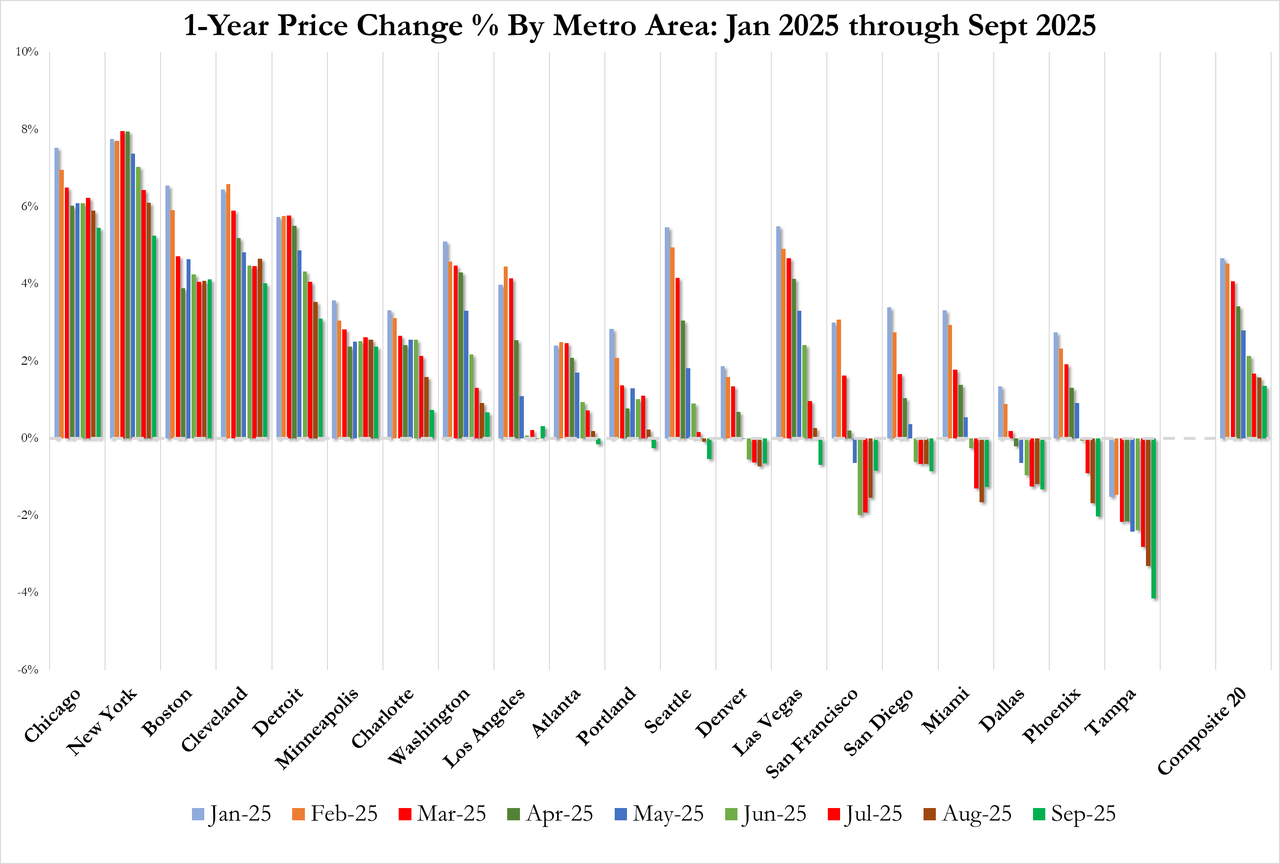

This is the opposite of the housing bubble from The Big Short where home prices in Phoenix, Las Vegas, Los Angeles and Florida rose then crashed. Instead, the fastest growing cities are in the northeast and midwest.

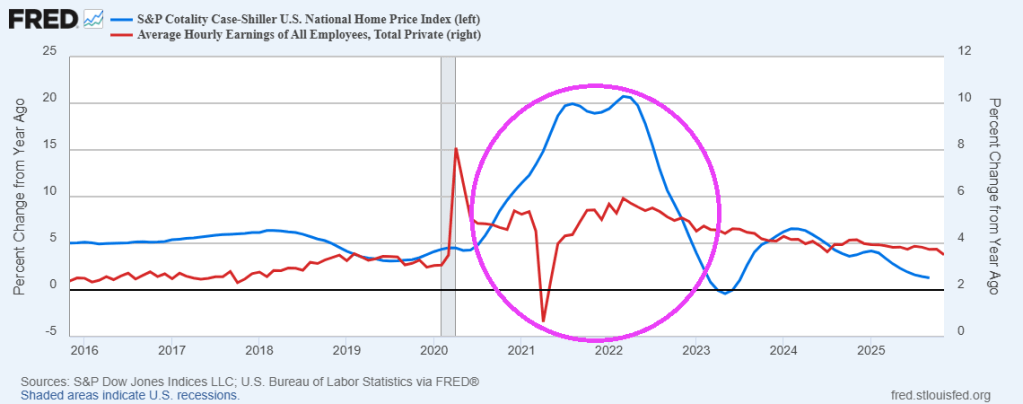

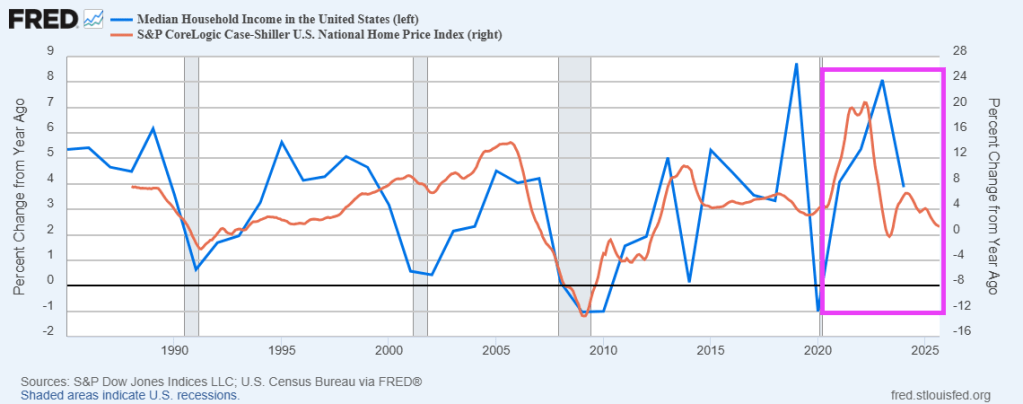

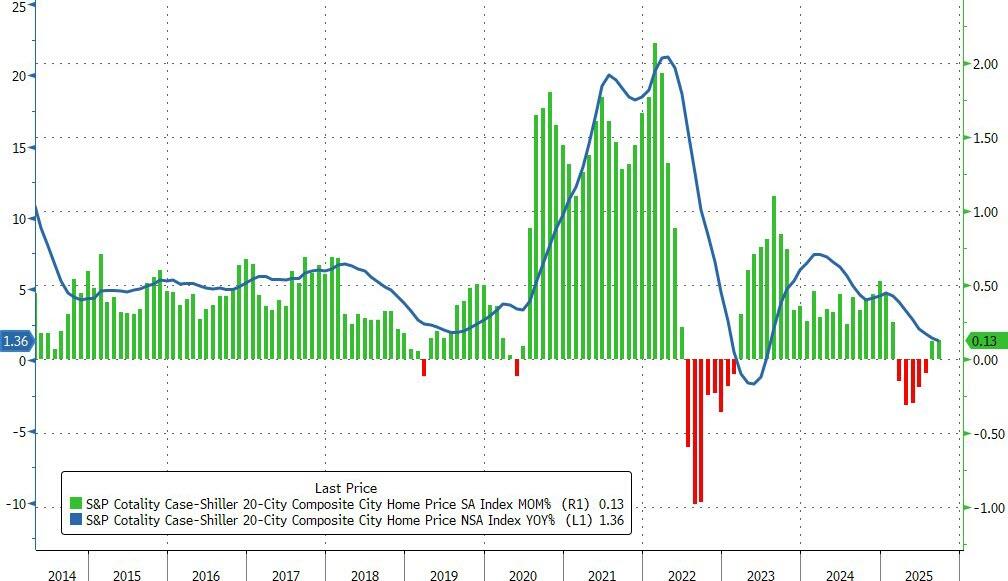

The Case-Shiller 20-City Home Price Index rose 1.3% year over year in October 2025, easing from a 1.4% increase in September and coming in slightly above market expectations of a 1.1% gain. This represents the smallest annual increase since July 2023, reinforcing signs that the US housing market is settling into a much slower growth phase. Home price appreciation continues to trail consumer inflation. With October CPI estimated at around 3.1%, inflation-adjusted home values appear to have edged modestly lower over the past year.

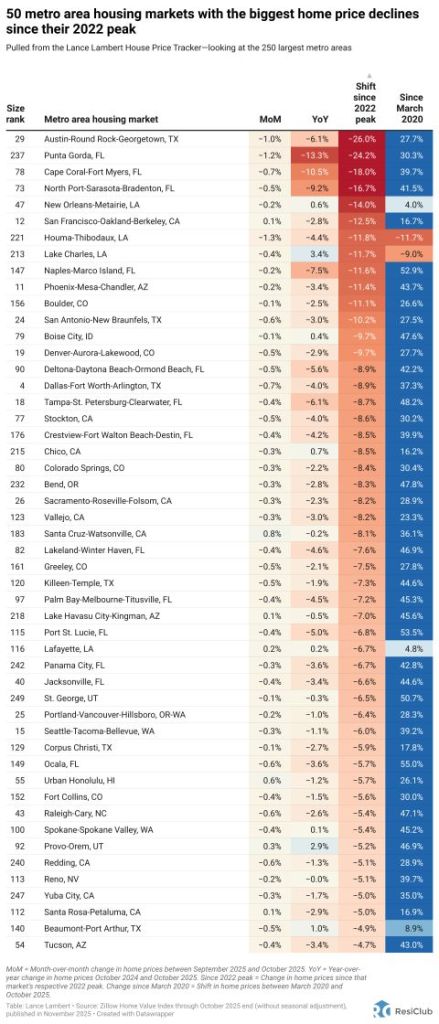

Regional data point to a pronounced geographic rotation. Chicago now leads all major markets with a 5.8% annual gain, followed by New York at 5.0% and Cleveland at 4.1%. In contrast, Tampa recorded a 4.2% decline, the steepest among the 20 cities, and its 12th consecutive month of falling annual prices. Other former pandemic boom markets, especially in the Sun Belt, are seeing the sharpest declines, led by Phoenix (-1.5%), Dallas (-1.5%), and Miami (-1.1%).

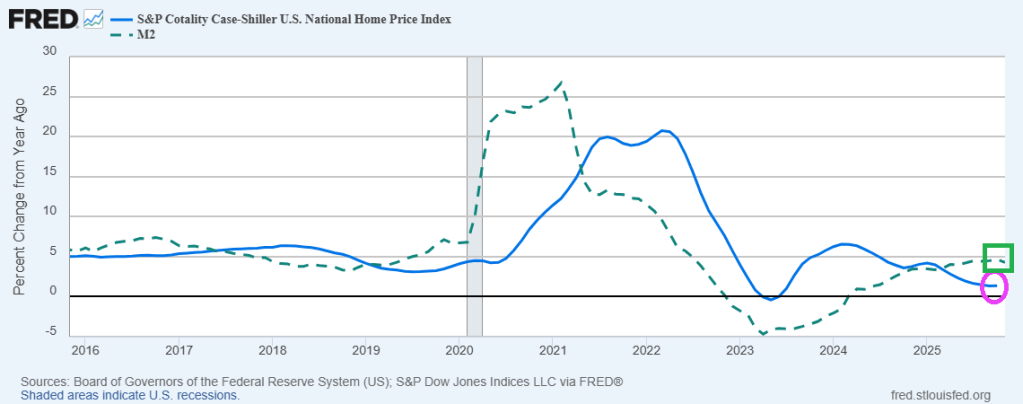

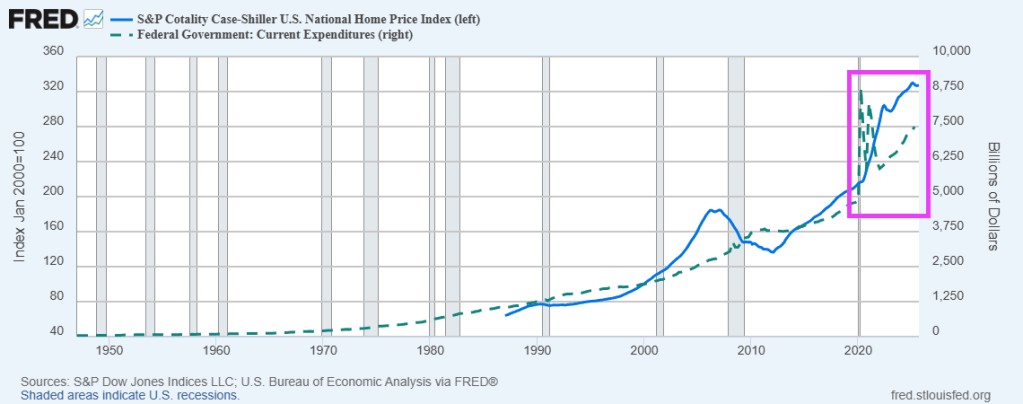

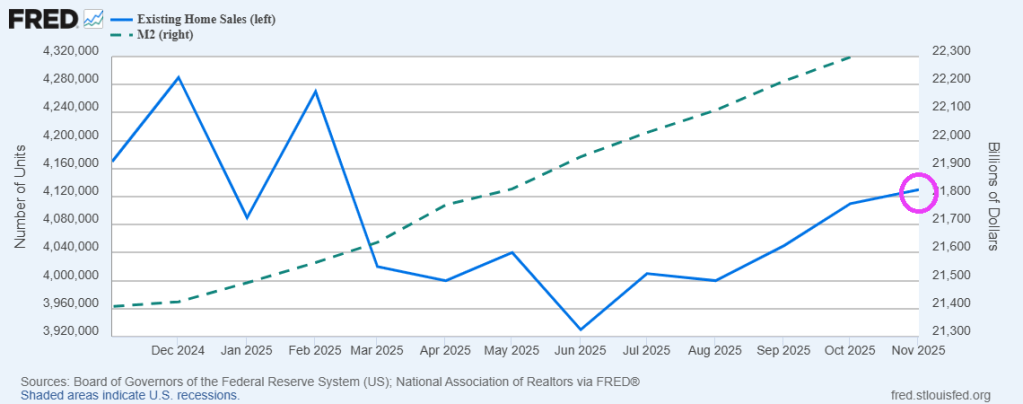

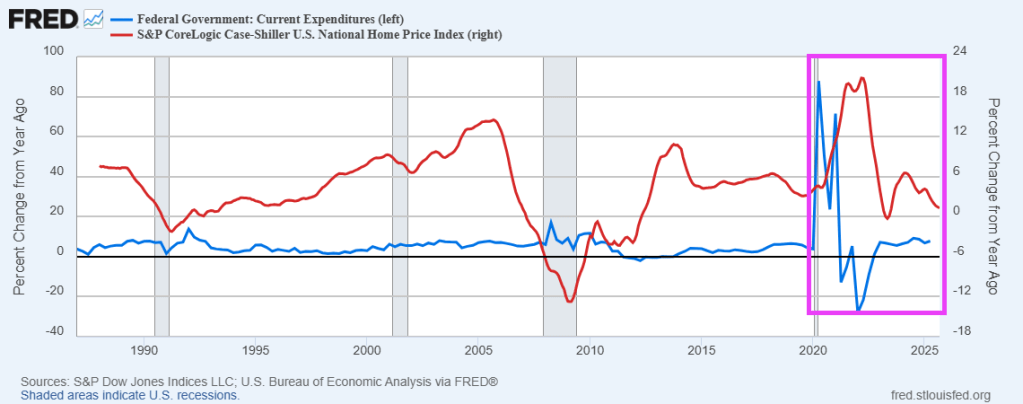

Housing price growth has stalled even though M2 money growth is higher YoY.

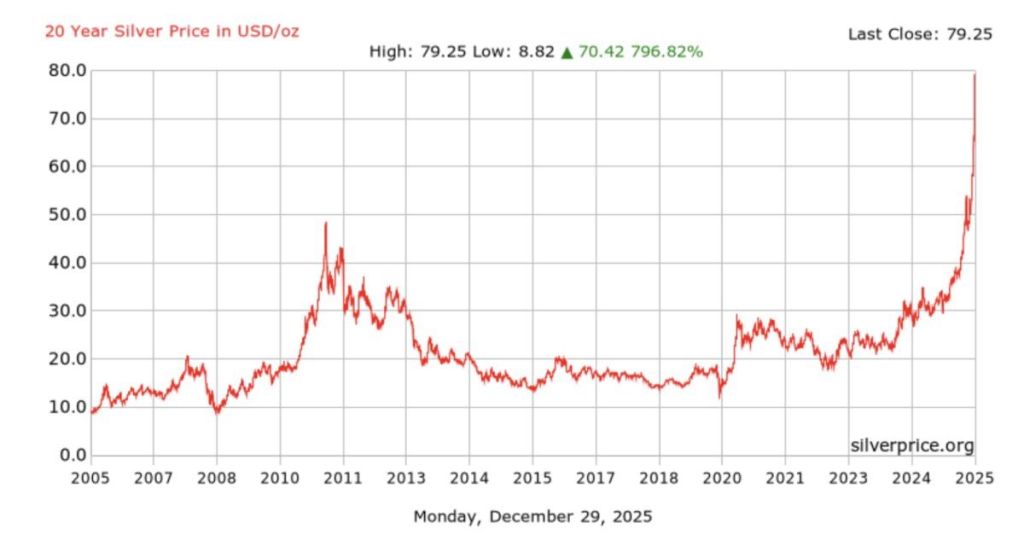

On the silver front, silver regained losses yesterday, but increased margin requirements are causing losses again.

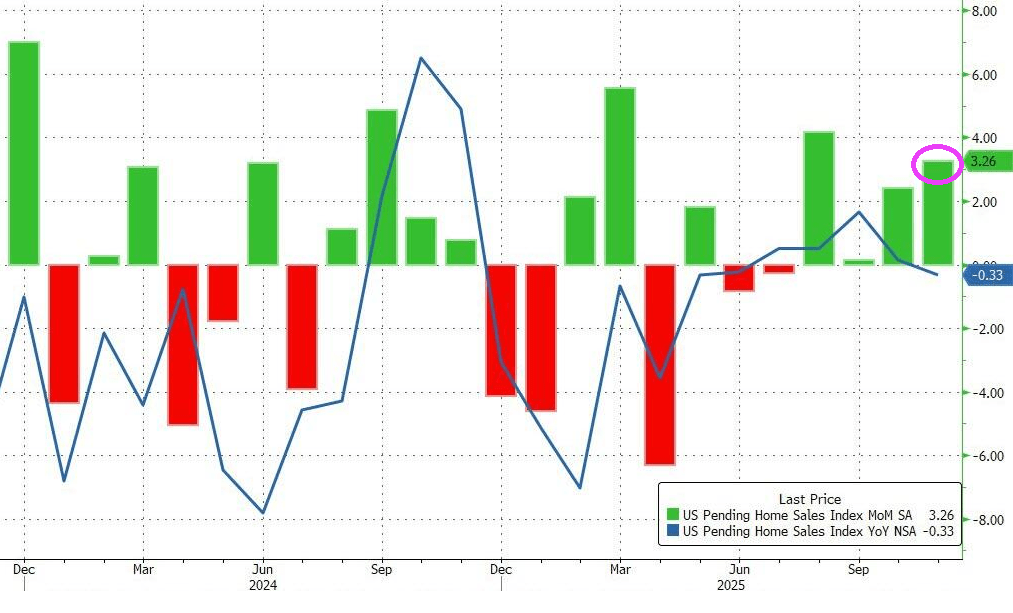

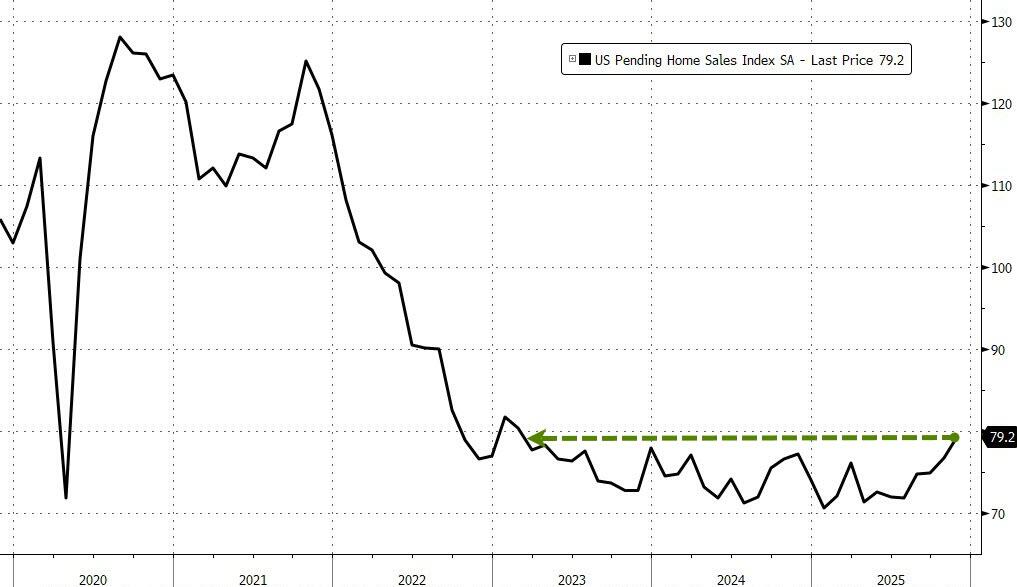

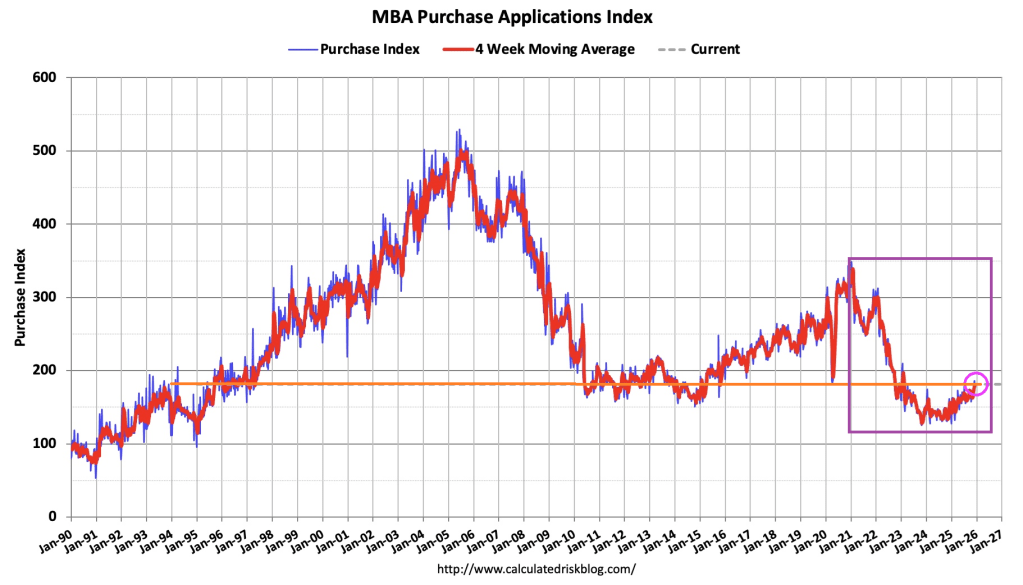

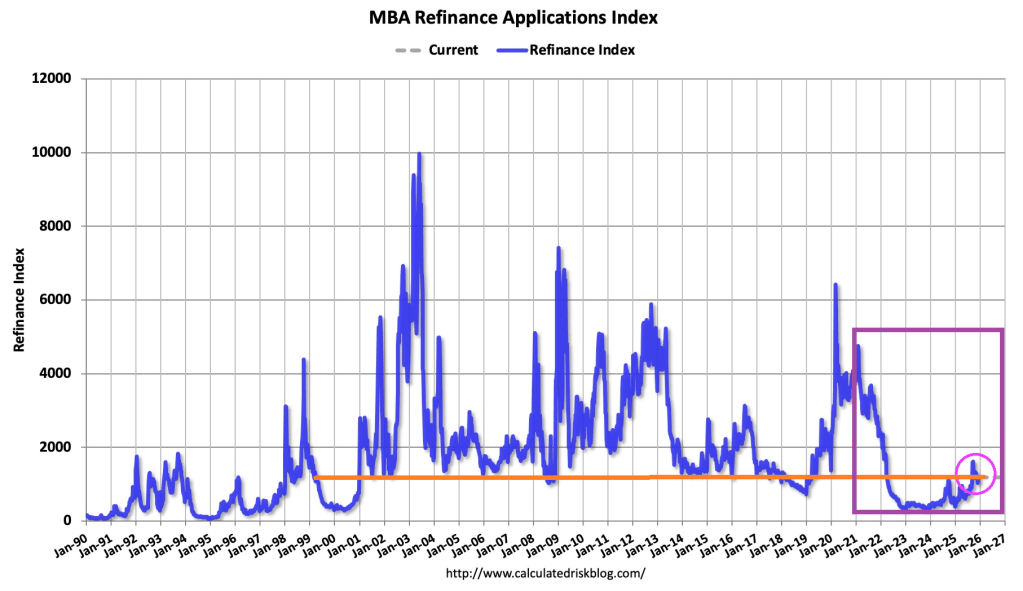

Today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.