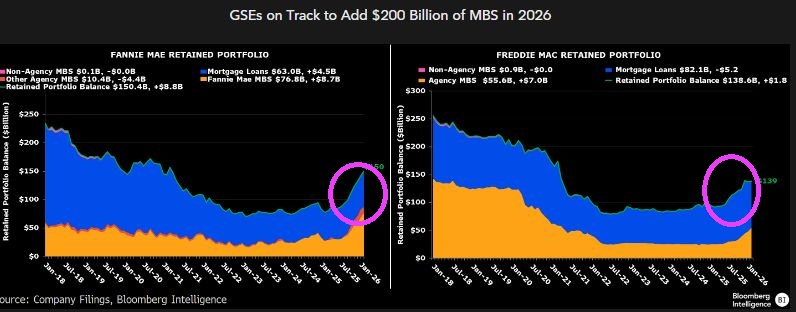

I spoke at the American Action Forum in Washington DC on the future of government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. Speaking with me was Laurie Goodman from The Urban Institute. Laurie loves Fannie Mae and Freddie Mac and argued passionately against shutting them down. I argued to shrink their retained portfolios to zero and privatize them.

When Trump was elected President for the second time and the House of Representatives was controlled by Republicans, there was hope that Fannie Mae and Freddie Mac would be privatized. But alas, it was not to be.

In fact, the retained portfolios for Fannie Mae (left) and Freddie Mae (right) are increasing, not decreasing.

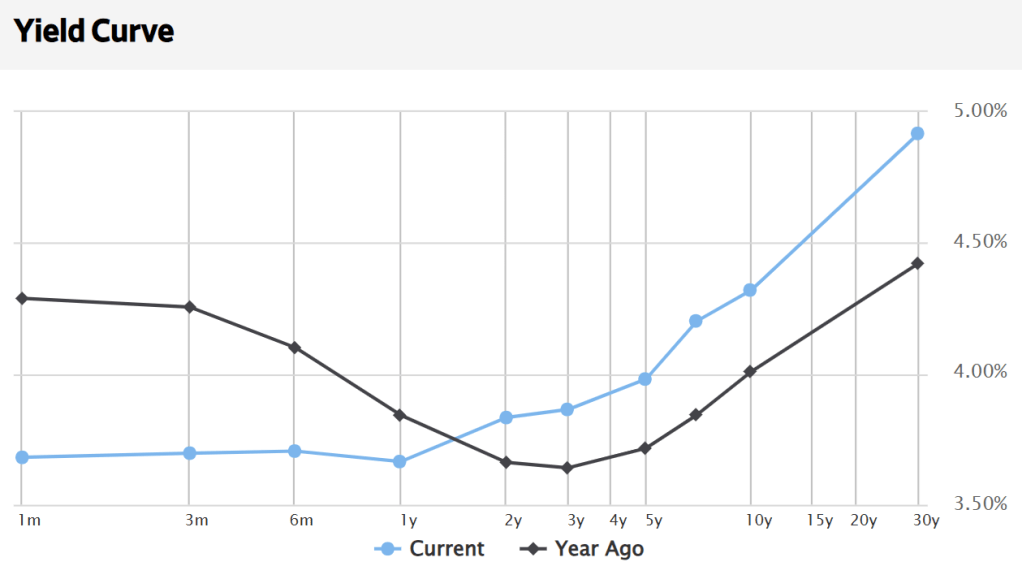

Trump’s threats of bombing Iran back to the stone age continues. But the impact on Treasury yields is interesting. As the US economy continues to grow, the US Treasury curve takes on the familiar upward slope. With rising long rates. Particularly when compared to the negative humped yield curve of a year ago.

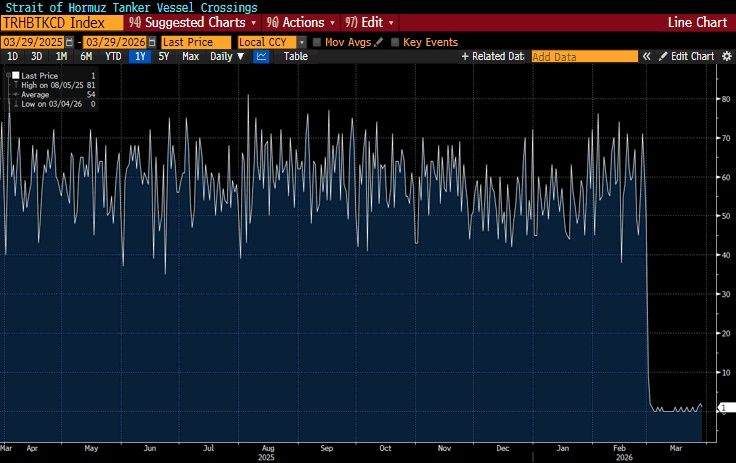

The Strait of Hormuz, a choke point for Middle East crude oil delivery to the rest of the world, has witnessed vessel crossings grinding to a near halt.

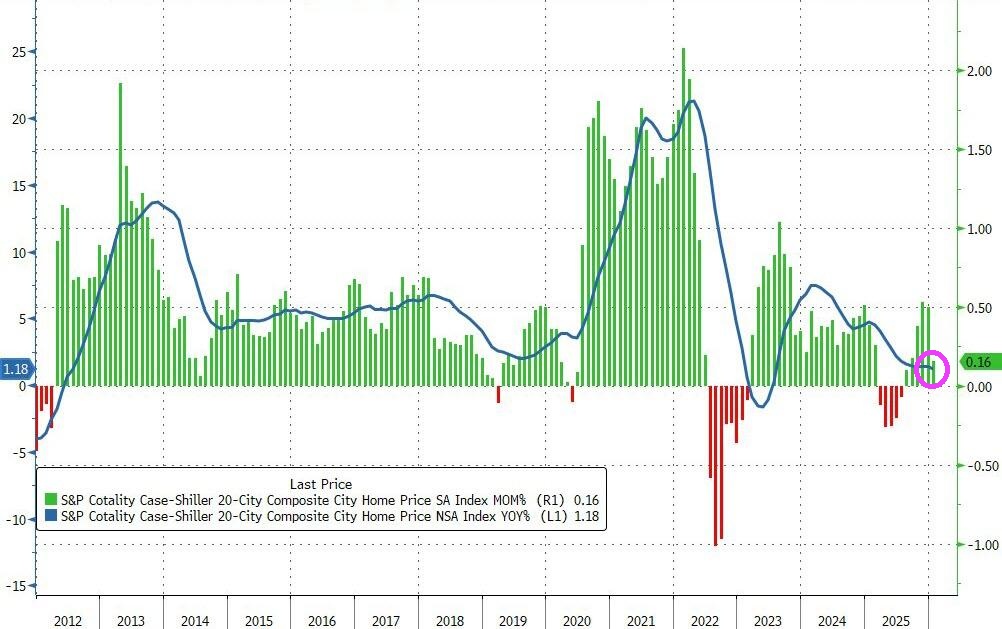

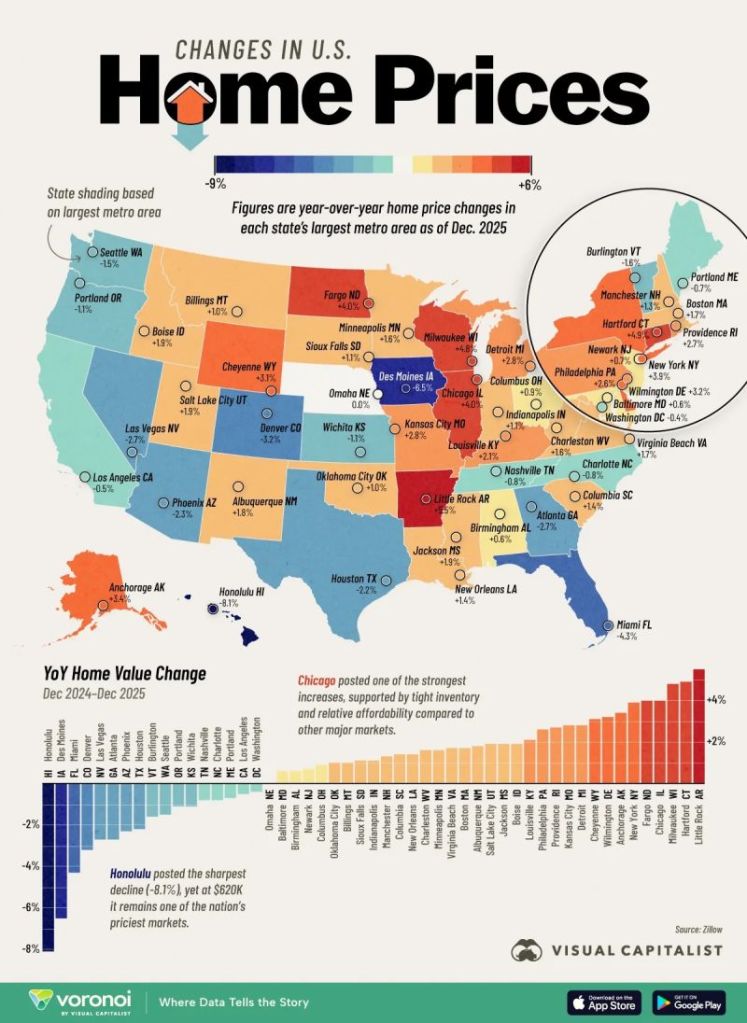

We are seeing mean reversion in home prices in red cities and blue cities.

The price of homes in America’s to 20 cities rose just 0.16% MoM in January (the lowest MoM rise since August and well below the 0.35% MoM expected.

Source: Bloomberg

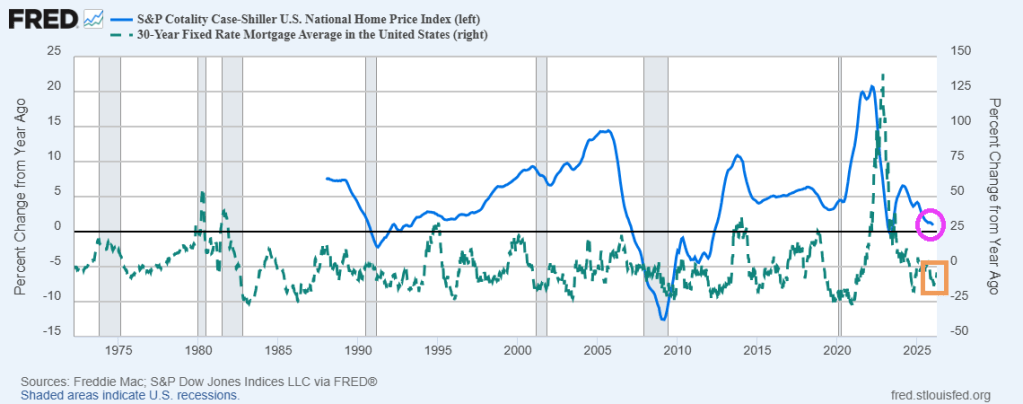

Home prices rose 0.9% YoY as mortgage rates have fallen. Home prices are still too high.

New York leads with a 4.9% annual gain, followed by Chicago at 4.6% and Cleveland at 3.6%, while Tampa fell 2.5%…

Don’t be confused. This isn’t leftists running to blue cities. It is mean reversion. The prior fleeing blue cities to red cities created a mean reversion effect where red cities home prices rose too fast and blue cities fell too fast.

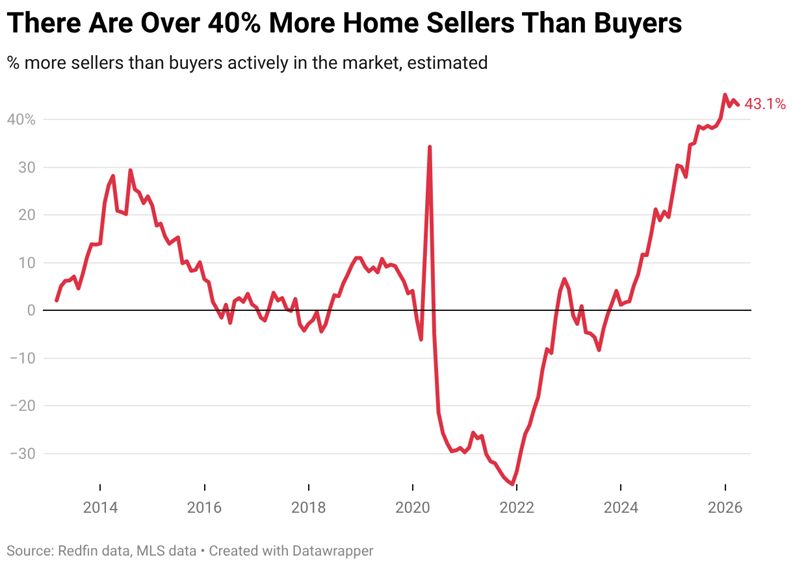

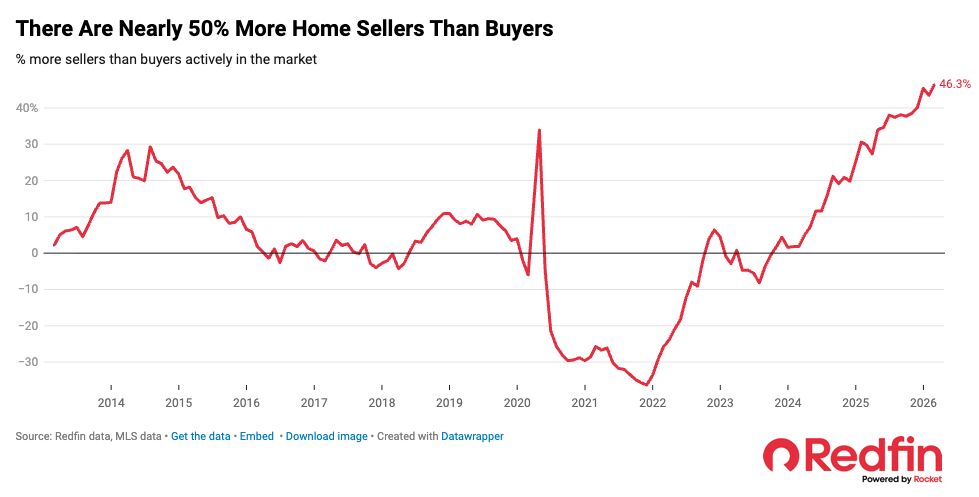

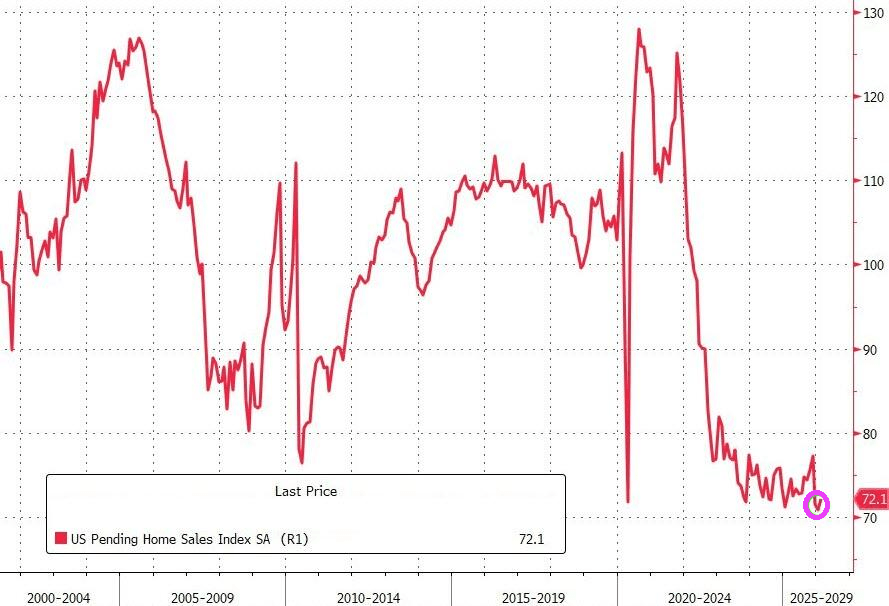

Nothing has been the same in the US housing market since the Covid outbreak of 2020. According to Redfin, there are nearly 50% more home sellers than buyers.

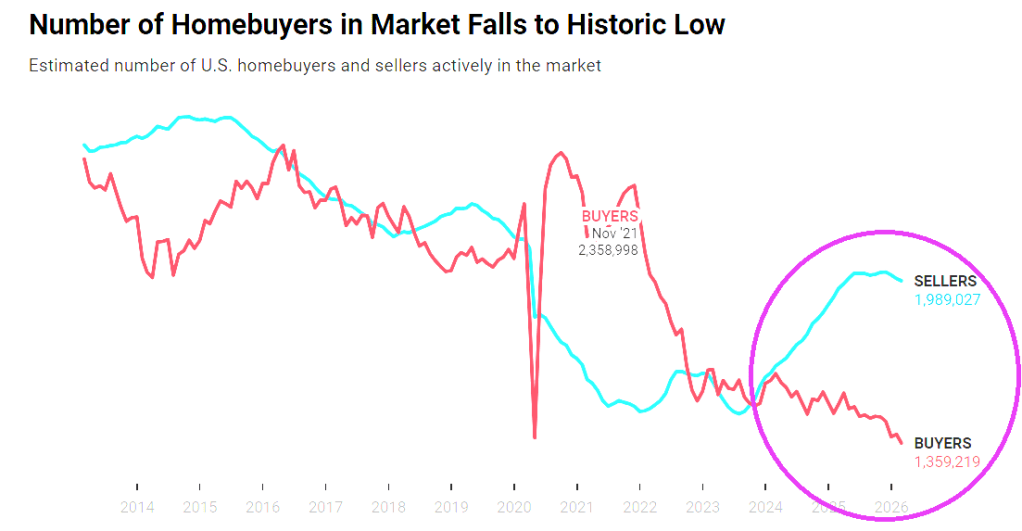

And the number of homebuyers has fallen to historic lows.

A good reason there are so few buyers is that home prices has soared after the Federal government’s spending spree after Covid.

Prayers for the soul of Noelia Castillo Ramos, murdered by the Spanish government. For being gangrape TWICE by immigrants then attempted suicide.

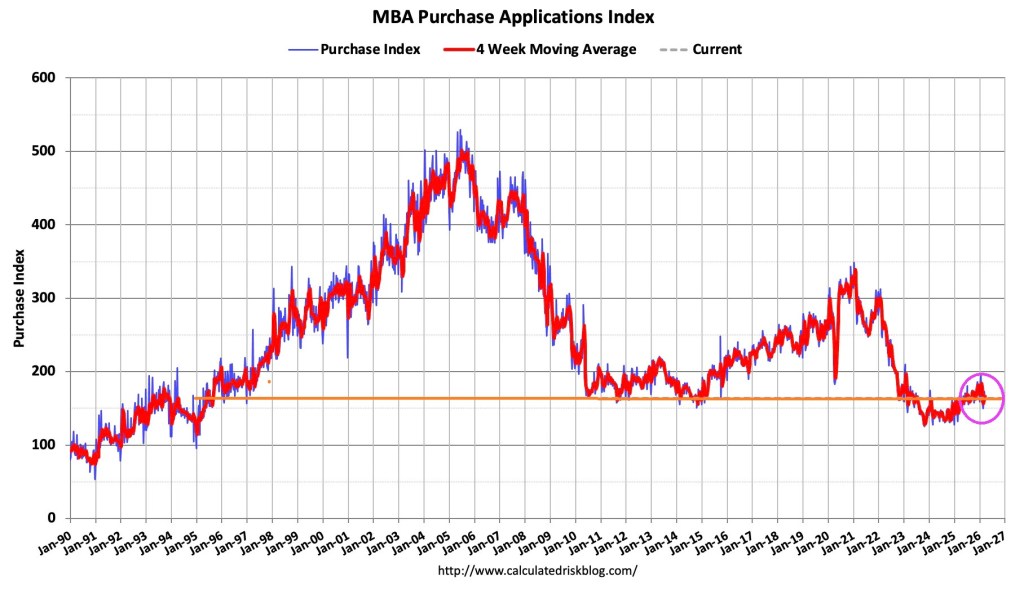

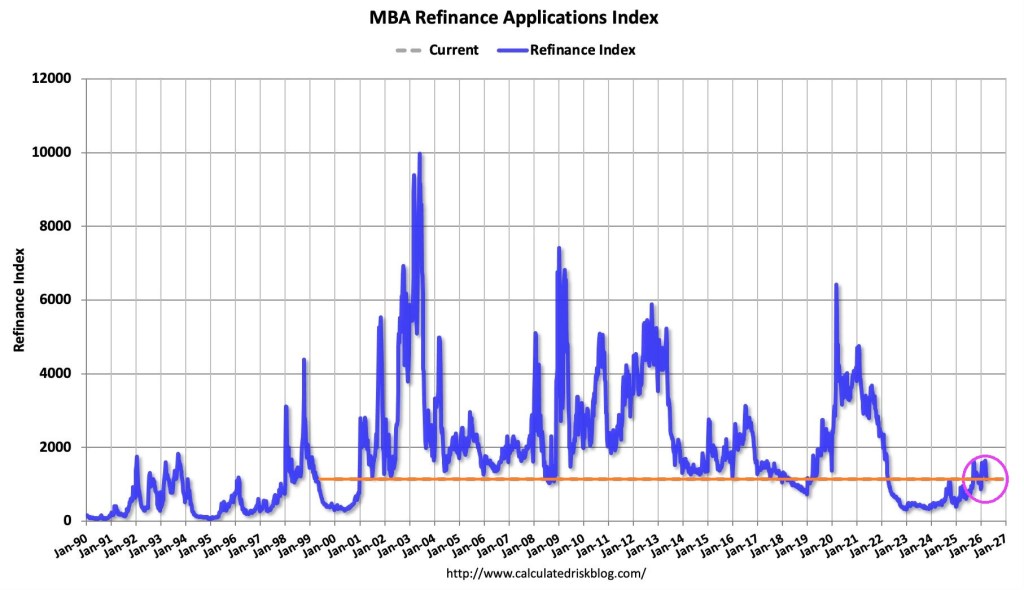

Mortgage applications decreased 10.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 20, 2026.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 10 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 5 percent higher than the same week one year ago.

The Refinance Index decreased 15 percent from the previous week and was 52 percent higher than the same week one year ago.

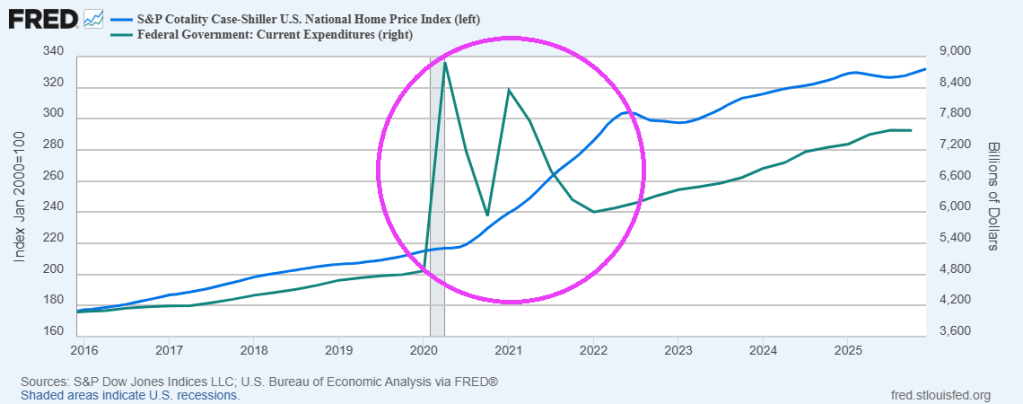

Nothing has been the same since Covid outbreak in 2020 and the resulting Federal government spemding spree.

So much for the “Trump has ruined the economy” mantra of politicians and celebrities.

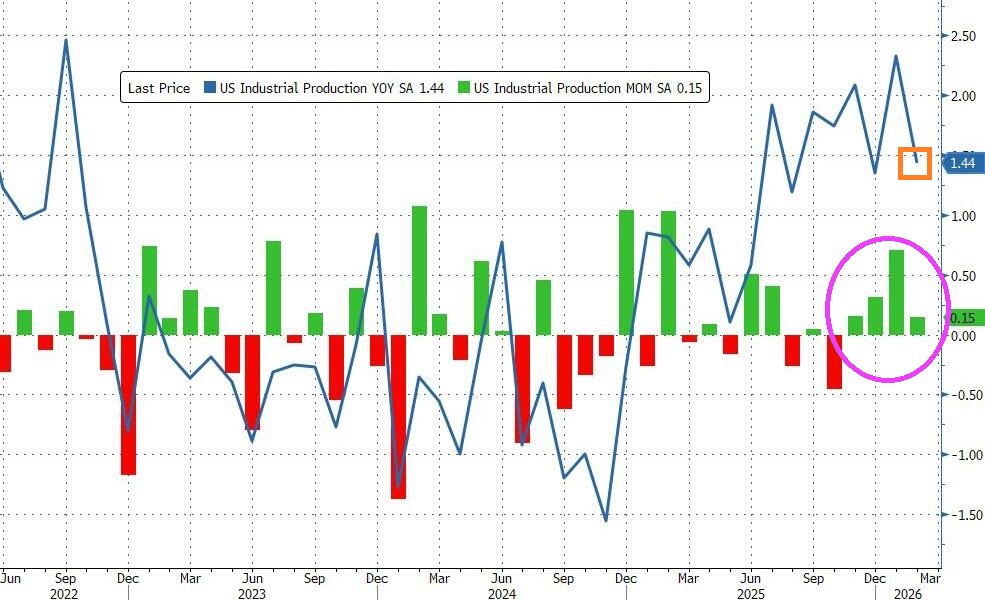

After a strong gain in January, US Industrial Production continued to expand in February, rising 0.2% MoM (better than expected +0.1%) – the fourth straight month of gains with Production up 1.44% YoY.

Source: Bloomberg

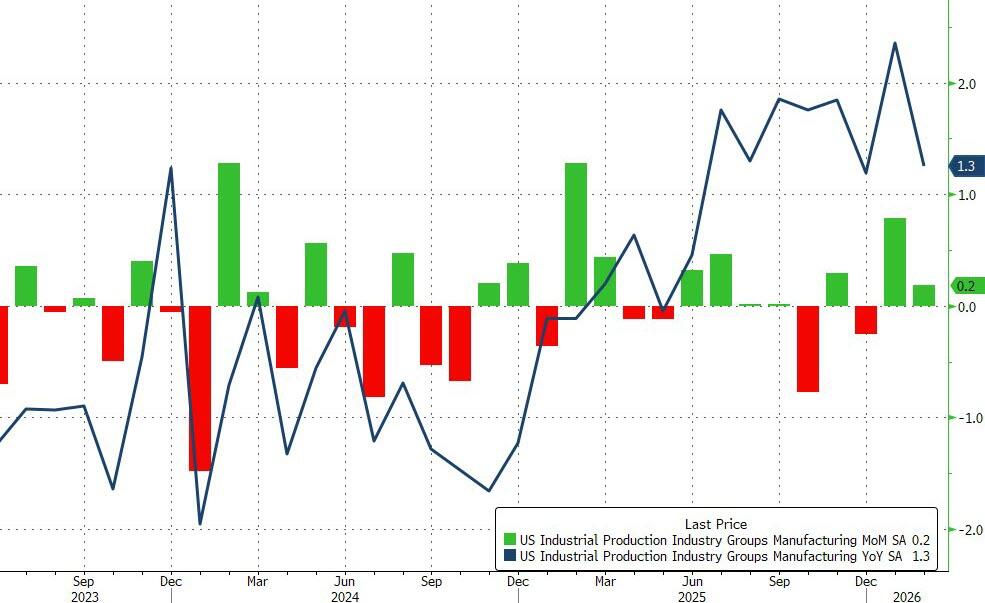

Manufacturing output also beat expectations, rising 0.2% MoM in February.

Durable manufacturing output edged up 0.1 percent, with mixed results across categories; the index for motor vehicles and parts posted the largest gain, and the index for machinery posted the largest loss.

Nondurable manufacturing output rose 0.2 percent, with gains in the production of chemicals, of plastic and rubber products, and of paper products outweighing declines in the output of petroleum and coal products and of food, beverage, and tobacco products. The output of other manufacturing (publishing and logging) rose 1.3 percent.

Mining output increased 0.8 percent in February, following a 0.9 percent increase in January. The output of utilities fell 0.6 percent in February, reflecting no change in the index for electric utilities and a 4.7 percent drop in the index for natural gas utilities.

Source: Bloomberg

Capacity Utilization printed 76.3 (better than expected)…

…maintaining the positive trend since Trump’s second term began.

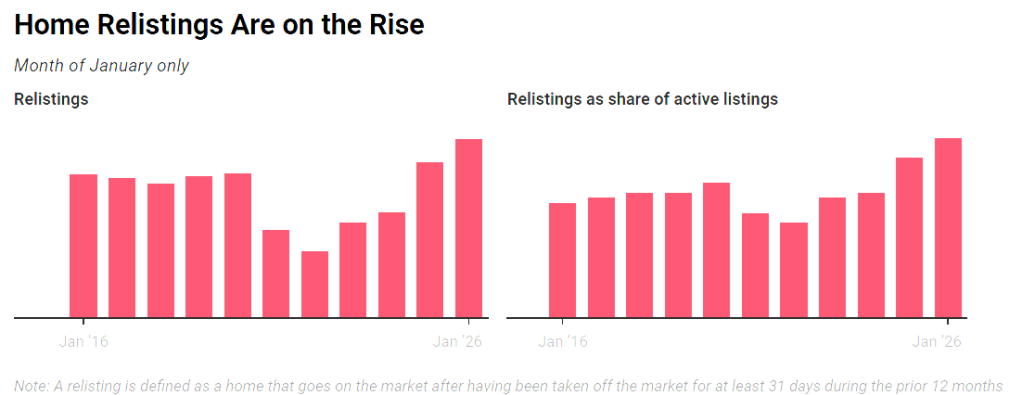

Delistings soared in 2025 after sellers began to outnumber buyers, and decided to take their homes off the market to take another bite at the apple this spring. Overall delistings hit a record high of 112,788 in December, while relistings this year represented 3.6% of all homes on the market.

Supply gains have been concentrated in the South and West, particularly among homes priced under $500,000. While the Northeast and Midwest have seen some growth, they are still lagging behind the other regions.

As of February, active listings climbed by 7.9 percent year over year, reaching 914,860 homes across the nation for sale. A little more than 7 percent of those listings resulted in contract cancellations—down slightly from the same time in 2025.

An analysis of the country’s 50 largest markets showed sharp increases in inventory in Seattle, with a 38.5 percent hike, as well as Louisville, Kentucky, 27.3 percent higher, and San Jose, with nearly 25 percent more homes on the market.

On the other side, Hartford, Connecticut, experienced the deepest drop in inventory at over 82 percent, as well as Providence, Rhode Island, at 61.1 percent.

Overall, homes spent a median of 70 days on the market in February, four days longer than a year earlier.

{kind=link}

{kind=link}

You must be logged in to post a comment.