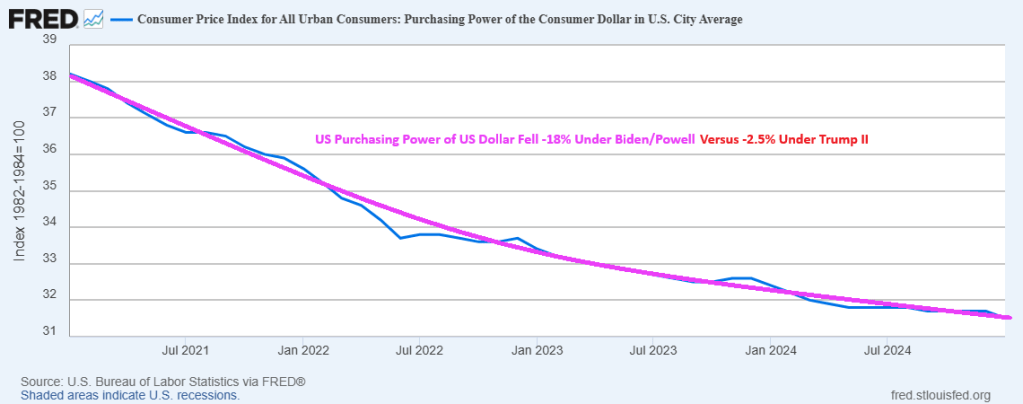

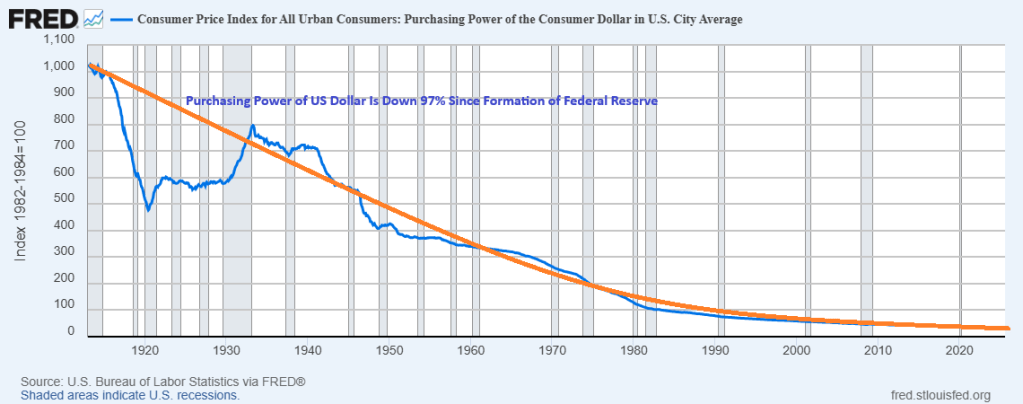

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913. It is the House of the Dying Dollar.

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913.

Of course, Trump II is only 9 months old and Biden had 4 long years to destroy the dollar.

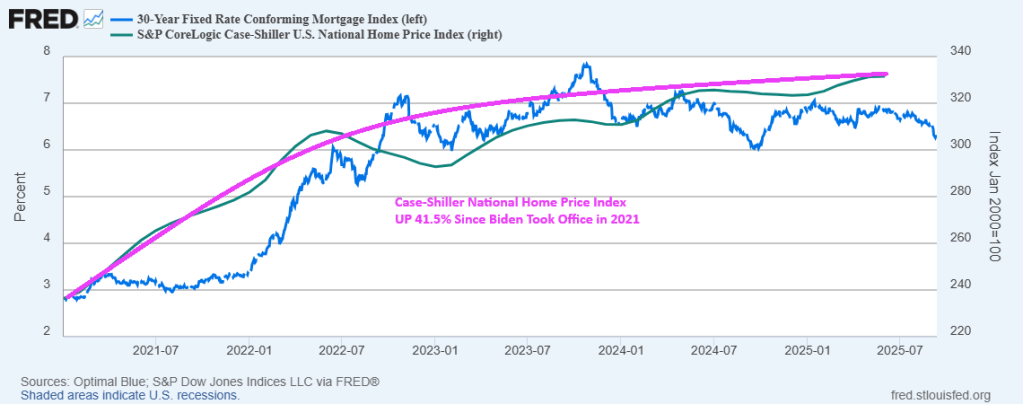

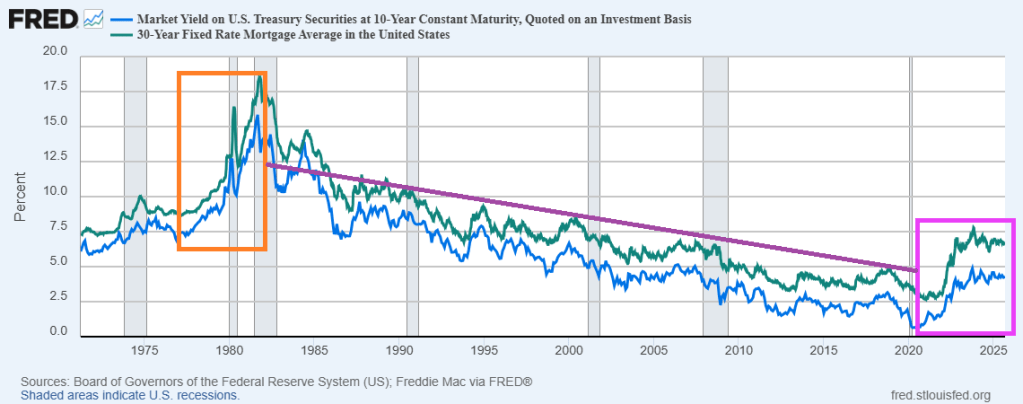

Mortgage rates remain elevated since the Biden Administration took control in 2021. Although under Trump, the rise in the 30-year mortgage rate has slowed. But the 30-year mortgage rate is up 126% since the beginning of 2021 and the “Joe The Boss” Biden administration.

Mortgage originations at large banks declined a whopping 74% under “Joe The Boss” Biden.

Between mortgage rates rising by 126% and house prices rising by 41.5% under “Joe The Boss” Biden.

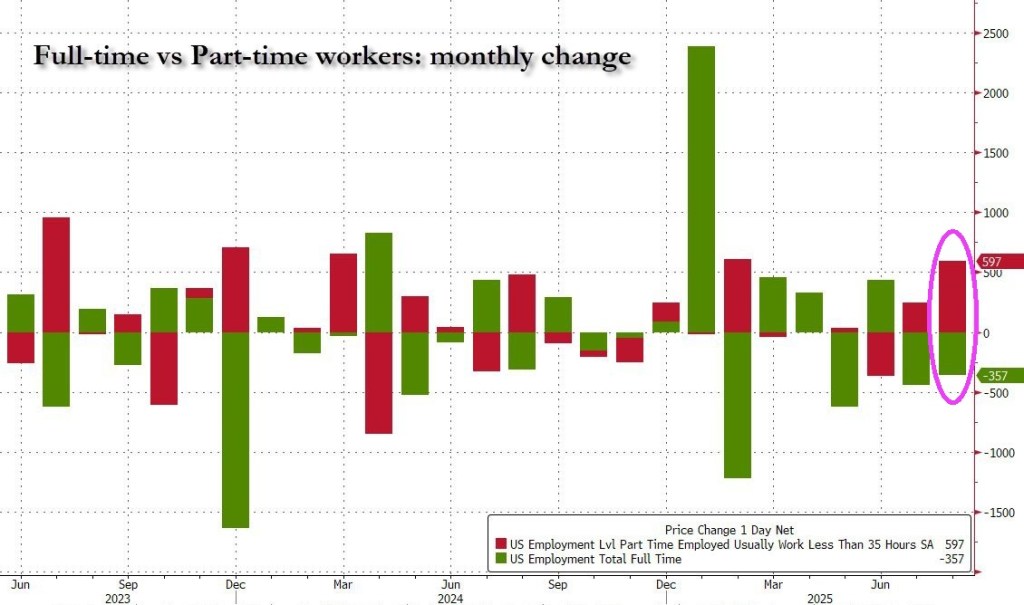

U-3 unemployment rate rose to 4.3%. U-6 unemployment and part-time rose to 8.1%.

Total private jobs added was 38k while manufacturing jobs added was down -12k.

Government jobs dropped -16k.

It gets worse! All of the jobs added were PART-TIME!

It gets even worse: native-born workers plunged by 561K, the biggest one month drop since August 2024. Foreign-born workers increased by 50K, the first increase since March.

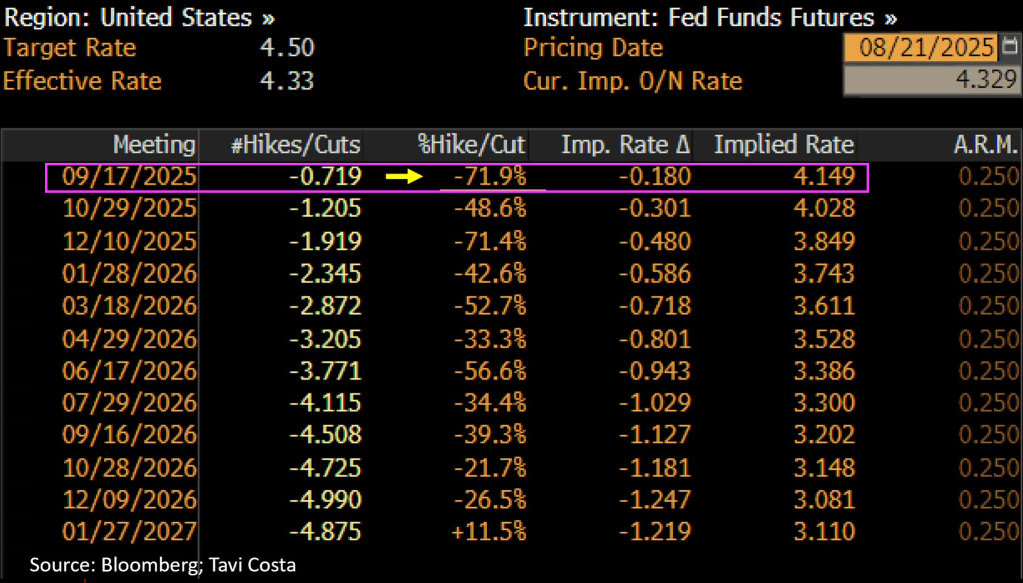

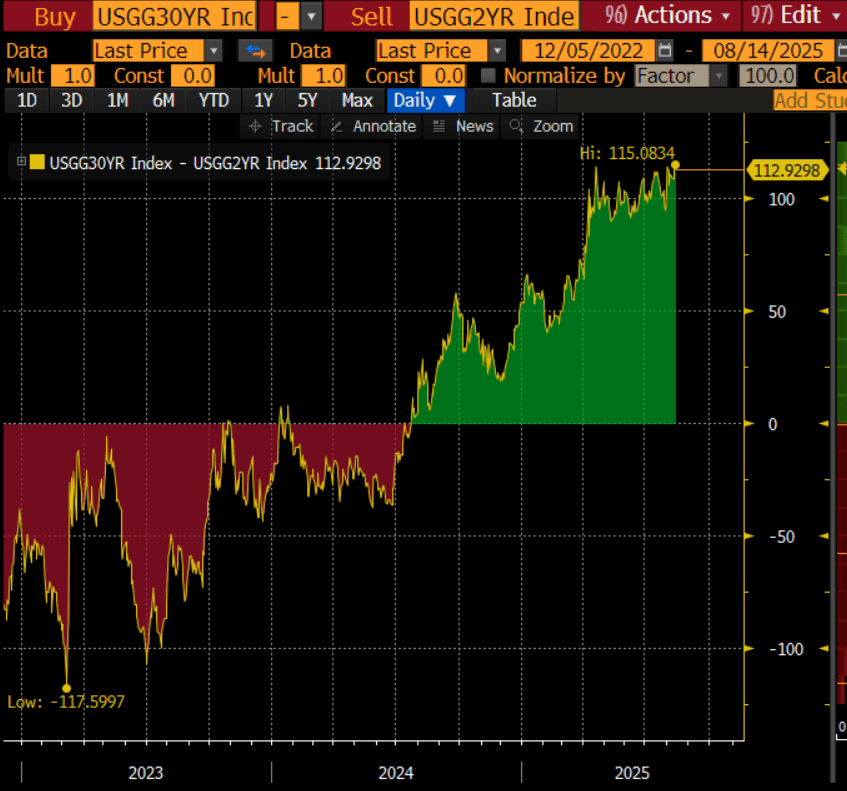

Let’s see if The Fed drops the hammer on rates by 50 basis points.

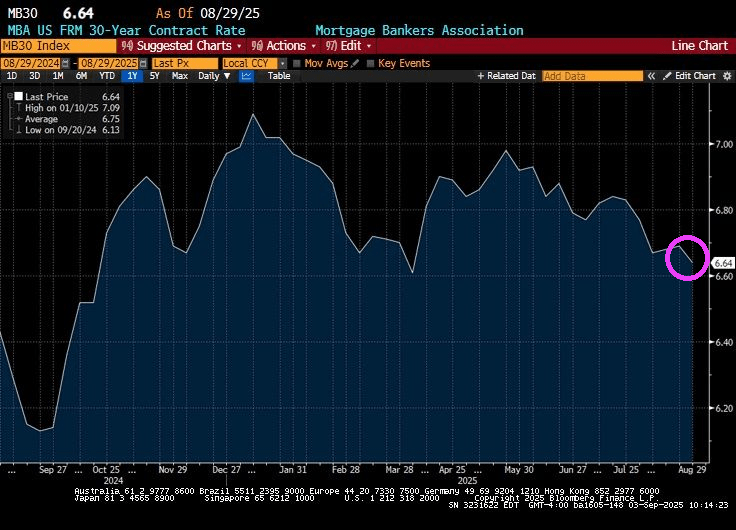

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

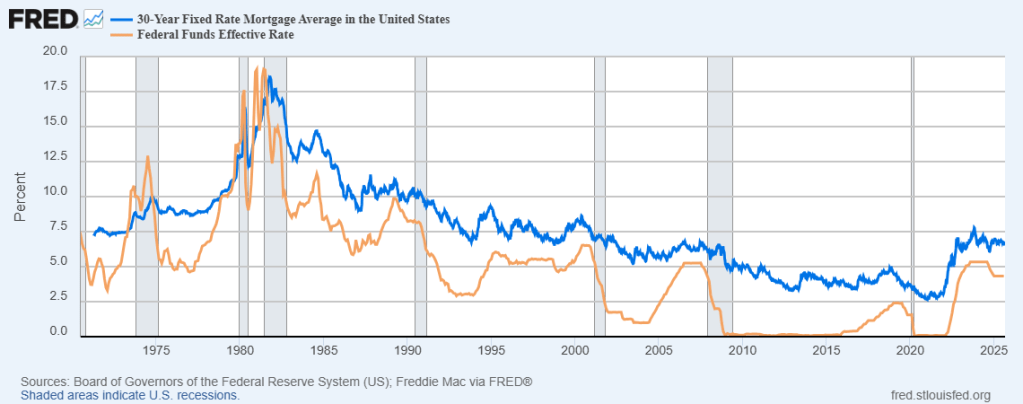

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

Month-over-month sales increased in the Northeast, South, and West, and fell in the Midwest. Year-over-year, sales rose in the South, Northeast, and Midwest, and fell in the West.

• 2.0% increase in existing-home sales – seasonally adjusted annual rate of 4.01 million in July.

• Year-over-year: 0.8% increase in existing-home sales

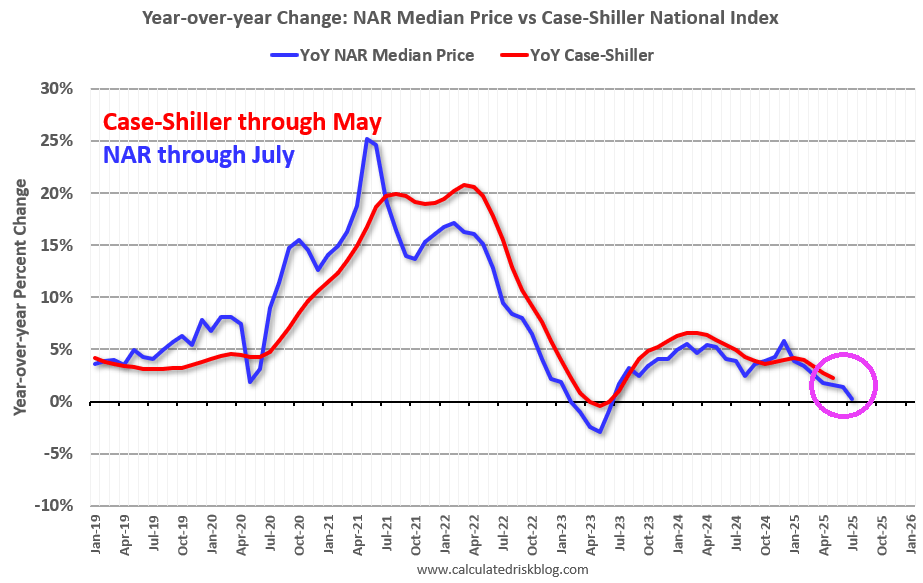

Median existing-home price for all housing types, up 0.2% from one year ago ($421,400) – the 25th consecutive month of year-over-year price increases.

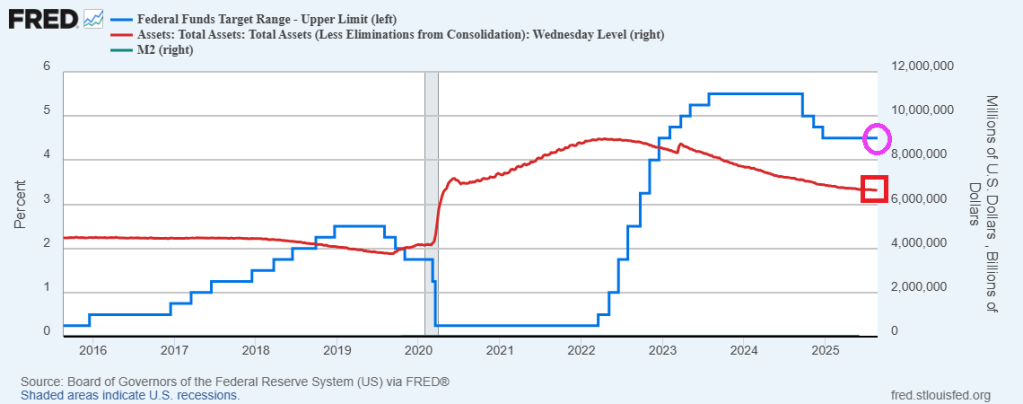

It will be hard to make housing more affordable as long as The Fed keeps printing money.

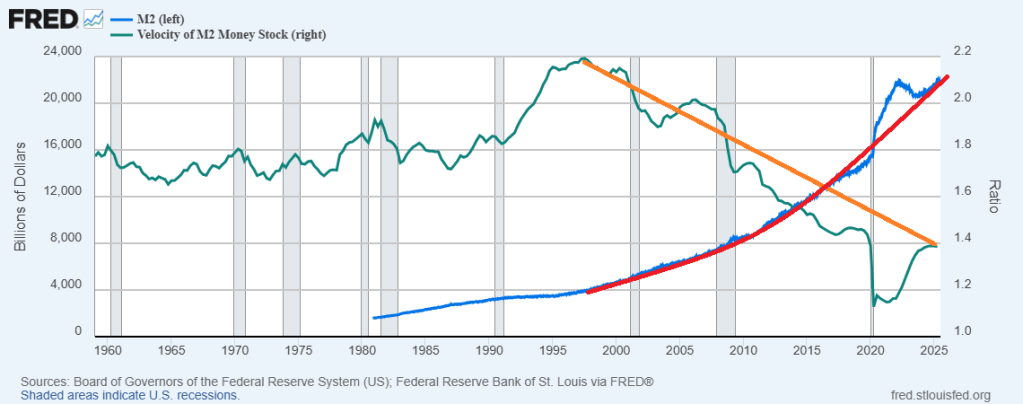

Powell et al cutting rates 25 basis points won’t really matter as long as they continue to print money. Unfortunately, M2 VELOCITY peaked under the Clinton Administration and has declined since despite frantic money printing.

What happended in 1995? Clinton’s National Homeownership Strategy that mandated HUD partners (GNMA, FHA, Fannie Mae, Freddie Mac, banks, etc.) to lower credit standards to encourage homeownership.

We need FHFA Director Bill Pulte to avoid doing what Democrats love (everything free or cheap).

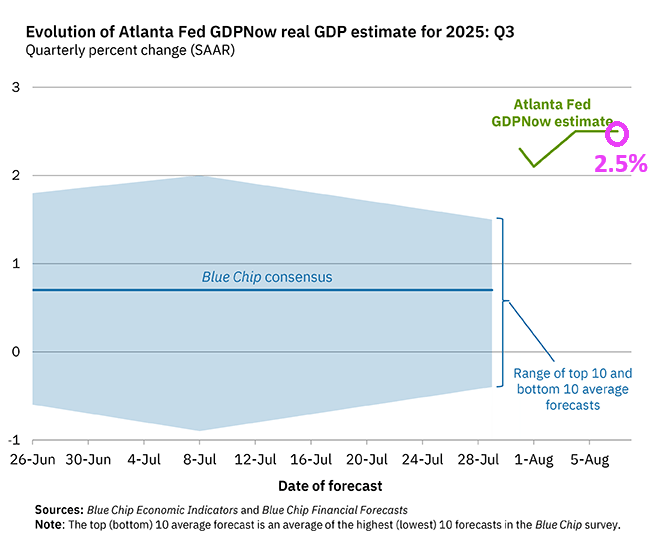

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 2.5 percent on August 7, unchanged from August 5 after rounding. After this morning’s wholesale trade report from the US Census Bureau, the nowcast of the contribution of inventory investment to third-quarter real GDP growth increased from 0.76 percentage points to 0.82 percentage points.

Federal spending, elevated with the outbreak of Covid in 2020 remains higher than pre-Covid levels as does M2 Money printing.

The latest inflation report continues to show no negative impact from tariffs. Core goods prices were up 0.2% in July. They are up just 1.1% over the past 12 months and are actually up a lesser 0.8% since President Trump began phasing in tariffs.

Business applications are booming under Trump’s economy.

While consumer prices are calm (2.7% YoY).

Shelter inflation is higher than the average price increase (3.7% YoY).

They can’t accuse Fed Chair Jerome Powell of trying too hard to help Donald Trump. Mortgage rates moved lower last week, following declining Treasury yields as economic data releases signaled a weakening U.S. economy. As a result, the 30-year fixed rate decreased for the third straight week to 6.77 percent. As a result …

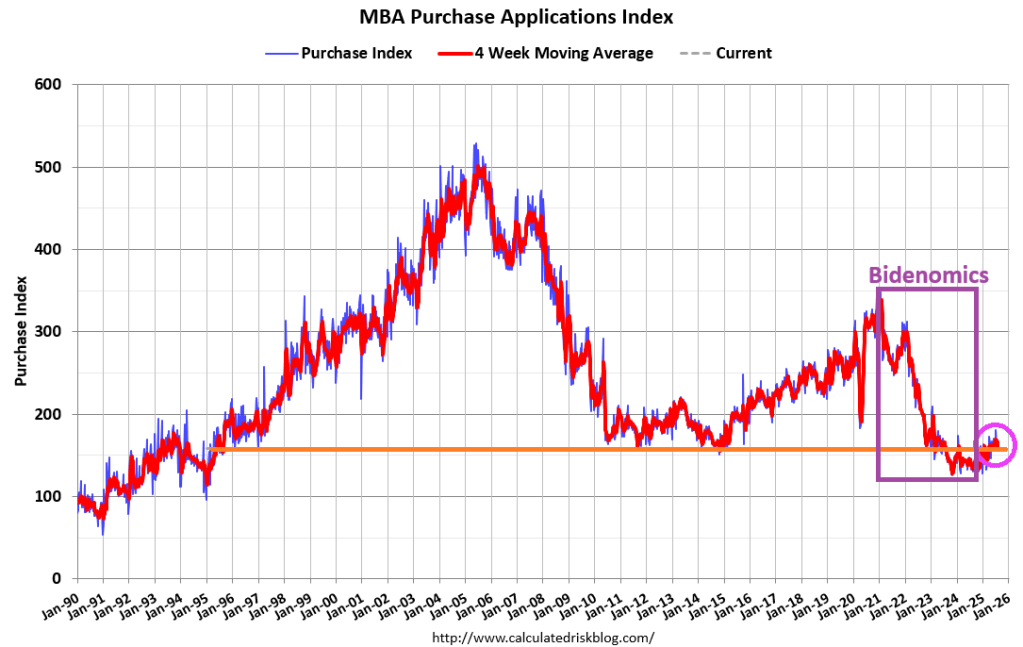

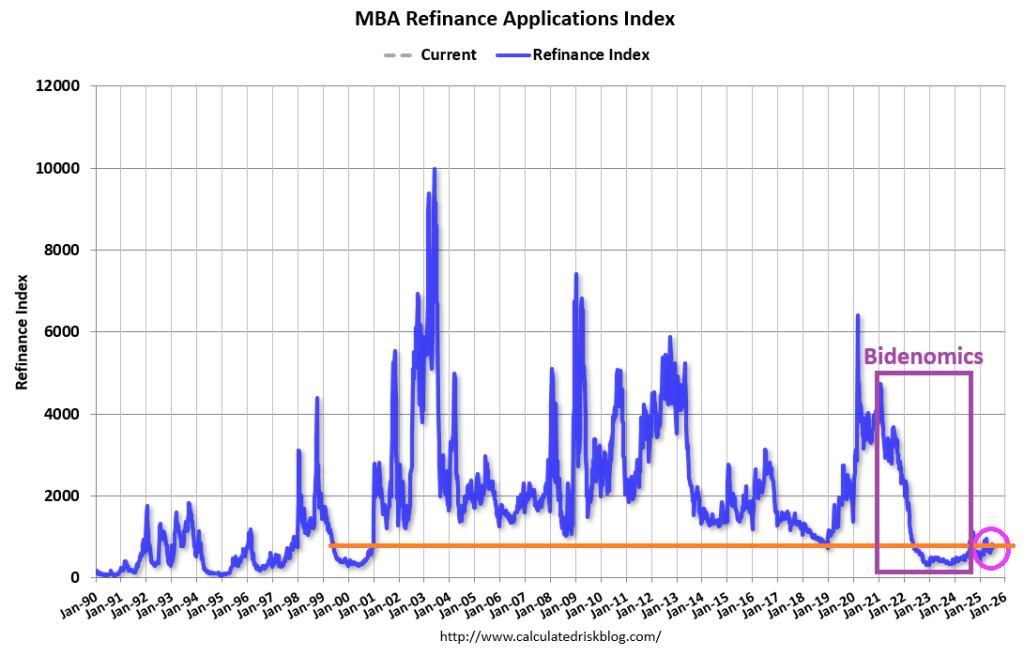

The Market Composite Index, a measure of mortgage loan application volume, increased 3.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 18 percent higher than the same week one year ago.

The Refinance Index increased 5 percent from the previous week and was 18 percent higher than the same week one year ago.

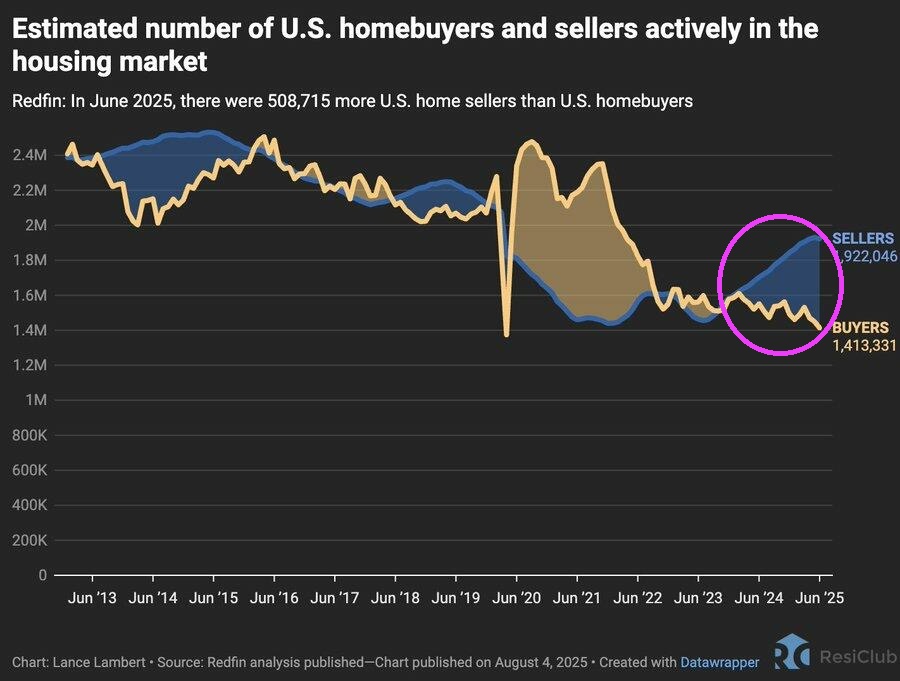

And the number of sellers in the housing market is greatly outweighing the number of buyers.

Mortgage and housing economists should breathe a sigh of relief that Bidenomics is over, but I doubt it they will.

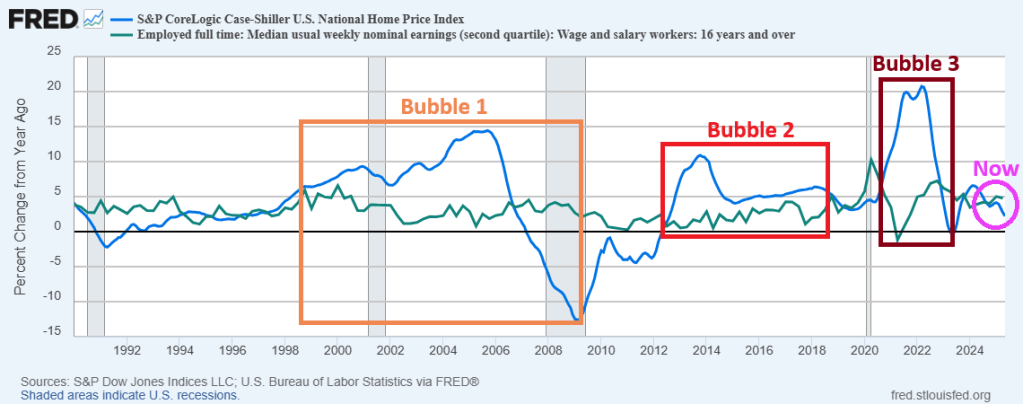

The US housing market is finally slowing down in terms of price growth. But this is after 3 Federal government-fueled house price bubbles.

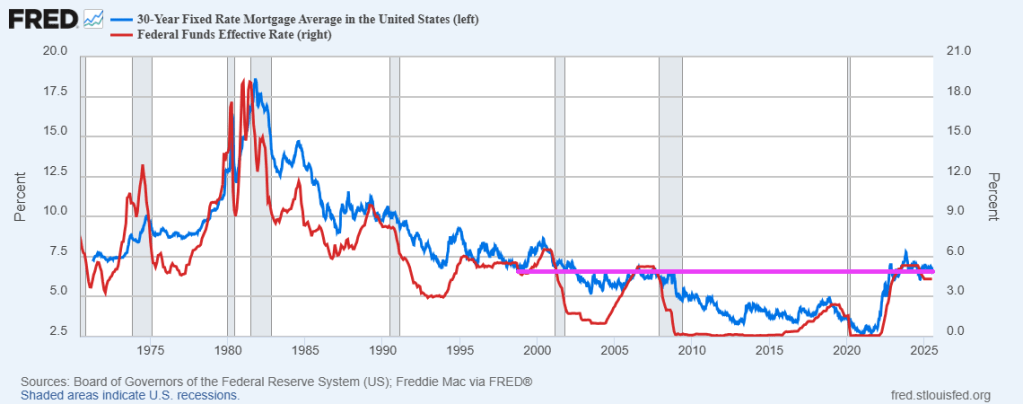

In addition to record-high housing prices, mortgage rates are higher than levels going back to 2006.

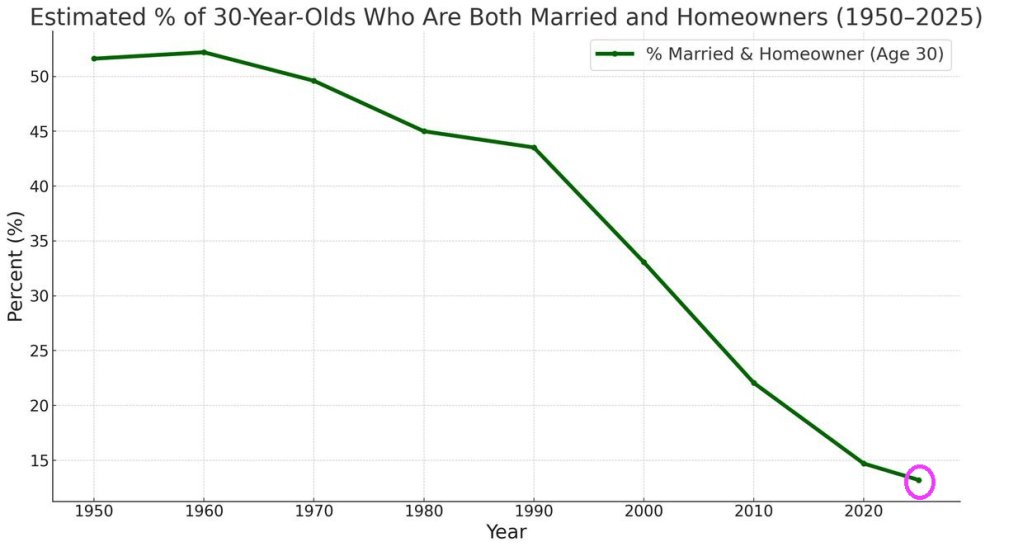

Throw in the “woke” movement, and we have a problem. The percentage of 30-year-olds who are both married and homeowners has plummeted to the lowest level since 1950.

Simply lowering interest rates won’t fix this problem. Much of the housing “crisis” is due to local and state level politicians and their restrictive housing policies. Like LA Mayor Karen “Venceremos Brigade” Bass allocating the burnt-down Pacific Palisades area on the Pacific Ocean to “affordable housing.”

You must be logged in to post a comment.