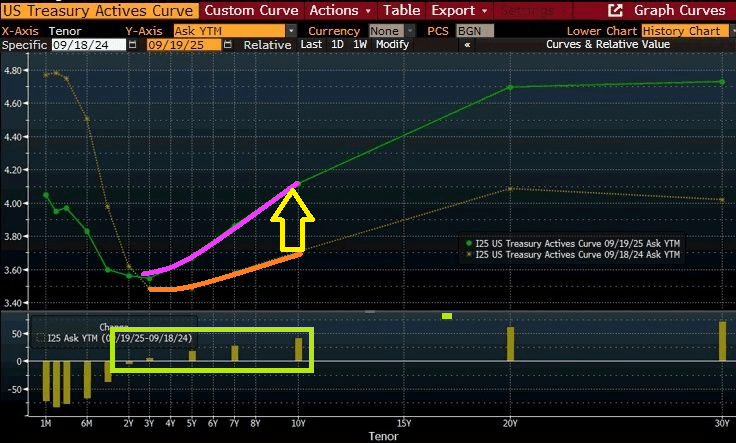

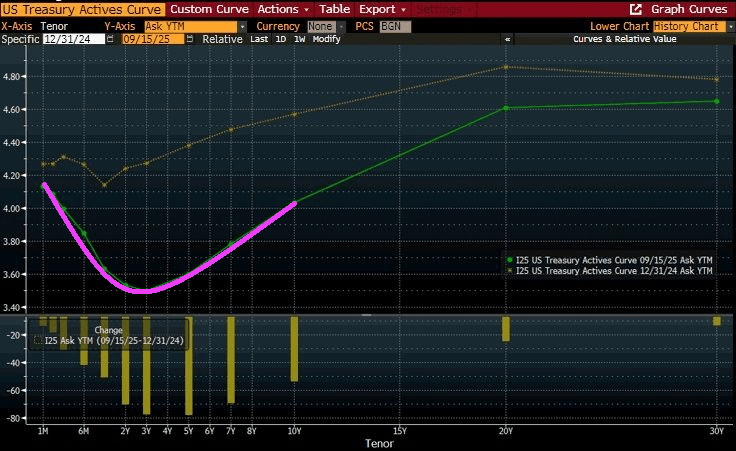

It’s Friday and the US Treasury yield curve is rising/steepening at the 10-year tenor.

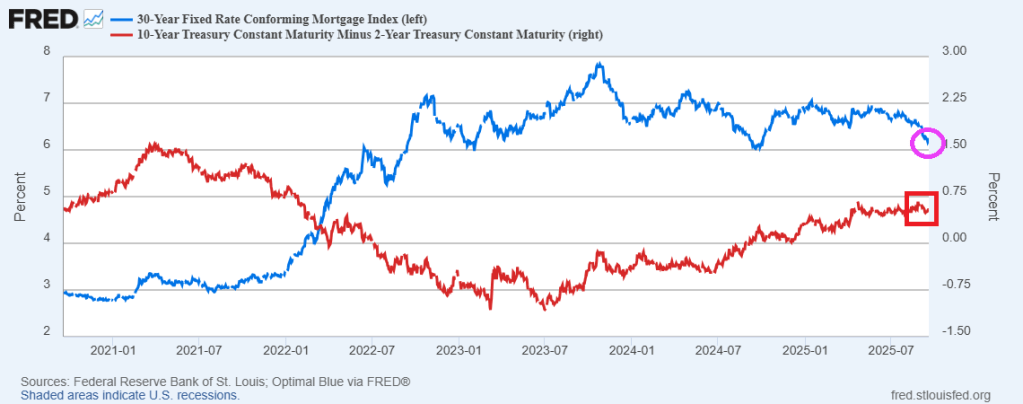

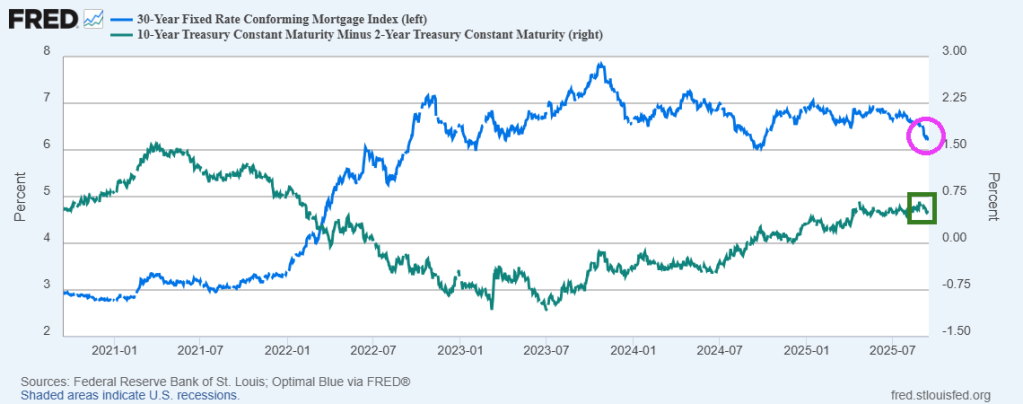

As of yesterday, the 30-year mortgage rate fell to 6.17%

Thanks in part to Funky Cold Jerome!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

It’s Friday and the US Treasury yield curve is rising/steepening at the 10-year tenor.

As of yesterday, the 30-year mortgage rate fell to 6.17%

Thanks in part to Funky Cold Jerome!

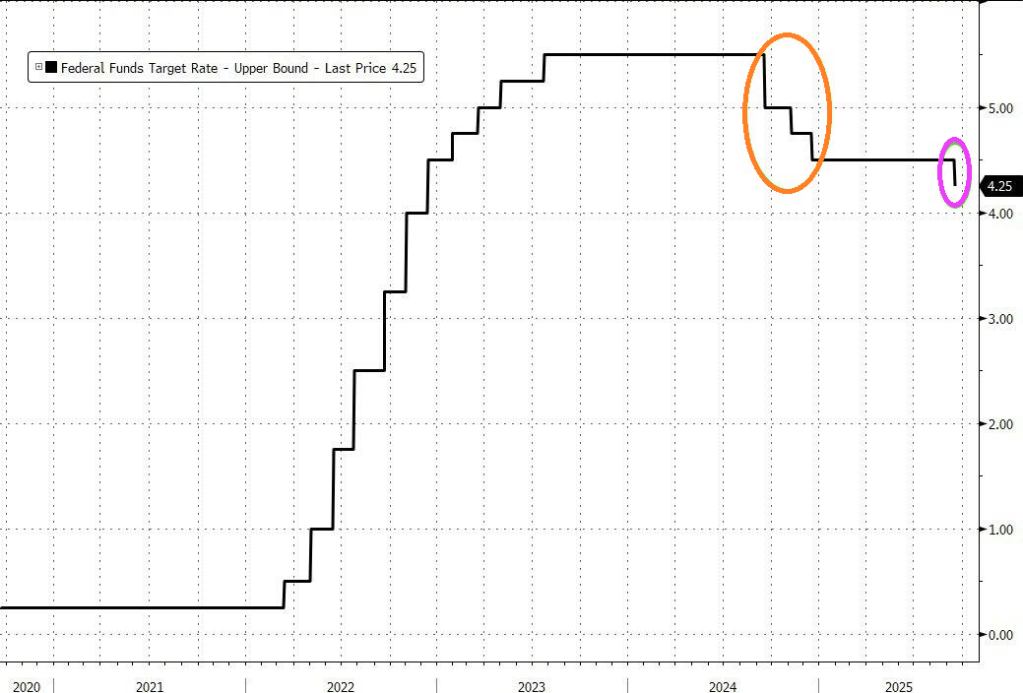

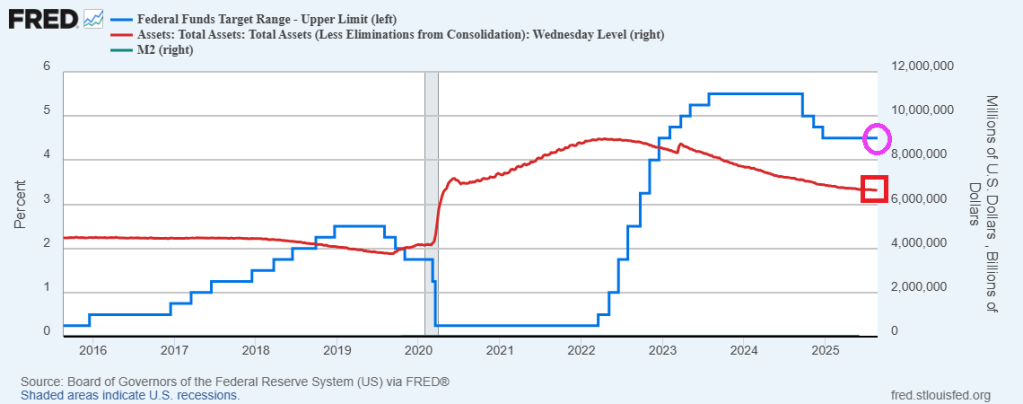

Well, The Fed cut their target rate by 25 basis points.

Following The Fed’s 25 bp cuts, the 10Y yield fell below 4% to 3.9879%.

The Fed Dots??

We shall see tomorrow if mortgage rates fall.

Of course, as soon as I posted this, US Treasury 10Y yields surged. This often happens with The Fed’s incompetent messaging.

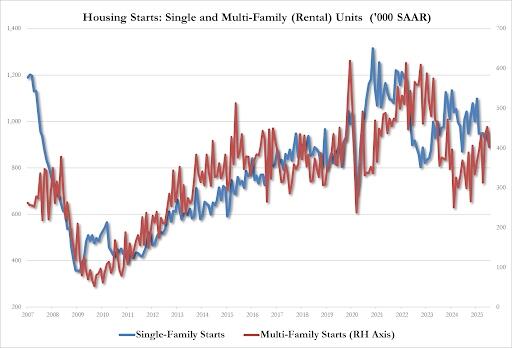

It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

Housing starts:

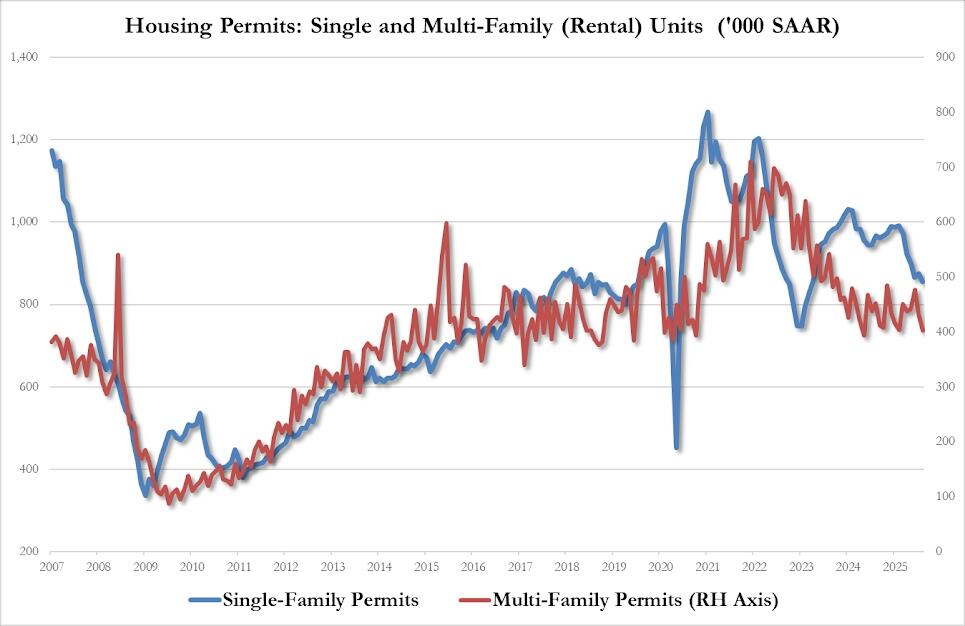

Housing permits?

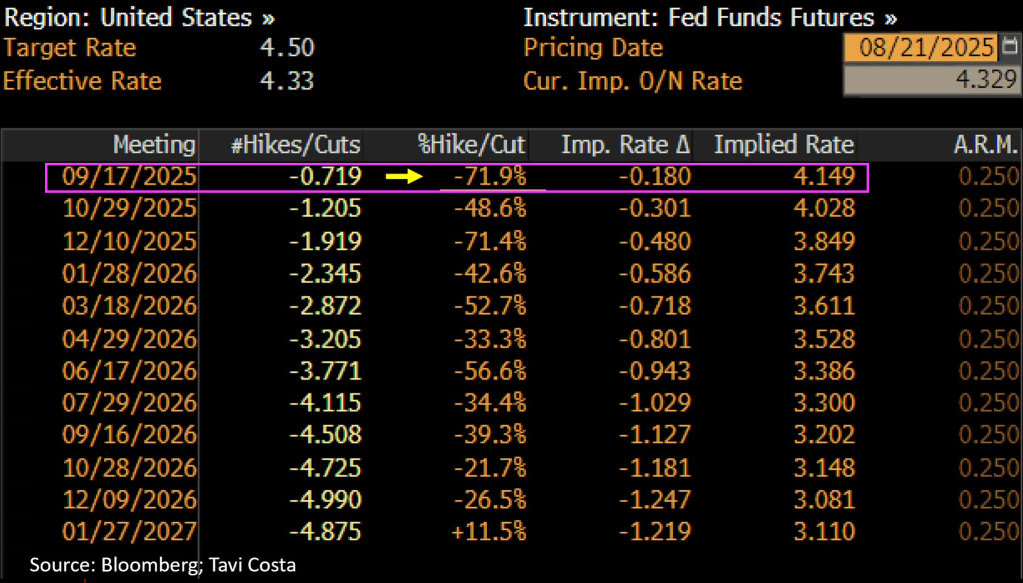

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

Participants in the mortgage market are hoping for relief in the mortgage market when The Fed lowers rates tomorrow.

But the reality is the the bond market is expecting declining short-term rates, but not much change at the 10-year tenor.

Mortgage rates have fallen since October 23, 2023 as the yield curve has gradually steepened.

So don’t be surprised if The Fed cuts rates tomorrow and there is little or no reaction in mortgage rates.

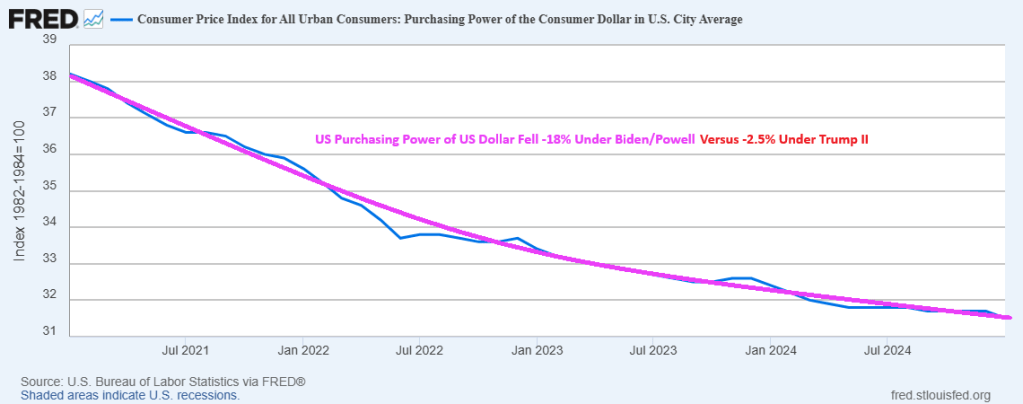

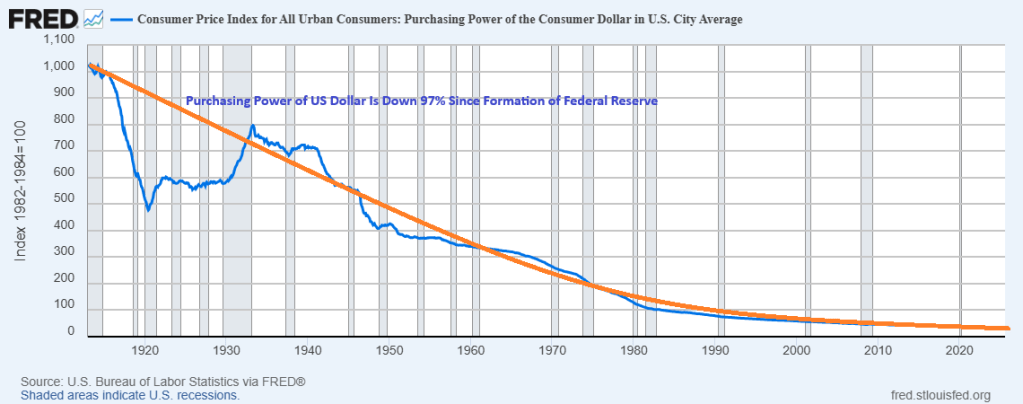

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913. It is the House of the Dying Dollar.

Under The Federal Reserve, the purchasing power of the US Dollar has declined -97% since the establishment of The Federal Reserve in 1913.

Of course, Trump II is only 9 months old and Biden had 4 long years to destroy the dollar.

US housing is simply unaffordable!

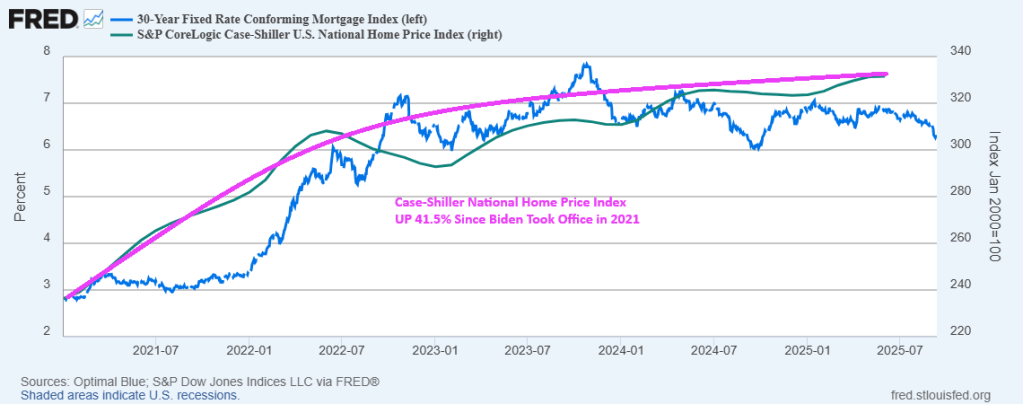

Mortgage rates remain elevated since the Biden Administration took control in 2021. Although under Trump, the rise in the 30-year mortgage rate has slowed. But the 30-year mortgage rate is up 126% since the beginning of 2021 and the “Joe The Boss” Biden administration.

Mortgage originations at large banks declined a whopping 74% under “Joe The Boss” Biden.

Between mortgage rates rising by 126% and house prices rising by 41.5% under “Joe The Boss” Biden.

US housing is simply unaffordable.

Guiseppe “Joe The Boss” Biden.

Actually, this is a photo of Guiseppe “Joe The Boss” Masseria. A New York crime boss assassinated by Lucky Luciano in 1931.

Not exactly the Guns Of August. More like a wet cap gun firing.

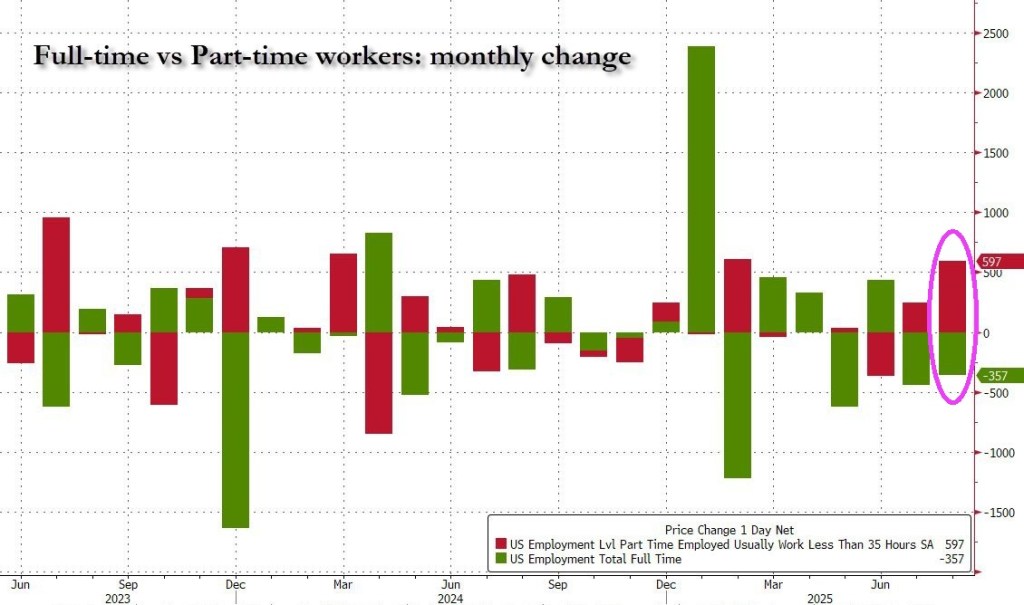

The jobs report for August showed only 22k jobs added.

U-3 unemployment rate rose to 4.3%. U-6 unemployment and part-time rose to 8.1%.

Total private jobs added was 38k while manufacturing jobs added was down -12k.

Government jobs dropped -16k.

It gets worse! All of the jobs added were PART-TIME!

It gets even worse: native-born workers plunged by 561K, the biggest one month drop since August 2024. Foreign-born workers increased by 50K, the first increase since March.

Let’s see if The Fed drops the hammer on rates by 50 basis points.

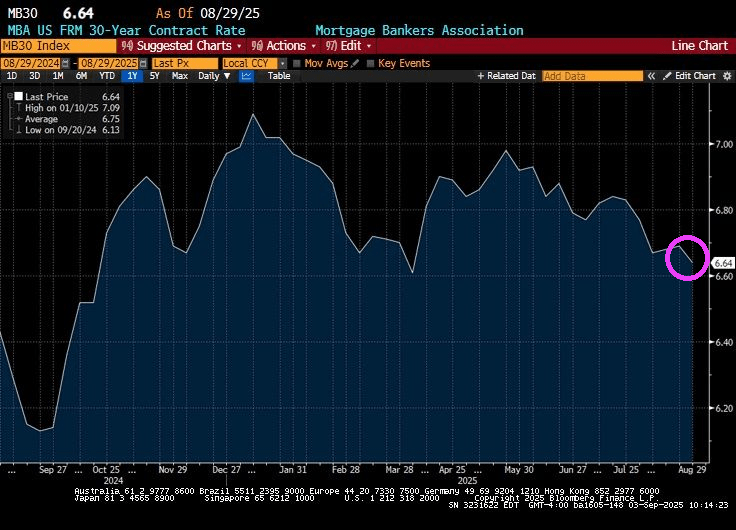

The good news? The US 30-year mortgage rate fell slightly to 6.64%.

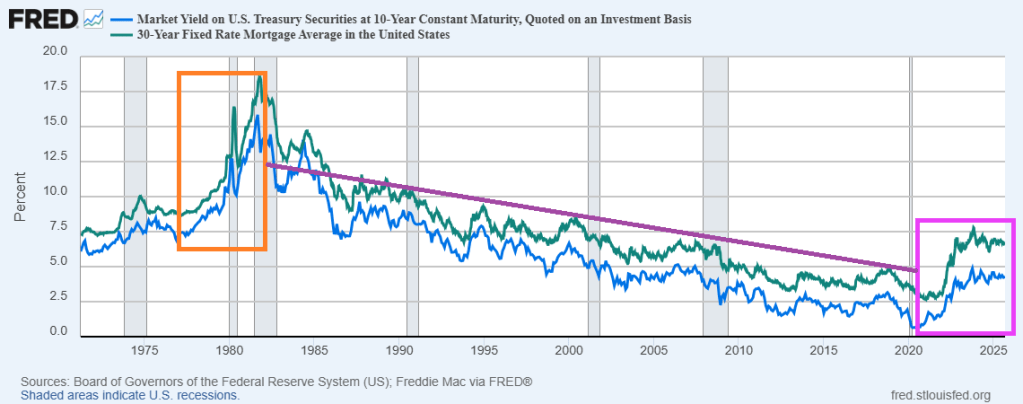

The bad news? It seems to be a milder repeat of the Ford/Carter years of the late 1970s/early 1980s. Rising 10-year Treasury yields and 30-year mortgage rates during the Ford/Carter years … and early Reagan years. The difference? The Federal Reserve is fundamentally different today than previously. With Bernanke/Yellen, The Fed became more “activist” (like Obama/Biden-appoointed District Judges). Powell is returning to the Yellen model of Fed activism … not doing much.

Now the market awaits a rate cut from The Fed at the next FOMC meeting. But 30-year mortgage rates are most closely related to the 10-year Treasury yield than the short-term Fed Funds rate. Theoretically, The Fed could cut their target rate by 25 basis points and mortgage rates could be uneffected. Or even rise.

Here is a video of Fed Chair Jerome Powell trying to lower mortgage rates.

What about the mortgage rates, Fawlty?

People get ready! Powell and the Fed might actually lower their target rate at The Fed’s Open Market Committee meeting on September 17.

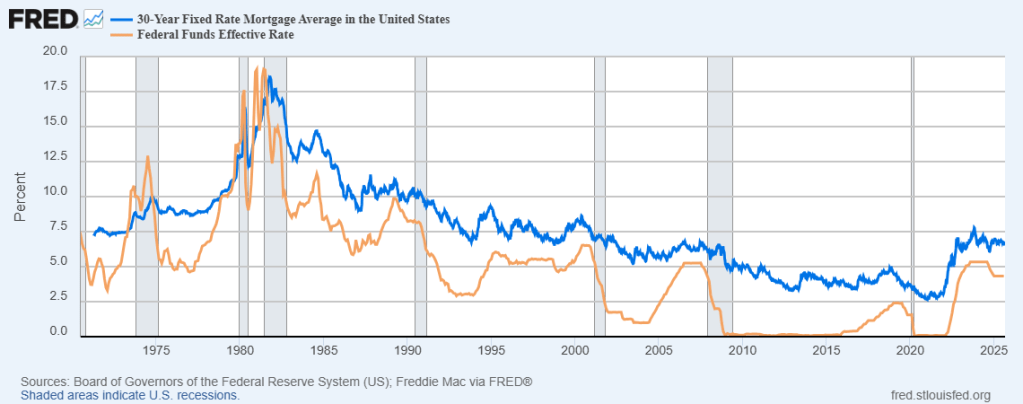

The Fed hasn’t touched rates under Trump, but were hyperactive under Biden.

Let the good times roll? I wonder if Jay Powell and the other Fed honchos are taking Jackalope Rides in Jackson Hole, WYO?

The Federal Reserve is Dazed and Confused. Their money printing is making housing progressively more expensive and unaffordable.

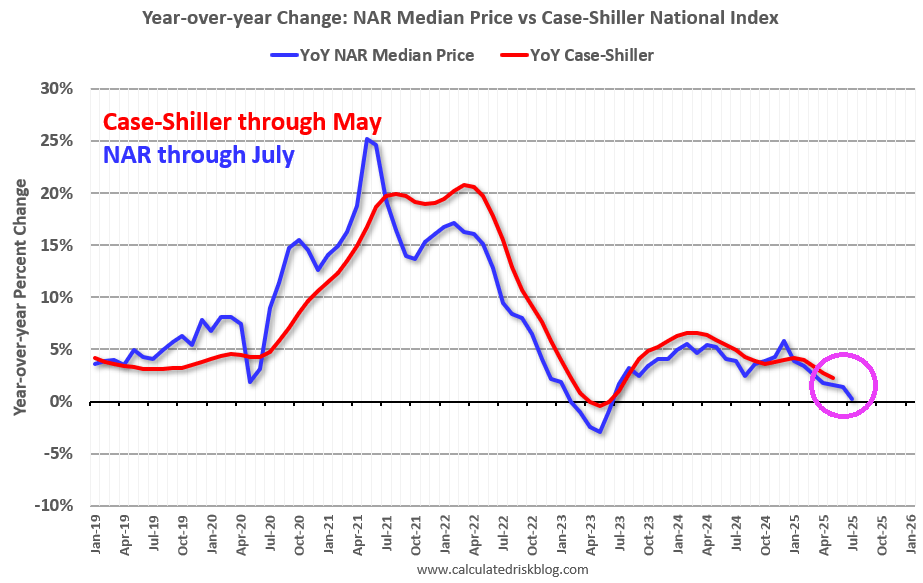

Existing-home sales increased by a measley 2.0% in July, according to the National Association of REALTORS® Existing-Home Sales Report.

Month-over-month sales increased in the Northeast, South, and West, and fell in the Midwest. Year-over-year, sales rose in the South, Northeast, and Midwest, and fell in the West.

• 2.0% increase in existing-home sales – seasonally adjusted annual rate of 4.01 million in July.

• Year-over-year: 0.8% increase in existing-home sales

Median existing-home price for all housing types, up 0.2% from one year ago ($421,400) – the 25th consecutive month of year-over-year price increases.

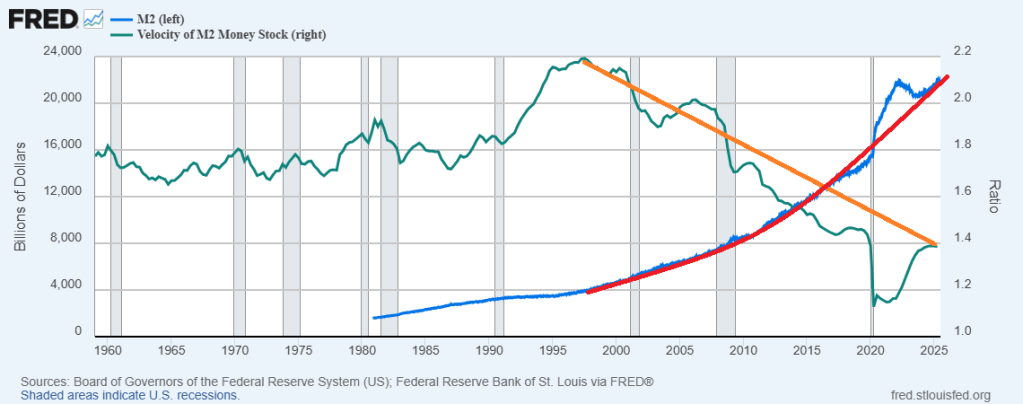

It will be hard to make housing more affordable as long as The Fed keeps printing money.

Powell et al cutting rates 25 basis points won’t really matter as long as they continue to print money. Unfortunately, M2 VELOCITY peaked under the Clinton Administration and has declined since despite frantic money printing.

What happended in 1995? Clinton’s National Homeownership Strategy that mandated HUD partners (GNMA, FHA, Fannie Mae, Freddie Mac, banks, etc.) to lower credit standards to encourage homeownership.

We need FHFA Director Bill Pulte to avoid doing what Democrats love (everything free or cheap).

{kind=link}

{kind=link}

You must be logged in to post a comment.