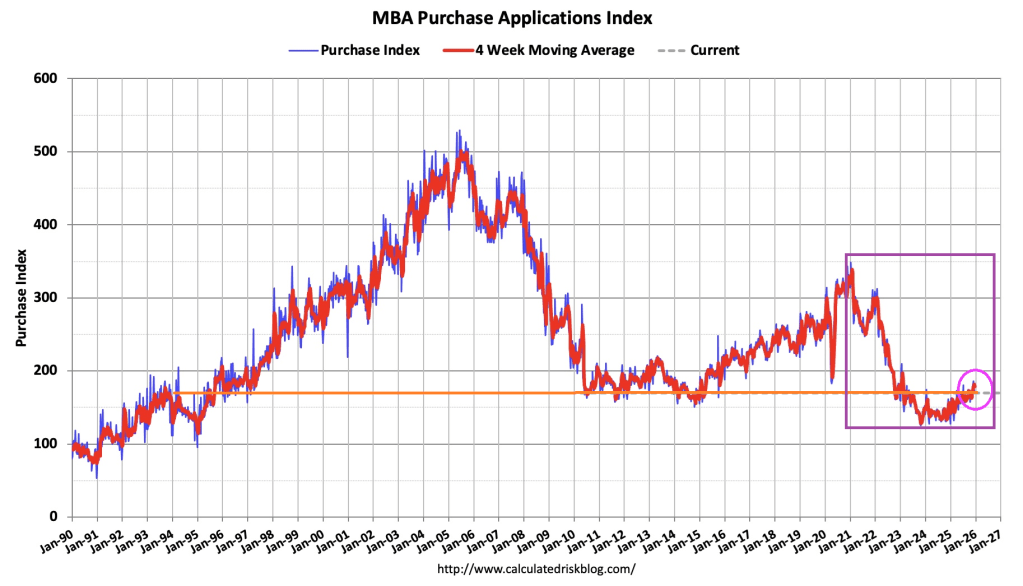

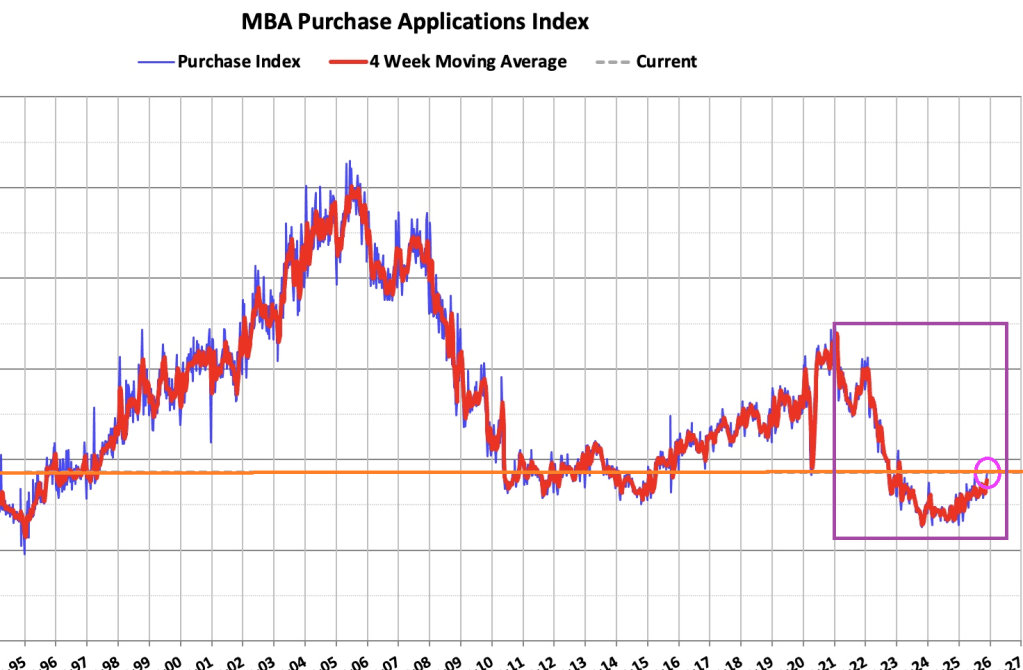

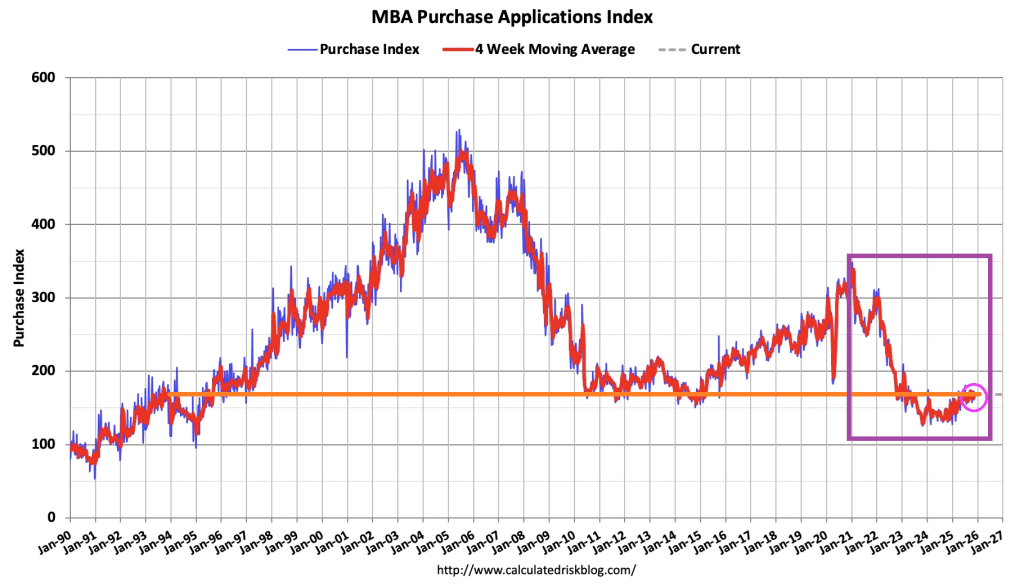

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 16 percent higher than the same week one year ago.

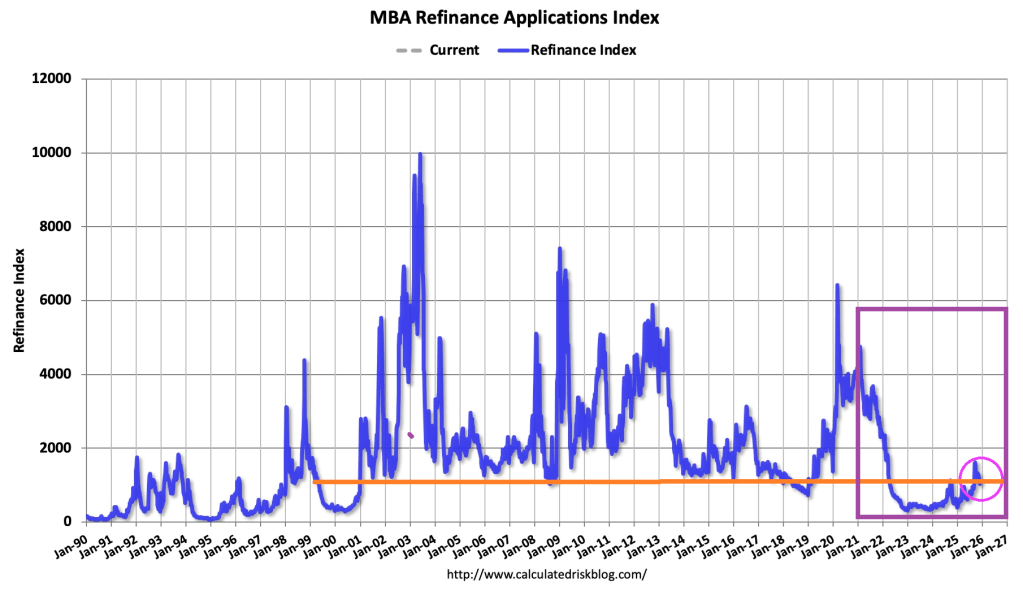

The Refinance Index decreased 6 percent from the previous week and was 110 percent higher than the same week one year ago.

Overall mortgage application volume fell last week, despite the slight decline in mortgage rates. I expect the trends of a softening job market, sticky inflation, elevated home inventories, and steady mortgage rates will persist into the new year.

Politicians love to scream about housing being simply unaffordable. Like mayor-elected Mandami in New York City. But the reality is that housing prices vary by city and there are more affordable cities than New York City to choose from. Federal policies should not be focused on letting people staying a particular city.

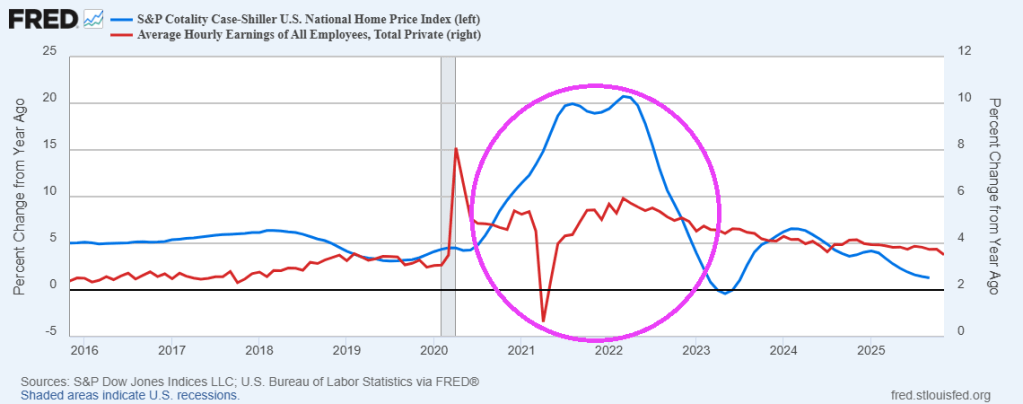

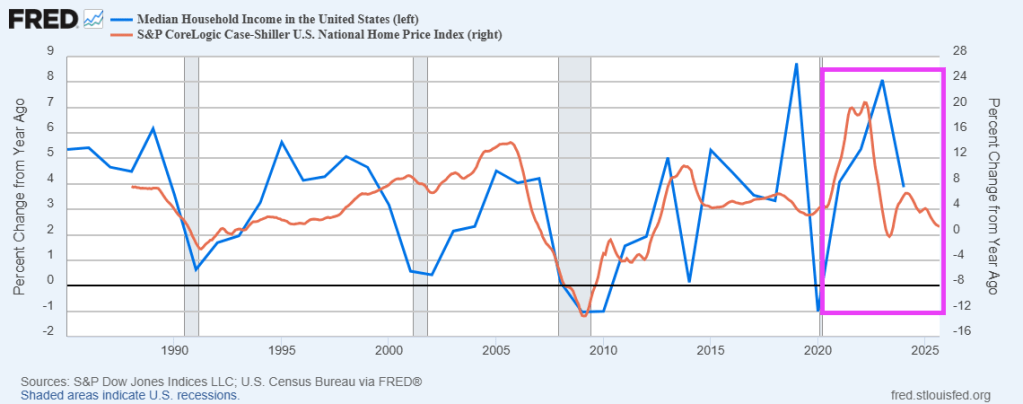

When we look at housing prices compared to average hourly earnings, we see housing prices rising with average hourly earnings … as expected.

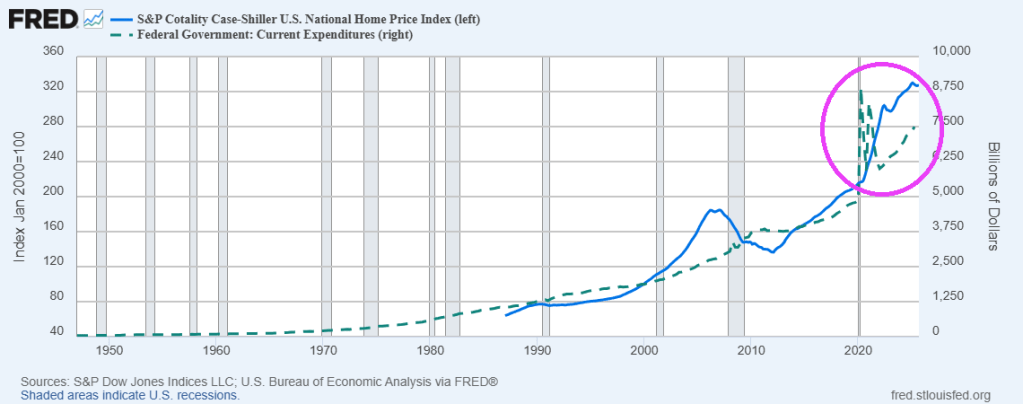

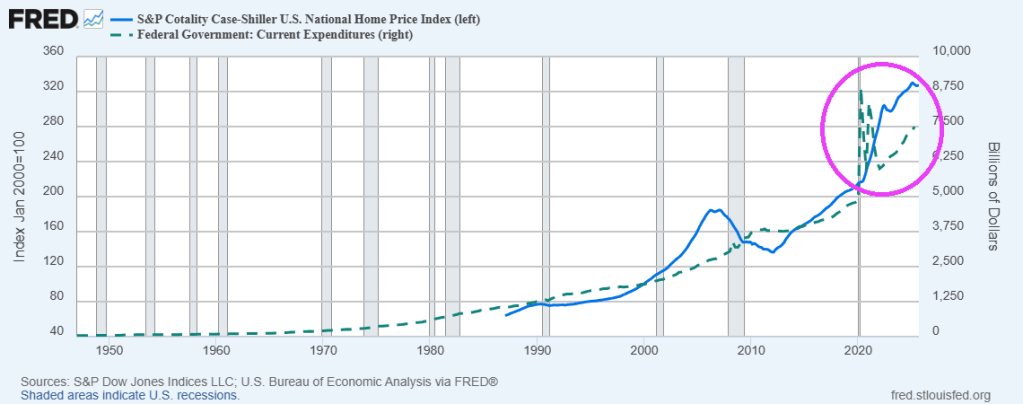

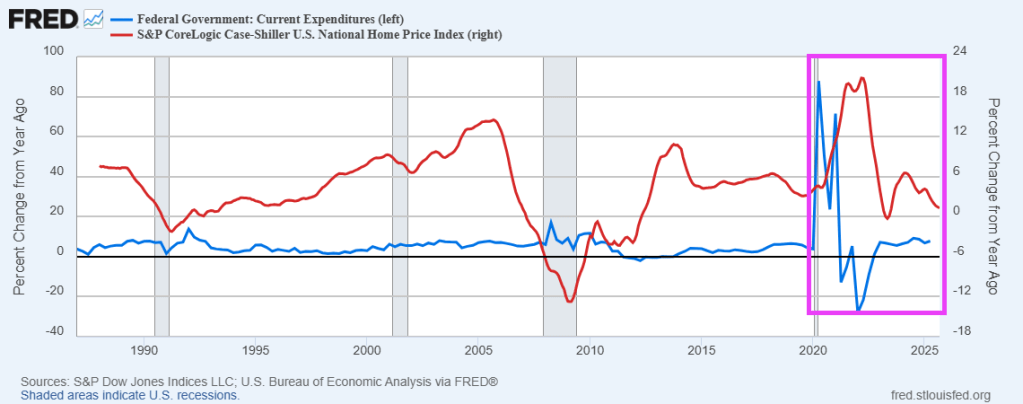

If we look at year-over-year changes, we see the Covid bump in housing prices corresponding with the surge in Federal spending. But things have simmered down since the bump in 2020-2023.

My suggestion is for the Federal government to stop interfering in the housing market.

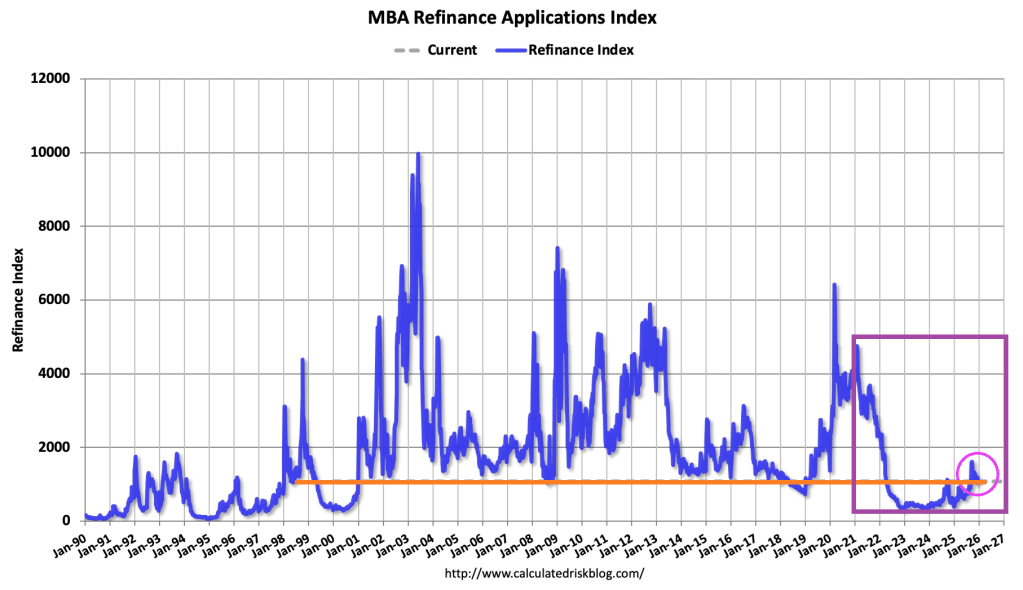

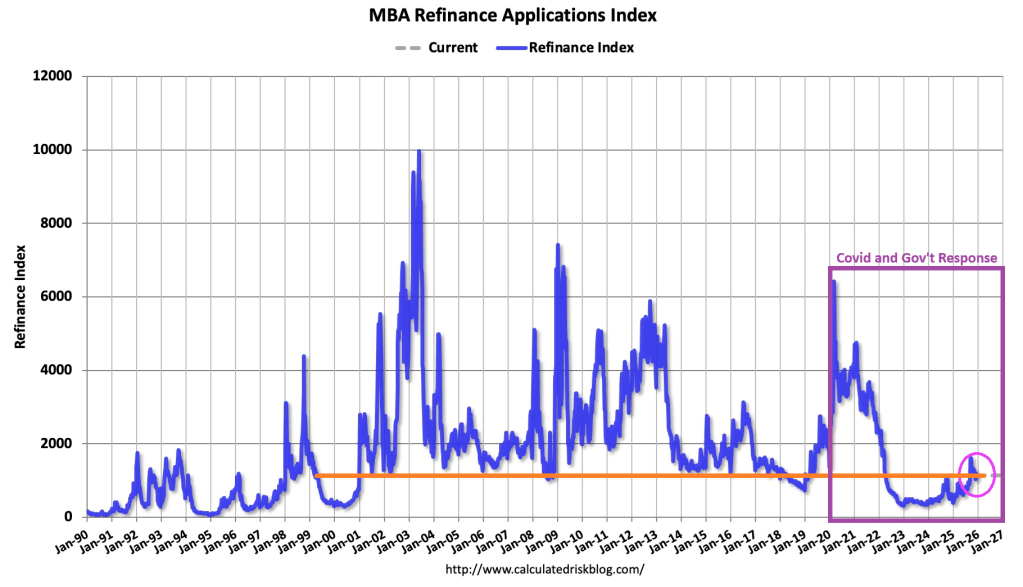

Nobody wastes money like government, particularly around events like Covid where Federal spending led to housing prices spiking after Covid outbreak in 2020. This made housing unaffordable for most households. This in turn helped kill the mortgage market.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 7 percent compared with the previous week and was 13 percent higher than the same week one year ago.

The Refinance Index decreased 4 percent from the previous week and was 86 percent higher than the same week one year ago.

Once again, the government response to the Wuhan Covid virus of 2020 helped drive up housing prices killing off mortgage demand.

Hallelujah, I love this economy so! Of course, former First Lady Jill Biden is on the national tour trashing the economy saying it was “perfect” under Joe Biden.

The Market Composite Index, a measure of mortgage loan application volume, increased 4.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 49 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index increased 32 percent compared with the previous week and was 19 percent higher than the same week one year ago.

The Refinance Index increased 14 percent from the previous week and was 88 percent higher than the same week one year ago.

Compared to the prior week’s data, which included an adjustment for the Thanksgiving holiday, mortgage application activity increased last week, driven by an uptick in refinance applications,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Conventional refinance applications were up almost 8 percent and government refinances were up 24 percent as the FHA rate dipped to its lowest level since September 2024. Conventional purchase applications were down for the week, but there was a 5 percent increase in FHA purchase applications as prospective homebuyers continue to seek lower downpayment loans. Overall purchase applications continued to run ahead of 2024’s pace as broader housing inventory and affordability conditions improve gradually.

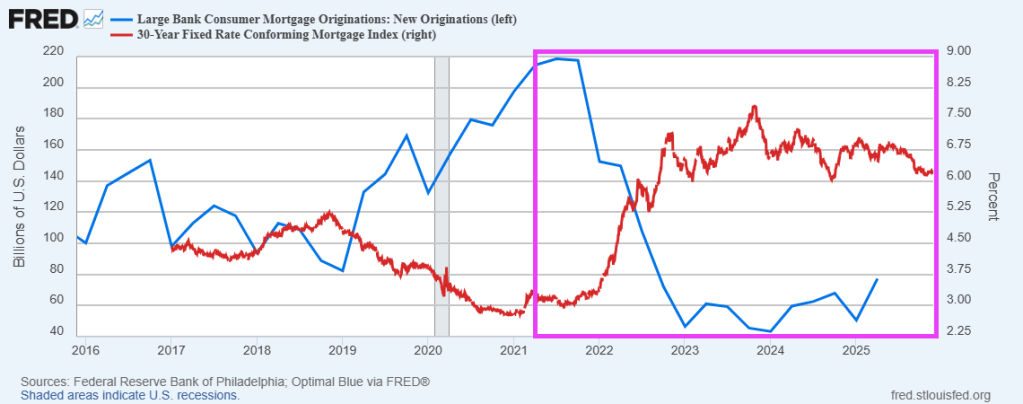

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.33 percent from 6.32 percent, with points increasing to 0.60 from 0.58 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Mortgage applications decreased 1.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 28, 2025. This week’s results include an adjustment for the Thanksgiving holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 33 percent compared with the previous week. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index decreased 32 percent compared with the previous week and was 17 percent higher than the same week one year ago.

The Refinance Index decreased 4 percent from the previous week and was 109 percent higher than the same week one year ago.

Mortgage rates moved lower in line with Treasury yields, which declined on data showing a weaker labor market and declining consumer confidence. The 30-year fixed mortgage rate declined to 6.32 percent after steadily increasing over the past month. After adjusting for the impact of the Thanksgiving holiday, refinance activity decreased across both conventional and government loans, as borrowers held out for lower rates. Purchase applications were up slightly, but we continue to see mixed results each week as the broader economic outlook remains cloudy, even as cooling home-price growth and increasing for-sale inventory bring some buyers back into the market.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.32 percent from 6.40 percent, with points decreasing to 0.58 from 0.60 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

According to Bill McBride at Calculated Risk, In October, sales in these markets were up 2.4% YoY. Last month, in September, these same markets were up 7.7% year-over-year Not Seasonally Adjusted (NSA). The NAR reported sales were up 2.9% YoY NSA, so this sample is close.

Miami FL and central Florida lead the nation in closed sales of housing with Columbus OH second with 9.5% YoY growth in closed sales.

Let’s see if Ohio State beats Indiana for the Big 10 championship game on Saturday after OSU whooped Michigan 27-9 and won the gold pants this past Saturday.

Former Detroit Lions HC Matt Patricia, now OSU’s defensive coordinator.

How can the current housing disaster be fixed? One answer is to build more homes (made difficult by local government zoning and building policies). Another is increase household income. But Fed money printing is the easiest way to increase home prices.

Since the Federal government spending spree associated with Covid ended, median household income has declined. But so have home prices.

But in terms of home price growth compared to median household income, you can see that home price growth has slowed after the Covid spending spike, but so did median household income.

Pray that The Fed doesn’t resort to trying to fix the housing market. They will only make things worse.

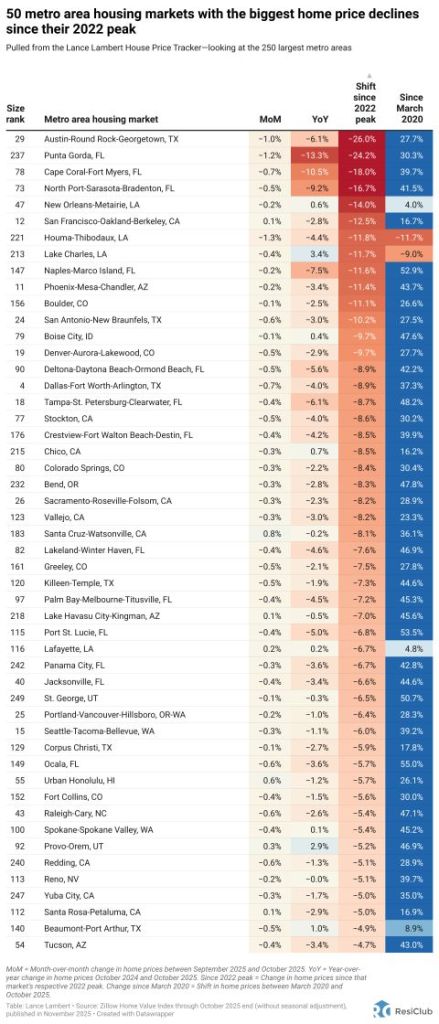

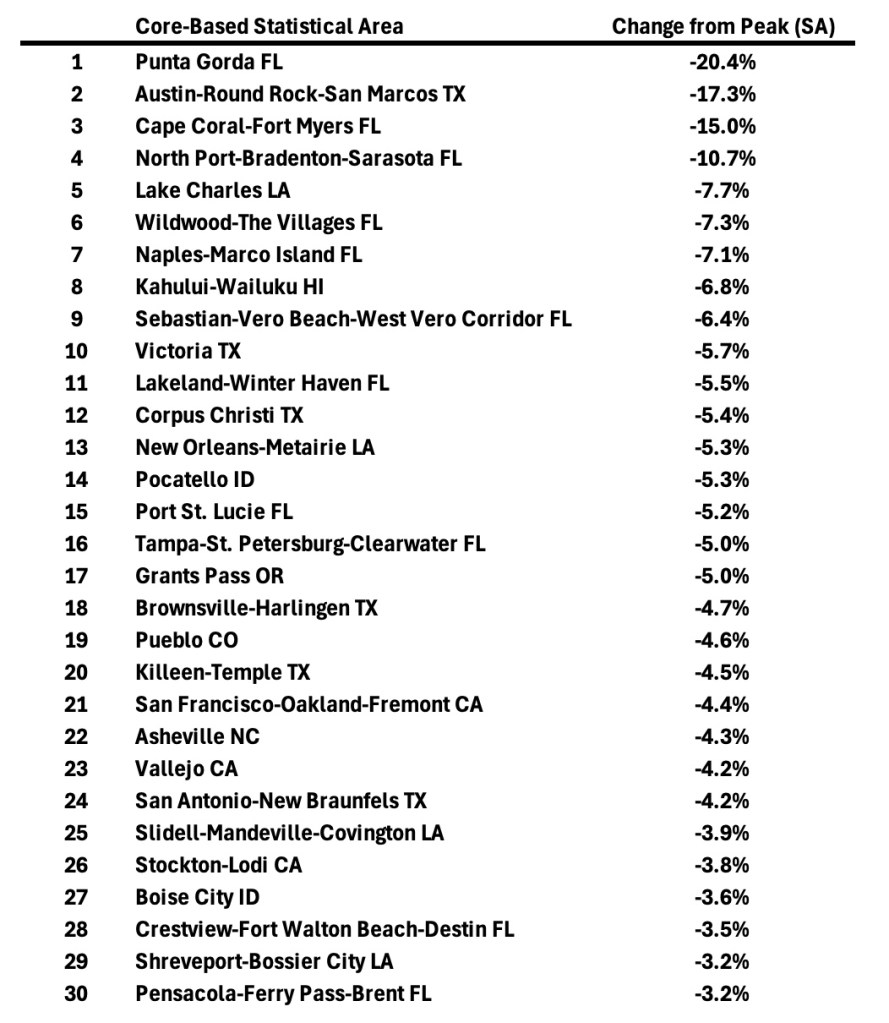

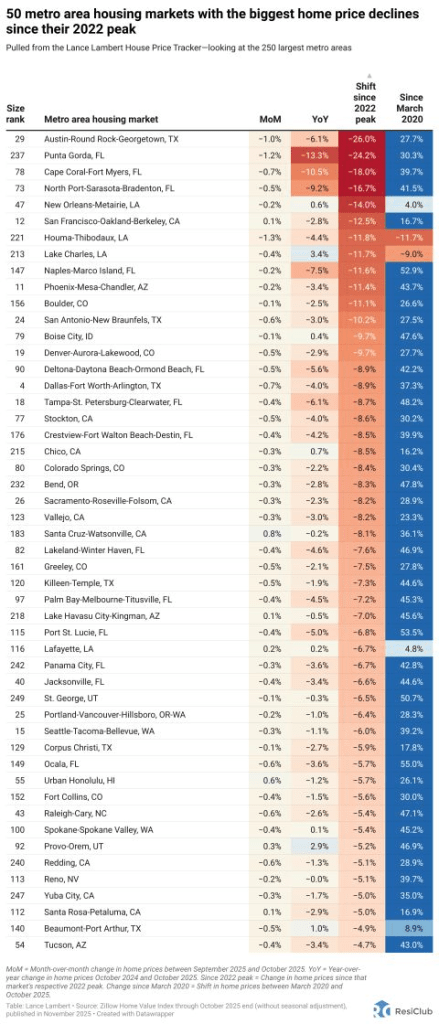

There was a rush from the northeast US to Florida, now we are seeing a reversal in home prices. Punta Gorda FL, a suburb of Ft Myers, leads the nation with a -20.4% decline from its peak. Austin TX is second at -17.3% from peak. And Fort Myers FL is third at -15.0% from peak. In fact, 11 of the top 30 losers are in Florida. Texas has 6 of the top 30.

Another slice of the data show Punta Gorda FL with -13.3% YoY loss. And Naples FLA is down -11.6% YoY.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 20 percent higher than the same week one year ago.

The Refinance Index decreased 6 percent from the previous week and was 117 percent higher than the same week one year ago.

The refinance share of mortgage activity decreased to 53.4 percent of total applications from 55.4 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.9 percent of total applications.

The FHA share of total applications decreased to 18.8 percent from 19.9 percent the week prior. The VA share of total applications increased to 15.4 percent from 15.2 percent the week prior. The USDA share of total applications increased to 0.4 percent from 0.3 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.40 percent from 6.37 percent, with points decreasing to 0.60 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

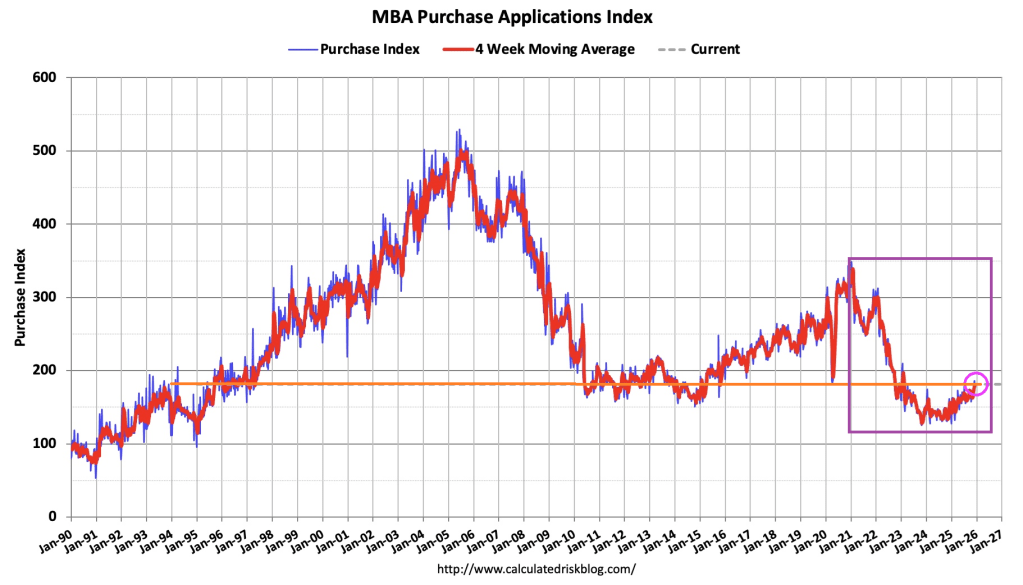

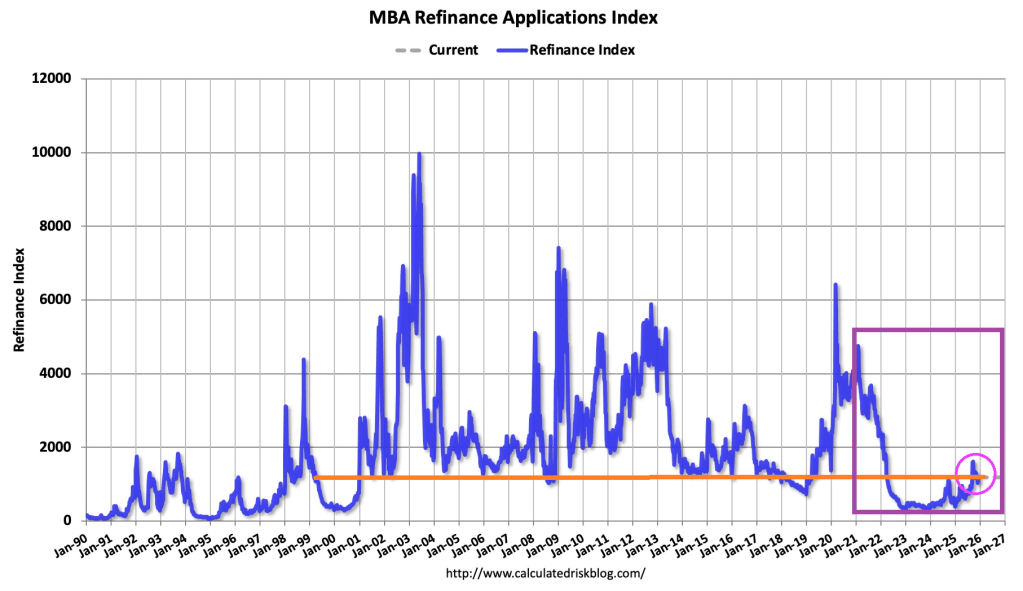

But mortgage demand hasn’t been the same is 2021. Rates are higher, mortgage demand is lower. Higher home prices coupled with higher mortgage rates is bad news.

You must be logged in to post a comment.