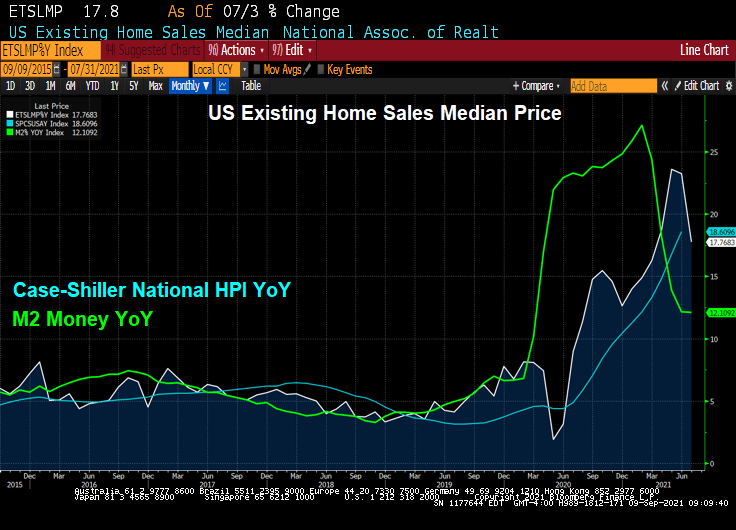

Not only after home prices screaming at near 20% YoY growth, but apartment rents are surging as well.

(Bloomberg) — Apartment rents were up in August from a year earlier in all the top 30 U.S. metro areas, the first time that’s happened since the start of the pandemic, according to a new report by Yardi.

The national average rent inmulti-family buildings rose 10.3% from a year earlier to $1,539 — the first double-digit rise in the dataset’s history — after a $25 increase in August, the real-estate firm said. Over the past 10 years, the average pace of growth has been 2%.

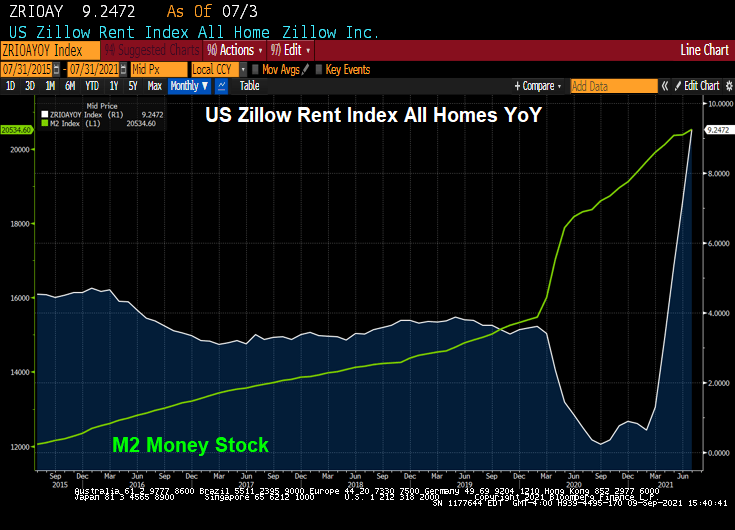

Zillow’s rent index of all homes is growing at 9.25% YoY.

Fed Chair Jerome “Inflation is Transitory” Powell.

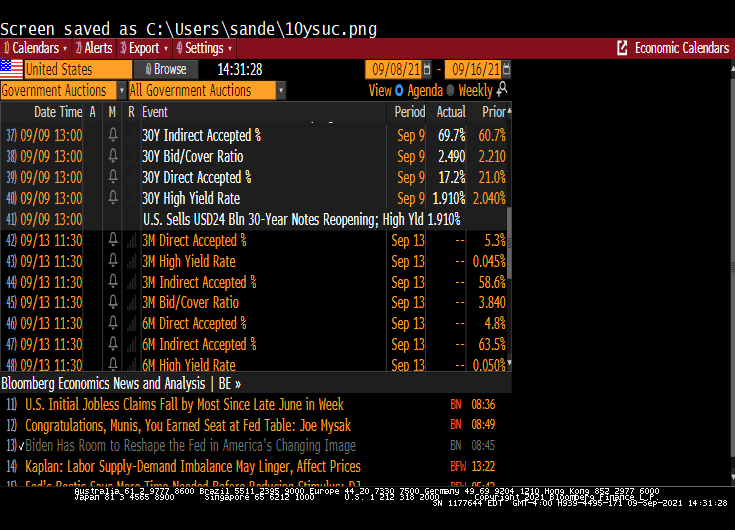

Face it, the 30-year Treasury market is not as interesting as widely-traded as the 10-year Treasury market. But we did see some interesting revelations in today’s 30 year Treasury auction.

If yesterday’s 10Y auction was blockbuster, one of the strongest benchmark sales on record, then today’s $24 billion offering of 30Y paper – the last coupon auction of the week – was nothing short of spectacular.

Printing at a high yield of just 1.910%, the auction not only stopped at the lowest yield since January’s 1.825%, but also stopped through the When Issued by a whopping 1.8bps, the most since April and ended 4 consecutive months of tails in the 30Y tenor.

The bid to cover of 2.486 was not only a big jump from last month’s 2.208 but also the highest since the 2.500% in July 2020, and far above the six-auction average of 2.276.

The bid-to-cover ratio is the dollar amount of bids received in a Treasury security auction versus the amount sold. The bid-to-cover ratio is an indicator of the demand for Treasury securities. A high ratio is an indication of strong demand.

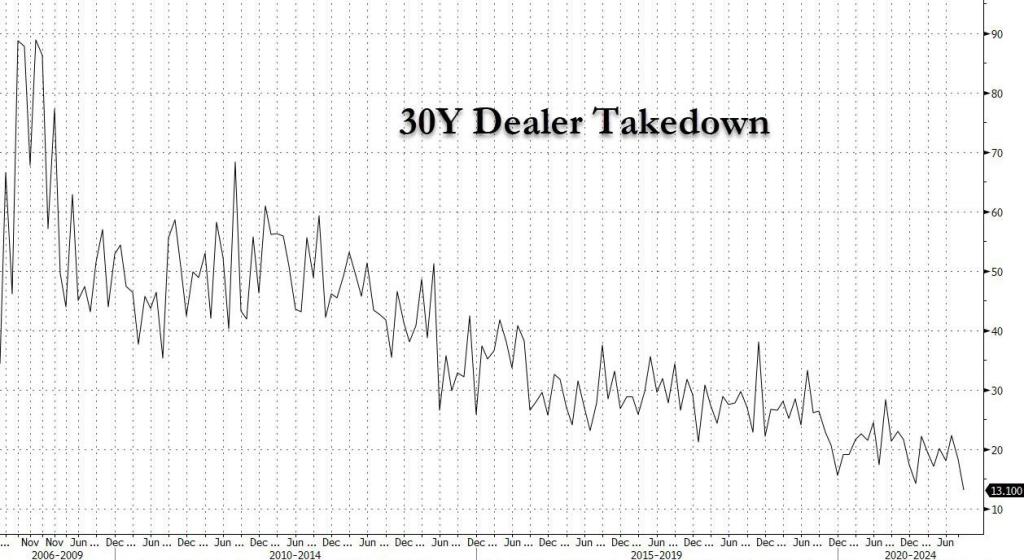

Primary dealers are responsible for absorbing any supply not bought by direct or indirect bidders. Indirect bidders, which include fund managers and foreign central banks. Dealer takedown of the 30Y Treasury is historically low.

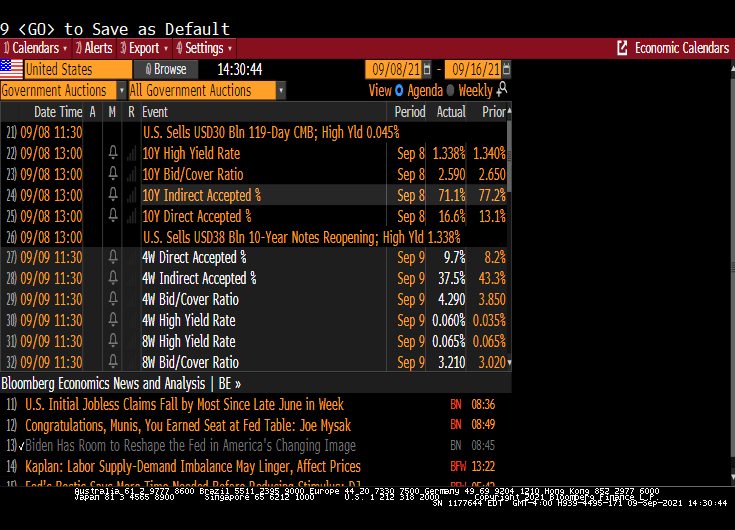

The 10-year auction was similar in that the high rate fell. But the bid-to-cover declined.

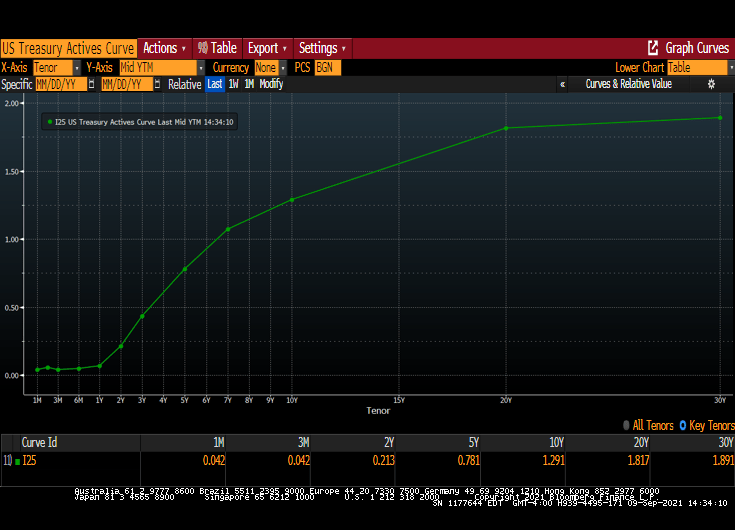

The US Treasury actives curve remains upward sloping, albeit at lower yields across the curve.

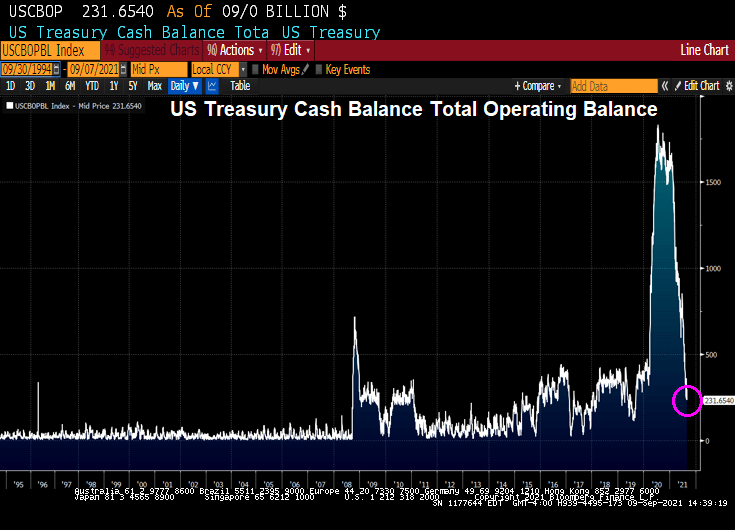

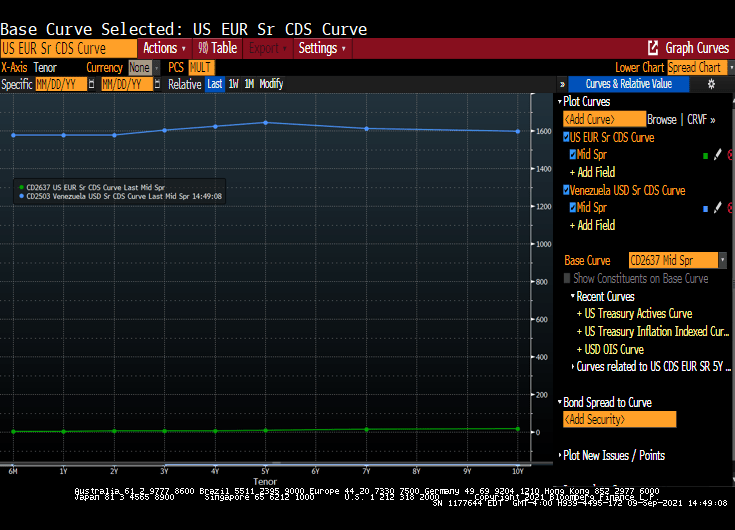

Meanwhile, Treasury Secretary Janet Yellin’ is fear-mongering about a possible US debt default. True, US Treasury cash balance has declined to $231 billion.

Will Congress pass a budget and fill the Treasury coffers will lots of money? Of course. Here is the US CDS curve compared to Venezuela’s CDS curve. The US curve is close to zero while Venezuela’s at near 1,600 across tenors.

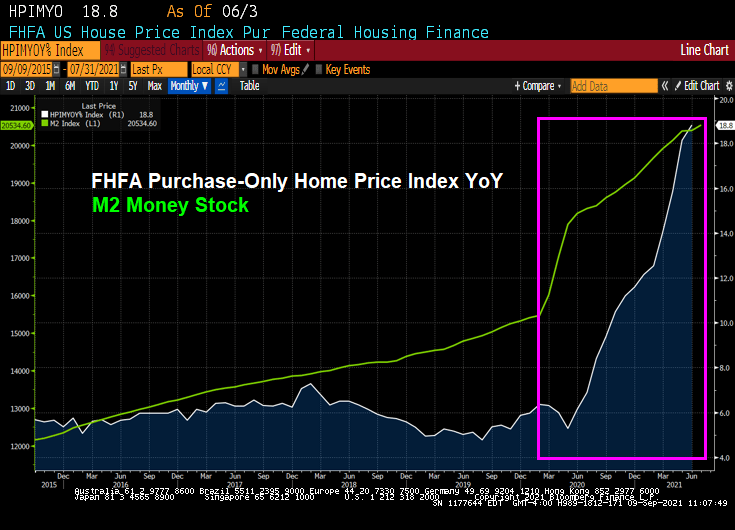

Covid struck in early 2020 and The Fed spiked the punchbowl with a massive surge in M2 Money. Like a storm surge.

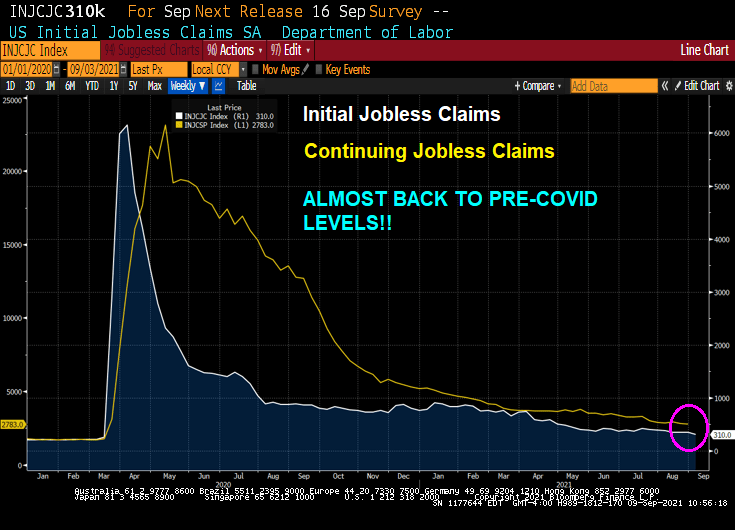

Today’s unemployment report showed initial jobless claims and continuing jobless claims ALMOST at pre-Covid levels.

So it appears that The Fed’s job is done (under the assumption that The Fed had anything to do with the recovery).

So did The Fed almost violently overreact to the Covid crisis? The Atlanta Fed’s Raphael Bostic says it is too early to withdraw while St Louis Fed’s James “Bully” Bullard says it is time to taper.

Really Raph? 18.8% price growth is not enough for you?

(Bloomberg) — Orchard, which offers cash to homebuyers upfront so they can purchase a new residence before selling their old one, raised $100 million to fuel growth in an ultra-competitive housing market that’s pushing shoppers to find new ways to stand out.

The fundraising round values the startup at more than $1 billion, making it the latest unicorn company to tackle the challenge of simplifying the process of buying or selling a home. Boston-based Accomplice led the round, with existing investors FirstMark, Revolution, First American and Juxtapose also participating.

“We can say we’re a unicorn, which feels good for about five seconds, and then it’s back to the real world of building a business,” Chief Executive Officer Court Cunningham said in an interview. “We’re trying to create a modern way to buy and sell homes, and that’s capital intensive.”

Cunningham, previously CEO of online marketing company Yodle, started Orchard in 2017 to take on what he viewed as a ripe opportunity: Consumers were frustrated with the traditional way of buying and selling homes, and the $1.7 trillion U.S. housing market was big enough to make tackling the problem worthwhile.

Orchard focuses on people who are trying to buy their next home while selling an existing one, a nerve-wracking process that can cause a transaction to collapse or result in households carrying two mortgages. In addition to offering cash to help clients buy their next home, the New York-based company provides funds to make light repairs before listing the existing home on the market. Orchard seeks to profit by operating as a brokerage and earning commissions.

There have always been services that purchase homes from you. Typically, there firms simply pay off your mortgage, so if you have a higher mortgage balance relative to you home value, you may not like what you are offered. But Orchard is not that model.

If you “List with Orchard,” and your home doesn’t end up selling on the open market, Orchard will buy your home. Sellers in some markets also have the option to sell immediately to the company. Orchard wants you to list for 30 days before selling to them for their backup cash offer price. If you sell directly to Orchard, you’ll also pay an additional 1% convenience fee on top of the 6% you’re already paying commission.

When home prices have been rising at a 17-18% YoY pace, this seems like a good model. But what if The Federal Reserve removes it massive monetary stimulus and/or The Federal Government slows down it fiscal stimulus? Then Orchard, if they purchase your home, will likely lose considerable amounts. Being aware of this possibility, Orchard is likely to buy homes at a considerable discount.

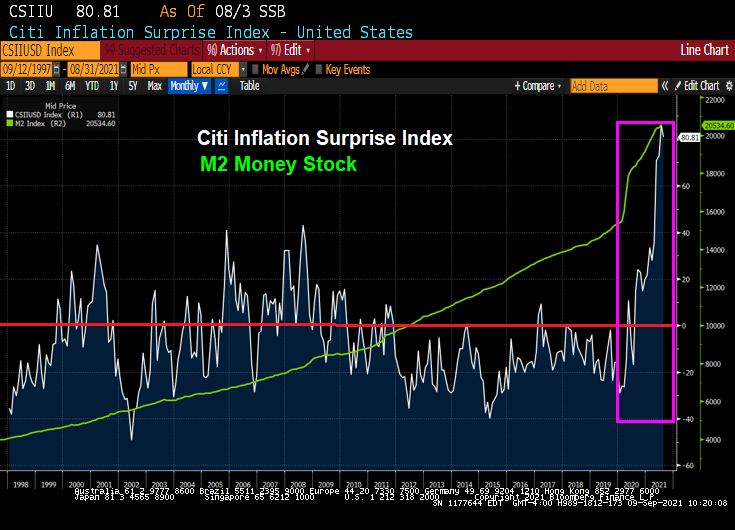

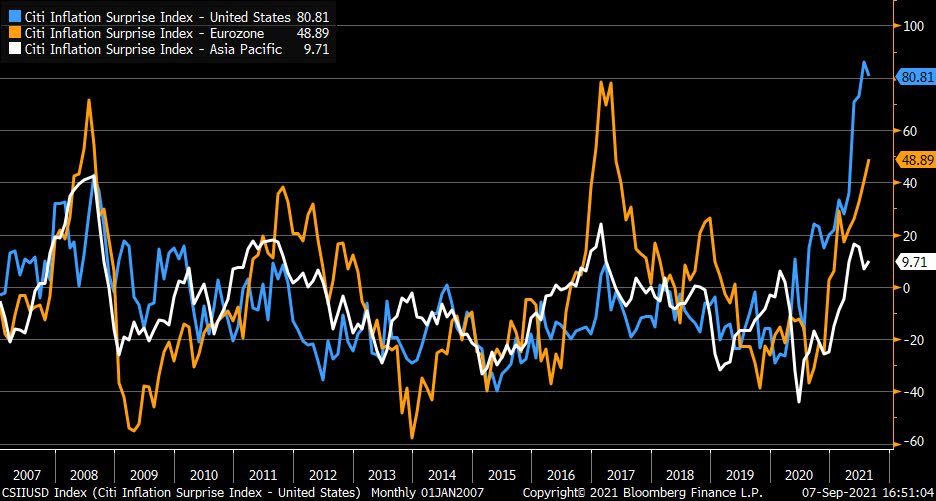

But there is still worries about inflation. Here is the Citi Inflation Surprise index.

Publicly traded companies known as iBuyers are pioneering a high-tech approach to home-flipping intended to make selling properties easier. Those firms include Opendoor Technologies Inc., Redfin Corp., and Offerpad Solutions Inc. A fourth, Zillow Group Inc., recently raised $450 million by issuing bonds, backed by the homes it buys and sells.

Economic growth downshifted slightly to a moderate pace in early July through August. The stronger sectors of the economy of late included manufacturing, transportation, nonfinancial services, and residential real estate. The deceleration in economic activity was largely attributable to a pullback in dining out, travel, and tourism in most Districts, reflecting safety concerns due to the rise of the Delta variant, and, in a few cases, international travel restrictions.

The other sectors of the economy where growth slowed or activity declined were those constrained by supply disruptions and labor shortages, as opposed to softening demand. In particular, weakness in auto sales was widely ascribed to low inventories amidst the ongoing microchip shortage, and restrained home sales activity was attributed to low supply.

Growth in non-auto retail sales slowed a bit in some Districts, rising at a modest pace, on balance, across the nation.

Residential construction was up slightly, on balance, and nonresidential construction picked up modestly.

Trends in loan volumes varied widely across Districts, ranging from down modestly to up strongly.

Reports on the agriculture and energy sectors were mixed across Districts but, on balance, positive.

Looking ahead, businesses in most Districts remained optimistic about near-term prospects, though there continued to be widespread concern about ongoing supply disruptions and resource shortages.

Employment and Wages:

All Districts continued to report rising employment overall, though the characterization of the pace of job creation ranged from slight to strong.

Demand for workers continued to strengthen, but all Districts noted extensive labor shortages that were constraining employment and, in many cases, impeding business activity.

Contributing to these shortages were increased turnover, early retirements (especially in health care), childcare needs, challenges in negotiating job offers, and enhanced unemployment benefits.

Some Districts noted that return-to-work schedules were pushed back due to the increase in the Delta variant.

With persistent and extensive labor shortages, a number of Districts reported an acceleration in wages, and most characterized wage growth as strong—including all of the midwestern and western regions.

Several Districts noted particularly brisk wage gains among lower-wage workers.

Employers were reported to be using more frequent raises, bonuses, training, and flexible work arrangements to attract and retain workers.

Prices:

Inflation was reported to be steady at an elevated pace, as half of the Districts characterized the pace of price increases as strong, while half described it as moderate.

With pervasive resource shortages, input price pressures continued to be widespread.

Most Districts noted substantial escalation in the cost of metals and metal-based products, freight and transportation services, and construction materials, with the notable exception of lumber whose cost has retreated from exceptionally high levels.

Even at greatly increased prices, many businesses reported having trouble sourcing key inputs.

Some Districts reported that businesses are finding it easier to pass along more cost increases through higher prices.

Several Districts indicated that businesses anticipate significant hikes in their selling prices in the months ahead.

Here are the highlights by Regional Feds:

Boston: Economic activity in the First District expanded at a modest to strong pace over the summer of 2021. Contacts reported higher prices and wages but complained more about an inability to get supplies and to hire workers. Contacts were optimistic and hoped supply issues would ease in 2022.

New York: Growth in the regional economy moderated, though contacts remained optimistic about the near-term outlook. Employment and wages increased, with businesses reporting widespread labor shortages. Tourism leveled off, and service-sector businesses reported some deceleration in activity. Input price pressures remained widespread, and more businesses have raised or plan to raise their selling prices.

Philadelphia: Business activity continued at a moderate pace of growth during the current Beige Book period – still below levels attained prior to the pandemic. The rise of Delta variant cases has trimmed growth in some sectors, while labor shortages and supply chain disruptions continued apace. Overall, wage growth increased to a moderate pace, while prices continued growing moderately and employment continued to grow modestly.

Cleveland: Economic activity grew solidly, but supply constraints limited many firms’ ability to meet demand. Staff levels increased modestly amid intense labor shortages. Reports of rising nonlabor costs, wages, and prices continued to be widespread. Firms expected demand would remain strong in the near term, but they were less optimistic that labor and supply challenges would abate enough to ease the upward pressure on wages and costs.

Richmond: The regional economy expanded moderately, but many firms faced shortages and higher costs for both labor and non-labor inputs. Port and trucking volumes picked up from already high levels, but manufacturers and services firms experienced delays and long lead times for goods. Employment rose moderately as labor shortages and wage increases were widely reported. Price growth picked up and was robust compared to last year.

Atlanta: Economic activity expanded moderately. Labor markets improved and wage pressures became more widespread. Some nonlabor costs rose. Retail sales increased. Leisure travel was strong and hotel occupancy levels rose. Residential real estate demand remained solid. Commercial real estate conditions were steady. Manufacturing activity expanded. Banking conditions were stable.

Chicago: Economic activity increased moderately. Employment increased strongly, manufacturing grew moderately, business spending was up modestly, construction and real estate rose slightly, and consumer spending decreased slightly. Wages and prices increased strongly while financial conditions slightly improved. There was some retreat in prospects for agricultural income.

St. Louis: Economic conditions have continued to improve at a moderate pace since our previous report. Across all industries, contacts are concerned about the Delta variant and its economic impact. Contacts continued to report that labor and material shortages. Overall inflation pressures remain elevated, but firms reported varying degrees of pass-through to customers.

Minneapolis: The District economy saw moderate growth despite continued inventory shortages and higher prices. Employment grew strongly but hiring demand continued to outstrip labor response by a wide margin. Consumer demand remained strong, leveraging growth in services, tourism, and manufacturing. Drought took a growing toll on agriculture, though higher prices benefited farmers. Minority and women-owned business enterprises saw moderate growth in activity.

Kansas City: Economic activity continued to grow at a moderate pace through August. Demand remains elevated for most businesses, and a majority of contacts expect activity to remain elevated amid the recent surge in COVID cases. Wages grew at a robust pace, but labor shortages persist. As a result of widespread drought, pasture and range land in several states was in poor or very poor condition.

Dallas: The District economy expanded at a solid rate, with broad-based growth across sectors. Employment growth was robust, with a pickup seen in the service sector. Wage and price growth remained elevated amid widespread labor and supply chain shortages. Outlooks stayed positive, though surging COVID-19 cases has added uncertainty to outlooks.

San Francisco: Economic activity in the District expanded moderately. Hiring activity intensified further, as did upward pressures on wages and inflation. Retail sales increased modestly, while conditions in the services sector deteriorated somewhat. Activity in the manufacturing and agriculture sectors increased slightly. Residential construction edged down somewhat, while lending activity remained largely unchanged.

As Milton Friedman once said, “If you put The Federal Government in charge of the Sahara Desert, in 5 years there would be a shortage of sand.” And The Fed is no slouch at creating shortages either.

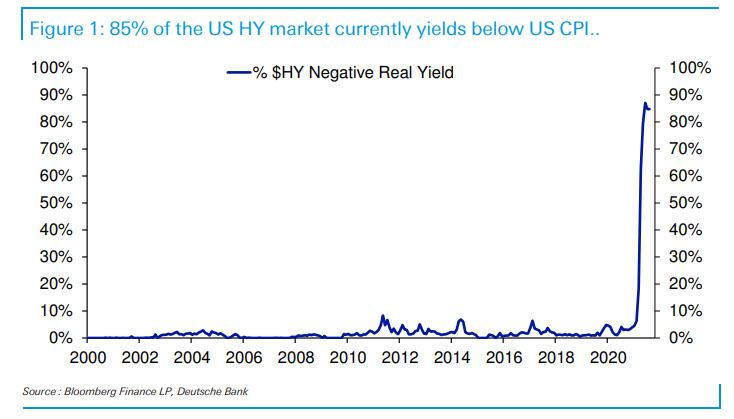

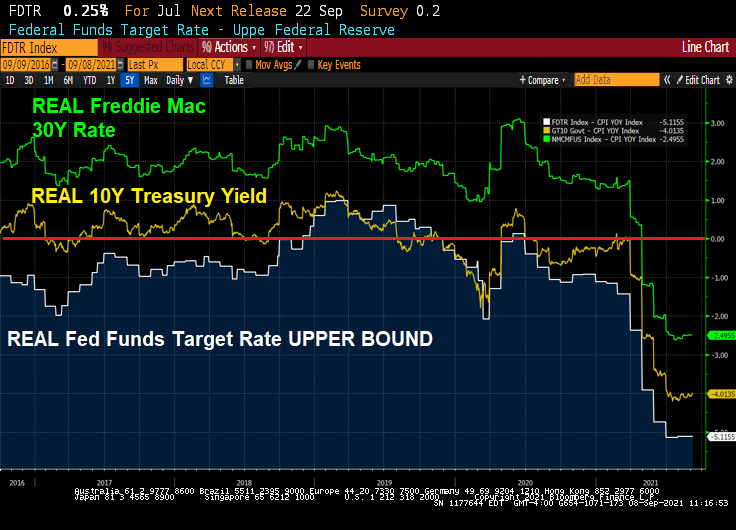

According to Deutsche Bank, 85% of the US High Yield market has a yield below the current rate of inflation.

Its not only high-yield bonds that have negative REAL yields, but even The Fed Funds Target rate is negative at -5.12%. The real 10-year government bond yield is -4.01% and the REAL Freddie Mac 30-year mortgage survey rate is -2.5%.

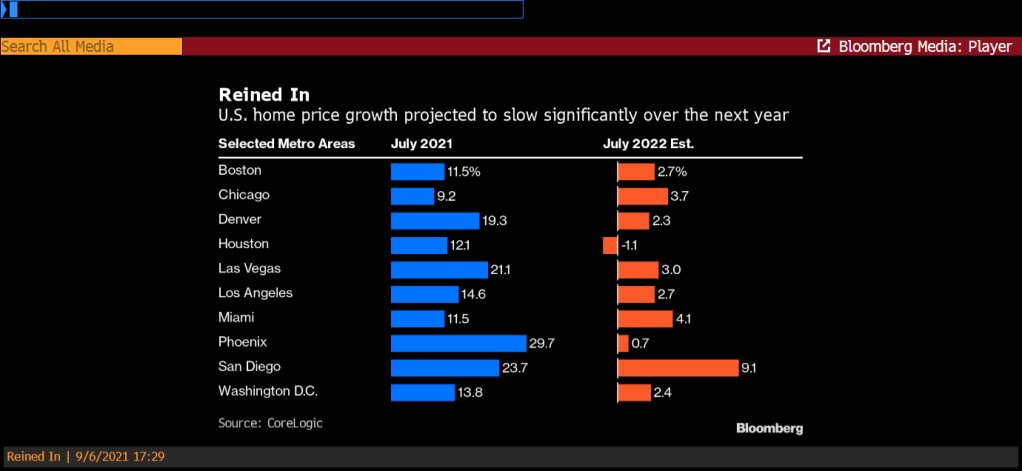

The jump is the largest 12-month gain in the index since the series began 45 years ago. On a month-over-month basis, home prices increased by 1.8% in July from June.

“Home price appreciation continues to escalate as millennials entering their prime home buying years, renters looking to escape skyrocketing rents and deep pocketed investors drive demand,” said Frank Martell, president and CEO of CoreLogic, a global property-information firm.

The rush of home buyers — amid extremely low mortgage rates — has caused a lack of supply, which is unlikely to be resolved over the next five to 10 years “without more aggressive incentives for builders to add new units,” he said in a statement.

But it is the forecast for July 2022 that is interesting. A slowdown in home price growth across the board.

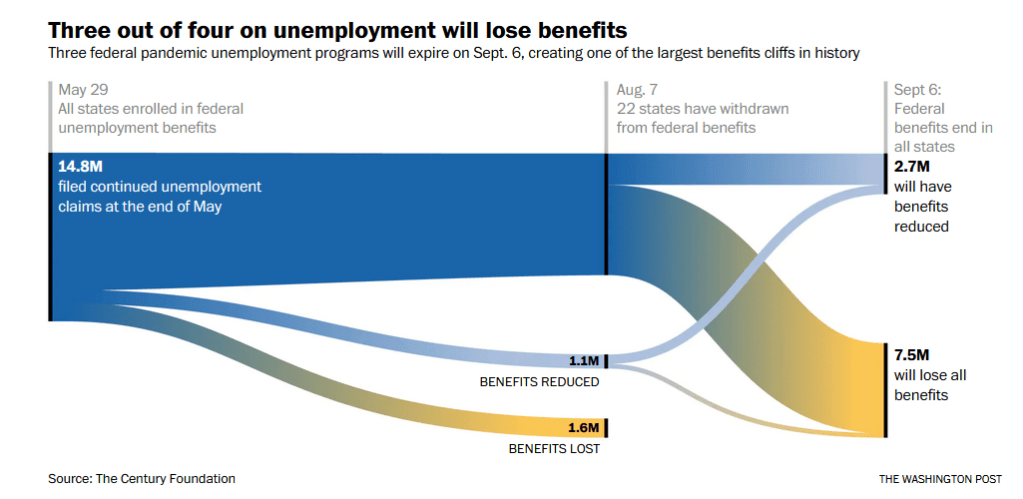

Lets see what happens to wage growth are three out of four Americans lose their Covid benefits as of today.

What if inflation is actually transitory like The Federal Reserve has been saying? Or is The Fed really telling us about an impending economic slowdown after the Fed’s and Federal government stimulypto wears off?

Iron ore prices have slowed noticeably after peaking earlier this year. Lumber futures (random length) have crashed to pre-Covid levels.

On the other hand, food stuffs and raw industrials remain elevated, but the growth in price has stalled (see pink box).

President Biden, aka The Kabul Klutz, is now recommending tax increases as a result of the terrible jobs report from Friday. Rather than focus on The Fed’s monetary stimulus not working for the labor market.

The problem with fiscal stimulus is that the debt lasts forever but the GDP effects are short-lived. And The Fed is a crazy train.

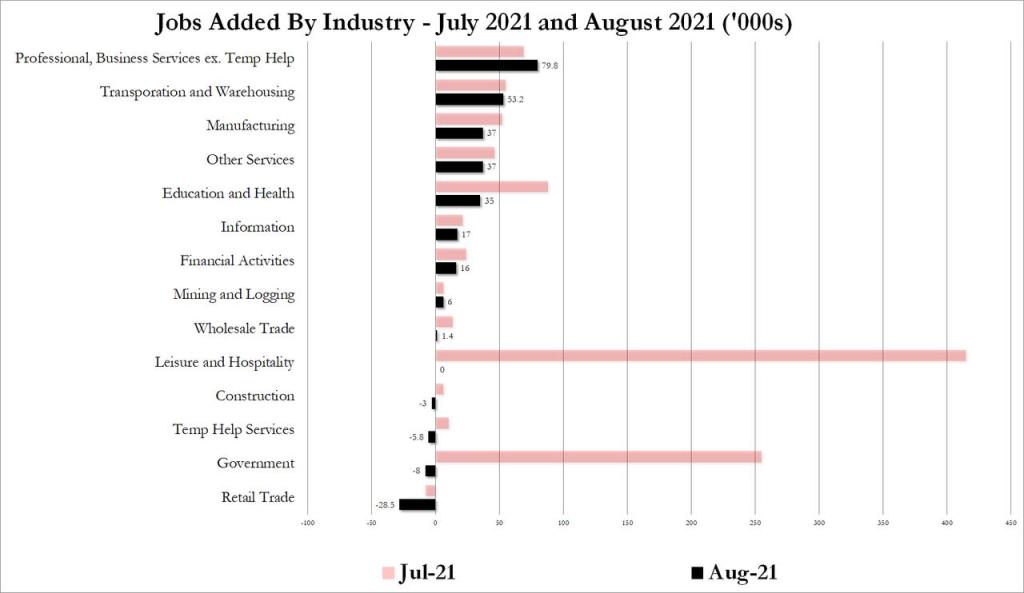

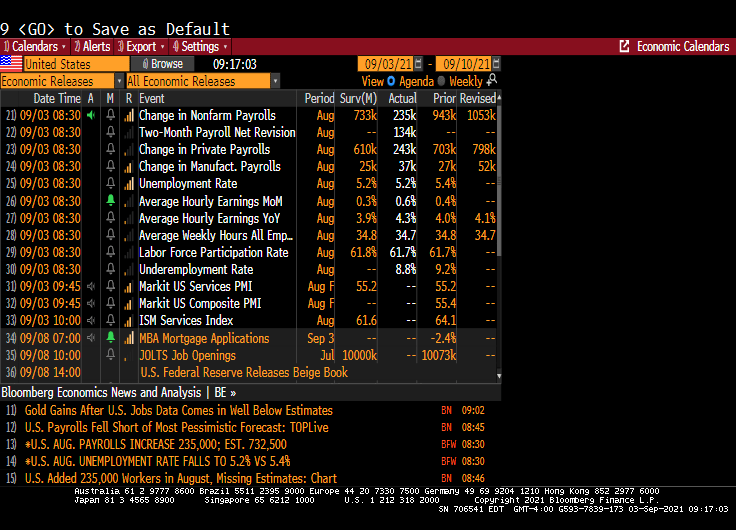

Well, after the dismal ADP print we knew that the August jobs numbers would be worse than imaginable. And they were!

A big miss on the topline job creation number — the establishment survey suggested only 235,000 jobs were created in August, versus expectations for 733,000 — has undercut what little chance there was left of a Fed announcement on tapering later this month. It should make for a very interesting debate among policy makers about forward momentum in the labor market.

The shocker was in the leisure and hospitality sector, which created zero new jobs on net in August after figures of around 400,000 in each of the previous two months. There was a dip in hiring in other service sectors too, but nowhere near as significant. That could perhaps be due to some early impact from the spread of the delta variant in recent weeks.

On the household survey, the numbers looked better. According to those figures, the unemployment rate fell to 5.2%, in line with estimates, thanks to a 509,000 increase in reported employment. That also propelled the prime working-age employment to population ratio to 78%, from 77.8% in July.

Disparities narrowed in August as well, according to prime working-age EPOP ratios by race and ethnicity. Prime working-age Black EPOP, in particular, jumped to 73% from 72.2% the month before — outpacing the rest.

Equity futures pared a modest gain after the release, with contracts on the S&P 500 Index flat as of 9:09 a.m. in New York. With wages climbing, Treasury yields rose, with those on 10-year notes rising 4 basis points to 1.33%. The Bloomberg Dollar Index was down 0.3%.

The unemployment rate dropped which a misleading headline. That simply means that more people dropped out of the labor force than were unemployed. Not a good way to lower the unemployment rate.

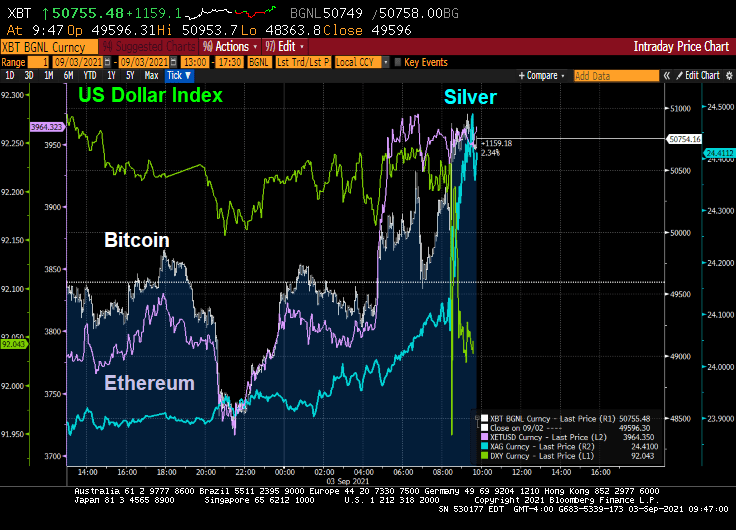

Alternative investments silver, Bitcoin and Ethereum rose on the lousy jobs report as the US Dollar dropped.

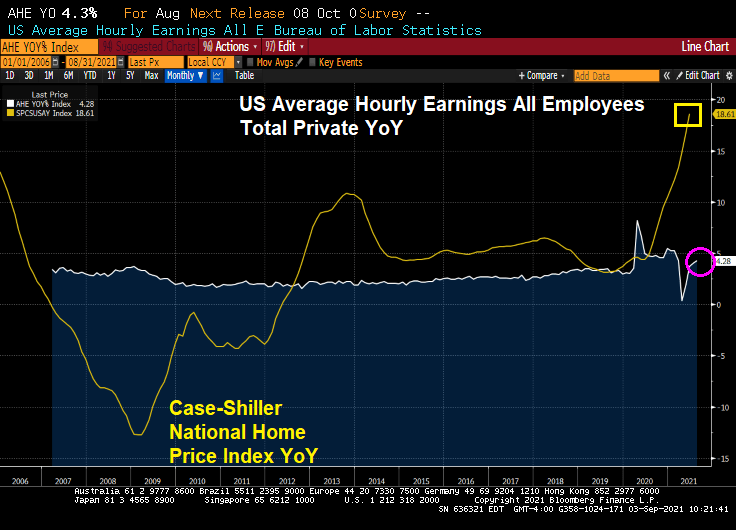

The good news? US Average Hourly Earnings All Employees Total Private YoY rose to 4.28%! The bad news? US home prices are rising at a 18.61% pace.

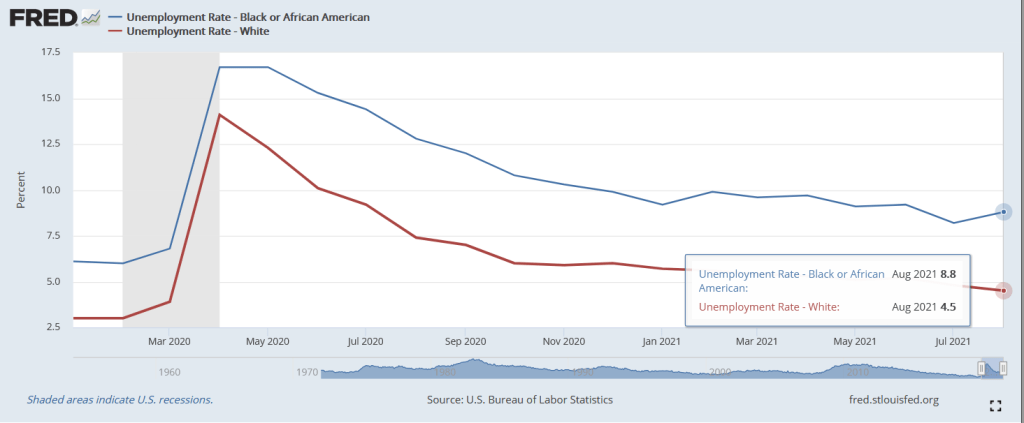

The bad news? Black unemployment rose to 8.8% in August while white unemployment fell to 4.5%. This represents a widening of the employment gap that is higher in August than pre-Covid.

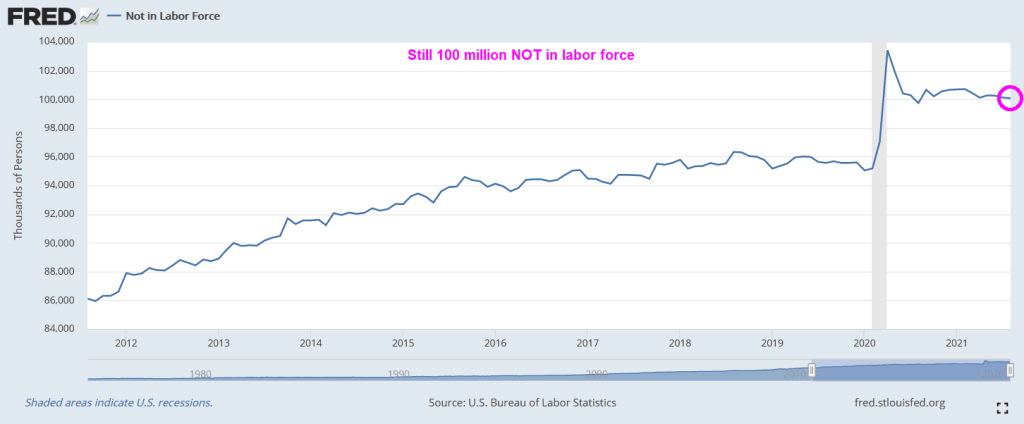

There are still over 100 million NOT in the labor force, higher than pre-Covid.

So, The Fed’s plans to begin tapering have gone up in smoke.

In a meandering and sometimes off-kilter investment outlook posted on his website, the onetime bond king said longer-term Treasury yields are so low that the funds that buy them belong in the “investment garbage can.”

Ten-year yields traded at 1.29% as of 6:07 a.m. in New York. They are likely to climb to 2% over the next 12 months, handing investors a loss of roughly 3%, he wrote. Stocks could also fall into the category of “trash” should earnings growth fall short of lofty expectations.

“Cash has been trash for a long time, but there are now new contenders,” said Gross, who co-founded Pacific Investment Management Co. in the 1970s and retired in 2019. “Intermediate to long-term bond funds are in that trash receptacle for sure, but will stocks follow? Earnings growth had better be double-digit-plus or else they could join the garbage truck.”

The Bloomberg U.S. Treasury index has fallen 1.4% this year, and an extension of that decline would make for its first annual loss in eight years. Investment-grade debt in general has suffered similarly, with a Bloomberg gauge on track for the worst yearly performance since 2015.

Gross, 77, has been bearish on bonds for a while. In March, he told Bloomberg TV that he began betting against Treasuries at about the 1.25%. Rates initially sold off in the aftermath, but have since rallied as a resurgent coronavirus raises concerns over economic growth.

In Monday’s note, Gross suggested supply and demand dynamics are stacking up against Treasuries, saying that yields at current levels have “nowhere to go but up.”

The Federal Reserve, which has been absorbing about 60% of net Treasury issuances through its quantitative-easing program, may soon start scaling back asset purchases at a time when demand from foreign central banks and investors has already been waning, he wrote. Meanwhile, fiscal deficits of at least $1.5 trillion going forward suggest Treasury supply will remain high.

“How willing, therefore, will private markets be to absorb this future 60% in mid-2022 and beyond?” Gross wrote. “Perhaps if inflation comes back to the 2%+ target by then, a ‘tantrum’ can be avoided, but how many more fiscal spending programs can we afford without paying for it with higher interest rates?”

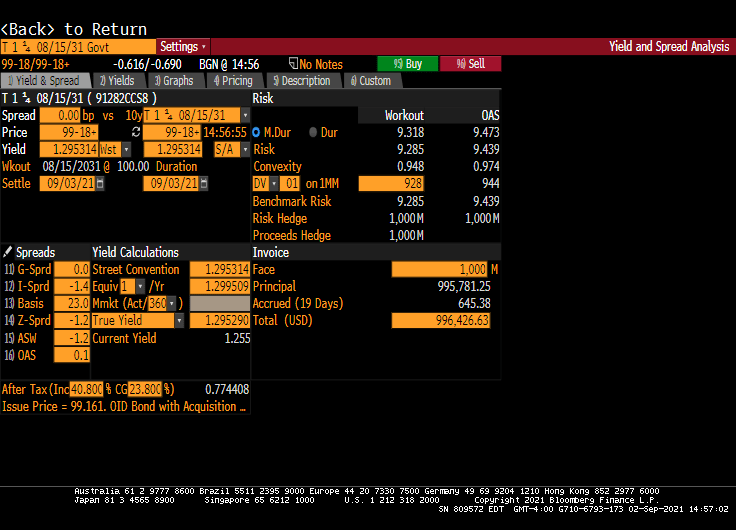

Duration of 10-year Treasuries is 9.473 given the low coupon rate indicating relatively high risk given a low coupon rate.

You must be logged in to post a comment.