President Trump ordered Fannie Mae and Freddie Mac to operate like The Federal Reserve. Buying assets to manipulate interest rates. In this case, F&F have been ordered to buy $200 billion of agency MBS.

Thursday’s Truth Social post triggered an immediate snap tighter in mortgages, led by the belly and lower coupons. By pulling MBS spreads tighter and crowding out real-money buyers, Fannie and Freddie’s purchases would push incremental demand into Treasuries as the next-best duration substitute, putting a modest bid under the belly of the curve.

However, execution and the ultimate size of purchases is still unclear, as my colleague Alyce Andres noted. If the government-sponsored enterprises GSEs stagger purchases, and signal an ultimate increase above the announces $200 billion, further tightening should occur. They can fund a lot of the buys from existing liquidity portfolios, though there’s a path where they could issue short-term debt to preserve operating buffers and could nudge repo wider at the margin.

The bigger transmission channel is hedging, as highlighted by colleagues Ira Jersey and Will Hoffman. Unlike the Fed, the GSEs actively hedge MBS holdings, shedding duration by paying fixed rates in swaps and using swaptions to manage the negative convexity and vega risks embedded in mortgages. That matters for swap spreads and for volatility, especially in the belly.

That’s why GSE MBS purchases don’t have to be huge to change the feel in rate markets. The post-Global Financial Crisis regime dulled the classic convexity feedback loop because the Fed held such a large amount of agency MBS and didn’t hedge it, while the GSEs shrank their portfolios. Trump’s directive risks bringing more of that regime back.

A recent note out of Goldman Sachs frames it cleanly: A $200 billion build could lift the active convexity-hedger footprint by about 25%. The street then starts front-running the mechanical flows — paying in selloffs, receiving in rallies — which makes breakouts more likely even if day-to-day ranges look calm, Goldman added.

Positioning makes the setup more precarious. JPMorgan already saw mortgage valuations as a “bit snug” before the announcement, while BofA flagged that rates market had recently added fresh belly shorts sitting against a backdrop of benchmark funds still overweight MBS versus IG.

That mix can keep the initial tightening sticky, but it also raises the odds of sharp reversals if the market decides the purchasing flows are slower, smaller, or more heavily hedged than hoped.

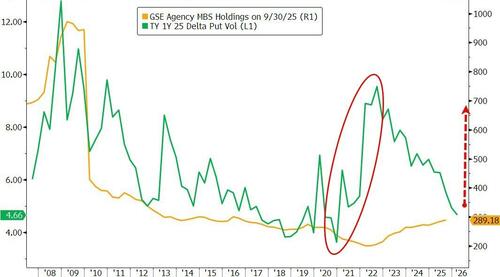

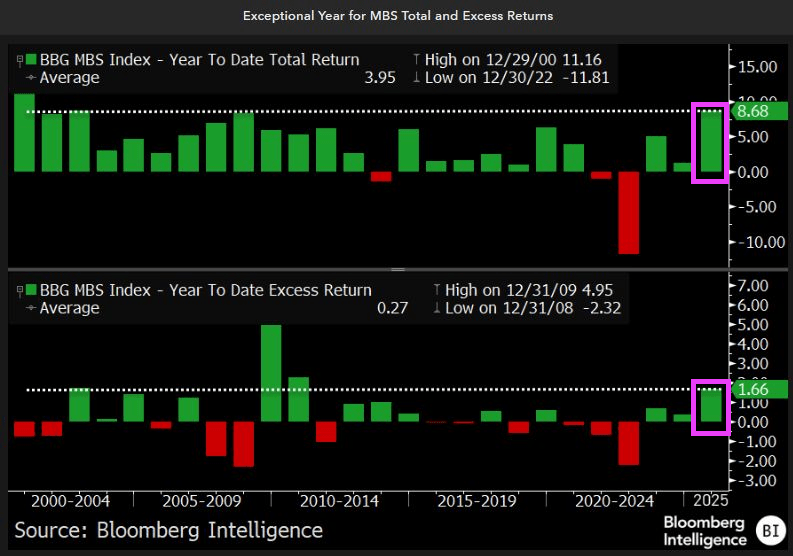

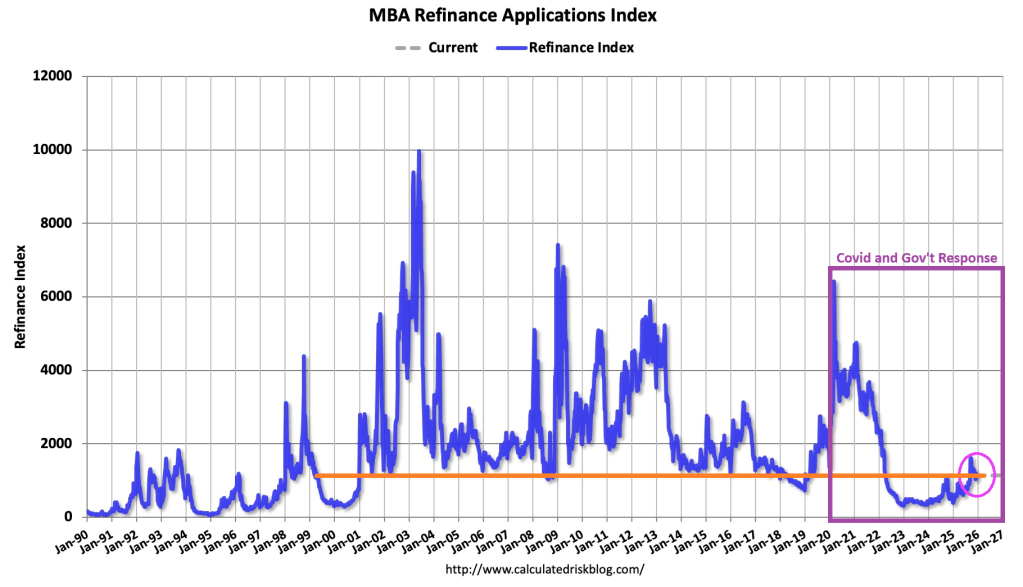

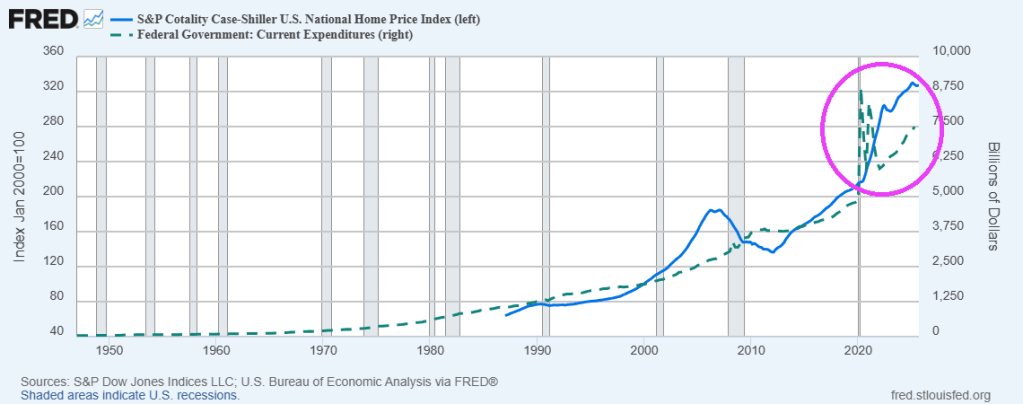

Fannie and Freddie’s retained portfolio are soaring along with the duration gap.

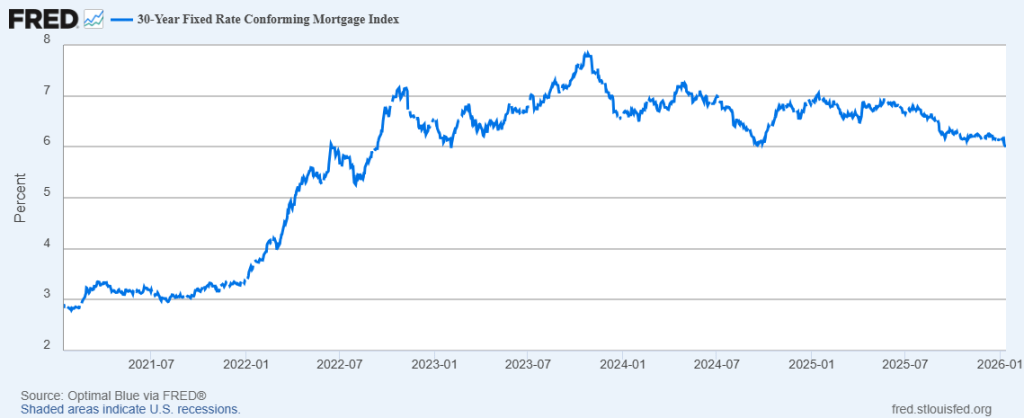

The effect on mortgage rates has so far has been negligible. The 30-year conforming mortgage just fell below 6% at 5.99%.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.