Case-Shiller home price indices are out today. The Case-Shiller NATIONAL home price index is up 1.5% on a year-over-year basis, but down -0.30% on a month-over-month basis).

Don’t worry. The Fed won’t stop printing money.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Case-Shiller home price indices are out today. The Case-Shiller NATIONAL home price index is up 1.5% on a year-over-year basis, but down -0.30% on a month-over-month basis).

Don’t worry. The Fed won’t stop printing money.

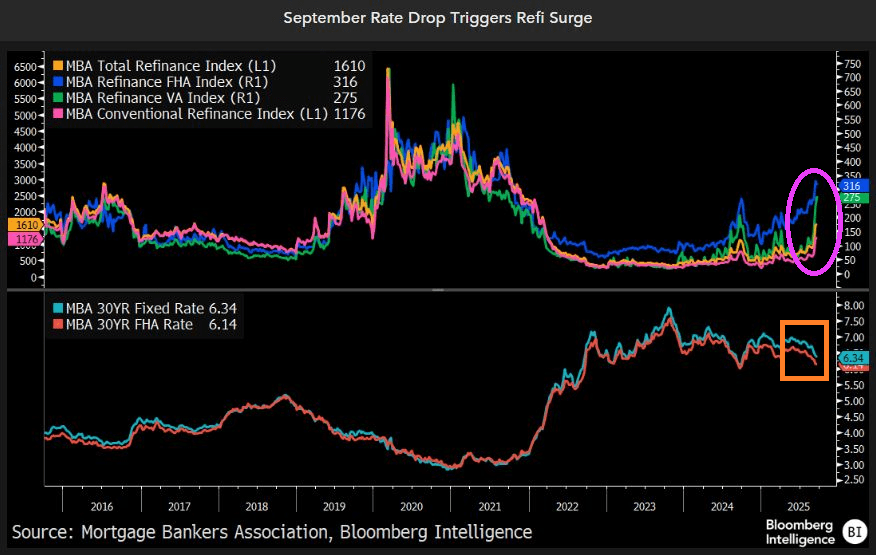

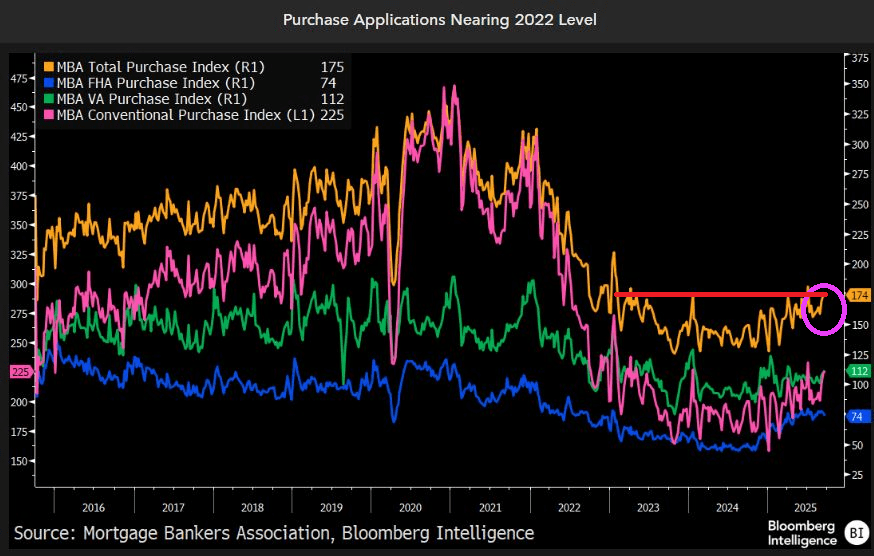

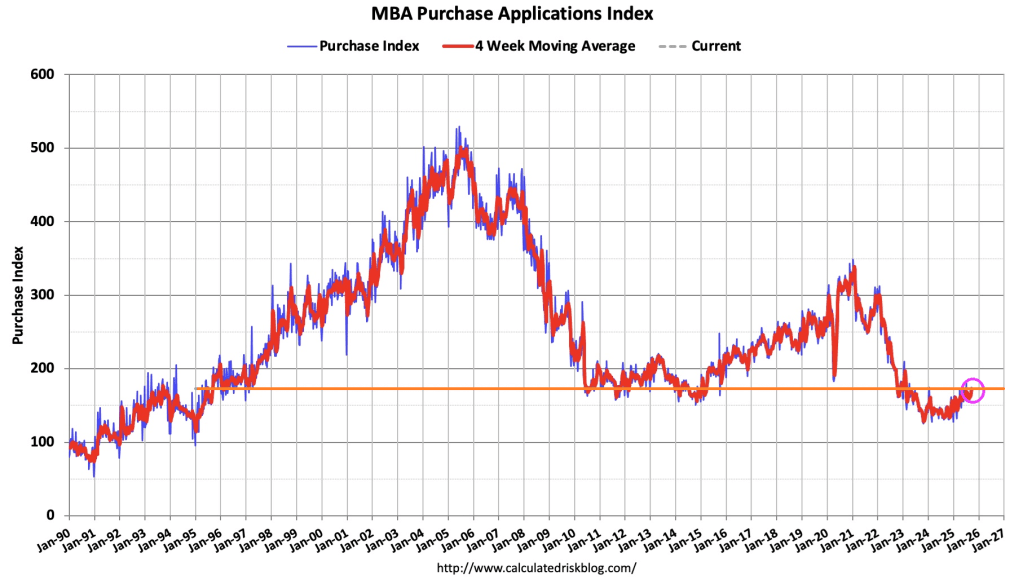

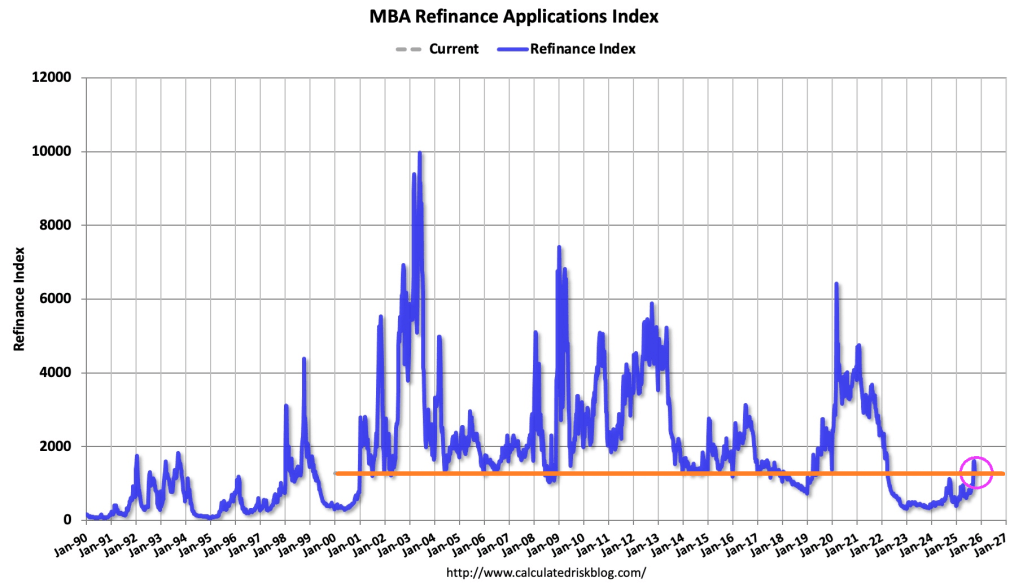

The September drop in mortgage rates is sparking the biggest boom in refinancings since the pandemic. Mortgage-refinancing applications have surged above the decade average, despite that period including the record-breaking refi boom of 2020-21 when rates fell to all-time lows. Purchase-loan demand has also rebounded to its best for this time of year since 2022, yet remains well below pre-pandemic levels.

Purchase demand (applications) nearing 2022 levels.

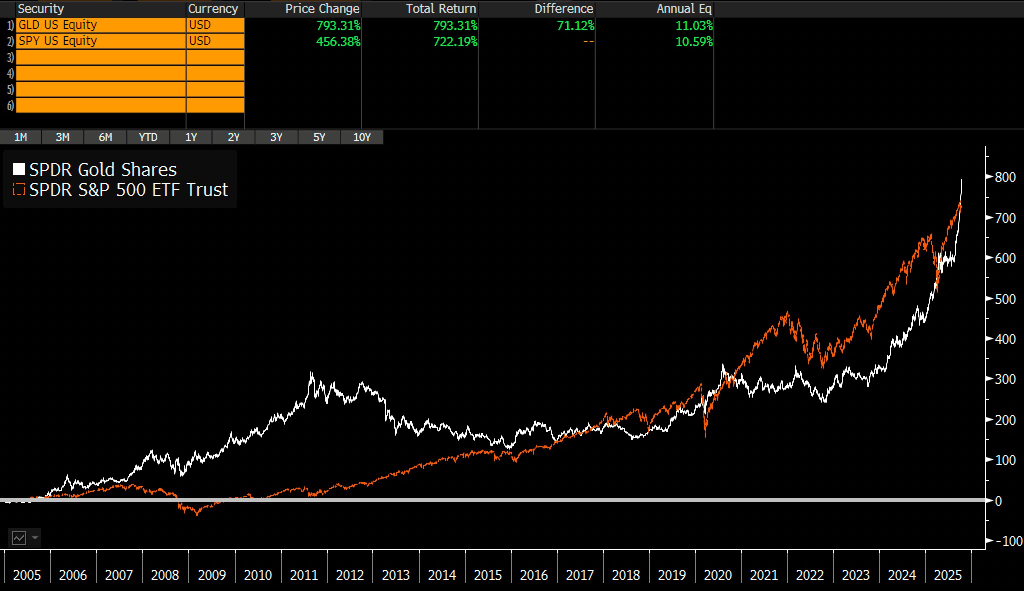

While not mortgage-related, gold is soaring!!

Thanks to Bloomberg’s Erica Adelberg for her amazing charts.

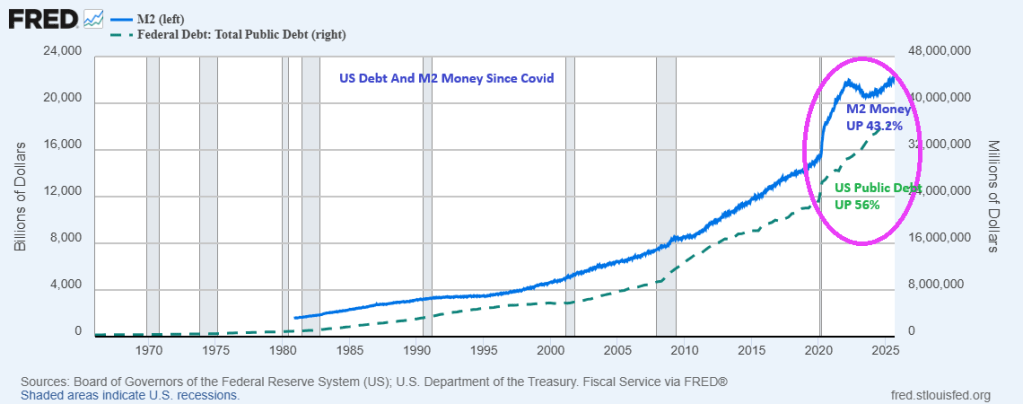

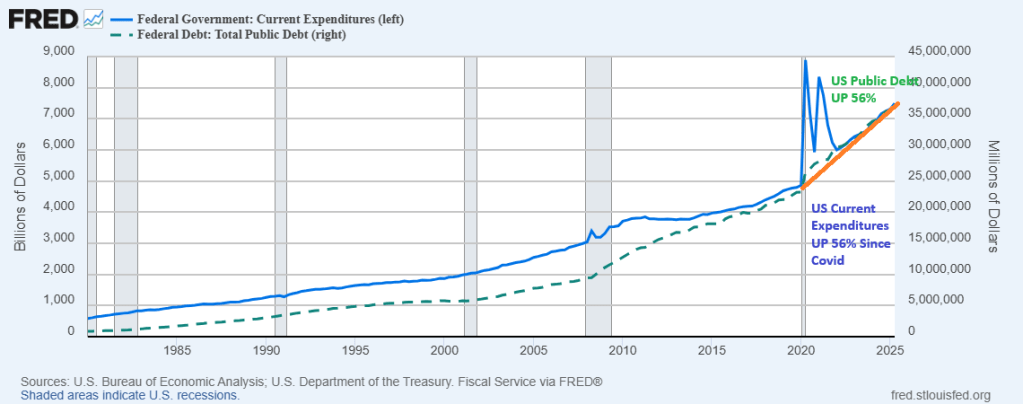

The Federal government is having a party! A spending party requiring massive growth in Federal borrowing AND Fed M2 money printing.

Federal borrowing has increased by 56% since Covid in 2020. And Fed M2 Money increased by 43.2% since Covid outbreak.

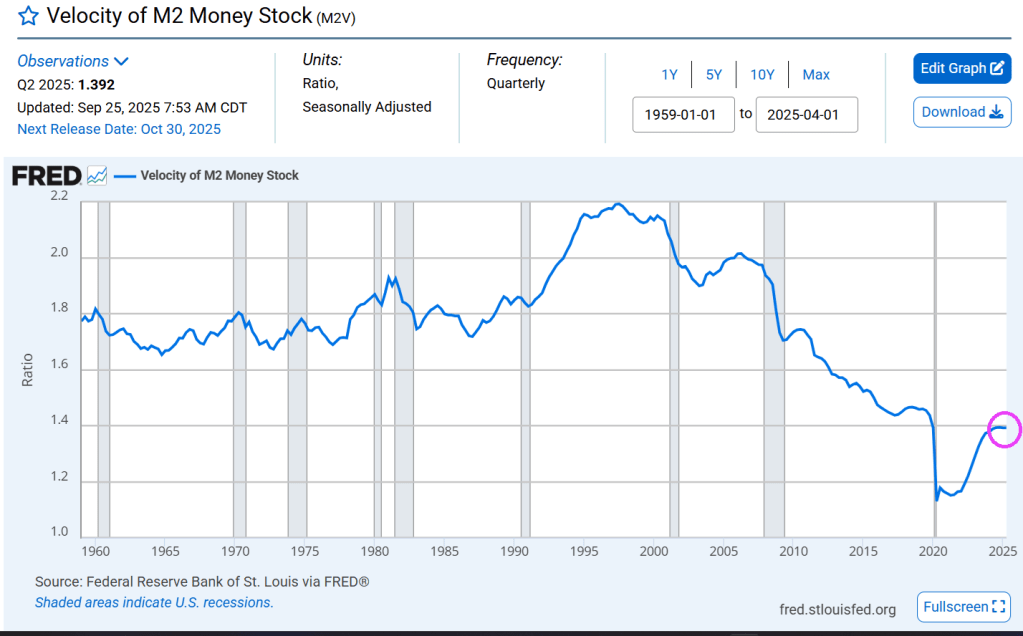

M2 money velocity (GDP/M2) is now at 1.392.

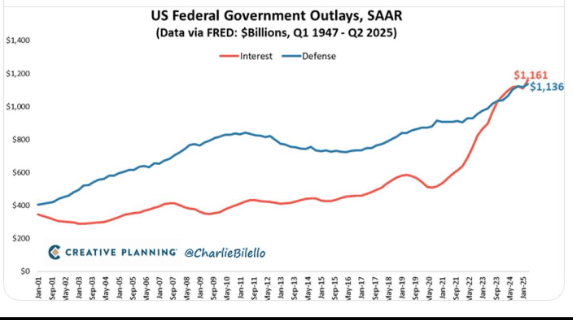

As of Q2, interest payments on the national debt exceeds spending on defense.

Despite being shut down by Democrats and Chucky Schumer, The Federal government and Federal Reserve continue to borrow and print money like crazy.

Can we ask the US House and Senate if they will ever return US Federal government spending to pre-Covid levels? Both US Federal government spending and public debt are up 56% since the Covid outbreak in 2020.

The answer is no. Politicians thrive on Federal spending.

Feelin’ stronger for the most part.

Mortgage applications decreased 4.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 3, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent higher than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 18 percent higher than the same week one year ago.

With mortgage rates on fixed-rate loans little changed last week, refinance application activity generally declined, with the exception of a modest increase for FHA refinance applications.

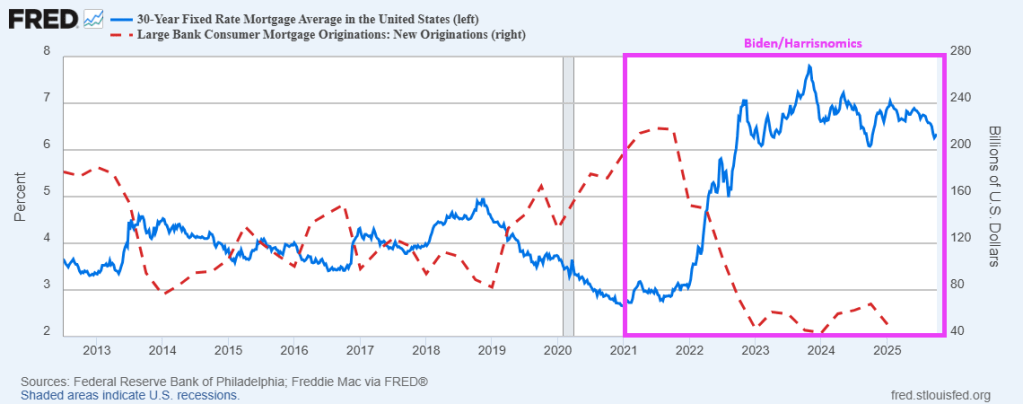

Mortgage demand dwindled since Covid and Biden/Powell and hasn’t recovered.

Shutdown!

Mortgage applications decreased 12.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 26, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 12.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 16 percent higher than the same week one year ago.

The Refinance Index decreased 21 percent from the previous week and was 16 percent higher than the same week one year ago.

Mortgage rates increased to its highest level in three weeks as Treasury yields pushed higher on recent, stronger than expected economic data. After the burst in refinancing activity over the past month, this reversal in mortgage rates led to a sizeable drop in refinance applications, consistent with the view that refinance opportunities this year will be short-lived.

Yes, the Federal government has shut down.

US home prices are downshifting to a lower gear.

Home prices across the top 20 cities in the US fell by 0.07% MoM (less than the 0.2% decline expected) – the fifth straight monthly drop in prices. This pulled the YoY price appreciation down to 1.82%, the lowest since July 2023.

The U.S. housing market continues its dramatic shake-up, with 7 cities seeing outright price declines YoY, lead by Tampa FL.

On the up side, Attom lists the following big gainers in price.

#10 – Wichita County, Texas

#9 – Whitfield County, Georgia

#8 – Tompkins County, New York

#7 – Fayette County, Pennsylvania

#6 – Schuylkill County, Pennsylvania

#5 – Jackson County, Michigan

#4 – Kankakee County, Illinois

#3 – Tom Green County, Texas

#2 – Saint Louis County, Missouri

#1 – Jasper County, Missouri

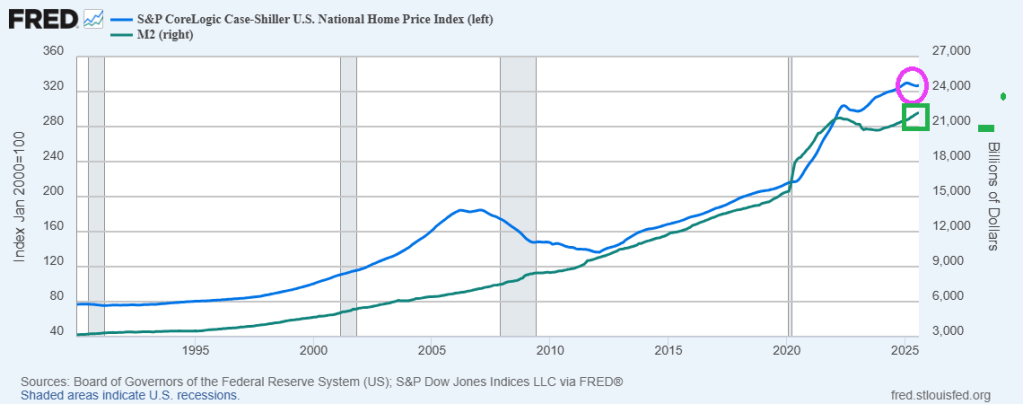

A simple model of national home prices? Try Fed money printing.

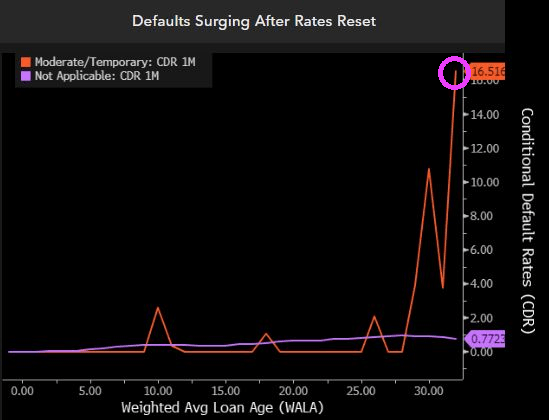

In addition to soaring sellers to buyers ratio in US housing markets, we now have surging mortgage default risk (CDR) after mortgage rate resets.

Did Powell and The Fed (aka, Jay Powell and the Blackhearts) wait too long to cut rates?

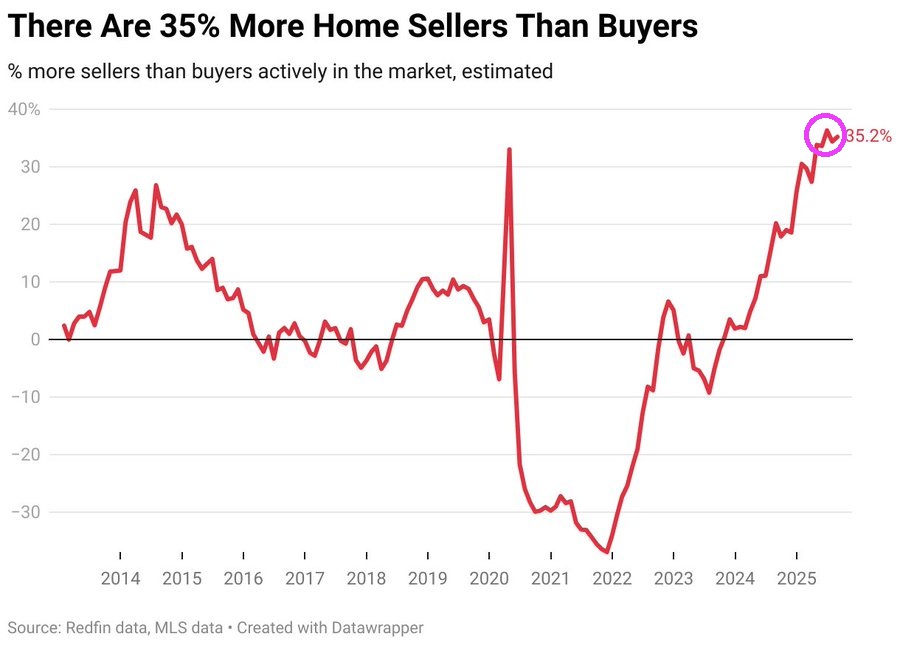

Here is the soaring ratio of home sellers to buyers. OOOGG!!!

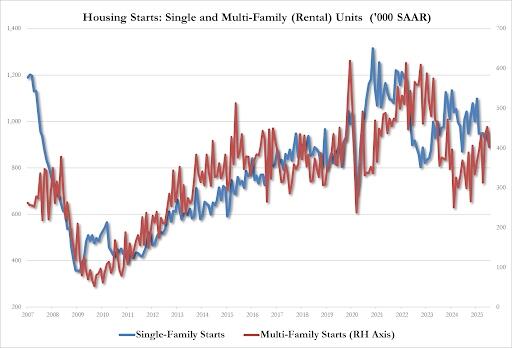

It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

Housing starts:

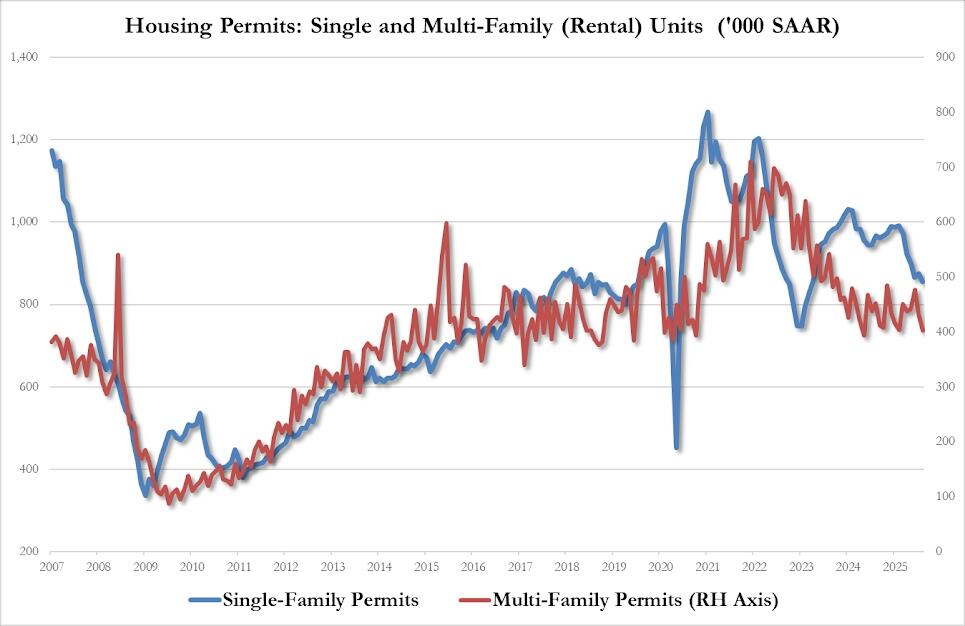

Housing permits?

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

Participants in the mortgage market are hoping for relief in the mortgage market when The Fed lowers rates tomorrow.

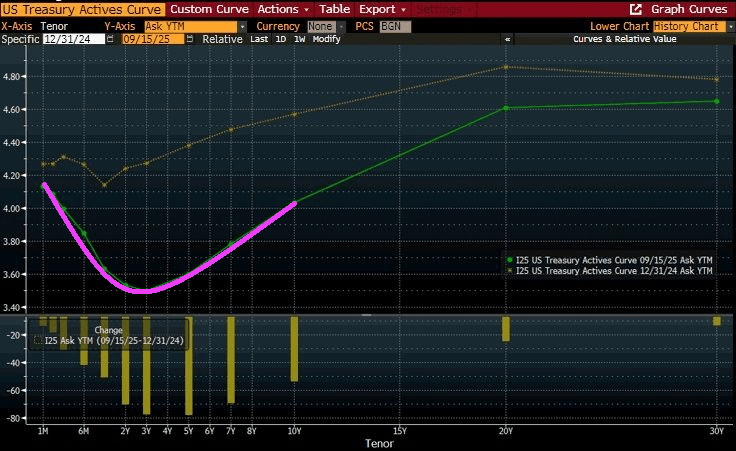

But the reality is the the bond market is expecting declining short-term rates, but not much change at the 10-year tenor.

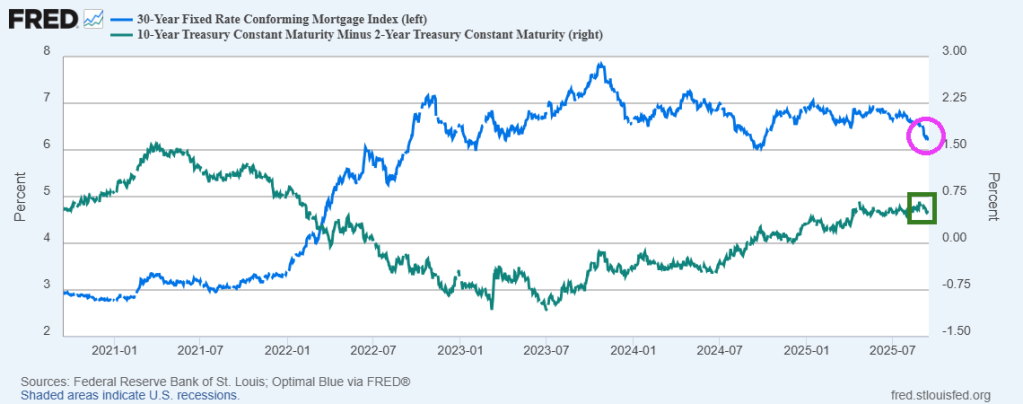

Mortgage rates have fallen since October 23, 2023 as the yield curve has gradually steepened.

So don’t be surprised if The Fed cuts rates tomorrow and there is little or no reaction in mortgage rates.

{kind=link}

{kind=link}

You must be logged in to post a comment.