October STICKY core inflation is still up 4% YoY (year-over-year)

Core CPI rose 0.3% MoM (as expected) which pushed it up 3.3% YoY (not even close to the 2% mandate)…

Source: Bloomberg

There has not been a single monthly decrease in core consumer prices since Biden too office.

dddd

Between The Fed’s insane monetary policy and Biden/Harris insane fiscal policies, we are living in a world where Ray Bradbury’s novel Fahrenheit 451 becomes a reality. Instead of books burning, it is the US Dollar burning.

The US is the expensive tower of power … but it should be cheap. Getting rid of coal power was idiotic and The Left’s fear of nuclear power is laughable.

Europe’s fertilizer plants, steel mills, and chemical manufacturers were the first to succumb. Massive paper mills, soybean processors, and electronics factories in Asia went dark. Now soaring natural gas and electricity prices are starting to hit the US industrial complex.

On June 22, 600 workers at the second-largest aluminum mill in America, accounting for 20% of US supply, learned they were losing their jobs because the plant can’t afford an electricity tab that’s tripled in a matter of months. Century Aluminum Co. says it’ll idle the Hawesville, Kentucky, mill for as long as a year, taking out the biggest of its three US sites. A shutdown like this can take a month as workers carefully swirl the molten metal into storage so it doesn’t solidify in pipes and vessels and turn the entire facility into a useless brick. Restarting takes another six to nine months. For this reason, owners don’t halt operations unless they’ve exhausted all other options.

At least two steel mills have begun suspending some operations to cut energy costs, according to one industry executive, who asked not to be identified because the information isn’t public. In May, a group of factories across the US Midwest warned federal energy regulators that some were on the verge of closing for the summer or longer because of what they described as “unjust and unreasonable” electricity costs. They asked to be wholly absolved of some power fees—a request that, if granted, would be unprecedented.

Michael Harris, whose firm Unified Energy Services LLC buys fuel for industrial clients, says costs have risen so high that some are having to put millions of dollars of credit on the line to secure power and gas contracts. “That can be devastating for a corporation,’’ he says. “I don’t see any scenario, absent explosions at US LNG facilities’’ that trap supplies at home, in which gas prices are headed lower in the long term.

EIA Average Electricity Cost Cents

EIA cost data chart by Mish

EIA Cost Data January 2021 vs May 2022

Residential: 12.69 to 14.92

Commercial: 10.31 to 12.14

Industrial: 6.39 to 8.35

Transportation: 9.61 to 10.79

All: 10.36 to 12.09

Those prices are through May 2022. Much electrical energy comes from natural gas.

US Natural Gas Futures

US Natural Gas Futures courtesy of Trading Economics

US gas prices fluctuated wildly in June and July. I suspect the average price is 7.33 or so for both months. Things are decidedly worse in Europe.

EU Natural Gas Price

US Natural Gas Futures courtesy of Trading Economics

From 25 or even 50 to 200 is one hell of a leap. It’s somewhere between 300% and 700% depending on your starting point vs 100% or so for the US.

Let’s now check the latest PPI data for a look at where things are and more importantly headed.

PPI Electrical Power Index 2020-Present

PPI data from the BLS, chart by Mish

From pre-pandemic to January of 2021, the PPI electrical power index was flat. It has since surged on a relatively steady pace.

From May to July the index went from 231 to 238. That tacks on another three percentage points since the EIA report.

PPI Electrical Power Index 1991-Present

PPI data from the BLS, chart by Mish

Long Term Trend

The long-term trend does not exactly look pretty.

And as Bloomberg noted, Century Aluminum Co. says it’ll idle the Hawesville, Kentucky, mill for as long as a year, taking out the biggest of its three US sites.

The beer industry uses more than 41 billion aluminum cans annually, according to a Beer Institute letter to the White House dated July 1.

“These tariffs reverberate throughout the supply chain, raising production costs for aluminum end-users and ultimately impacting consumer prices,” according to the letter signed by the CEOs of Anheuser-Busch, Molson Coors, Constellation Brands Inc.’s beer division, and Heineken USA.

This letter to the president comes amid the worst inflation in more than 40 years and just months after aluminum touched a multi-decade high. Prices for the metal have since eased significantly.

Whatever victory beer makers and drinkers may have with aluminum prices may not last with US aluminum plants shutting down.

Then again, the cure for everything is likely to be a huge recession.

Zero Consumer Inflation

I am pleased to report there was no consumer inflation in July.

The CPI report resulted in a nonsensical Twitter debate on the meaning of zero. For the record, assuming you believe the numbers, there was indeed zero inflation month-over-month.

The accurate rebuttal is: One month? So what?

Moreover, zero is not as good as it looks. All of it was due to a 7.7 percent decline in the price of gasoline. And year-over-year inflation was a hot 8.5 percent.

Meanwhile, rent and food keep rising and the price of rent will be sticky. Gasoline is more dependent on recession and global supply chains.

The above reports and this one industrial costs puts a spotlight on the silliness of the Fed’s focus on consumer inflation as if that’s all that matters.

The Fed has blown three consecutive bubbles trying to produce two percent consumer inflation while openly promoting raging bubbles in assets and missing the boat entirely on industrial matters.

I just watched Dennis Quaid in “Reagan”. Excellent film. But it reminded me of how Reagan sank the Soviet Union: by outspending the Soviet Union on the arms race. It worked! The Soviet Union, hamstrung by grossly inefficent central planning, couldn’t keep up and collapsed under President George H.W.Bush.

Fast forward to today. Starting with Barack Obama and Joe Biden in 2009, following the financial crisis in 2008. The Federal government ramped up Federal spending, and Federal debt. While The Federal Reserve, the hand maiden to the Federal government, ramped up M2 Money supply.

“You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before.” – Rahm Emmanuel

Then came Biden/Harris who drove Federal debt and spending to absurb level (orange box). Like the financial crisis, fans of big government and big government spending will utter the word “Covid.” But that is gross misleading. Covid was the excused for wild spending and debt issurance. And MORE Fed money printing. It’s almost as if Obama/Biden/Harris were replicating Reagan’s bankrupcy strategy in reverse! That is, collapsing the US from within.

As we are all painfully aware, the US Debt now stands at $36 TRILLION with $220.3 TRILLION in unfunded liabilities. Too bad total US Assets are only $217 TRILLON.

Do I believe that Obama/Biden/Harris want a “Great Reset”? Absolutley. Just look at our fiscally unsustable open borders and our politiicians blatanly lying to us. :Like Ohio’s Senator Sherrod Brown who brags about his helping write the border bill that would reverse Trump’s deportations and fund the speeding up of immigration.

The Presidential and Vice Presidential debates thus far feature weak moderators asking lame questions. For example, there are still 97 hostages stll held by Hamas and what would the candidates do to get them released? (Hint: Trump/Vance would have sensible responses. Harris would just laugh and say she was raised in a middle class family and Walz would look like a deer in the headlights. Then we have national debt of $36 trillion, $271K per taxpayer.

But the hidden bomb that will never be discussed is unfunded liabilities (entitlements) such as Social Security and Medicare. Currently, unfunded liabilities are $219 TRILLION or $650K per citizen.

Of course, Biden/Harris have let the southern border wide open to criminals and uneducated Democrat voters who will voter for MORE entitlements.

So, when will the lame debate moderators ask HARD questions? And can Harris attempt to answer one hard question without laughing or falling back on lame “I was raised in a middle-class household.” etc.

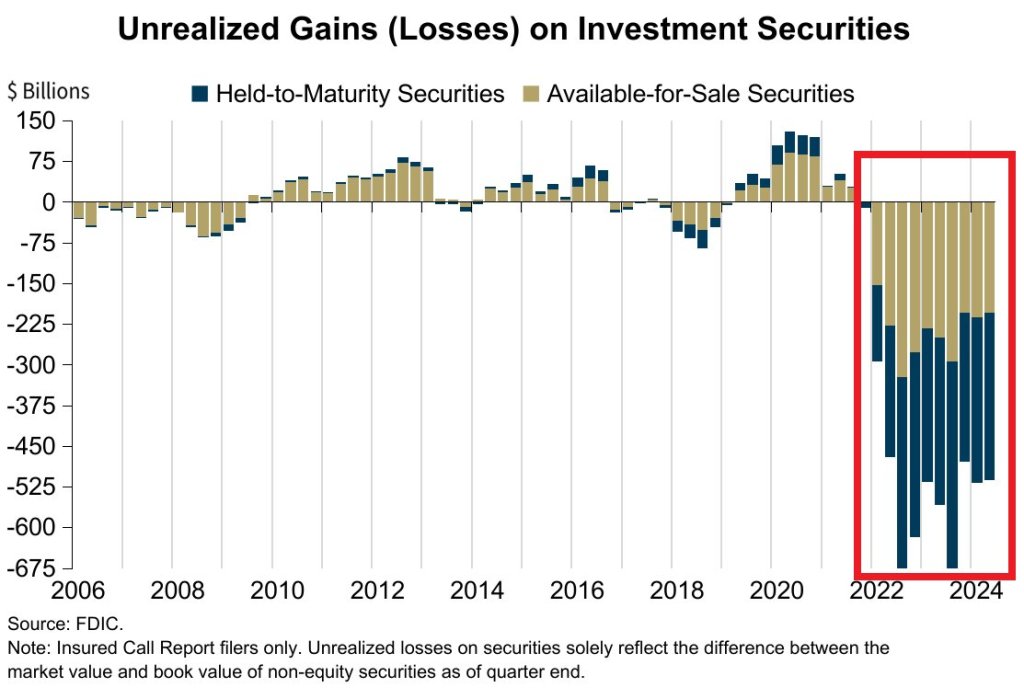

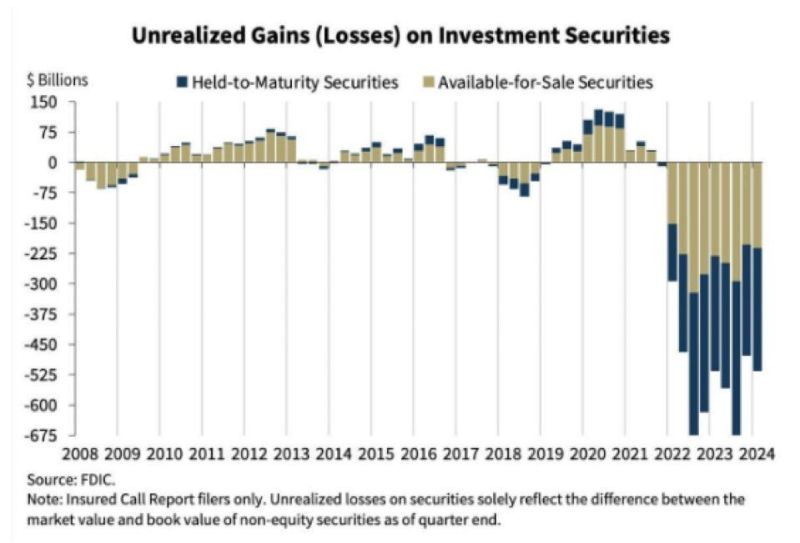

Q2 marks the 11th STRAIGHT quarter of unrealized losses on investment securities for banks, a streak never seen before. The number of banks on the FDIC Problem Bank List increased to 66 and represents 1.5% of total.

This is in addition to price Increases over last 4 years… CPI Medical Care: +7.8% CPI Apparel: +12.7% CPI Used Cars: +18.3% CPI New Cars: +20.5% CPI Food at home: +21.4% CPI Shelter: +23.4% CPI Food away from home: +25.4% CPI Electricity: +29.8% CPI Gas Utilities: +34.9% CPI Transportation: +38.8% US Home Prices: +48.0% CPI Auto Insurance: +52.4% CPI Gasoline: +53.5% CPI Fuel Oil: +54.9%

Don’t spill the wine, its too expensive under Biden/Harris/Powell.

These are the essential pillars of “21st century socialism” and the radical left Peronism that obliterated Argentina. These are also the main elements of the economic plan presented by Kamala Harris and the Democratic Party. Undoubtedly, this is the most radical socialist economic plan ever announced by the Democrats.

According to the Committee for a Responsible Federal Budget (CRFB), Harris’s proposals will cost $1.95 trillion over 10 years. However, it emphasizes that if certain measures become permanent, this figure could increase to $2.25 trillion.

The Harris campaign has stated that these costs will be offset by a classic excuse of socialism in any election: “higher taxes on corporations and high earners.” This is, obviously, ludicrous, because there is no revenue measure that will cover the already bloated $2 trillion annual deficit and an added $2 trillion. The mantra of “higher taxes for the rich” always means higher taxes and more inflation, a hidden tax, for you.

The Congressional Budget Office (CBO) has already warned of the fiscal disaster of the United States, with an annual deficit of 6% of GDP. Despite not accounting for a recession and projecting record tax revenues from 2024 to 2034, the CBO predicts an explosion in the budget deficit from $1.9 trillion to $2.8 trillion by 2034, even before factoring in Harris’s new spending plan. This means that the adjusted deficit will rise above 6.9 percent of GDP by 2034, almost twice the average of 3.7 percent over the previous 50 years.

Following the Harris plan, the United States public debt will likely increase by $24 trillion in a decade. As I have explained, there is no set of revenue measures that can bring $2 trillion per year in additional tax receipts, and tax hikes will harm both investment and growth.

An economy that generates an annual deficit of 6 percent of GDP to achieve a mere 2 percent annual growth is already on a dangerous path, and Harris’ plan would make it even worse.

Kamala Harris promises to cut inflation by spending and printing more money, reducing competition, and attacking businesses. It has never worked and never will because it is upside-down economics. Welcome to the US “Peronism.”.

Imagine all those United States citizens who have escaped Latin American or European economies impoverished by interventionism to find a better opportunity in the United States only to find that the same policies will be implemented by Harris.

The narrative of price gouging and greedflation is simply false. In 2023, profit margins in the grocery industry hit the lowest level since 2019, at 1.6%, according to the IMF. Corporations, even if they were stupid and reckless, cannot make all prices rise constantly. Competition would eat away at their market share; newcomers would eliminate them, and aggregate prices would fall. Furthermore, stores and businesses cannot make aggregate prices soar, maintain the increase, and consolidate it, which is the measure of inflation (CPI) we read every month. The only thing that can make all prices rise and continue increasing at a slower pace is printing money and eroding the purchasing power of the currency.

The only thing that can make aggregate prices rise constantly is the destruction of the purchasing power of the currency, which comes from massive government spending and printing currency to disguise fiscal imbalances.

Kamala Harris and her team know that their spending plan will make the national debt soar and that price controls do not reduce prices. In fact, these should not be called “price controls” but “limits to competition.” If corporations were the cause of inflation and price controls were the solution, Peronist Argentina would have enjoyed the lowest inflation in the world in the past decades.

Harris’ proposals to forgive debt are profoundly anti-social. They do not forgive any debt; they just add it to the national debt and make you pay for it. This enormous increase in public debt will be a burden for every American, particularly the poorest, with persistent inflation and lower real wages. US citizens have already endured negative real wage growth since January 2021, when Biden took office, according to the Federal reserve of St Louis. Expect worse.

Why does Harris promote the same policies that have failed everywhere? Promising free stuff and blaming others for the negative consequences is the defining strategy of socialist politicians.

Are you surprised to see how Germany, France, and other historically rich nations slump into stagnation, high debt, persistent inflation, enormous taxes, and the destruction of the middle class? Those policies are what Harris is promising. Who benefits? The vast government and its surrounding corporations reap the benefits.

Many people hold the belief that a nation cannot be considered socialist if it contains private companies. It makes no sense. State control does not limit itself to capital ownership but also to the imposition of increasingly restrictive laws, regulations, and confiscatory taxes. In fact, the government likes to absorb most of the wealth created by the private sector without the inconvenience of managing the businesses. Huerta de Soto defines socialism as “any system of institutional, methodical aggression against the free exercise of entrepreneurship” and that is precisely what Harris promises.

Higher taxes and more debt.

The government will print money to provide subsidies in a currency that is constantly losing value. It will blame stores and businesses for inflation. Interventionist policies will continue to erode the private sector. And they will repeat.

The makers of these policies are aware that they will negatively impact the economy, yet they will also engender a substantial number of enslaved citizens who rely on the government and must abide by its decisions. Voters see an alleged tsunami of free money but ignore the fact that they will pay for it through higher inflation, lower real wages, and diminishing opportunities for small businesses and families.

Yes, under Obama/Biden, then Biden/Harris,

The Harris team believes deficits do not matter and that the Federal Reserve can always disguise any budget imbalance. However, cracks have already appeared. Persistent inflation is the consequence of years of excessive spending and monetization. The next step is the risk of losing the US dollar as the world reserve currency when the world stops accepting the ever-increasing debt.

Under Obama/Biden and Biden/Harris, we have seen massive money printing and devaluation of the US Dollar. Trump/Pence too, but they were nailed with Covid. And the Democrat shut down off schools and local economies.

But all Harris (America’s Eva Peron) wants to do is dance. And not answer serious questions.

After watching the Democrat hate fest last night (Aka, the Democrat National Convention), I was not shocked that the DNC platform looked like a playbook to destroy the US economy. High taxes, endless spending, more regulations, etc. Not a word about the staggering side of the US debt load … with Harris’ economic plan projected to add a whopping $25 trillon in debt to the already massive $35+ trillion debt load.

And not a mention that US interest payments on the national debt already exceeds defense spending. And is booming!

Of course, Harris’s economic vision is a continutation of Biden’s disastrous visions (which are Obama’s vision of US obliteration). Most politicians in Congress are millionaires (including Bernie Sanders) and won’t suffer from their insane “progressive” policies. Watching last night’s DNC hatefest was like watching nasty 2nd graders having a party.

Of course, the drove of anti-American, anti-properity speakers spewing venom (I hate Hillary’s flat-tone speaking style) like Hillary, Jaime Raskin (aka, Rasputin), AOC, etc. all failed to acknowledge to acknowledge the already monstrous size of the US debt ($35+ trillion) or the massive size of the unfunded promises ($218+ TRILLION). Of course not.

The handle the staggering interest payments that will crowd out other spending, The Federal Reserve will be forced to lower rates.

Of course, Democrats will wheel out “economists” like Robert Reich who say that the debt doesn’t matter.

“There’s a big difference between fair pricing in competitive markets, and excessive prices unrelated to the costs of doing business,” the Harris campaign wrote in a statement, adding, “Americans can see that difference in their grocery bills.”

The Harris campaign said the vice president will unveil the new federal proposed ban on Friday at a campaign rally in the battleground state of North Carolina as part of a broader economic policy platform. The proposal will ensure food companies can’t exploit consumers to increase profits, according to CBS News, citing Harris-Walz campaign officials.

Harris’ policy speech will also call on the Federal Trade Commission and state attorneys to examine corporations violating price-fixing rules. Her remarks are expected to echo Biden’s actions and rhetoric, especially with his war against meat processing companies that he alleges are responsible for higher burger prices at the supermarket.

VP Harris’ campaign argues that lowering Americans’ costs is a function of socialist-style price controls. Yet this is the quickest way to understand that Harris’ economic team has no actual understanding of inflation.

Heritage Foundation’s EJ Antoni explained, “Here’s your “price gouging” narrative: average costs paid by businesses have risen just as much as costs charged to consumers – if businesses are being “greedy,” they’re doing it all wrong…”

Instead of curbing out-of-control government spending, which debt rises $1 trillion every 100 days, and understanding that monetary inflation driven by the Federal Reserve’s money creation is the root cause of inflation, Harris deflects the actual problem: The Fed. She instead goes after big corporations for ‘illegal price gouging.’

Here’s a snippet of Money Metals Midweek Memo’s Mike Maharreycommenting on Harris’ proposed price-fixing ban on big food companies:

The second “dumb” idea Maharrey discussed came from Vice President Kamala Harris, who was recently asked about her plan to combat inflation. Maharrey criticized her response, which he described as “word salad,” pointing out that she merely acknowledged the problem without offering any concrete solutions. Instead, she promised to take on “big corporations” engaging in “illegal price gouging,” corporate landlords, and big pharma.

Maharrey argued that Harris’s approach misses the root cause of inflation, which is monetary inflation driven by the Federal Reserve’s money creation. He cited the July budget deficit data, revealing that the Biden administration spent another $574 billion in just one month, running a $243 billion deficit. Maharrey emphasized that inflation is not caused by corporate greed but by the government’s excessive spending and borrowing.

“Price inflation is a symptom of monetary inflation, which has everything to do with money creation by the Federal Reserve,” Maharrey explained. He warned that Harris’s proposed policies, including price controls, would likely lead to shortages and exacerbate the problem rather than solve it.

“We are no longer talking about hypothetical communism, we are talking about two straight up communists who want to institute a federal price ban on food and a federal minimum wage that is going to make every corporation go out of business.

…

Voting for communism is not the solution to your precious feelings.”

Grocery stores have a 3-4% profit margin if they are lucky.

Kamala Harris, despite being VP for almost 4 years, is going to annouce her plans for taming inflation. Why doesn’t she do it now?? What Harris can’t control is The Federal Reserve that is losing money at breakneck speed.

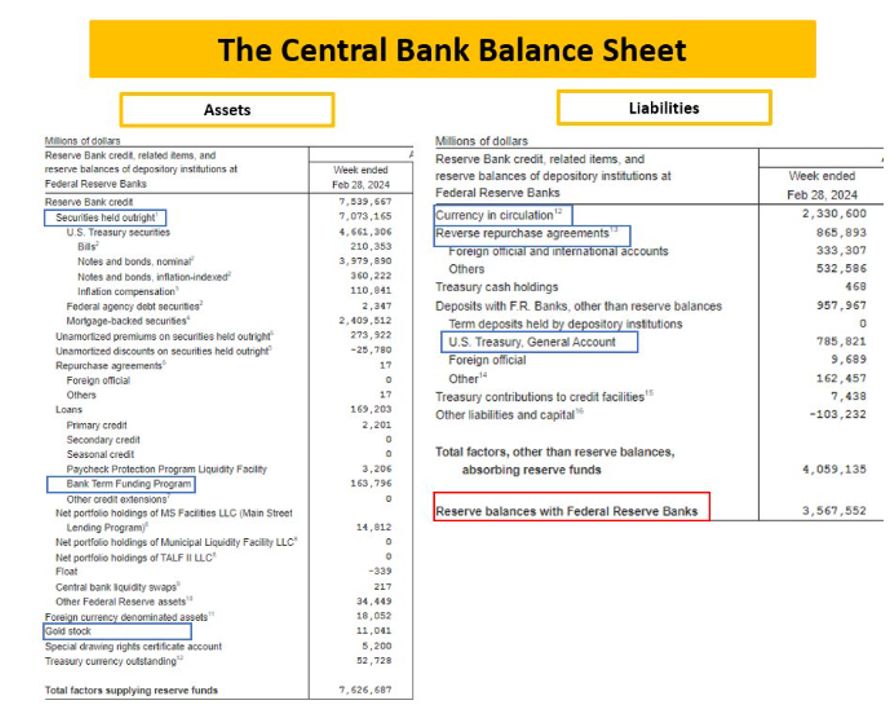

Here is The Fed’s balance sheet.

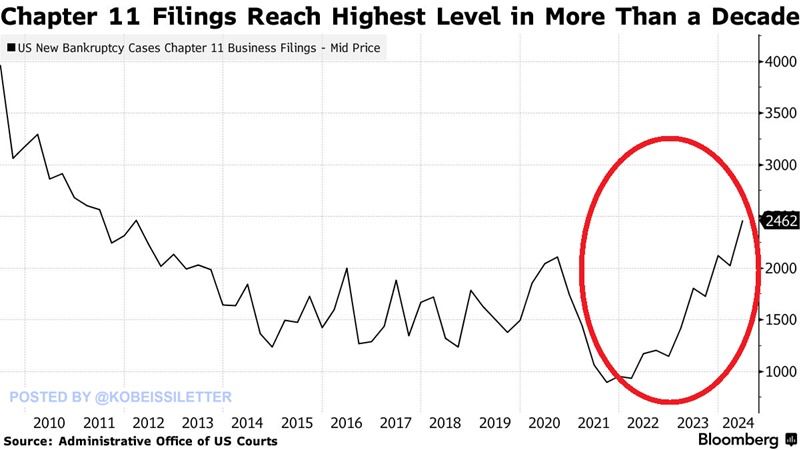

I shudder to think what Harris will propose to solve the highest bankrupty (Chap 11) rate in 13 years. Probably more Bidenomics (big wealth transfers to large corporations/donors).

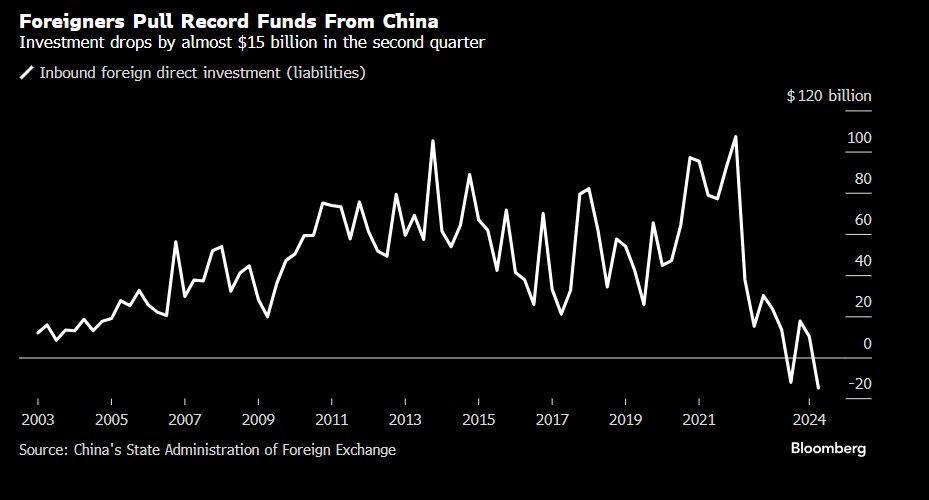

Meanwhile, foreigns pulled a record amount of funds from ailing China.

Kamala Harris will say anything to get elected, then fall back on her Communist agenda.

Remember the TV show “The Biggest :Loser”? That show was about weight loss.

Now The Federal Reserve has posted a record loss of $114 BILLION IN 2023.

The cause of the loss? Massive expansion of The Fed’s balance sheet coupled with rising interest rates. The two year track record of The Fed is truly appaling. With a bloated balance sheet, rising interest rates have caused staggering losses.

{kind=link}

You must be logged in to post a comment.