While the Chinese Wuhan virus (aka, the Fauci Flu) has plagued the world, another Chinese “export” is also suffering what is known as contagion: China’s real estate sector.

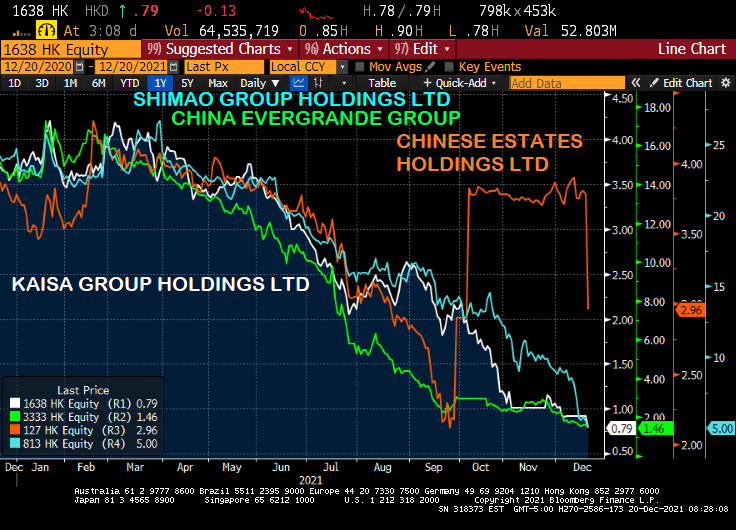

Real estate companies Evergrande, Kaisa, Shimao and Chinese Estates are falling like a rock today.

But it has been a steady decline since Q1 2021 except for Chinese Estates. But they have resumed their death dive.

On the debt side, Evergrande is down to 18.856 while Kaisa has lost less (but still quite a bit) and Shimao’s bond look almost like a good investment, relative to Kaisa and Evergrande. But they are all sucking wind. Maybe they all have the Fauci Flu?

Let’s see if this latest Chinese “export” washes ashore in the USA.

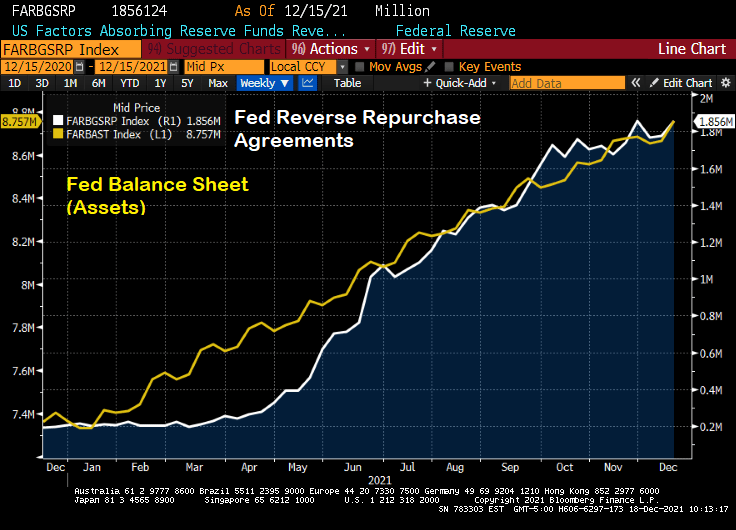

I love listening to Fed talking heads (or Fear The Talking Fed). They mostly seem to acknowledge that inflation is a problem and that the excessive monetary stimulus should be reduced.

But then I see the chart of The Fed’s balance sheet and The Fed’s reverse repo operations.

Then we have Federal Reserve Governor Christopher Waller saying that Th Fed could start raising interest rates as early as its March 15-16 meeting, after deciding to end asset purchases sooner than planned. My question is … why wait until the March meeting?

Is it fear of the Omincron Variant (which sounds like a Frederick Forsyth thriller)? Does The Fed not want to rock the boat prior to the Christmas season? The US is at or near full employment, so what is the real reason for delaying a rate increase until March or June? Or the fear that Congress won’t pass Biden’s Build Back Better Act?

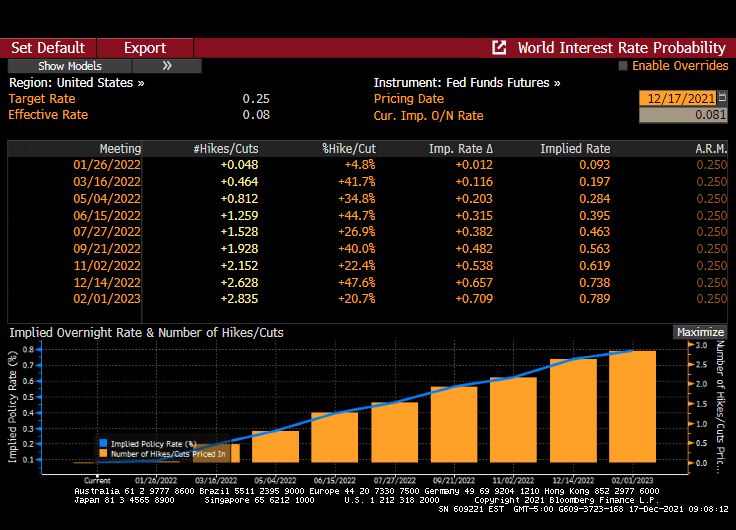

Fed Funds Futures infer that one rate hike will occur at the June Fed Open Market Committee (FOMC) meeting and one at the November meeting.

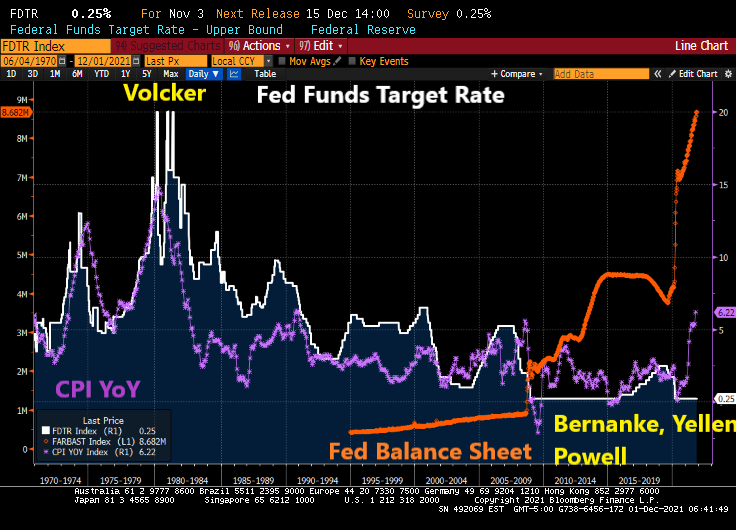

The Fed’s new theme song is “Hold That Tiger” meaning that despite soaring inflation rates, The Fed kept their target rate at 0.25%. Way to really pull a Volcker and raise rates to choke off inflation. … NOT!

However, The Fed doubled the pace of tapering to $30 billion a month. Median forecast shows three rate hikes in 2022, three in 2023.

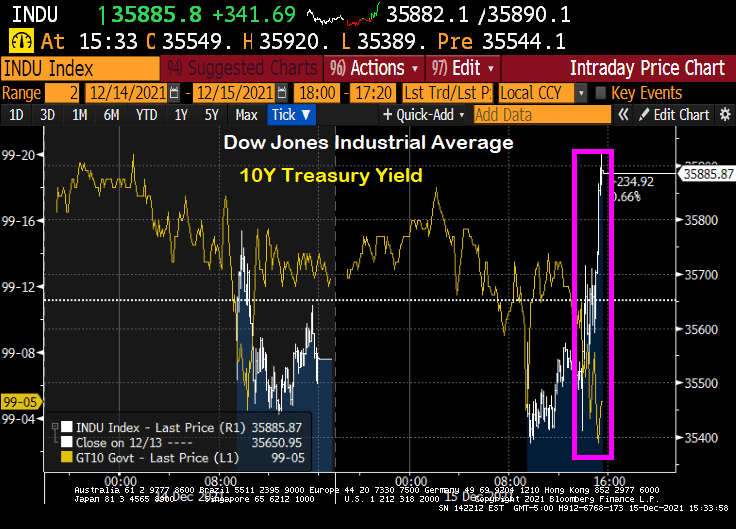

The reaction? The Dow rose 363 points as of 3:36pm EST and the 10-year Treasury yield rose a measly 1.9 bps as markets celebrate The Fed DOING NOTHING TO CURB INFLATION.

If price stability is squandered, financial stability is put at risk. If financial stability is lost, the economy is imperiled and the social contract is threatened.

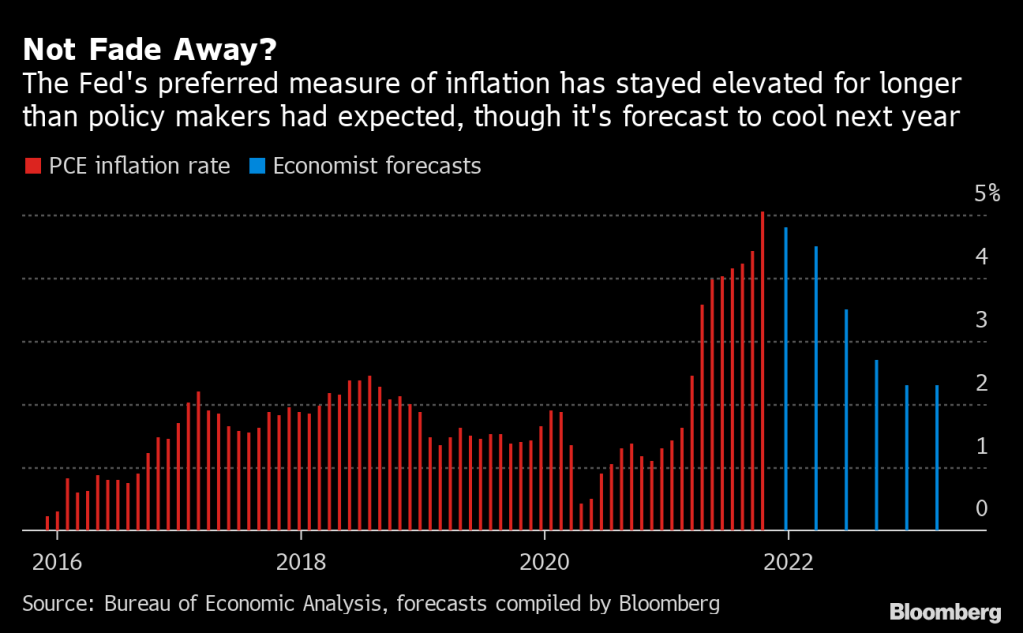

During the past several quarters, U.S. inflation has surged—now running about triple the Federal Reserve’s 2% target. The surge in prices is unlikely to reverse on its own. The longer that prices are unstable, the greater the challenge to the conduct of macroeconomic policy. The last thing the country needs is its third major economic upheaval in a decade and a half.

The consequences of inflation—and the attendant risks—have long been understood. In 1898 economist Knut Wicksell explained: “Changes in the general level of prices have always excited great interest. Obscure in origin, they exert a profound and far-reaching influence on the whole economic and social life of a country.”

I agree with the op-ed, but as Paul Harvey liked to say, “And now for the rest of the story.”

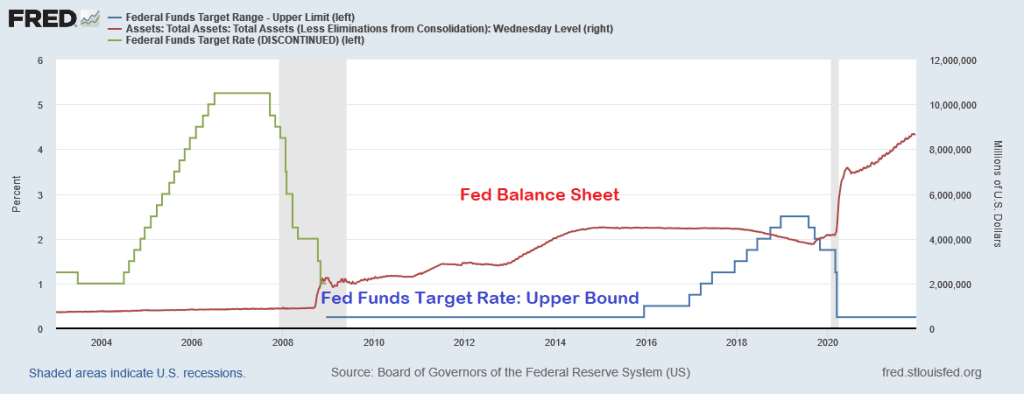

The Federal Reserve is only half of The Federal government “Stimulypto.” Starting in late 2008, The Fed crashed their target rate to 25 basis points and began their quantitative easing (QE) program where The Fed purchased Treasuries and Agency Mortgage-backed Securities (MBS) amongst other assets. Notice in the chart below that QE was adjusted, but never went away and The Fed’s target rate only was increased once before Trump’s election as President, then raised eight times then decreased five times. And no rate increases under Biden. So The Fed scorecard is Obama/Biden: 1 rate increase. Trump: 13 rate changes. And The Fed’s balance sheet has gone bananas since the COVID outbreak.

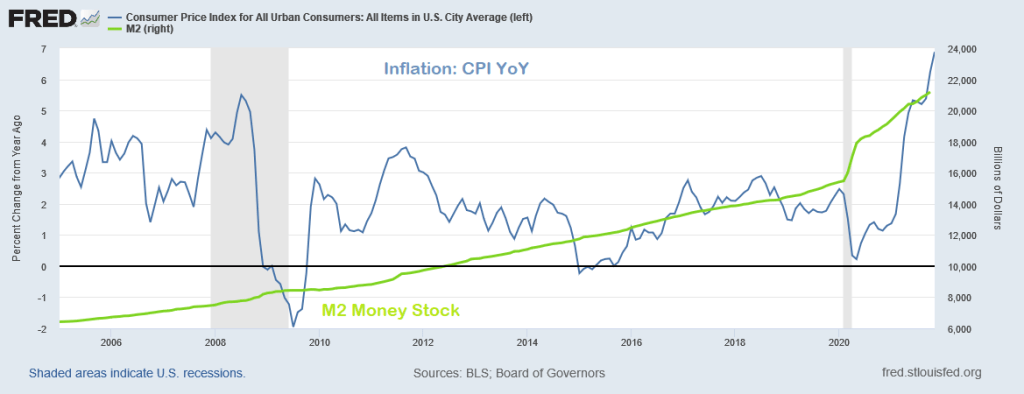

Inflation, as measured by the Consumer Price Index (CPI) didn’t really take-off until March 2021 as a result of STIMULYPTO (excessive monetary stimulus + Federal government spending).

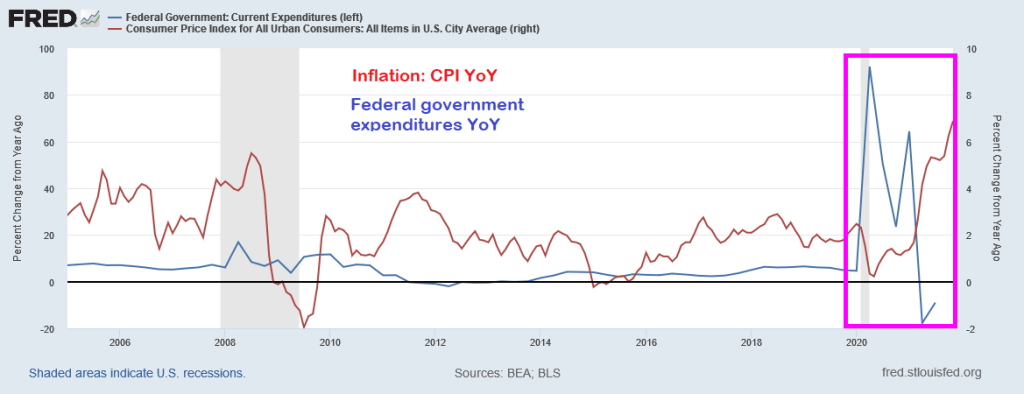

Here is the Federal government spending surge that helped generate the highest inflation in a generation.

So while the op-ed author blames inflation solely on The Federal Reserve, The Fed was unable to achieve its inflation goal for much of the post-financial crisis period. It was the double whammy of Fed monetary stimulus + Federal government stimulus (spending) that pushed inflation to 6.8%.

Following Paul Harvey’s “The Rest of the Story,” I choose baseball player Whammy Douglas to represent the double whammy of Fed + Fed government stimulus to produce inflation. THAT is the rest of the story.

Throw in the Biden Administration’s war on fossil fuels (driving up energy costs by over 50%) and we have a TRIPLE WHAMMY!!

The WSJ op-ed author was focused only blaming The Fed. Sorry, it was a Double Whammy.

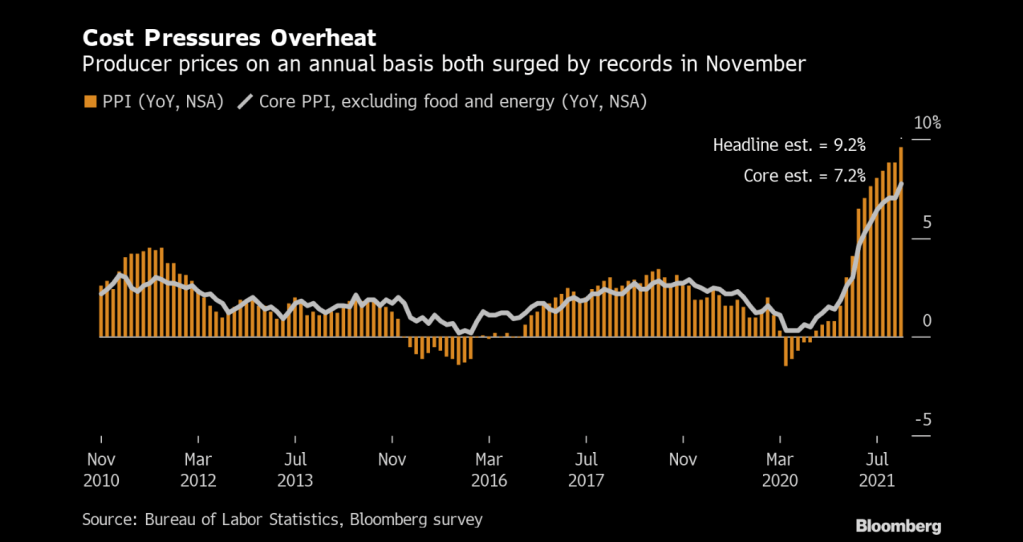

Prices paid to U.S. producers posted a record annual increase of almost 10% in November, a surge that will sustain a pipeline of inflationary pressures well into 2022.

The producer price index for final demand increased 9.6% from a year earlier and 0.8% from the prior month, Labor Department data showed Tuesday. Both advances topped economists’ forecasts.

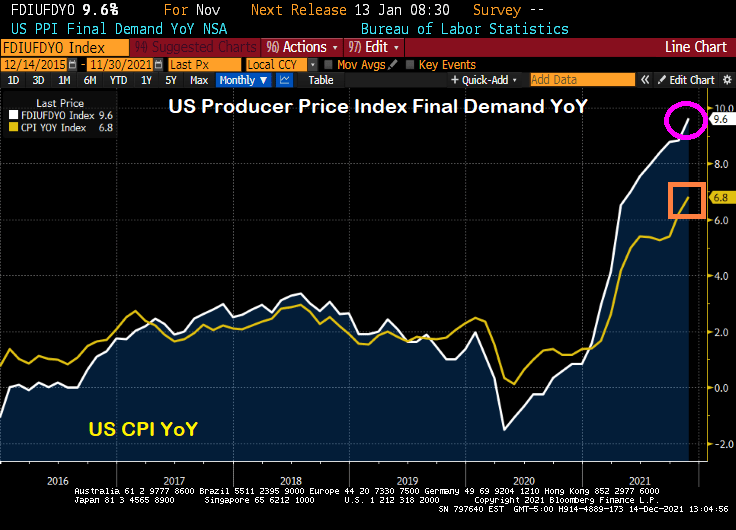

Even more interesting (or frightening) is that PPI Final Demand YoY is soaring faster than CPI YoY. If CPI catches up to PPI, then we have serious trouble.

With inflation seemingly growing out of control, Powell and Biden should sing “76 Trillion Dollars” which will be the US national debt after Biden and Congress get done with their spending splurge.

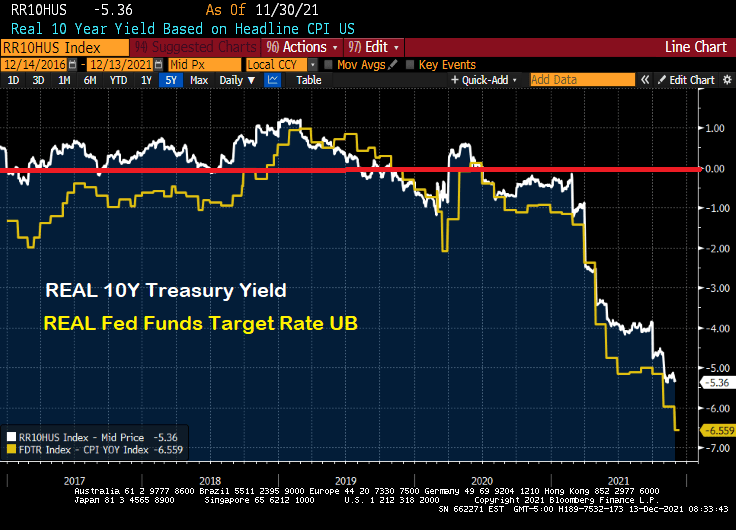

Inflation-adjusted return of Treasuries fell to lowest since the 1980s. For bond investors, this is their version of Kevin’s Famous Chili from The Office! Or The Fed’s Famous Chili!

(Bloomberg) — Treasury investors are losing more money than they have in four decades, once inflation is taken into account. And if markets are right, they’re unlikely to come out ahead for years.

The federal government’s debt has already lost about 2% outright over the past year as the Federal Reserve started removing pandemic-era stimulus from the economy and inched closer toward raising interest rates. But on top of that, the consumer price index has surged 6.8%, putting investors even deeper in the hole.

Taken together, that’s resulting in the worst real returns — or those adjusted for inflation — since the early 1980s, when then Fed Chair Paul Volcker was in the midst of fighting a wage-price spiral. What’s more, the dynamic isn’t expected to change: The bond market is projecting that 10-year Treasury yields will hold below the inflation rate for the next decade, meaning any investment income will be more than wiped out by the rising cost of living.

If we look at the REAL 10-year Treasury yield and REAL Fed Funds Target Rate, they are both negative.

Let’s see if Powell spills his famous chili on Wednesday at 2:00PM EST. The Fed keeps saying they are serious about controlling inflation, just like Kevin Malone.

The U.S. is poised to enter Year Three of the pandemic with both a booming economy and a still-mutating virus. But for Washington and Wall Street, one Covid aftershock is starting to eclipse almost everything else.

Already-hot inflation is forecast to climb even further when November data comes out on Friday, to 6.8%. That would be the highest rate since Jimmy Carter was president in the early 1980s — and in the lifetimes of most Americans.

And the CPI change since last year, according to the Federal Reserve of St Louis FRED is a staggering 16.262%.

And with U.S. Jobless Claims plunge to 52-year low, its about time that The Fed begins removing the humongous monetary stimulus.

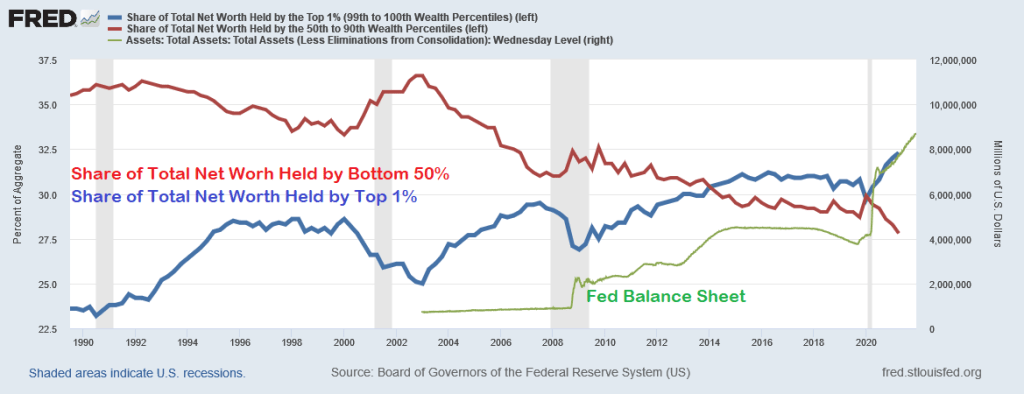

After all, largely thanks to Federal Reserve policies, we have seen the greatest wealth redistribution in US history … to the top 1%.

China cut the amount of cash most banks must hold in reserve, acting to counter the economic slowdown in a move that puts the central bank on a different policy path than many of its peers.

The People’s Bank of China will reduce the reserve requirement ratio by 0.5 percentage point for most banks on Dec. 15, releasing 1.2 trillion yuan (US$188 billion) of liquidity, according to a statement published Monday.

The reduction was signaled by Premier Li Keqiang last week when he said that authorities would cut the RRR at an appropriate time to help smaller companies, and is the second reduction this year.

The decision comes after recent data showed the economy and industry stabilizing, although Beijing’s tightening curbs on the property market have led to a slump in construction and worsened a liquidity crisis at developer China Evergrande Group and other real estate firms.

Evergrande’s ADR is collapsing (now 5.975) along with Evergrande debt falling to 23.12 (versus 100 par).

China’s credit impulse has nosedived (see pink box) as the PBOC drops bank reserve ratios to lowest level since 2007 in an effort to float the boat. Will the PBOC drop in reserve ratios stem the tide? Or is it peasant magic?

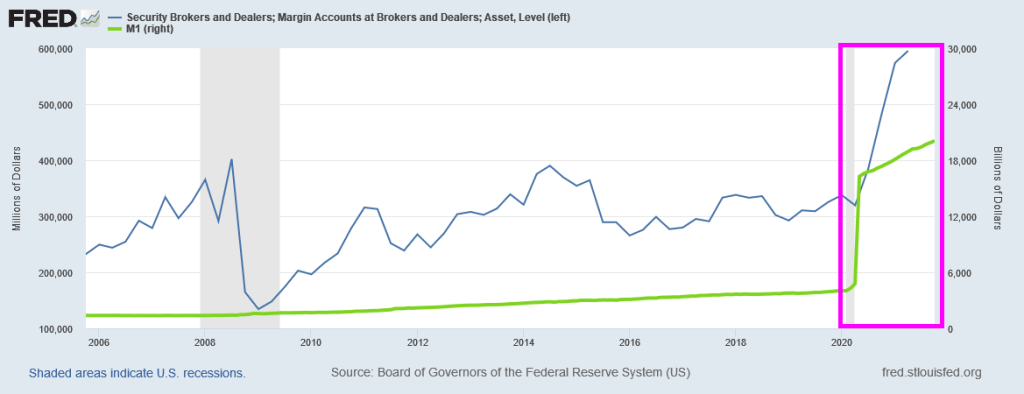

As we are all painfully aware, The Federal Reserve went on a 2nd money printing spree to allegedly stave-off the economic impacts of the COVID outbreak in March 2020. The first money printing spree took place in late 2008 as The Fed tried to stave-off the economic impacts of the housing bubble burst of 2008 and the ensuing financial crisis.

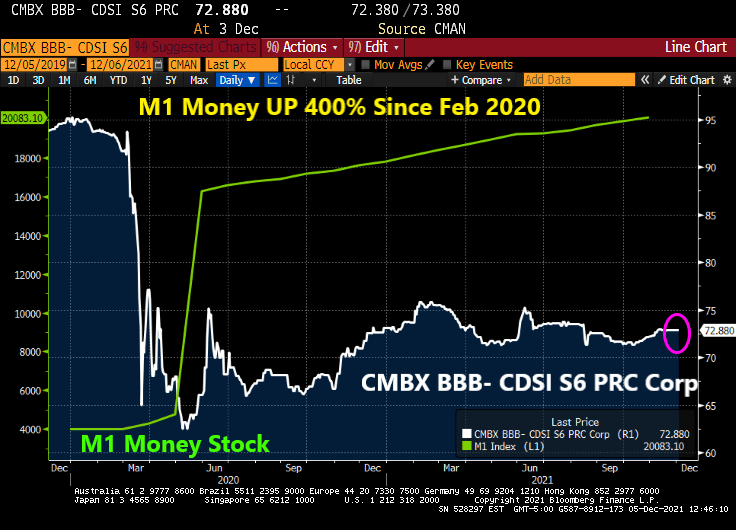

But for now, we have this horrifying chart showing the exploding margin accounts at security brokers and dealers (not, not the Walter White-type dealers, but Wall Street dealers). Notice the 400% surge in M1 Money stock after COVID struck.

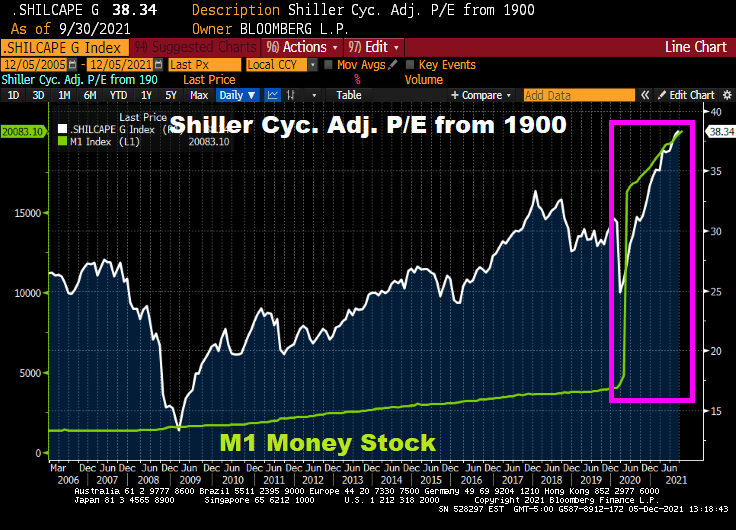

Of course, the soaring stock market is feeding the margin loop, encouraged by The Fed. Check out the Shiller Cyclically Adjusted Price Earnings (CAPE) ratio after The Fed’s M1 printing storm.

What can’t money printing fix? How about CMBS prices (or CMBX BBB- S6 prices … down 30.5% since just before COVID struck.

Let’s see if The Fed sucks the 400% growth back to zero.

Calamity Jay Powell is no longer mentioning “transitory” when it comes to inflation, but does Powell and the FOMC have the moxie to ACTUALLY raise rates more than a smidge??

(Bloomberg) — Team Transitory is throwing in the towel.

In a clear sign that the Federal Reserve is shifting to tighter monetary policy, Jerome Powell — who’s spent months arguing that the pandemic surge in inflation was largely due to transitory forces — told Congress on Tuesday that it’s “probably a good time to retire that word.”

The Fed chair, tapped last week for another four-year term, still thinks inflation will ebb next year.

But in testimony before the Senate Banking Committee, he acknowledged that it’s proving more powerful and persistent than expected, and said the Fed will consider ending its asset purchases earlier than planned.

A number of economists are forecasting cooling inflation next year, which gives Powell an excuse to NOT raise rates, other than just a bit.

For a little history, inflation was rampant in the 1970s and early 1980s. Fed Chair Paul Volcker, all 6’7 of him, raised the Fed Funds target rate (white line) to 20% on several occasions. The result? Inflation cooled from over 14% in 1980 to 2.46% by 1983. But since 2008, Fed Chairs Bernanke, Yellen and Powell have been the ANTI-Volckers … keeping the Fed Funds Target rate near zero for the the most part and adopted their gut-wrenching quantitative easing programs that are still here today.

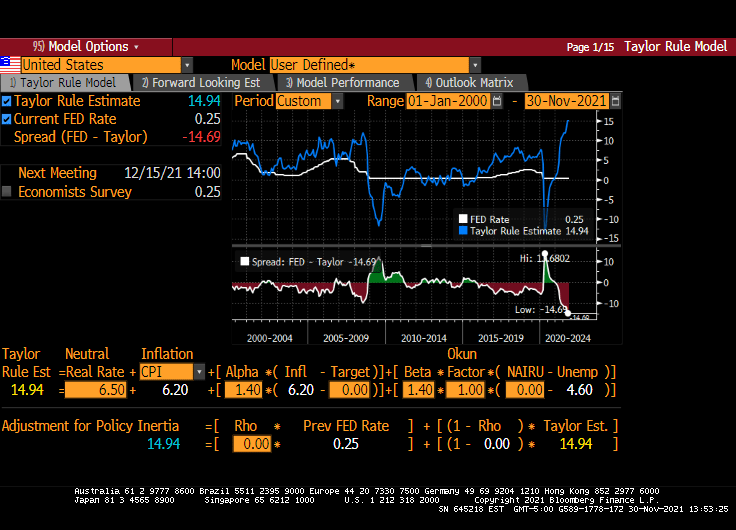

Of course, Powell could do what Volcker did (and the Taylor Rule suggests) and raise their target rate to 15% to cool inflation.

But does Powell and the other FOMC members have the moxie to really cool inflation? Frankly, no. Powell until yesterday played the TRANSITORY card and still believes that inflation will cool by 2022.

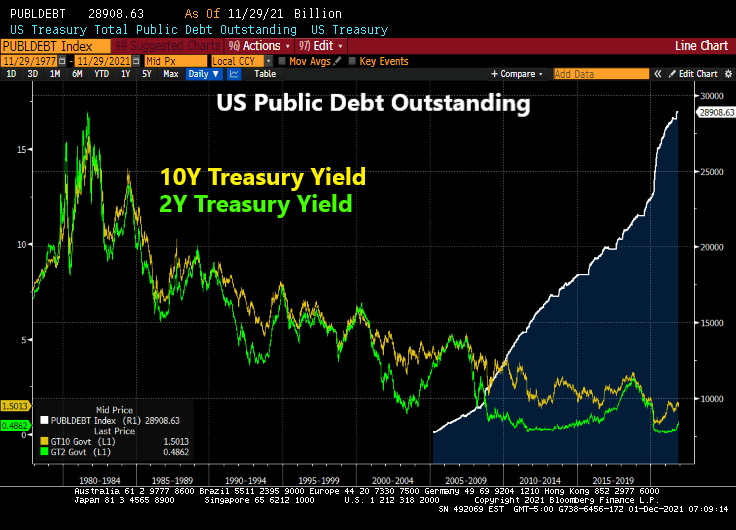

True, the Federal government has binged on borrowing (up 172% since January 2009). And with Biden and Congress trying to spend trillions more (much of which will be added to the public debt rolls, so increasing interest rates ala Volcker is very problematic.

And then there is always the good ‘ole excuse not to raise rates if needed. Other than admitting that The Fed is monetizing Federal government spending to which there is no end in sight.

You must be logged in to post a comment.