The delinquency rate on commercial mortgage-backed securities (CMBS) for offices spiked to 8.1% in July, the highest in 11 years.

The delinquency rate of office CMBS loans has QUADRUPLED in 1.5 years.

Delinquencies are currently rising at a faster pace than during the 2008 Financial Crisis. A top AAA-rated CMBS experienced a $40 million loss in May for the first time since the 2008 Financial Crisis.

While not an office, Edward Hopper painted some great real estate properties!

Kamala Harris, despite being VP for almost 4 years, is going to annouce her plans for taming inflation. Why doesn’t she do it now?? What Harris can’t control is The Federal Reserve that is losing money at breakneck speed.

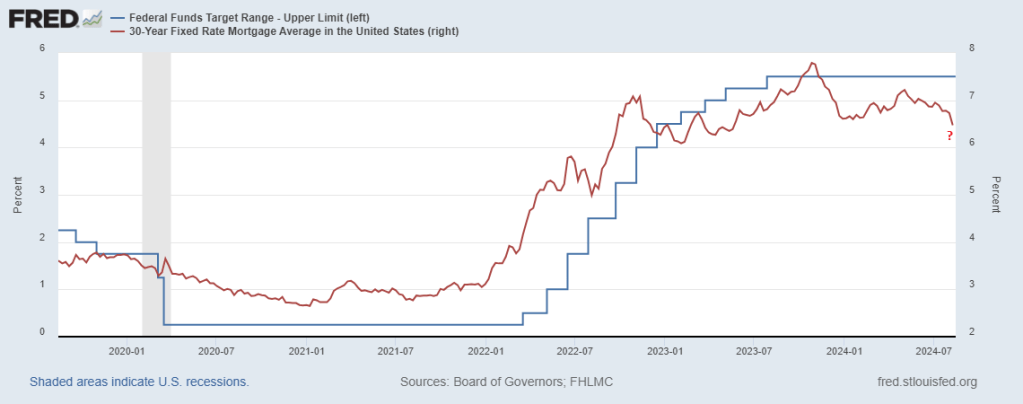

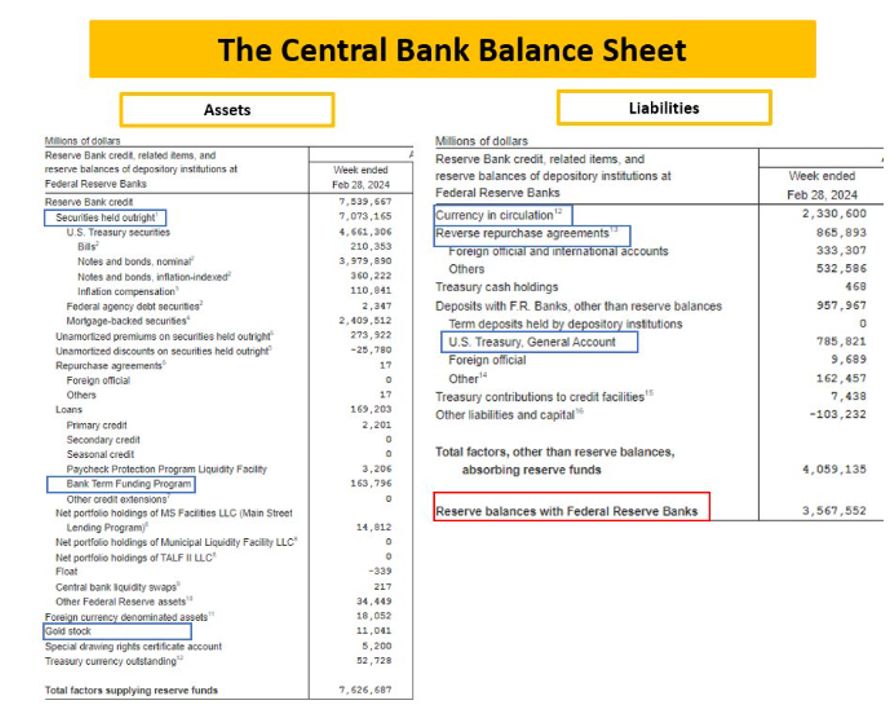

Here is The Fed’s balance sheet.

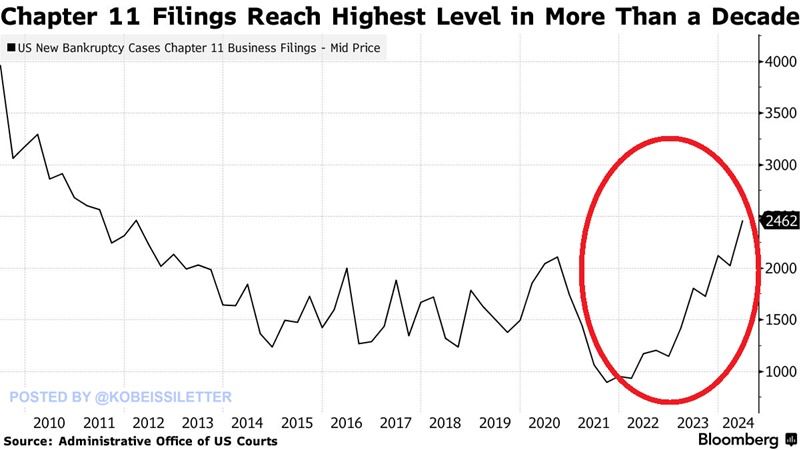

I shudder to think what Harris will propose to solve the highest bankrupty (Chap 11) rate in 13 years. Probably more Bidenomics (big wealth transfers to large corporations/donors).

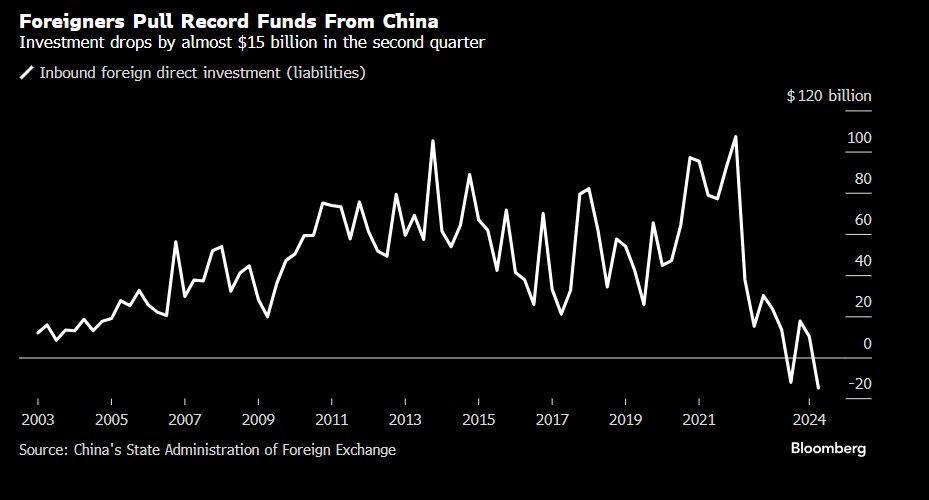

Meanwhile, foreigns pulled a record amount of funds from ailing China.

Kamala Harris will say anything to get elected, then fall back on her Communist agenda.

The slowing US economy has a silver lining: Treasury and mortgage rates are declining. And the is spurring faster mortgage prepayments.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending August 2, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 0.3 percent compared with the previous week and was 11 percent lower than the same week one year ago.

The Refinance Index increased 16 percent from the previous week and was 59 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.55 percent from 6.82 percent, with points decreasing to 0.58 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The deciine in rates led to an increase in MBS convexity.

Mortgage applications decreased 3.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending July 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Note the decline in mortgage purchase demand after Biden/Harris were sworn into office in Janaury 2021.

The Refinance Index decreased 7 percent from the previous week and was 32 percent higher than the same week one year ago. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) remained unchanged at 6.82 percent, with points increasing to 0.62 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Because of rising rates under Biden/Harris economic policies, mortgage refinancing demand has gotten crushed.

We are in the latter half of the year, so seasonalility will kill off purchase mortgage demand compared to the Spring and early Summer.

This scene from the film “McCabe and Mrs. Miller” sums up our political plight quite nicley. Politicians spend like crazy to stay in power (Biden/Harris) are excellent examples). Politicians promises endless money, then shoot the economy. The US is broke and relies on printing money and boowed funds to stay afloat. Harris wants to raise taxes on everyone to fund her plans like even MORE emphasis of failed green energy schemes and endless foreign wars. I doubt if Harris could defend her spending plans in light of the US already $35 TRILLION in debt.

Even more worrisome if thev fact that DC politicians have promised entitlements (Social Security, Medicare, etc. totalling $217.63 Trillion. Or 623% higher than the rapidly increasing national debt.

Biden/Harris raised thr national debt by 25% in less than 4 years. And Harris wants to increase spending! Harris wants illegal immigrants put on Social Security and Medicare, further bankrupting those entitlement programs.

Let’s see Harris explain her indefensible budget (like raising taxes and not hurting economic growth).

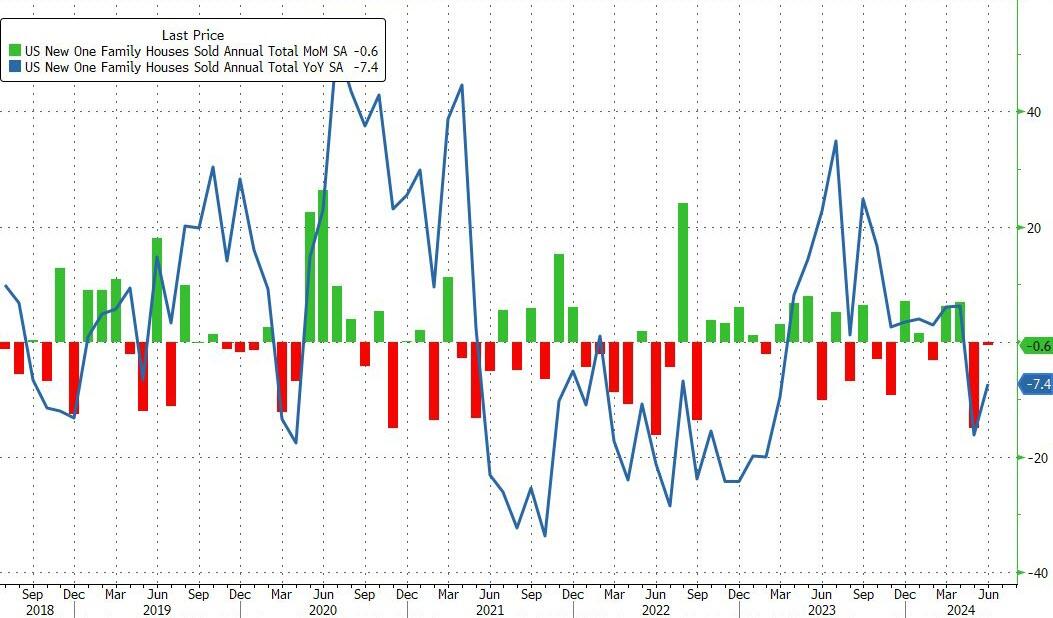

After a disappointing dump in existing home sales in June, new home sales just confirmed the slowdown, dropping 0.6% MoM (notably below the 3.4% MoM expected) and also saw a major downward revision in May from -11.3% MoM to -14.9% MoM. That leaves new home sales down 7.4% YoY…

Source: Bloomberg

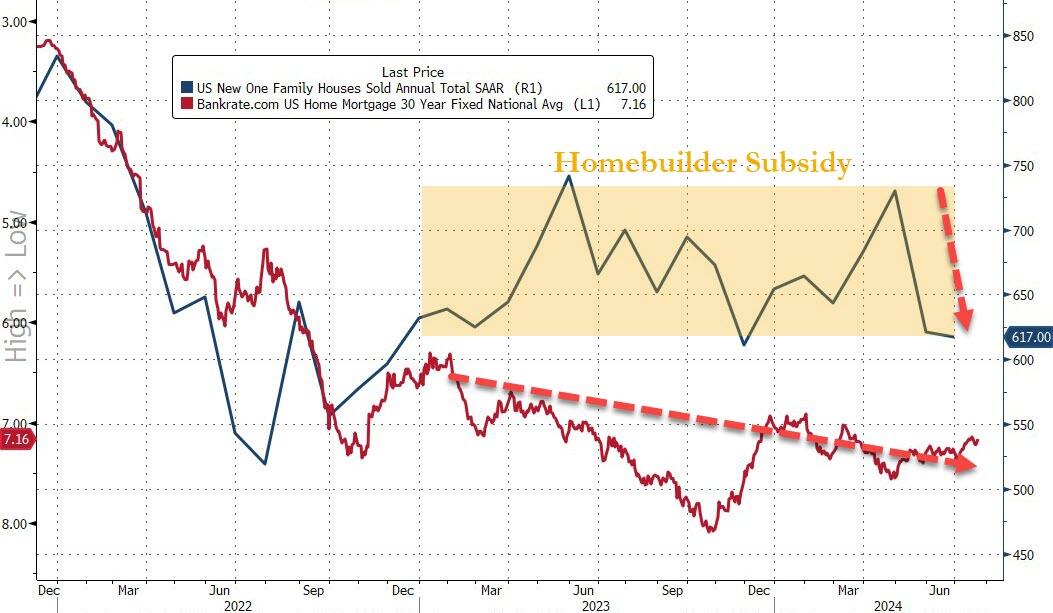

That shift dragged the new home sales SAAR down to 617k – basically unchanged since 2016…

Source: Bloomberg

While the median new home price rose in June, it remains below the median existing home price…

Source: Bloomberg

It appears the homebuilder subsidy fad is wearing off as mortgage rates show no signs of easing significantly…

Source: Bloomberg

Of course, none of this should be a surprise as homebuyer confidence has collapsed to an all-time record low…

Source: Bloomberg

Will cutting rates help?

Probably not. Bidenomics is now called Harrisnomics (or Cacklenomics) since Harris as VP was the tiereaker in the US Senate. So, she holds some responsibility for the outrageous, wasteful spending in Washington DC.

Here is a chart of Non-commerciak net positions for US Treasuries, currently showing more bailing out of Treasury positions. Has the world sours on DC’s fiscal train wreck and The Fed?

Of course, budget deficits are a disaster with Biden/Congress spending like drunken sailors in port and showing no signs of letting up. The good news? At least a court struck down Biden’s illegal cancelation of student debt (a desperate attempt to win votes). That would have spiked the budget deficit.

As I pointed out yesterday, the UNFUNDED entitlements promised by the Federal government are now larger than that total national assets (business, household). In other words, if the US liquidated ALL assets, they couldn’t pay off the UNFUNDED entitlements. And good luck taking away the entitlements!

President Biden was expected yesterday to propose a cap of 5% on annual rent increases for tenants of major apartment landlords, and he did. Whether it can happen is something else.

As the White House communicatedon Tuesday, the administration is looking for Congress to pass legislation for landlords with more than 50 units in their portfolios, that being the proxy for institutional owners, although it would also affect private investors, family offices, and others that might own at least that many units. According to administration calculations, the total pool would cover 20 million rental units.

The law would then give landlords a choice. They could either restrict annual rent increases to no more than 5% a year or they would forfeit the ability to take fast depreciation of rental housing. There would be an exception for new construction or “substantial renovation or rehabilitation.”

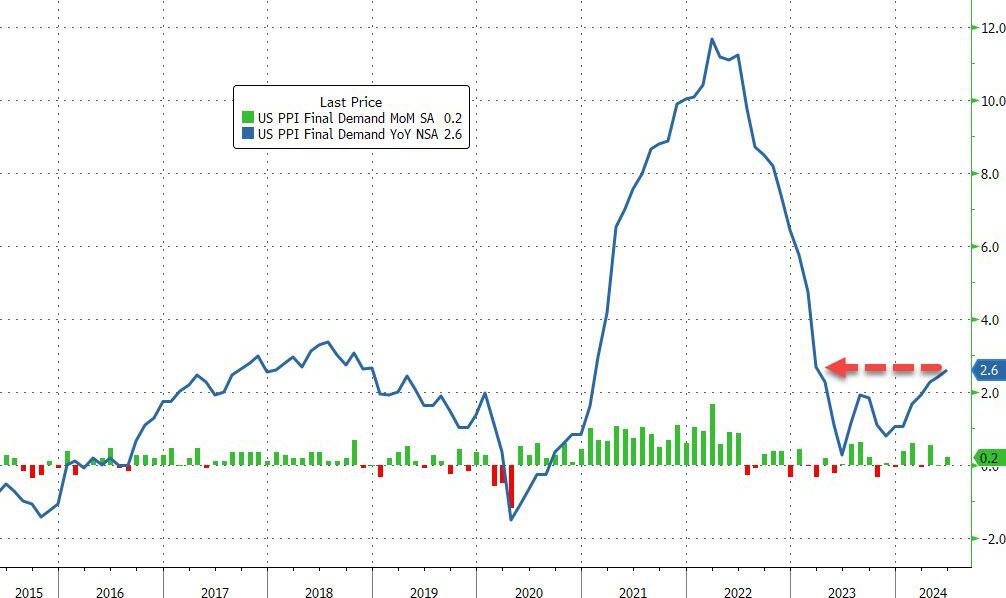

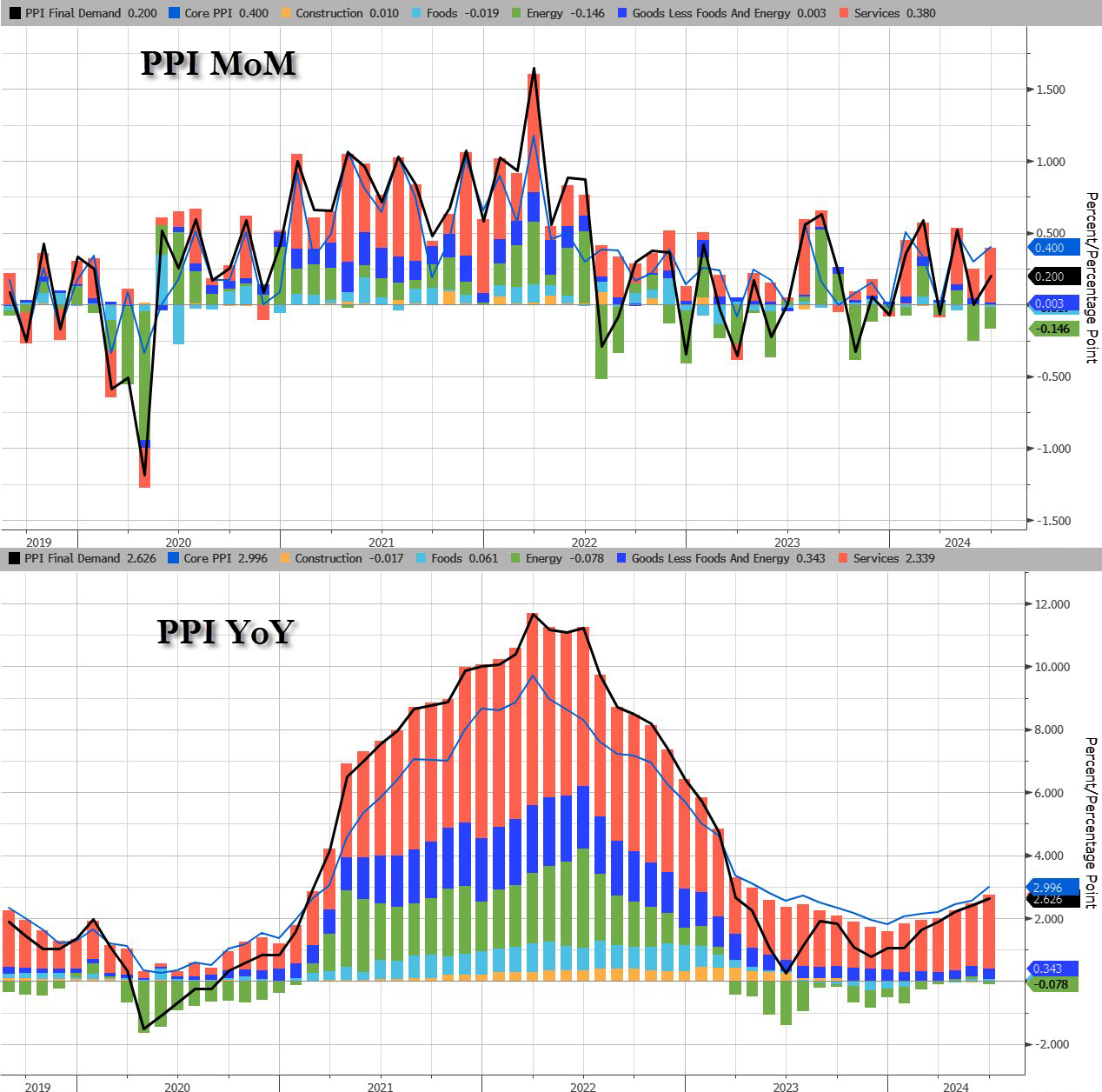

Core PPI rose by 0.4% MoM (double the 0.2% exp), sending the YoY price rise up by 3.0% (also the hottest since March 2023)…

Source: Bloomberg

The jump in PPI was driven by a resurgence in Services costs as Energy remains deflationary (for now)…

Source: Bloomberg

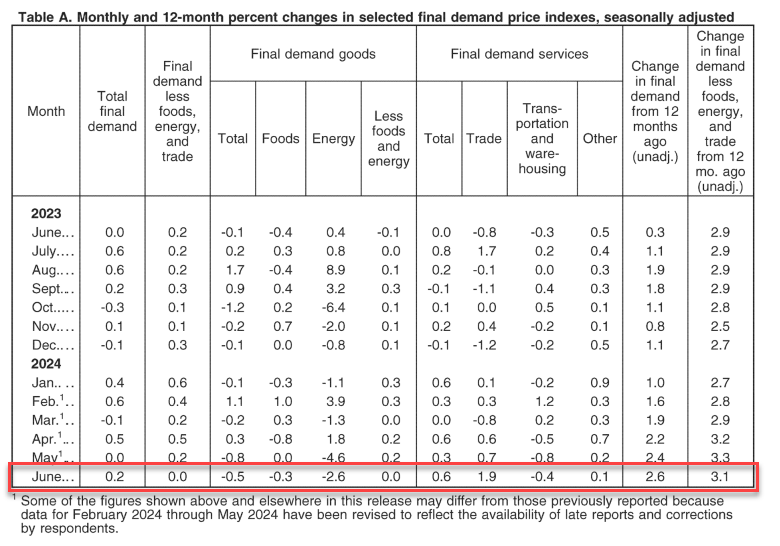

The June rise in the index for final demand can be traced to a 0.6-percent increase in prices for final demand services. In contrast, the index for final demand goods decreased 0.5 percent

Perhaps worse still, the pipeline for PPI (intermediate demand) is accelerating…

Source: Bloomberg

On the housing side, buying conditions for housing tanks to all-time low.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.